Breaking Down the Design Space of Money Market Liquidations

APR 13, 2022 • 17 Min Read

Report Summary

To find the merits and demerits of various liquidation mechanisms employed by DeFi money markets, we evaluate them on the following criteria: democratization of liquidation profits, speed of liquidations, transaction costs, protocol capital efficiency, price impact of liquidations, and penalties levied on borrowers.

The fixed liquidation discount model is the simplest, and most effective, but can make bad situations worse (during sharp drawdowns) as liquidators engage in Priority Gas Auctions when the base L1 is already congested. Often times, under this model, a larger than necessary portion of a borrower’s loan is liquidated as the bigger a liquidation is, the more profit a liquidator earns.

Stability pool based liquidations democratize the process to a broader community instead of being dominated by bots. Users can deposit funds into this pool to take part in liquidations. On the downside, passive liquidations rely on individual users selling the collateral they bid on, which could reduce or eliminate profits during extended drawdowns. However, new products such as B. Protocol automate this component, vastly improving the UX of passive liquidations.

Dutch auctions are proving to be a fairly effective method for liquidation. However, these methods induce larger discounts the longer an auction runs, providing liquidators with a disincentive to be early. Euler’s “quasi-Dutch auction,” on the other hand, has sped up the process of a general Dutch auction, thereby improving efficiency.

Liquidation queues facilitated by the likes of Kujira on Terra are akin to stability pools, providing users with an easy UI and the ability to bid on liquidations in an orderbook-like fashion. This is primarily used to process liquidations on Terra’s Anchor money market.

Introduction

Liquidations are a popular concept in the crypto asset market. With crypto’s volatility comes lucrative opportunities, but as the saying goes, there is no reward without risk. Liquidations refer to the process of a leveraged position being wound down due to the risk of impending insolvency. When this occurs, the assets a borrower/trader posted to guarantee repayment are seized – either partially or completely.

Users who have traded crypto derivatives or taken loans from DeFi money markets will be familiar with the concept of liquidations. While derivative based liquidations are far more prevalent, for the purpose of this report we’re going to zone in on money market centric liquidations.

In the wild west of DeFi, traders looking to increase their exposure with leverage or take a speculative bet on tokens, can take over-collateralized loans from popular money markets like Aave and Compound. This act, however, doesn’t come without risks. If the value of a borrower’s collateral decreases against the borrowed asset, the borrower’s collateral assets are subject to liquidation.

A good liquidation mechanism is essential for trustworthy money markets, and should help protocols weather periods of market volatility and illiquidity. In this report, we explore some of these mechanisms, and evaluate each of them across the key criteria that are crucial to a well-functioning liquidation system.

What makes for a good liquidation mechanism?

Avoiding the occurrence of bad debts is the primary aim of a liquidation design, as unliquidatable collateral is a loss typically borne by the protocol or socialized among token holders/depositors. Other considerations such as improving the access of liquidation surpluses and tempering the severity of penalties may also alleviate an otherwise unfortunate experience. We believe that a good design should refrain from crippling borrowers with overly harsh liquidation penalties, minimize the cost of carrying out a liquidation, and ensure that there is sufficient liquidity to unwind these positions – especially during torrid market conditions.

Taking these considerations into account, we created a framework to evaluate various liquidation mechanisms. The key factors can be distilled as follows:

- Democratization of liquidation profits is defined as the access to, and competition for, liquidations and their resulting profits. Liquidations on Ethereum are typically dominated by keeper bots that compete to liquidate discounted collateral.

- Speed of liquidations can be measured by how quickly the protocol is able to get rid of underwater positions via liquidation.

- Transaction costs refers to the cost borne by liquidators for liquidating collateral.

- Capital efficiency refers to borrowing power, measured by the LTV ratio. A higher LTV indicates better capital efficiency, and lower LTV indicates lower capital efficiency. The main reason for including this was to ascertain whether protocols were limiting capital efficiency to make room for more effective liquidations.

- Price impact refers to the impact of liquidations on the price of an asset. Several liquidation designs have internal sources of liquidity or other levers such as limits and delays to minimize price impact on exchanges.

- Liquidation penalty is defined as the penalty a borrower incurs as a result of liquidation. An optimal penalty for borrowers is one that is just enough to incentivize liquidators but without leading to cascading liquidations.

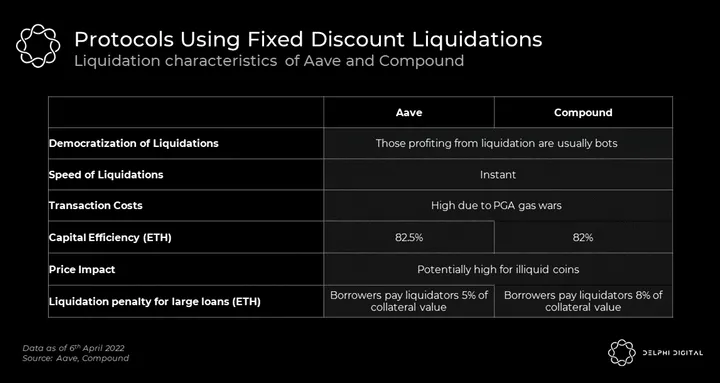

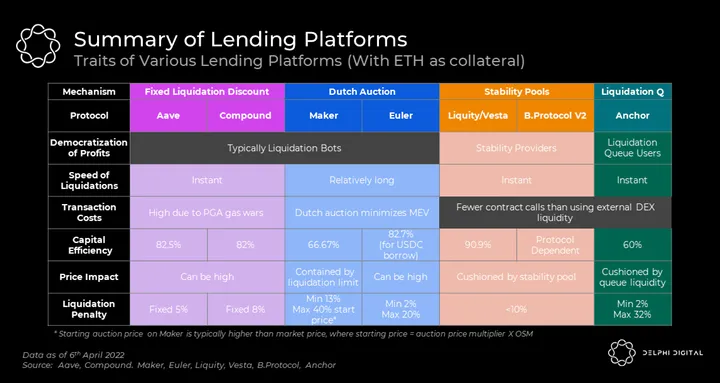

Fixed Liquidation Discount: Aave and Compound

The most straightforward type of liquidation mechanism is the fixed discount liquidation that Aave and Compound employ. In a fixed discount liquidation, loans within the liquidation threshold are able to be instantly liquidated at a predetermined discount. This liquidation discount typically depends on the asset used as collateral, with more volatile assets commanding a higher liquidation discount.

Aave allows liquidators to purchase up to 50% (close factor) of an underwater position at up to a 15% discount (depending on the collateral type) of the current market price. A liquidator must have sufficient balance of the debt asset before initiating the liquidation call to purchase the capital at a discount. Liquidators then engage in PGAs (Priority Gas Auctions) to determine who gets to liquidate the loan position.

The benefits of the fixed liquidation discount are clear. The liquidation discount, or liquidation spread, is known upfront, giving liquidators some certainty of profitability given a liquidation opportunity. Settlement is also done within the same block, avoiding long auction times which cost time and transaction fees. Liquidators can also make use of flash loans, which reduces the exposure of holding the assets needed to execute the liquidation.

However, due to limited space in an Ethereum block and the profitability of a liquidation, competition among liquidators has led to them over bidding in PGAs, in an effort to be the earliest. (Data between April 2019-2021 shows that 73.97% of the liquidations pay an above average transaction fee on Aave v1, Aave v2, Compound and dYdX). This gas war leads to MEV and network congestion, which could result in more liquidations as borrowers find it harder to re-collateralize their positions during periods of high transaction costs.

Furthermore, high close factors can be exploited by liquidators. Even if a loan would be sufficiently collateralized by liquidating e.g. 20% of the position, a profit maximizing liquidator would be incentivized to liquidate up to the maximum of 50% of the debt within one execution, as they are receiving more collateral at a discount to market prices. Over-liquidation is thus better for liquidators but worse for borrowers, which throws off the optimal game theory for both parties. Low close factors, on the other hand, could result in multiple liquidation transactions for the same loan position, increasing transaction costs and network congestion.

Furthermore, a fixed discount may not be sufficient to cover the transaction cost of small liquidations. Aave, for instance, has bad debt consisting of small positions that are unprofitable for liquidators to liquidate. On the other end of the spectrum, discounts can be overly harsh for large position sizes and thus discourage large borrowers. To illustrate both points, an ETH position worth 1m would have to suffer a liquidation penalty of a whopping $50k, while a small position of $1,000 has a $50 penalty – barely enough to cover a liquidator’s gas costs

Revisiting our original criteria, we summarize Aave and Compound’s fixed discount liquidation characteristics below.

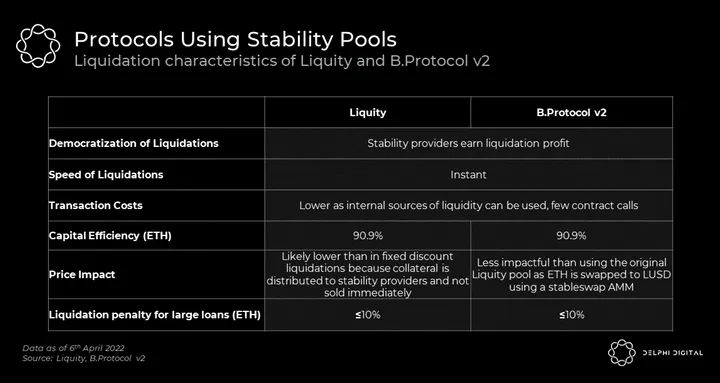

Stability Pools: Liquity and B Protocol

Liquity championed the iconic stability pool design that has since gone on to be adopted by protocols like Vesta and Euler. Instead of relying on external capital provided by liquidators, the stability pool acts as a source of liquidity to repay liquidatable debt.

The stability pool is funded by those who deposit LUSD tokens (in the case of Liquity) into the pool. When a loan position is below the liquidation threshold, an amount corresponding to the remaining pools is instantaneously taken from the Stability Pool’s balance for debt repayment. In exchange, the entire loan position is transferred to the Stability Pool and distributed pro-rata to stability providers. Stability providers stand to benefit as they have “purchased” ETH at a discount with their LUSD.

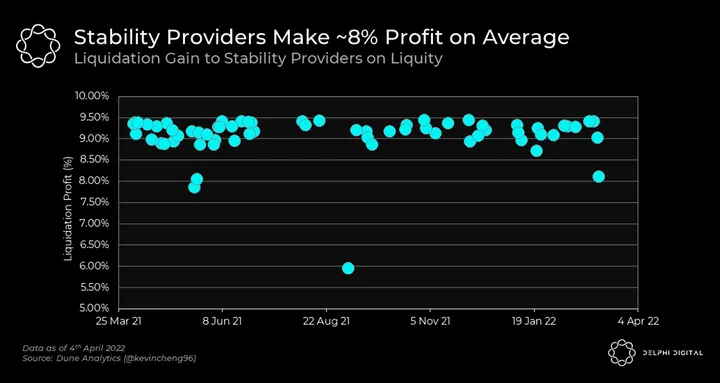

Liquity’s stability pool has been fairly constant, with an average liquidation discount of ~9% and a weighted average of ~8%.

Stability pools are great because they are an internal and immediate source of liquidity for liquidation events. Instead of incurring price slippage and swapping on external DEXes, transaction costs for stability pool liquidations are lower since it only consists of an internal token transfer.

However, the stability pool mechanism doesn’t take into consideration the opportunity cost of capital. Profits are also not time weighted. This means that all stability providers receive the discounted collateral pro-rata, without consideration for who has had their capital in the pool the longest. As stability providers receive the collateral, there is also a risk that the price of collateral continues to drop even further before stability providers have the chance to liquidate it.

An interesting innovation that has developed alongside stability pools is B.Protocol’s Backstop Automated Market Maker (B.AMM) – an AMM that optimizes for money market liquidations. It allows for auto-compounding of the Stability Pool profits by automatically selling the liquidated collateral back into Stability Pool deposits.

The diagram above depicts the liquidation flow using the stability pool liquidity backstop, with and without the B.AMM.

A stability pool with or without the B.AMM:

- A stability pool consists of a pool of IDLE assets (E.g. LUSD) which may be deposited to yield bearing protocols when not used for liquidations.

- The BITE component connects IDLE to the money market for liquidations. When a bite transaction is called, IDLE assets are withdrawn to repay the accounts debt, while transferring the account’s collateral to the user.

The work flow for a stability pool that doesn’t integrate with B.Protocol’s B.AMM stops here

A stability pool with the B.AMM has a unique process flow:

- Same as step 1 without a B.AMM; IDLE assets are deposited to a stability pool.

- Instead of transferring the account’s collateral to the user, the liquidated collateral (E.g. ETH) is transferred to the REBALANCE component.

- REBALANCE sells the liquidated collateral in exchange for the asset in the IDLE component (LUSD in this case)

- This is done using B.AMM which integrates Curve’s Stableswap invariant.

- Liquidated Collateral is normalized to USD value using an oracle price feed.

- The seized collateral is put for sale at a discount to market price (max discount is 4%) but the discount is less than the liquidation discount to maintain profitability.

- Anyone can interact with this smart contract to purchase the seized collateral

- The RETURN component deposits proceeds from the sale back to the IDLE stability pool so the process can repeat.

One obvious drawback is that stability pools may earn slightly lower liquidation profits with the B.AMM as profits are shared with B.AMM discount buyers. However, the B.AMM lets profits auto-compound while reducing the liquidity provider’s exposure to the collateral asset. Adding LUSD back to the stability pool also deepens its liquidity. This further reduces the potential price impact of liquidations.

In the above two mechanisms, liquidations occur more or less near the predetermined discount level set by the protocol. In the following sections, we will examine auction style mechanisms with a dynamic liquidation discount.

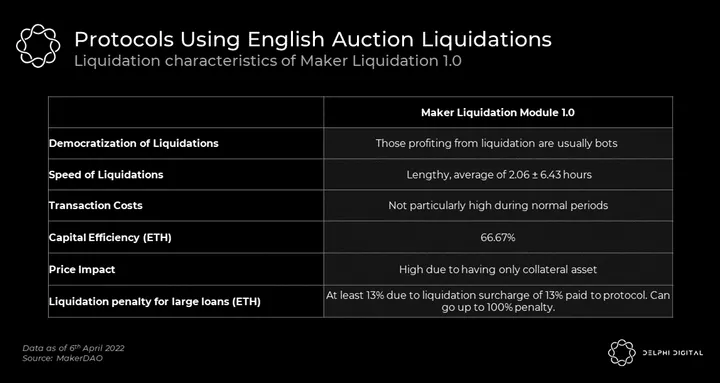

English Auction: Maker (Before Mid-2021)

Prior to Maker’s new liquidation module upgrade, its collateral auction consisted of an English auction, where potential liquidators submitted bids of increasing value followed by a possible reserve auction.

In the first auction, bidders would raise that bid by offering more DAI until it covered the outstanding debt or until the auction duration expired. A key point to note is that bidders must have sufficient DAI balance, and a successful bid is locked up for several blocks.

If sufficient DAI was offered to cover the debt in the English auction, it is followed by a reverse auction. If not, the collateral auction ends after the English auction; the winning bidder is awarded the collateral and the protocol incurs bad debt.

In the former case, bidders bid on accepting smaller parts of the collateral in the reverse auction, until the auction reaches the maximum duration, or until no bidder is willing to bid lower than the current bid. Thereafter, the winning liquidator is allowed to finalize the liquidation and receive the proposed collateral.

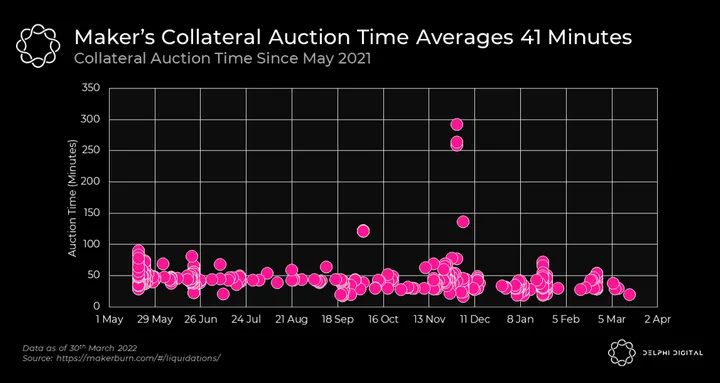

Maker’s liquidation 1.0 design resulted in lengthy liquidation durations of 2.06 ±,6.43 hours (mean ± standard deviation) on average. Having to lock up the bid amount also meant that liquidations couldn’t occur within the same block and flash loans cannot be used. The implication is that keepers would have to take on price exposure to the asset (an insignificant risk in Maker’s case as DAI is a “stable asset”). Also keepers could end up holding on to much needed liquidity during periods of low liquidity, exacerbating price volatility on exchanges.

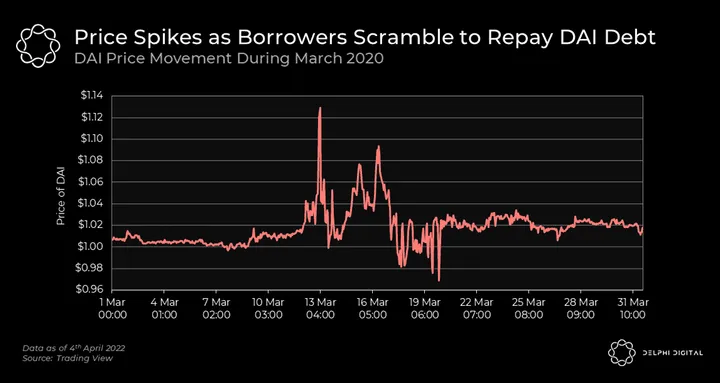

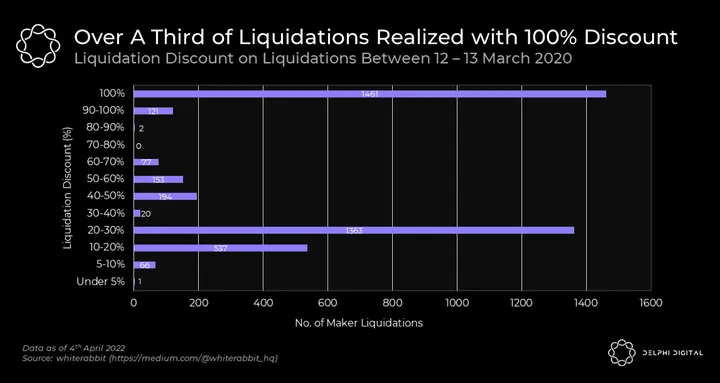

The determinants of this system were very much exemplified during the market collapse of Mar. 12-13, 2020, where market conditions caused a over 50% drop in the value of ETH. At the time, DAI was backed solely by ETH collateral, triggering 4,447 liquidations as ETH’s price tanked. Demand for DAI surged as borrowers rushed to repay their DAI debt, causing DAI to trade overpeg.

The English auction design also famously gave rise to “zero bid auctions” where a number of collateral auctions were won by liquidators placing zero bids (i.e. they received someone’s ETH collateral without paying a single DAI). The issue as outlined by Maker was caused by a mix of network congestion and a lack of DAI liquidity, which prevented other liquidators from making new bids to contest the zero bids.

DAI spiked to over $1.12 as seen in the chart below.

Users had their collateral confiscated without any recourse in 36% of the triggered liquidations. Liquidator bots benefited the most at the expense of borrowers and the protocol.

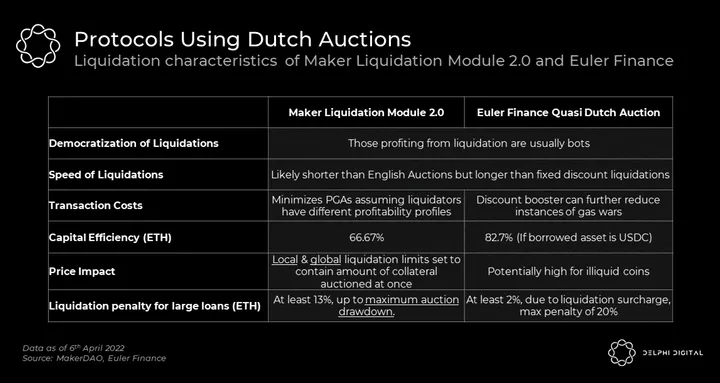

Dutch Auction: Maker and Euler

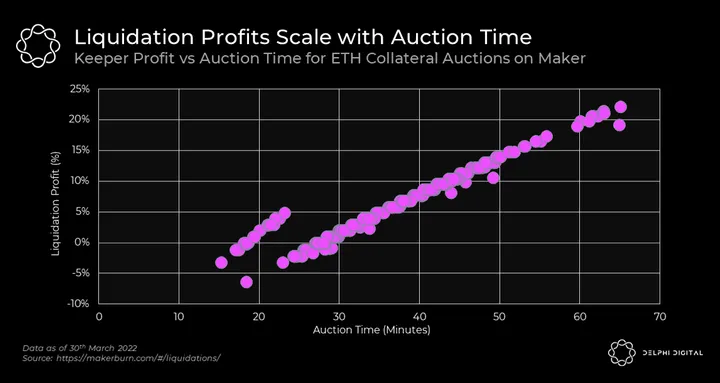

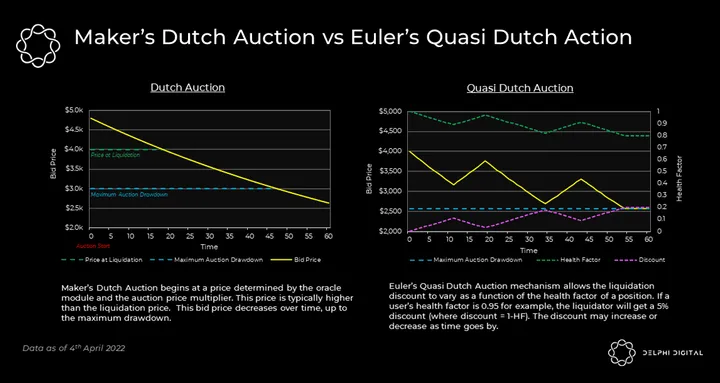

In response to the shortcomings of their previous liquidation mechanism, Maker implemented Liquidations 2.0 in May 2021. Since then, the liquidation process has been streamlined into a single Dutch auction. Here the collateral is priced at a high initial bid that decreases deterministically over time until a willing buyer is found. If there is no willing buyer, the discount on the collateral increases up to a predetermined limit (thereby avoiding zero bids) or until the maximum auction duration is reached.

Therefore, at any point in time during the auction, potential liquidators must decide whether to jump in at the current offer or wait for the discount to increase. If the choice is the latter, the would-be liquidator risks giving it up to another liquidator willing to accept a smaller discount. Liquidators will thus choose to liquidate just when it is sufficiently profitable for them to take the bid.

Data from Maker’s auctions shows that collateral auctions that take a longer time to find a willing bidder typically result in a higher profit due to the larger discount on collateral.

Unlike before, auction settlement is now done within the same block of the liquidator accepting the bid, so flash loans can be used to bypass capital requirements of an English auction. However, though the liquidation process is shorter than the English auction, it still doesn’t compare with the immediacy of the fixed liquidation discount design.

We would also like to highlight a variant of the Dutch auction Euler finance uses, dubbed a “quasi Dutch auction”. In this version, the collateral’s liquidation bonus varies according to how underwater position is, up to a limit of 20%. For instance, if the health factor is 0.95, the liquidation bonus to the liquidator is 5%. [Liquidation Bonus = 1 – HF].

With either Dutch auction, there is no financial benefit for being early. Assuming that liquidators have different profit targets and/or breakeven points, the Dutch auction reduces the occurrence of expensive PGAs inherent in the fixed liquidation discount design. PGAs, however, still can happen if liquidators jump in to bid for collateral in the same block.

To combat this, Euler gives liquidators the ability to earn a “liquidation discount booster” if they lend on the protocol. The booster gives lender-liquidators the opportunity to front-run liquidators that have no stake in the protocol by helping them reach profitability in the Dutch auction before those without the booster. In this manner, the liquidation discount booster incentivizes lending, and further limits PGA wars as competition is limited and skewed in favor of lender-liquidators.

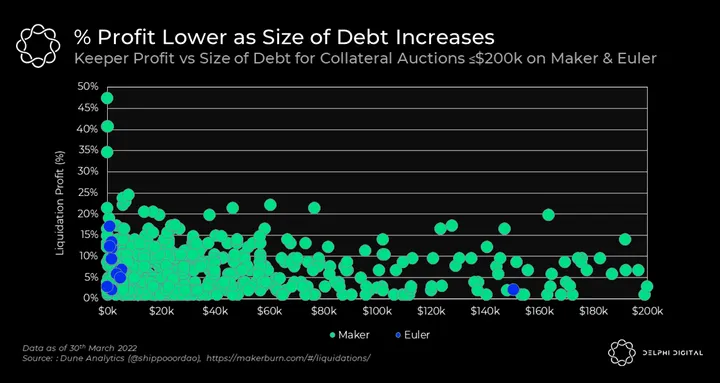

Perhaps the most useful characteristic of any form of Dutch auction is that it lets the liquidation discount vary with the size of debt, since larger loans can be liquidated profitably at a smaller percentage discount compared to smaller loans. By extension, the discount can also scale more effectively with gas costs of that particular period. During periods of network congestion, a higher percentage discount will be required to end the auction compared to lull periods all things held equal.

*Note: Liquidation Profit for Maker was calculated using 1 – (settlement amount/market value of collateral received). Settlement amount is the sum of the liquidation penalty and debt amount paid by the keeper to the protocol. Market value of the collateral receive is the amount of collateral sold multiplied by the (starting price/auction price multiplier)

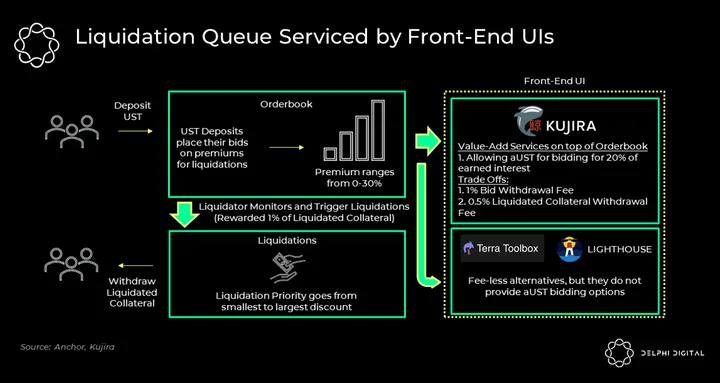

Liquidation Queue: Anchor, Kujira, Lighthouse, and Terra Toolbox

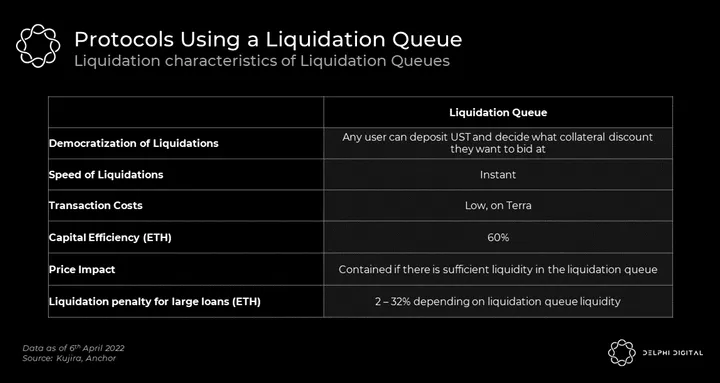

The Liquidation Queue is an orderbook of bids for purchasing liquidated collateral, currently used in Anchor Protocol’s liquidation process. Users that would like to participate in the liquidations on Anchor may place UST bids at a liquidation discount of their choice between 1-30%, in 1% intervals.

The lower the discount, the higher up it is placed on the queue. During a liquidation event, a liquidator triggers the liquidation, and the collateral is sold into those bids from the highest bid to the lowest. The collateral is distributed pro-rata tp bids within each premium interval, and not based on the time of bid placement.

For a liquidation on Anchor, the minimum penalty to borrowers is 2% (1% for Liquidator that triggers the liquidation, 1% for liquidation fee accrued to the protocol) and the maximum would be 32% (1% for Liquidator, 1% for Liquidation Fee, 30% Maximum Discount or when queue is empty). Each borrower’s drawdown is dynamic, determined by remaining bids in the liquidation queue.

A liquidation queue provides a ready source of liquidity for liquidation events. In some cases, liquidatable collateral can be sold at a lower discount compared to the fixed discount model, but this is largely dependent on the amount of liquidity and where bidders choose to place their orders. In the case of bETH on Anchor, the liquidation spread currently concentrates around the 4-10% discount level, with a maximum of 11% since its inception last year.

Kujira Orca, Lighthouse Defi and Terra Toolbox have built easy to access UIs for any user that wishes to participate in Anchor’s liquidations. Some of these front-ends, such as Kujira Orca even allows bids in aUST, where users can earn Anchor yields while waiting for their bid to be filled. For their services, Kujira charges 1% on bid withdrawal, 0.5% on collateral withdrawal, and 20% of aUST earnings when bidding for collateral with aUST. While Lighthouse Defi and Terra Toolbox do not charge fees, they also do not support the ability to use aUST for bids.

Conclusion

Liquidations are largely a zero sum game between liquidators and borrowers. Whatever the borrower loses is gained by the liquidator (and sometimes the protocol). Thus, determining the best type of mechanism depends on what type of user you are. In the summary table below, we put various protocols side by side to qualitatively examine which platform is better suited for each type of user. Generally speaking, for those seeking a slice of liquidation profits, depositing in stability pools or liquidation queues have the low barriers to entry compared to running a keeper bot.

For borrowers with large loan positions, dynamic discount auction models should theoretically be more lenient, unless they have high liquidation surcharges as in the case of the 13% fee levied by Maker. For borrowers with small loan positions, fixed liquidation discounts are a prudent choice – though it may often be at the expense of the protocol. However, nothing is a one-size-fits all solution, as each money market may have additional features and specific parameters to mitigate some of the flaws in a certain liquidation mechanism.

We believe that liquidation processes should be influential in determining which money market to use, among other considerations. An optimal process could mean more lenient liquidation penalties for borrowers, or a lower risk of socialized bad debt for lenders and token holders should the unexpected happen.

Liquidation mechanisms have largely existed in DeFi as an insignificant feature of money markets. Often overlooked are the variations that have emerged and improvements that have taken place over the last few years. It’s during periods of market volatility where these liquidation mechanisms take center stage and prove their merit.

0 Comments