Ethena’s native token $ENA goes live today. Ethena is one of our highest conviction bets this cycle both at Delphi Ventures and personally, I believe:

Ethena’s native token $ENA goes live today. Ethena is one of our highest conviction bets this cycle both at Delphi Ventures and personally, I believe:

- sUSDe will offer the highest dollar yield in crypto at scale

- USDe will become the largest stablecoin outside of USDC/USDT in 2024

- Ethena will become the highest revenue generating project in all of crypto

In this post, I’ll cover what Ethena is, why it’s interesting, as well as breaking down the risks as I see them.

The Opportunity

Stablecoins are still undeniably one of crypto’s killer apps.

The market has repeatedly shown it wants yield on stables. The issue is generating it in an organic, sustainable way.

Ethena is able to provide this yield with the byproduct being a stablecoin. The stablecoin captures the yield while the capital used to mint the stablecoin generates it.

Specifically, the capital used to back the stable is placed into a delta neutral exposure of Long Staked ETH and Short Eth perp, with both legs of the position typically providing a yield.

sUSDE yield = stETH yield + funding rate (currently 35.4%)

In this way, Ethena effectively combines the two largest sources of “real yield” in crypto: ETH staking (~$3.5b/year) and perp basis funding (~$37b/year in OI between ETH/SOL/BTC, earning an avg of ~12%).

This is an implementation of Arthur Hayes’s original idea of a “synthetic USD”. While delta neutral positions like this have previously been attempted (e.g. UXD), they’ve never before been able to tap into centralised exchange liquidity.

Ethena and the stablecoin trilemma

Before digging into the design and its risks, it’s worth providing a brief summary/history of stablecoin designs and where they fit into the stablecoin trilemma.

There are 3 popular forms of stable coins: Overcollateralized, Fiat Backed, and Algorithmic.

They each address various parts of the stablecoin trilemma (i.e. the inability to be simultaneously Decentralized, Stable, and Scalable/Capital Efficient) but ultimately fall short in addressing all 3.

Fiat Backed (USDC, USDT)

- StabIlity: Authorised participants (i.e. market makers) can mint and redeem them to arb price and ensure they maintain peg

- Scalability: They’re 1:1 collateralised so they’re scalable + capital efficient

- Decentralisation: Highly centralised, meaning holders face both counterparty risk (bank solvency, asset seizure, etc) and censorship risk as legal entities can be coerced and bank accs frozen

Overcollateralised (DAI)

- Stability: Anyone can mint and redeem for underlying collateral and arbitrage the price, creating stability

- Scalability: Struggles on scalability side since it mostly exists as a byproduct of the demand for leverage.This is further worsened by the superiority of Aave and other products when it comes to this functionality

- Decentralisation: Highly decentralised when compared to alternatives, although there’s some reliance on both centralised stablecoins and treasuries as collateral

Algorithmic stablecoins (RIP)

- Scalability: Algorithmic stablecoins are highly capital efficient and scalable as they can be minted without exogenous collateral, and generally pass on some form of yield/rebasing to participants when demand exceeds supply

- Decentralisation: They’re also decentralised in that they tend to rely only on crypto-native collateral

- Stability: However, they fail miserably on stability as they’re backed only be endogenous collateral, which leads to reflexivity and eventual collapse via death spiral. Every algorithmic stablecoin ever tried has suffered this fate

Enter Ethena’s USDe

In my view, USDe is the most scalable fully collateralised stablecoin ever created. It’s not fully decentralised, nor can it ever be, but imo it nevertheless sits at a very interesting point on the tradeoff spectrum.

Stability

USDe is fully collateralised by a delta neutral position that consists of a long staked Eth spot position offset by a short Eth perp position. Authorised participants can redeem the stablecoin for the underlying collateral, which should lead to stability. That said, this is a new design and there are clearly risks (more on this later). It’s also unlikely to ever be as stable as fiat-backed stables, given redemption costs for those are free whereas USDe redemption cost will rely on liquidity conditions at the time (i.e. cost to unwind shorts).

Scalability

This is where USDe really shines for two main reasons. Firstly, like fiat-backed stables, Ethena can be minted 1:1 with collateral. However, unlike fiat-backed stables, Ethena is able to generate meaningful organic yield at scale for its holders. Specifically, USDe can be staked into sUSDe to capture the protocol yield, which is a combination of stETH yield and funding rates (i.e. demand for leverage).

sUSDE yield = stETH yield + funding rate (currently 35.4%)

Crucially, this yield is likely to be: a) scalable and b) counter-cyclical to treasury rates.

On scalability: Ethena effectively combines the two largest sources of “real yield” in crypto:

- ETH staking: ~$3.5b/year

- Perp basis funding: ~$35b/year in OI between ETH and BTC (coming this week), earning an avg of ~11% over last 3 years

This is likely to be much higher during a bull market as we’ve seen over the last 3 months where funding has averaged ~30%.

Ethena can also eventually add other assets like $BTC ($25b OI) and $SOL ($jitoSOL?) over time to further scale supply.

On counter-cyclicality: As treasury yields likely trend lower over time, demand for crypto leverage should go up as ppl go further out on the risk curve.

Ethena’s yields should remain high as treasury-backed competitors compress.

Decentralisation

Decentralisation is a multi-dimensional spectrum, and overall assessments will depend on how heavily you weight each of the dimensions. Personally, I’d say Ethena sits somewhere between fiat-backed and overcollateralised stables in terms of decentralisation.

It’s more censorship-resistant than fiat-backed stables in that there’s no dependence on traditional banking rails which ultimately rely on the fed via correspondent banking and can be shut down overnight. Arthur describes this well in his recent blog post.

However, it does face some counterparty risk with CEXes. Specifically, Ethena holds collateral off exchanges in MPC wallets with institutional grade custodians, which are then mirrored onto CEXes using Copper, Ceffu and Cobo.

Settlement happens every 4–8hrs, reducing counterparty risk with exchanges to the accrued profit of the short leg of the trade between settlement periods.

More importantly, unlike overcollateralised stablecoins which can be minted/redeemed permissionlessly on-chain, Ethena relies on calling an off-chain server to compute venue with the most efficient funding rate and mint USDe. This is a undeniably a centralisation vector which makes it vulnerable to censorship.

Profitability:

Unlike most other projects in crypto, Ethena is also insanely profitable. It has risen to become the most profitable dApp in crypto, eclipsing all of DeFi and sitting behind only Ethereum and Tron in 30d revenue generated.

Ethena’s profitability is expected to come from a take rate on the total yield generated. Right now that is going to the insurance fund, but eventually one expect this to be distributed to stakers.

Assuming a 10% take rate, Ethena’s protocol rev is:

Total Yield * (1–90% * (1 — sUSDe Supply / USDe Supply))

It’s worth noting that Ethena’s profitability is higher right now due to the shard campaign, as the staking rate is only ~30% due to point incentives for locking USDe. I’d expect this to increase post shards.

This dynamic also highlights why it’s so beneficial for USDE to succeed as a stablecoin. The more USDe is used a stablecoin, the less USDe is staked, and the more profitable Ethena is.

Risks

The most common FUD I’ve seen people focus on is funding risk i.e. what happens if funding flips negative for prolonged periods? Will we see a UST-like unwind/blow-up?

In response to this, it’s worth pointing out:

1) Funding has historically been highly positive.

2) There’s an insurance fund (IF) to cover periods of negative funding.

3) Most importantly, even in worst case scenarios where funding is negative for an unprecedented period of time and the IF is fully depleted, USDe is fully externally collateralised and has some level of “anti-reflexivity” built into the design, making it very different from UST.

1) Historical funding

Funding has historically been positive, especially when accounting for the Eth staking yield buffer. Over the last 3 years:

– funding averaged positive ~8.5% on an OI weighted basis

– funding net of staked ETH yields has only been negative on 11% of days

– max 13 consecutive days of negative funding vs 110 days positive

See this and this from Ethena contributors for some good data-driven analysis on this:

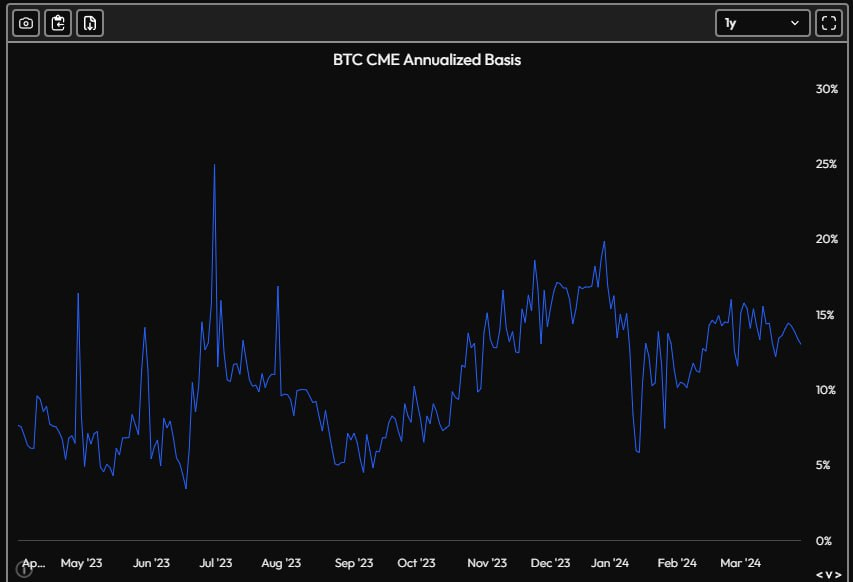

There also may be reason to believe funding will stay structurally positive long-term. Some exchanges (Binance, Bybit) have positive baseline funding rates of 11%, meaning if funding is within a certain range it snaps back to 11% by default. These exchanges make up >50% of OI. Even when we look at TradFi, CME Bitcoin futures are bigger than Binance and are currently yielding ~15%. In general, futures yield basis is positive the vast majority of the time as a proxy for the cost of capital.

2) Insurance Fund

When funding does flip negative, there’s an insurance fund in place which serves to subsidise sUSDE yield and ensure it’s capped at 0 (i.e. never goes negative).

A portion of protocol revenue will be redirected to the IF to ensure it grows organically over time. The IF has been bootstrapped with a $10m contribution from Ethena Labs.

It’s sitting at $27m and currently all protocol revenue is being sent to there (~$3m/week at current run-rate).

Both Ethena team and Chaos Labs have done extensive research into figuring out the optimal size for the IF (links below).

Their recommendations came in at between $20m — $33m per $1b of USDE supply.

3) Anti-reflexivity

Now, let’s assume a scenario where funding yields are negative enough to outstrip stETH yield and prolonged enough to drain the insurance fund.

In this case, the principal balance of the stablecoin will slowly erode below $1 as funding payments are made from collateral balance. While this sounds bad, the risk here is very different from algostables in that collateral slowly erodes over time rather than rapidly and violently collapsing to 0.

E.g. the max negative funding rate on Binance of -100% would imply a loss of 0.273% per day.

As Guy points out, this exogenous funding rate actually embeds “anti-reflexivity” or negative feedback loops into the design.

Yield goes negative → users redeem the stablecoin → shorts are unwound → funding mean reverts back above 0.

Redemption of the stablecoin helps balance funding rates and bring the system back into equilibrium.

This is the opposite of algostables where redemption tanks the price of the share token and creates the positive feedback loop which makes up the so-called “death spiral”.

Two additional things worth noting:

1) Any unwind will likely not happen suddenly when yields turn negative, but rather gradually as yields come down over time. Why hold USDeE if you can get the same yield from treasuries?

2) the insurance fund is a design choice made to optimise UX for sUSDE holders by smoothing out yields and avoiding them having to worry about principal loss day to day.

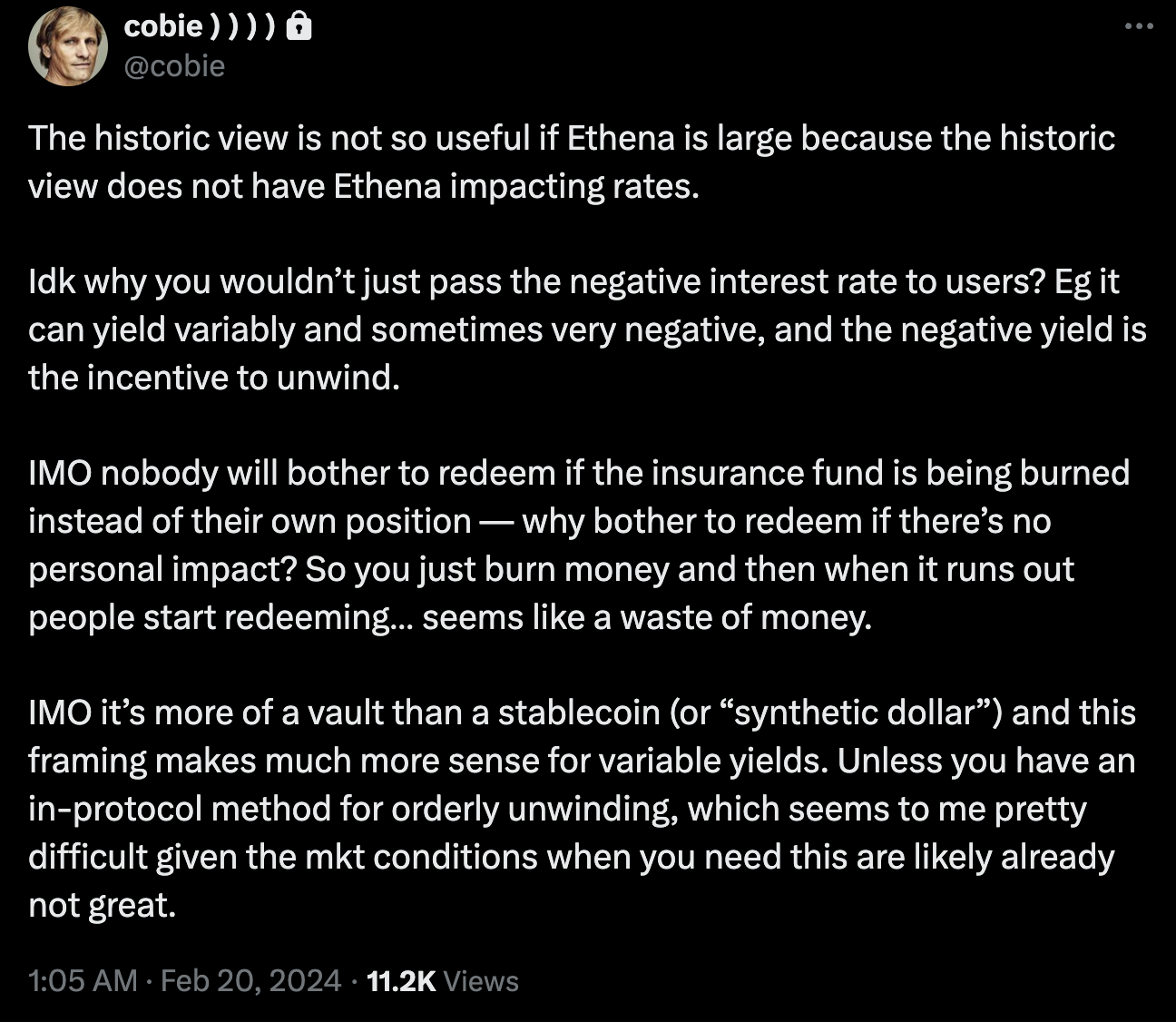

Ethena could instead choose to pass on negative yields to holders as Cobie suggests below, which would make the negative feedback loop even stronger by encouraging ppl to redeem quicker in response to changes in funding.

Other risks

While I don’t think negative funding is a particularly big risk, there are definitely plenty of other risks to think about. After all, this is an entirely new mechanism offering very high yield. No yield is without risks, and the higher the yield the more sceptical one should be. The below is a non-exhaustive list of risks and mitigants as I see them:

1) Historical funding rate data doesn’t include Ethena itself. If USDe gets sufficiently large vs overall OI, it could: a) meaningfully bring down average funding rates b) exacerbate funding rate vol which could lead to violent unwinds, bad execution and potential USDe depegs.

Relatedly, stETH yields are also likely to continue come down over time, further hurting the economics and making the above problem worse.

This is definitely a risk. A few mitigants:

a) There’s a 7 day delay on unstaking sUSDe which should help mitigate the magnitude of the panics as a lot of the supply will be staked.

b) Even in the worst case this depeg shouldn’t affect protocol solvency too badly, since the spread is passed on to the authorised participants redeeming. It would mainly harm the users redeeming at a loss and, more significantly, the protocols/users levering up on USDe.

2) LST collateral is relatively illiquid, and could get slashed and/or depeg. A sufficiently violent depeg could lead to Ethena getting liquidated and realising losses.

However, given Ethena uses limited to no leverage, only an unprecedented depeg would cause liquidation.

According to Ethena’s own research, this would require a 41–65% depeg of the LST vs ETH, with the highest depeg ever being ~8% on stETH in 2022 (see worked example in link).

Ethena also diversifies its LST exposure now which further mitigates this and only holds 22% of its collateral now in LSTs, with ETH making up 51% currently. stETH yields of 3 / 4% become less relevant when funding is +30% in a bull market, so Ethena will likely hold more ETH in bull markets and more stETH in bear markets.

3) Ethena has credit risk to CEXes on the short leg of the trade. A counterparty blow-up could mean: a) Ethena ends up net long instead of delta neutral b) USDe depegs based on its pnl exposure to the specific counterparty.

However, Ethena settles with CEXes every 4–8hrs, so they’re only exposed to the difference between two settlement periods. While this could be large during a fast violent market move, it’s not the same as being exposed to the entire notional amount.

Also worth noting that all stablecoins have some level counterparty risk, as we found out w/ USDC last May.

4) That said, all the above risks can get amplified and systemic once we start adding in USDe looped leverage.

This will definitely lead to some panics, liquidation cascades and USDe depegs. As mentioned above, this is likely to be more destructive to users and protocols that compose with USDe, rather than Ethena itself. However, in extreme cases it could also hurt Ethena.

The only way to repeg is to redeem for the underlying, unwinding shorts and potentially leading to large losses if liquidity is thin.

5) Ethena Labs and associated multi-sigs have control of assets (currently a ⅔ Multi-sig with Ethena, Copper, and an independent third party).

Theoretically, they could take out leverage against them off-chain or otherwise encumber them.

USDe holders have no legal rights and would have to fight this out in courts with no precedent to rely on.

6) Ethena could also get hit with an injuction and asked to freeze assets by a regulator, which would then indirectly control a bunch of ETH/stETH.

7) Finally, there are also likely a lot of unknown unknowns.

Ethena is effectively operating as a tokenised hedge fund in the back-end. This stuff is hard, there are a lot of moving parts and ways that things could go wrong. Don’t put in more than you can afford to lose.

Everything in crypto has risks, as we’ve found out repeatedly the hard way. Imo, the important thing is to be as transparent as possible about the risks and allow individuals to make their own decisions.

I’d say the Ethena team has generally done a good job of this, with some of the most comprehensive documentation and risk disclosures I’ve seen for an early stage project.

For my part, I have a lot of my personal stables in Ethena since before the shard campaign, bought a bunch of USDE/sUSDE Pendle YT, and also invested through Delphi Ventures. As you can probably tell by now, It’s one of the projects i’m most excited for this cycle.

I continue to think stablecoins are a $100b opportunity. Ethena strikes a very interesting point on the stablecoin tradeoff spectrum, and it’ll be hard to compete with its yield at scale.

I also consider Guy one of the best founders we’ve backed, who in a little over a year has taken Ethena from an idea to the fastest growing dollar-denominated asset in crypto of all time w/ $1.5b TVL.

In this time, he’s assembled a rockstar team to build out his vision, and surrounded himself with some of the best backers in the space (tier 1 CEXes, VCs, market-makers, etc). Very excited to see what he can do over the next few years.

Thanks to Yan Liberman for helping me brainstorm this post and put it together, to 0xDef1, Jordan and Conor Ryder for reviewing and Guy Young for answering all my dumb questions.