Introduction

Our fund thesis is entirely premised on the Internet Financial System. It is our Kierkegaardian idea to live and die for, and we often find ourselves attempting to explain the promise and meaning of the Internet Financial System to our friends and investors. It’s a difficult task because so much of the existing financial system is abstracted away from consumers — especially consumers in the first world who are content with existing financial infrastructure — and so much of what we are attempting to build is still in the conceptual and esoteric future. This article compiles a few of our best hits in an attempt to help you explain the Internet Financial System to your friends, family, and customers.

We are collectively building the Internet Financial System (IFS) — a better financial system on the cloud that can hold the world’s assets and provide financial services to 8 billion people. We believe the Internet Financial System is a paradigm shift in global financial activity like Gutenberg’s printing press was a paradigm shift in the production and dissemination of knowledge.

0. Unified Servers and Smart Contract Code

I will ask you, dear reader, to bear with me as we cover the two fundamental differences between the existing and Internet financial systems. This is the most technical part of the essay. If you find yourself tuning out, please skip ahead.

You may think the financial system already operates on the Internet because you can access a bank or brokerage service online, but the Internet is only an interface for you to send orders as you would to a pizza delivery restaurant. The pizza is not made on the Internet, and neither is your financial transaction. The existing financial system operates through a patchwork of siloed servers. There are over 90,000 financial institutions around the world, and most of them use internal servers that cannot be accessed from the outside. Your bank loan is just an entry into one of these servers. Any asset you hold — anything you own or owe — within the global financial system is an entry into one of these siloed servers. If you own a home in the US, you may be aware that your ownership is registered with federal, state, and local servers, and only a small group of permissioned administrators can send transactions to these servers. This is what we call the permissioned, siloed server problem.

Financial institutions use standards like SWIFT and ACH to communicate when sending transfers and sharing data. Still, these standards require several steps and manual oversight because of the disparity in underlying databases. When communicating between financial institutions across borders, you need local government institutions like central banks and international institutions like the Bank of International Settlements. The process is an expensive, cumbersome, and slow morass of paperwork and well-paid employees. This is the high transaction cost problem associated with permissioned, siloed servers.

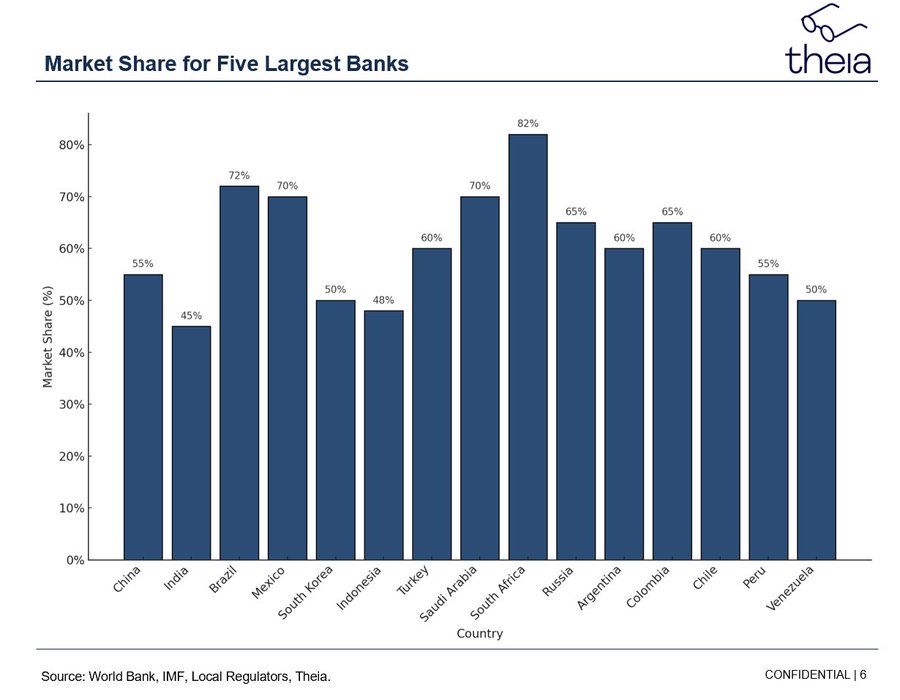

Two additional problems come from building a financial system on permissioned servers. The first is that it is difficult — really difficult — to start a financial services business. You need to find a gatekeeper who will allow you to post transactions to the web of permissioned, siloed servers we call the global financial system. Expect to pay them well. This is the problem of high barriers to entry for financial startups. There is a related problem where financial institutions have privileged permissions over entire regions. Three banks control over 50% of Colombia’s market share, and you need to work with them to lend money to a Colombian business. Market structure rhymes across most emerging economies. Every country has local financial institutions that act as gatekeepers for opportunities within their borders, and they use this privileged position to extract rents. This is the problem we refer to as the local banking oligopolies problem.

Notice that until now, we have explained the permissioned, siloed server problem and how it leads to burdensome transaction costs, high barriers to entry for startups, and local banking oligopolies.

There are high barriers to entry to building financial start-ups in permissioned server systems

Most nations have a few financial institutions that can act as gatekeepers to local opportunities

Let’s now consider one of the core strengths of Internet finance: code that can make commitments. This is the foundation of smart contracts. Chris Dixon compares smart contract code to a vending machine in which you input a dollar and receive a Coca-Cola. Smart contracts allow you to write code that responds to inputs in predetermined ways. A smart contract can release a

...