🌅 Welcome!

Two crypto draft bills are front and center today. The US is trying to ban algorithmic stablecoins, while Europe may require stablecoin issuers to hold capital. When it rains, it pours.

Alameda Research is repaying loans to Voyager Digital, GMX traders on Arbitrum have their third worst week ever, and our Research team explores opportunities in NFT lending.

This is the Delphi Daily. Let’s dive in.

🚨 In Case You Missed It

- Alameda Research is repaying a $200m loan to Voyager Digital, an insolvent crypto lender. The firm will get back $160m of collateral.

- Draft legislation in the US bans new algorithmic stablecoins for 2 years. The bill also requires stablecoin issuers to seek regulatory approval.

- EU finalizes the full text for crypto legislation, which requires issuers to publish whitepapers, platforms to register with authorities, and stablecoins to hold capital.

- Binance and FTX bid roughly $50m to buy assets of Voyager Digital. Binance’s current bid is slightly higher.

- OpenSea announces support for Arbitrum.

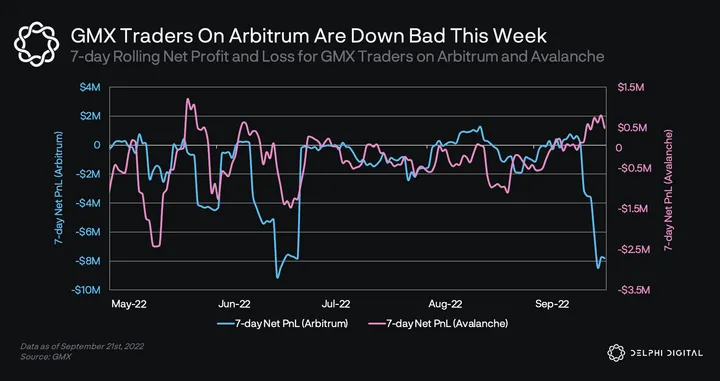

📊 GMX Traders On Arbitrum Are Down Bad This Week

- Last week, GMX traders on Arbitrum recorded the third largest seven-day rolling net loss of $8.4m on Sept 19th. During this period, open interest on GMX Arbitrum was primarily in long positions.

- However, the market moved against these traders, with ETH declining 20%. This resulted in the third largest daily loss for GMX traders on Sept 15th.

- On the other hand, GMX traders on Avalanche recorded the fourth largest seven-day rolling net profit of $803k on Sept 20th. During this period, open interest on GMX Avalanche was split even, but slightly more in short positions.

- Stats for GMX Avalanche were influenced by a DeFi trader that took advantage of GMX’s zero slippage and oracle pricing to extract over $500k of profit.

- This was done by repeatedly entering positions on GMX and manipulating the price of AVAX on centralized exchanges. Read more about these trades here.

- GMX is a decentralized spot and futures exchange that offers low swap fees and zero slippage trades. Liquidity is supplied by a multi-asset pool called GLP that earns fees from market making, swaps, and leverage trading.

- For more on GMX, Delphi members can read our Delphi Pro report here.

⚡ NFT Lending: A Rising Opportunity When NFTs Meet DeFi

- In 2020, we had “DeFi Summer.” In 2021, NFTs exploded into mainstream attention. In 2022, we see signs of a new narrative: DeFi products that enable the financialization of NFTs. Trend catchers should pay close attention to NFT finance.

- We’ve identified one vertical within NFT finance that is catching on quickly – NFT lending. This refers to protocols that enable NFT owners to take out loans against their NFTs, unlocking new avenues of liquidity.

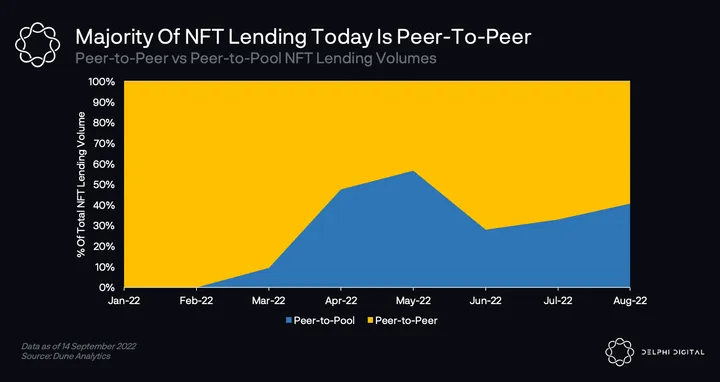

- There are two main approaches to NFT lending. Peer-to-peer lending (via NFTfi) has been the primary model for years, but peer-to-pool lending has gained attention with the launch of BendDAO & JPEG’d.

- In peer-to-peer lending, NFT owners obtain loans directly from other individuals. The product acts as a marketplace to match borrowers and lenders, functioning as a trustless middleman.

- In peer-to-pool lending, NFT owners obtain loans from a liquidity pool instead. This can be governed by algorithmically-determined parameters or set by the pool owners.

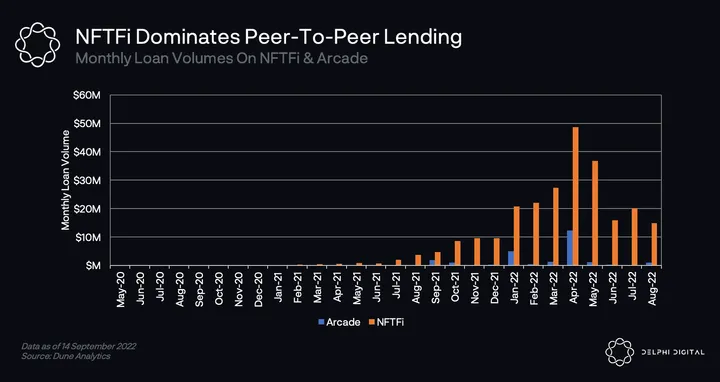

- NFTfi became the first protocol to offer NFT-backed loans via the peer-to-peer lending model starting in June 2020. It remains the most prominent protocol in this space today.

- Monthly loan volumes on NFTfi have grown parabolically since 2021, in line with the boom in NFTs. The protocol hit a peak of almost $50m in monthly loans in April 2022, before settling between $10-$20m per month over the last few months.

- NFTfi matches borrowers and lenders via its marketplace. Borrowers can list NFTs that they want to borrow against. Lenders place bids by offering terms – amount (wETH or DAI), duration, and interest rate.

- For more on NFT lending, Delphi members can read our Delphi Pro report here.

🐣 Notable Tweets

Earn NFTs from Optimism Quests

OPTIMISM QUESTS 🔴✨

Today, @optimismFND published their own series of Quests, similar to what @arbitrum has been doing

Users that complete Quests can get 18/18 Optimism NFTs

Note: 14% of $OP is still ready to be airdropped 🪂

Quests below 👇

— olimpio.lens ⚡️ (@OlimpioCrypto) Sept 21, 2022

Protocols for Undercollateralized Institutional Lending

Institutional Lending is gradually becoming the fastest-growing segment in DeFi.

Best of all, you can earn ATTRACTIVE RETURNS on your stables, lending to these institutions.

Here are 7 exciting projects offering undercollateralized lending to the capital markets.

🧵🪡..

— Viktor DeFi 🛡 (@ViktorDefi) Sept 21, 2022

0 Comments