Stablecoins are often cited as “crypto’s killer use case”. However, this framing lacks nuance. It is important to distinguish between two unique use cases:

- Oiling the cogs of DeFi/CeFi – settling trades, denominating trading pairs, collateral on money markets etc.

- Serving as a monetary asset – payment for goods and services, cross-border payments/remittances, monetary safe haven etc.

Historically, the former use case has been the principal driver of stablecoin growth. Consequently, stablecoin supply has been inherently tethered to the growth of crypto’s speculative casino. While this can certainly drive demand during favorable macro environments, supply inevitably contracts as soon as the macro tides turn.

However, this seems to be changing.

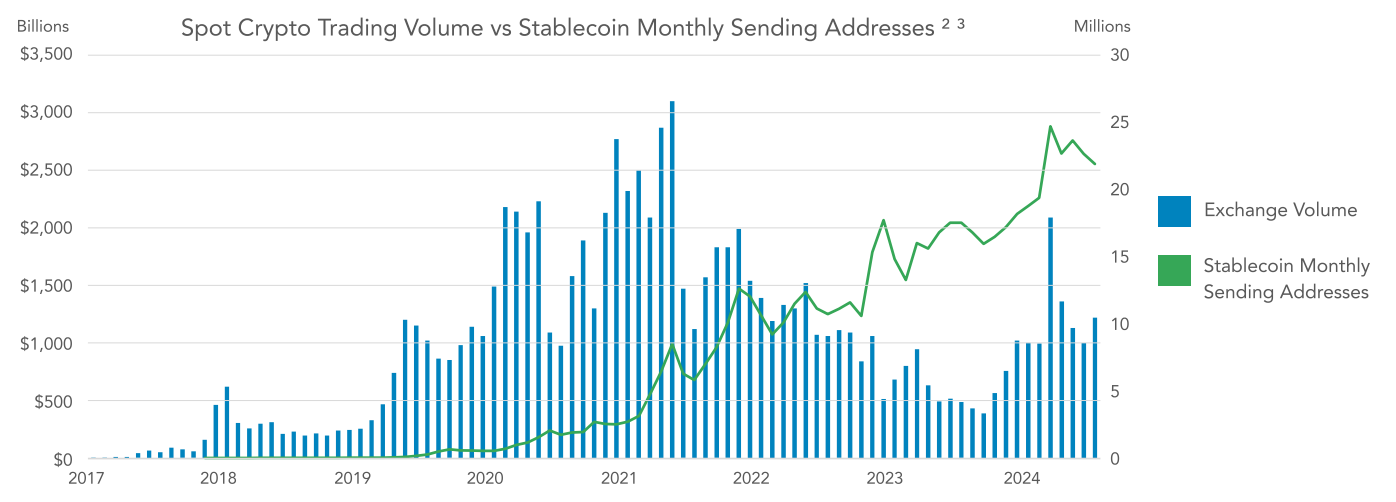

Source: Castle Island Ventures

Source: Castle Island VenturesDespite crypto exchange volume failing to bounce back from all-time highs, monthly addresses sending stablecoins continue to climb up and to the right. In other words, we have begun to see the real “killer use case” for stables — serving as a monetary asset – increasingly find PMF.

This has two notable downstrea

...