Intro

In our Year Ahead report for DeFi, we examined the thesis for so-called DeFi blue chips and their ability to bounce back from a tough year. Aave is one of those projects, and one that virtually everyone in crypto is aware of. We’ve recently created a Aave Dashboard, check it out in the Delphi Datahub here.

Aave is one of the core DeFi layers for the entire ecosystem. Their main product is a neobank for decentralized lending – users deposit funds which others can borrow. However, Aave’s strategy targets a much larger goal — creating the Aave super-app. Aave’s platform has expanded to seven different chains, has released a market for AMM tokens, a social network, and has even built cross-chain signaling into their backend.

Like most crypto projects, token holders control Aave through governance. Token holders decide how Aave spends their revenue, onboards new teams, the parameters for their apps, and the vision for the entity. Revenue and spending are where this report starts.

If we consider Aave a business, how is it performing relative to itself? Are token holders stewarding the DAO’s funds well? Is spending in line with revenue? Is Aave’s revenue in line with the rest of the market? How will the surrounding macro environment impact Aave?

We attempt to answer these questions by looking at Aave’s fundamentals.

Aave is an outlier in crypto because it provides decent financial documentation. For some DAOs, looking at their fundamentals would be highly challenging beyond cross-referencing the chain and governance.

Aave provides token holders with monthly financial reports and websites which detail their spending and revenue — a standard we hope becomes much more commonplace in this industry.

The Aave Business Model

As a neobank, Aave’s primary business model is relatively simple; they charge fees to use the Aave platform. Users pay fees whenever they borrow, deposit, liquidate, or use flash loans. The Aave protocol splits fees between the Aave DAO and those who backstop the protocol’s risk in the Safety Module through staking the native token, AAVE.

AAVE holders adjust fee parameters for each asset through governance. The specific fee level chosen for each asset is affected by an asset’s supply, market cap, market depth, and other market-specific parameters. This means each asset on Aave has a fee level associated with its perceived risk by the community.

Between Aave core contributors and AAVE holders, determining these various parameters for the protocol is a challenging balancing act. Fees need to be high enough to generate revenue for the protocol and offset any risks it takes, but also low enough to incentivize usage of the platform.

Revenue is the most critical metric for Aave to continue development. Although a decentralized entity, Aave still has to pay contributors and developers to work on the platform. Revenue is also important because Aave uses it to reward stakers in the Safety Module. Without significant revenue, there is little incentive for AAVE holders to backstop risk in the protocol. Paying stakers and developers is a significant source of expenses.

Analyzing Financials and Growth Prospects

Revenue

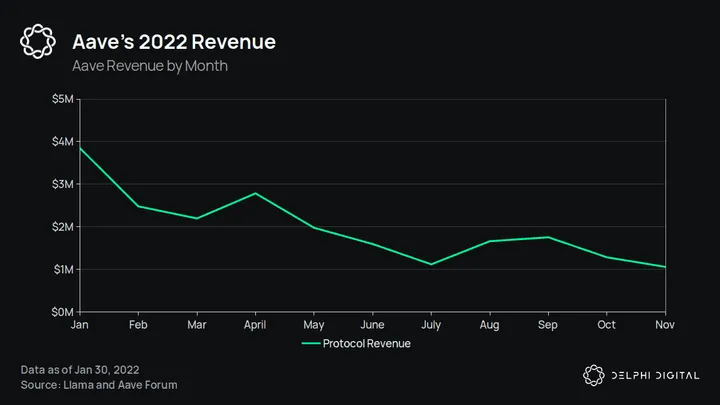

Unfortunately for Aave, revenue declined throughout 2022 on account of interest rate compression, lack of borrowing demand, and more attractive yield opportunities in other venues. Revenue here is the amount of money Aave is making after it pays stakers in the Safety Module. These are the funds that AAVE holders control. Protocol revenue from January to November 2022 sits at about $21.75M. This puts Aave on track for estimated revenue of ~$23M per year. Given that Aave is a protocol with almost $6.4B in TVL and a market cap of $1.19B, $23M per year doesn’t seem exceptionally profitable. However, Aave attracts deposits through a low net-interest margin — meaning that Aave takes less money off the top for profits than traditional banks, so earnings may always be somewhat muted.

$23M revenue gives Aave an estimated revenue per token of $1.62 (using circulating supply), while the current token price is $83.21. This revenue per token gives Aave an eye-watering P/S ratio of 51.5 — meaning AAVE tokens trade at a 51.5x multiple. A P/S of 40 is typical of a growth stock, so 51.5 is probably reasonable for a DeFi protocol with growth potential like Aave. A 51.5x multiple could even be low for something like a DeFi token which commands speculative upside.

However, there is an essential bit of nuance when looking at Aave’s revenue. Aave uses some of its fees to reward users who stake AAVE in the Safety Module. As such, the protocol’s total fees are much higher, but a significant portion goes to stakers and is not accessible by the DAO.

If you look at the total fees that the protocol accrues, it has a P/S ratio of about 17.25. But, as we are analyzing the DAO’s fundamentals, we think that looking at the revenue the DAO brings in presents a much clearer picture. If a business paid out a large chunk of its revenue as dividends to the point it operated at a loss, you would want to be aware of it.

User Growth

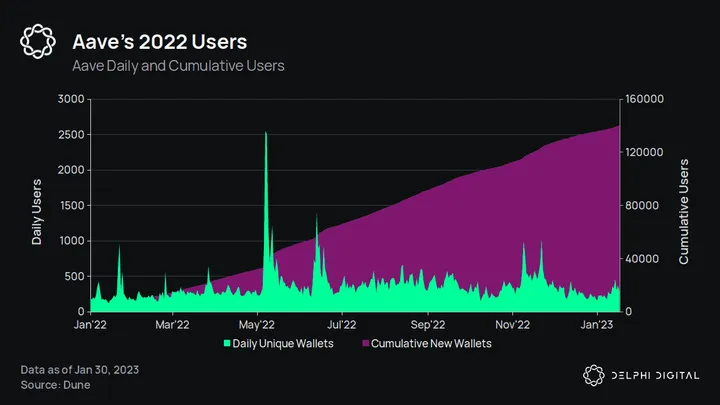

Despite macro headwinds and a disastrous year for crypto overall, Aave’s revenue prospects look fairly good, with decent customer growth over 2022. New users, measured by new wallets interacting with Aave, grew throughout 2022. Almost 140k new wallets connected to Aave in 2022. These are by no means all new unique users. Some new wallets are undoubtedly old users connecting with new wallets. Regardless, this is a positive trend for Aave. New addresses bring new deposits, new loans, new loan defaults, and drive more revenue to the protocol.

Despite macro headwinds and a disastrous year for crypto overall, Aave’s revenue prospects look fairly good, with decent customer growth over 2022. New users, measured by new wallets interacting with Aave, grew throughout 2022. Almost 140k new wallets connected to Aave in 2022. These are by no means all new unique users. Some new wallets are undoubtedly old users connecting with new wallets. Regardless, this is a positive trend for Aave. New addresses bring new deposits, new loans, new loan defaults, and drive more revenue to the protocol.

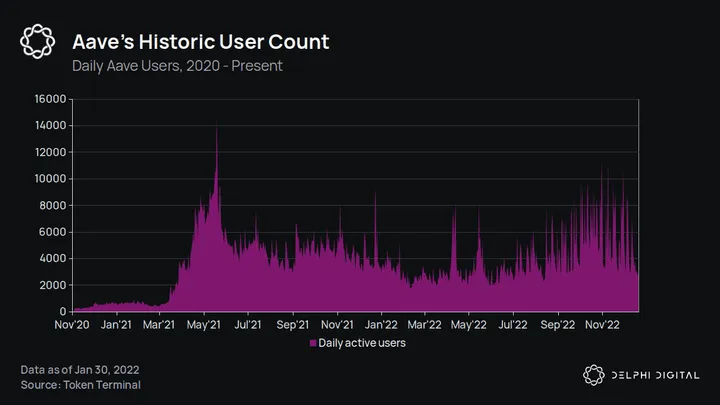

Even when looking back before 2022, we see that daily active users on Aave stayed relatively consistent throughout 2022. Aave now needs the broader market to improve so it can hopefully capitalize to increase revenue.

Core Expenditures by Aave

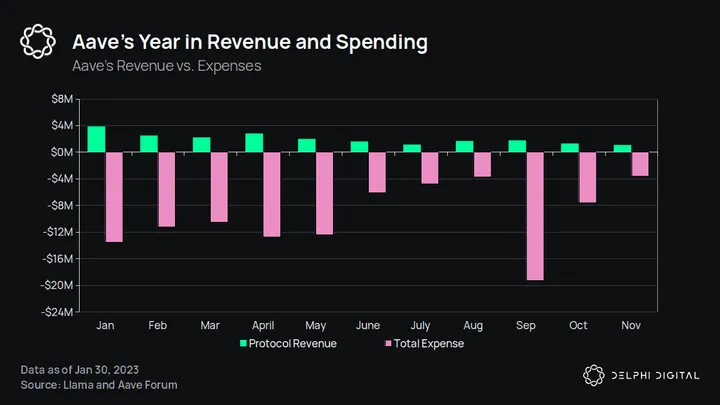

As savvy investors are aware, revenue is only one part of the equation when looking at the fundamentals of a business. Due to their importance for the future of a protocol, Aave crypto investors often need to pay more attention to expenses in DeFi. Expenses are where things look a little dire for Aave. Based on their financial reports, created by the team at Llama, Aave recorded a loss of $83M from January to November 2022. The Llama team has not yet released the December report, but we can estimate a total loss of around $85M for the protocol.

As savvy investors are aware, revenue is only one part of the equation when looking at the fundamentals of a business. Due to their importance for the future of a protocol, Aave crypto investors often need to pay more attention to expenses in DeFi. Expenses are where things look a little dire for Aave. Based on their financial reports, created by the team at Llama, Aave recorded a loss of $83M from January to November 2022. The Llama team has not yet released the December report, but we can estimate a total loss of around $85M for the protocol.

The way Llama records expenses includes liquidity incentives, staking rewards, and third-party payments. Each line item was higher than the entire year’s revenue for Aave. Between January and November, liquidity incentives and staking rewards cost Aave $28.7M and $37.3M, respectively. These items, although important, are a bit like depreciation in a business — they affect the overall position of a business but don’t reduce cash on hand.

In Aave’s case, these line items come from AAVE token emissions which reduce the ability of the protocol to fund future endeavors through token sales. They also dilute existing token holders, but many protocols pay for liquidity and incentives in this way.

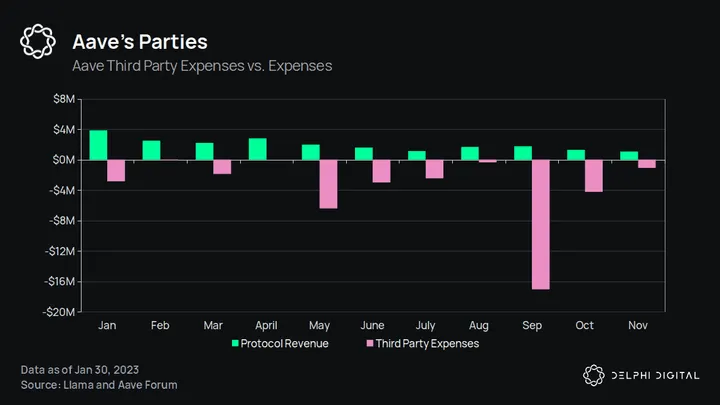

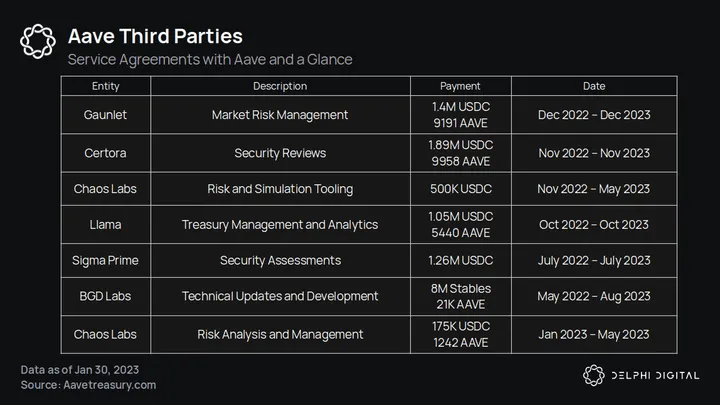

From a business management perspective, the most interesting aspect is Aave’s third-party expenses. As a decentralized entity, Aave doesn’t have a single entity that does all the development. Instead, firms can apply for funding from Aave to complete set tasks. Funding is usually streamed to these firms as they work, but Aave also experimented with retroactive funding to develop their v3.

From a business management perspective, the most interesting aspect is Aave’s third-party expenses. As a decentralized entity, Aave doesn’t have a single entity that does all the development. Instead, firms can apply for funding from Aave to complete set tasks. Funding is usually streamed to these firms as they work, but Aave also experimented with retroactive funding to develop their v3.

Between January and November of 2022, Aave’s third-party agreements cost the DAO almost $40M. September 2022 accounted for almost half of this item as they retroactively rewarded Bored Ghost Labs with $16.28M for developing Aave’s v3. Aave split the remaining $24M between a few separate entities providing services to Aave.

The Balance Sheet

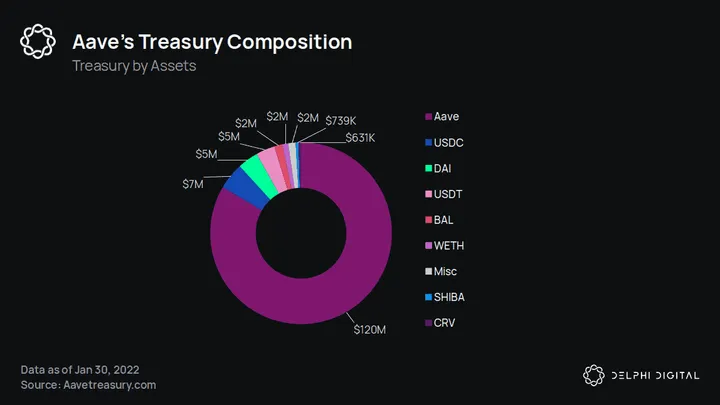

The story of Aave’s treasury is one we have seen time and again in the DeFi space — it consists mostly of native tokens, which have been hit hard by recent drawdowns. Aave’s treasury has two parts: the ecosystem reserve and the central treasury. The ecosystem reserve consists of AAVE tokens, which the protocol can leverage for liquidity mining or staking rewards.

The central treasury, on the other hand, consists of token revenue that Aave has earned through fee collection. The central treasury mainly consists of non-AAVE tokens, although the fee collector contract has accrued some AAVE via fees.

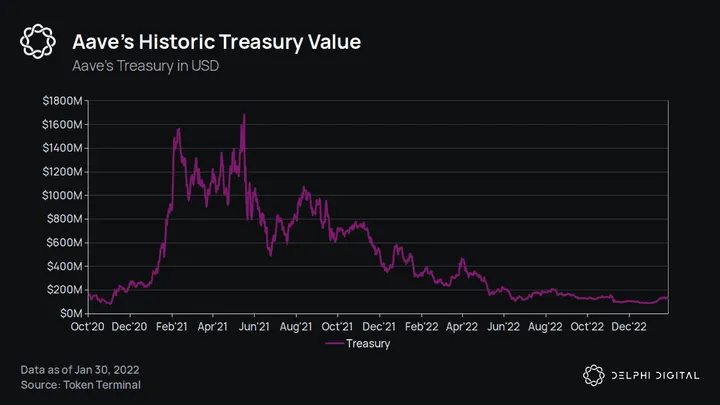

As is expected, when a DAO has a treasury consisting primarily of native tokens, the treasury value is subject to significant volatility – volatile crypto assets make for a volatile treasury. Peaking at a total value of $1.65B, the Aave treasury has since declined to around $143M — a 91% drawdown.

As is expected, when a DAO has a treasury consisting primarily of native tokens, the treasury value is subject to significant volatility – volatile crypto assets make for a volatile treasury. Peaking at a total value of $1.65B, the Aave treasury has since declined to around $143M — a 91% drawdown.

Thankfully for Aave, $30M of that treasury is in non-AAVE assets (mostly stablecoins).

$143M is a significant amount of money, but given Aave’s burn, it still gives us cause for concern. We worry that with Aave’s expenses, especially their third-party ones, they may quickly be approaching the end of their runway. If Aave continues spending at the same rate they did in 2022, it seems they only have 24 months of runway left, and even less if the price of AAVE declines. Aave could be betting that the market will improve in that time and revenue will increase, but that is a risky assumption.

$143M is a significant amount of money, but given Aave’s burn, it still gives us cause for concern. We worry that with Aave’s expenses, especially their third-party ones, they may quickly be approaching the end of their runway. If Aave continues spending at the same rate they did in 2022, it seems they only have 24 months of runway left, and even less if the price of AAVE declines. Aave could be betting that the market will improve in that time and revenue will increase, but that is a risky assumption.

The Fuzzy Stuff

Regarding Aave’s fundamentals, a slew of qualitative and fuzzy qualities offer Aave a definite advantage over its competitors. The first is that Aave has a solid brand, one of the strongest in DeFi. Maybe only Uniswap and Curve are as recognizable as Aave. The purple-hued color scheme and adorable ghost mascot are as strong a brand image as we have in DeFi. It’s hard to quantify, but people should not ignore Aave’s strong brand.

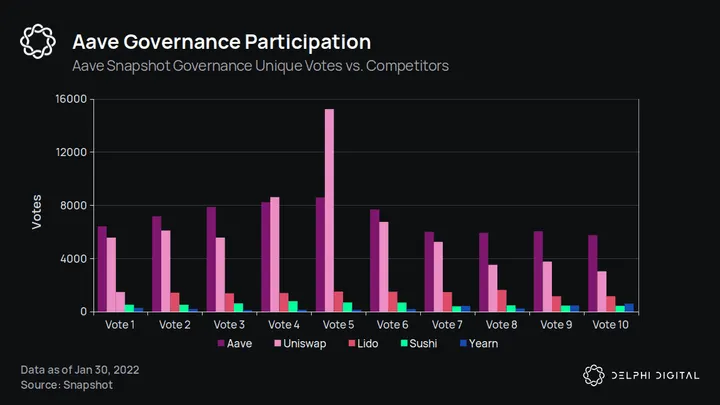

Secondly, among all the DeFi protocols we have seen, Aave has consistently had some of the best governance engagement. The forum is active, with dedicated individuals posting well thought-out responses and proposals. Their snapshot votes often have thousands of people voting, whereas others only have a few dozen. We can see this higher engagement level when comparing the last 10 Aave snapshot votes with comparable protocols.

Aave consistently has more participation. We have our misgivings about DAO governance as it currently exists, but in our opinion, Aave is a definite leader in this regard.

Growth Catalysts

Although struggling with revenue, Aave has some upcoming releases that may help increase revenue, drive more users to the platform, and ultimately create their super-app.

Time to GHO

The most exciting development for Aave is the launch of their stablecoin, GHO. GHO will function much like DAI in that it will follow a CDP model. Users will be able to mint GHO against the collateral they have supplied to Aave, and they will still earn interest on their deposited collateral while using it to mint GHO.

GHO opens up an entirely new market for Aave. Not only will they have a lending platform, but they will also have one that mints stablecoins on user deposits. Suddenly, with some development, Aave expands its platform and TAM to include stablecoins and significantly challenges MakerDAO and DAI. Even using a conservative LTV of 50%, Aave could mint upwards of 2.5B GHO immediately when it goes live — although it’s more likely Aave will slowly roll out GHO rather than all at once.

Cross-Chain Portal/Signaling

Aave v3 also introduced the Portal feature to the platform. The Portal allows approved bridges to burn aTokens (Aave deposit tokens) on one chain and then mint them on another. The Portal brings cross-chain composability to Aave assets and will add a ton of utility to GHO and bring liquidity to many chains. Aave users could deposit crypto assets on Aave Ethereum, move their aTokens to Aave Polygon, and mint GHO against them.

Given that Aave’s app exists on Ethereum, Polygon, Avalanche, Arbitrum, Fantom, Optimism, and Harmony One, the Portal may allow GHO users and Aave depositors to move between these chains quickly.

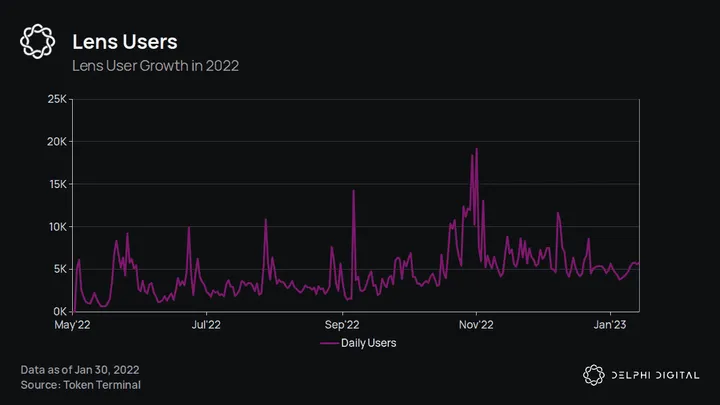

Lens Protocol

Lens Protocol, Aave’s decentralized social graph, launched in early 2022 and has seen steady growth. Lens now serves around 5k users per day. Although not Aave’s primary source of revenue, fees from this are relatively low at the moment. Lens expands Aave’s product suite and is an important pillar in their overall strategy of building the Web3 super-app.

Lens Protocol, Aave’s decentralized social graph, launched in early 2022 and has seen steady growth. Lens now serves around 5k users per day. Although not Aave’s primary source of revenue, fees from this are relatively low at the moment. Lens expands Aave’s product suite and is an important pillar in their overall strategy of building the Web3 super-app.

Aave and the Market

Looking at Aave in isolation, it’s easy to come away with a bearish outlook due to the declining fee revenue and high cash burn. However, when looking at Aave relative to its competitors, Aave is in a great position.

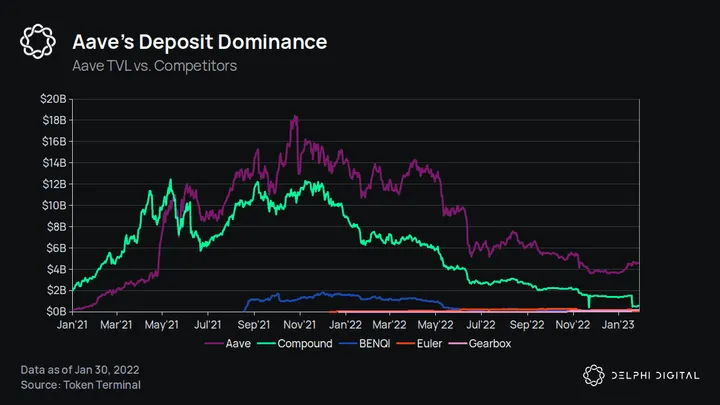

Regarding total value locked, which for lending apps would mostly be deposits, Aave is leading the market. Compound is Aave’s closest competitor and has less than half of Aave’s TVL. Other competitors are in a different league entirely. Granted, there have been significant TVL reductions throughout the market, but Aave still has more deposits than its competition. Aave’s dominance looks almost untouchable at this time.

Regarding total value locked, which for lending apps would mostly be deposits, Aave is leading the market. Compound is Aave’s closest competitor and has less than half of Aave’s TVL. Other competitors are in a different league entirely. Granted, there have been significant TVL reductions throughout the market, but Aave still has more deposits than its competition. Aave’s dominance looks almost untouchable at this time.

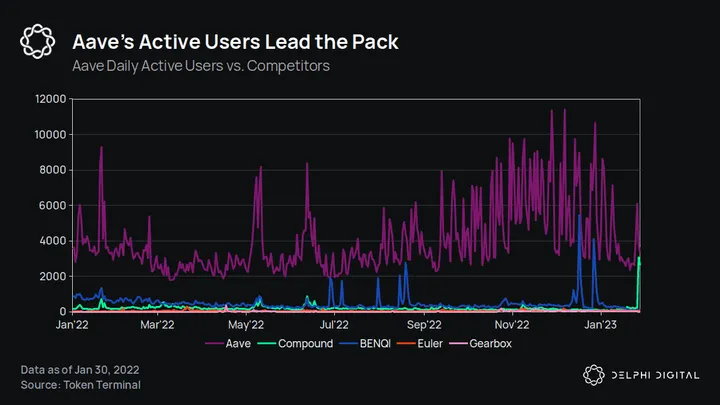

The same is true for Aave’s active-address count. Throughout 2022, Aave averaged ~4k daily addresses. Comparing that to Compound, which averaged 205 daily addresses, or Benqi’s 501, Aave firmly leads the pack.

The same is true for Aave’s active-address count. Throughout 2022, Aave averaged ~4k daily addresses. Comparing that to Compound, which averaged 205 daily addresses, or Benqi’s 501, Aave firmly leads the pack.

It is important to note that Benqi, Gearbox, and Euler are much newer than Aave and have not had as much time to grow their user bases. Even still, Aave’s higher usage stats paint a relatively bright picture for the protocol.

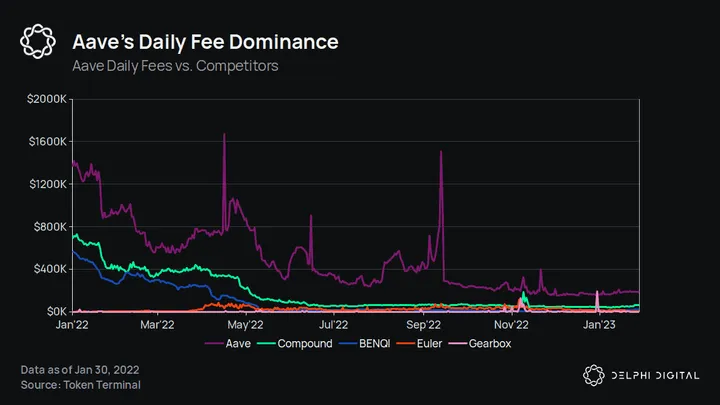

Aave’s much larger TVL and user base have unsurprisingly allowed Aave to maintain higher fee revenue than its competitors. As discussed in the revenue section of this report, Aave’s fees have declined throughout 2022, but Aave is still beating out its competitors. On average through 2022, Aave earned $517k in daily fees. Compound and Benqi, meanwhile, earned $186k and $105k, respectively. Aave’s daily fee revenue is almost triple its nearest competitor.

Aave’s much larger TVL and user base have unsurprisingly allowed Aave to maintain higher fee revenue than its competitors. As discussed in the revenue section of this report, Aave’s fees have declined throughout 2022, but Aave is still beating out its competitors. On average through 2022, Aave earned $517k in daily fees. Compound and Benqi, meanwhile, earned $186k and $105k, respectively. Aave’s daily fee revenue is almost triple its nearest competitor.

These three charts show that although 2022 was a challenging year for Aave, it has maintained and strengthened its dominance in the DeFi lending space. Aave’s moat is looking deep and wide.

Aave and the World

When we ponder how the macro environment may impact Aave, it looks like TradFi interest rates will be one of the largest challenges for crypto-native money markets.

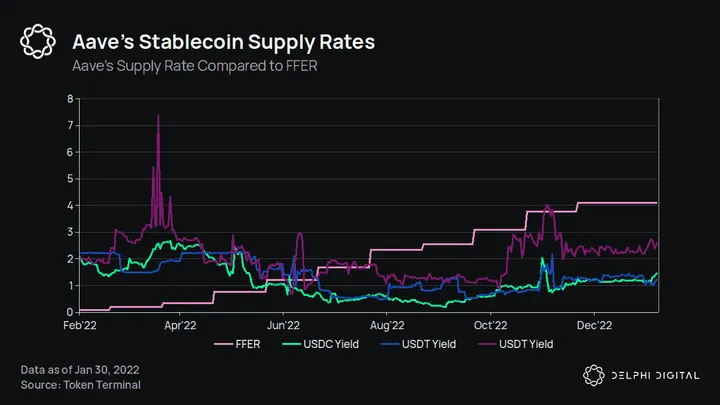

Rising TradFi rates could be one cause of Aave’s declining revenue. Throughout 2022, we have seen central banks around the world increase interest rates in an attempt to squash inflation. The Federal Funds Effective Rate at the end of December 2022 was 4.1%. Meanwhile, at best, stablecoin rates on Aave hovered around 1-2% throughout the year.

Rising TradFi rates could be one cause of Aave’s declining revenue. Throughout 2022, we have seen central banks around the world increase interest rates in an attempt to squash inflation. The Federal Funds Effective Rate at the end of December 2022 was 4.1%. Meanwhile, at best, stablecoin rates on Aave hovered around 1-2% throughout the year.

Rising rates give Aave a dubious value proposition. Users can hold a stablecoin or digital asset with regulatory uncertainty and deposit it in a lending protocol with solvency and smart contract risk for 1%, or they can buy a T-bill or get a savings account for 4.1%. Although a large chunk of users have stuck around in stablecoin and crypto-native money markets, it doesn’t bode well that a riskier market has lower interest rates than the de-facto global “risk-free asset.”

Aave’s lending rates are contingent on borrowing demand or demand for leverage. Given the state of the market over the past year, demand for leverage isn’t what it was in 2021 or early 2022. Thus, this systematically means lower rates on Aave. As demand for on-chain leverage increases, we will see Aave’s interest rates revert to more normal levels to reflect the required risk premium over traditional rates.

Ondo Finance bringing T-bills on-chain may help close the spread between TradFi and Aave, but this may not be possible at scale.

Conclusion

As we can see from this report, 2022 was a challenging year for Aave but an even more challenging one for their competitors. Aave’s revenue declined through 2022, and on an absolute basis, Aave is spending more than they’re bringing in. But even after more than a year of bearish conditions, Aave still has 24 months of runway if prices and revenue remain stable.

Aave leads the pack in users, revenue, developers, and TVL. Aave’s governance is also more active, and their branding is some of the strongest in the space. Despite various headwinds, Aave seems to be developing a moat, and it’s unlikely that we’re looking at anything close to the end-state for Aave.

Special thanks to Cheryl Ho for designing the cover image for this report and to Ashwath Balakrishnan and Brian McRae for editing.

0 Comments