💰$100 Swaps

Daily active addresses on Uniswap are spiking to levels not seen since May 2021.

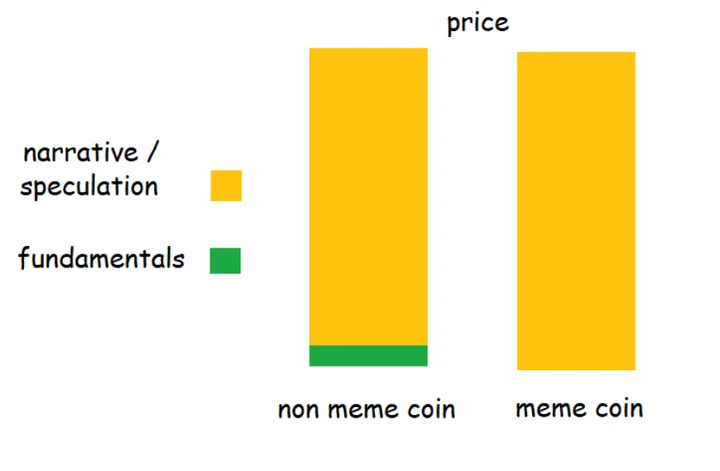

Why is this? Well, one of the main reasons is meme tokens, of course. The current rally’s poster boy, PEPE, has rallied nearly 100,000% over the past month to hit a peak market cap of nearly $2B.

Meme tokens are essentially coins whose main value proposition is the community that rallies around them. An argument can be made that this phenomenon applies to more than just memes in crypto… but that’s a newsletter topic for another week.

PEPE’s run has fueled massive speculation, most of which has been happening on-chain. As traders fight one another in PvP markets, they also find themselves competing with one another in the global Ethereum fee market. Ethereum users are forced to bid against one another for transaction prioritization in Ethereum’s limited block space. As on-chain activity increases, these bidding wars can get quite extreme, pushing fees to the stomach-churning heights we had grown accustomed to back in the glory days of 2021.

Luckily, this time around Ethereum has layer-2s to provide traders with cheaper fees and free themselves from the shackles of Ethereum layer 1 fees… right?

Despite considerable rise in layer-2 activity, Ethereum remains home to the highest volumes, deepest liquidity, and richest ecosystem. Thus, Ethereum hosts unparalleled network effects with arguably the strongest moat in crypto. This creates somewhat of an oxymoron where users claim that Ethereum needs cheaper fees, while spiking ETH fees simultaneously serve as proof that participants are willing to pay those fees to use the chain.

It’s crucial to remember that $100, or even $10, is not a realistic transaction fee for the average person. With these fees, crypto won’t scale past on-chain speculation. As market participants bid up ETH layer-1 fees, that impact is felt by all users that rely on Ethereum for transaction settlement, including layer-2s.

L2s “roll up” transactions into a single transaction, which is then settled on Ethereum (the layer-1). While gas costs are reduced significantly, the end result depends on the current state of Ethereum’s fee market. Currently, L2 fees are spiking to hit $1. Later this year, EIP-4844 will launch and can potentially reduce L2 fees by ~90%. But even with this drop, it’s not difficult to imagine L2 fees re-visiting these prices in a future crypto mania.

In a world where ETH fees are high, and L2 Uniswap Transactions cost $1, or even $0.50, it’s important to ask ourselves if this is good enough. For Ethereum L1, proponents will claim this is fine as Ethereum is optimized for security and not meant to be a transaction layer. Plus, high fees on Ethereum now burn ETH, turning it into a deflationary asset.

For L2s, this seems to work as well as they increasingly become the transaction layer. We’ve seen the use cases that low fees can unlock, especially with the rise of perpetual exchanges, notably GMX on Arbitrum.

L2s are in an amazing position, as they make money from fees while creating a profitable business model. They seem to have found their sweet spot where fees are low enough to attract users (along with token incentives) but high enough to generate revenue.

Intuitively, fees should have an inverse relationship with blockchain usage and use cases. The lower the fees, the greater the potential for activity.

Delphi analyst Ceteris dives into this in a recent Alpha Feed post: Are High ETH Fees Bullish or Bearish? Delphi Starter members can read more posts from Ceteris on our Alpha Feed here. Here’s an edited snipped:

“Market makers (MM) are often placing and canceling orders every block, and for a central limit order book exchange, you need sub-second block times. Let’s use 500ms as an example: with $0.10 fees, to place/cancel an order every block would be 172.8k tx’s/day for a single MM on a single market. With $0.10 fees this would cost $17,280/day, just for the privilege of placing orders. In the long-run Ethereum will add more data availability throughput with danksharding but the point remains, with any meaningful amount of activity, especially when we get into a bull-market, use cases will be priced out.”

Right now, fees are the premium you pay to participate in the on-chain economy. Normally, market conditions that create demand for low fees are the same conditions that warrant fee premiums. But, the current environment is attracting users that don’t necessarily value or respect fundamentals. Prices are going up, but this isn’t being reflected amongst the fundamentally attractive coins that tend to populate the bags of crypto’s biggest backers and builders. This creates a rare moment in time for anybody that is truly in crypto for the tech to take a step back and acknowledge just how important fees are.

Low fees are critical for creating an on-chain experience worthy of retaining the masses. One day, our children will laugh at us for paying exorbitant fees, but we’ll look back on these times with nostalgia for paying $100 swaps.

🔥 Meme of the Week

📚 Delphi Reads

Liquidity Book by Trader Joe is starting to host token launches to bootstrap liquidity. With Liquidity Book, projects can conduct fair launches by depositing single-sided token liquidity across a wide range and letting the market decide what the price should be.

Bitcoin fees (quite the theme for this edition!) have been skyrocketing to the dismay of many maximalists. Ordinals and BRC-20s are driving this disruptive catalyst with no end in sight. While not exactly innovative, Bitcoin NFTs seem to have organic network effects within the BTC community. Here is a great explanation on them by ChainLinkGod.

Foobar walks us through how not to get sandwich attack as jaredfromsubway.eth continues to make millions off the back of meme coin traders. “sandwich bots are only able to attack you because they see your buy order hanging around in the mempool before it gets included in a block. so you need to submit it to a private mempool instead of a public mempool. flashbots runs the largest private mempool, that’s who to use”

0 Comments