Policy Paper Series (Part 1): Reframing How We Look at a Crypto Legislative Solution

MAR 17, 2023 • 35 Min Read

This paper is authored by Sarah Brennan (GC at Delphi Ventures and Delphi Research), Gabriel Shapiro (GC at Delphi Labs), and Marc Goldich (GC at Proximity Labs) on behalf of LeXpunK.

Premise

The U.S. crypto regulatory dialogue needs a fresh approach.[1] In this series of papers, we explore a new foundational regulatory framework for public, permissionless blockchain-based networks that we believe will have strong public and political resonance[2] while actually promoting decentralization: a disclosure based-model with antitrust-like policy[3] underpinnings focused on regulating systemically important vertically-integrated centralized actors who dominate crypto-ecosystems.

In crypto, vertical integration implicates distinct systemic risks as it poses the risk of conflicts, engagement in anti-competitive behaviors, and market manipulation. As we have seen from the various implosions of sizable market actors this past year, most notably FTX, these centralized parties constitute the largest source of market instability, customer/user losses, and contagion risk. However, within the broader crypto ecosystem, the 2022 fallout was contained to centralized parties with counterparty risk and served as a real-time litmus test of the degree of dependency around the efforts of one or more centralized actors. We suggest that the fragmentation and decentralized nature of the space provides additional market robustness by design. This characteristic is both an improvement over traditional markets and one that regulation should seek to enshrine and protect.

We also believe that crypto gives rise to many novel questions, mandating the need for further exploration with policy makers to arrive at a sensible end point on many issues. However, from a policy perspective, regulators are very experienced and adept at recognizing and addressing the dangers posed by centralized actors engaging in anti-competitive behaviors. Solving for risks created by large market actors addresses contagion risk and does so in a much healthier way than engaging in ‘asset-specific’ discriminatory policies seeking to cut crypto off from traditional markets and the broader economy. For these reasons, we propose a rules-based intervention that specifically seeks to mitigate systemic risks created by large market actors operating on- and off-chain in systemically-important blockchain ecosystems. We strongly believe any workable regulatory scheme must respect, preserve, and reinforce inherent characteristics of public, permissionless blockchain-based networks, namely decentralization and disintermediation, to meaningfully advance the continuity and health of the space. This proposal seeks to minimize elements of centralization and permissioning, while assigning regulatory burdens to the subset of systemically important large market actors that are most likely to cause, and most able to ameliorate, risk on a ecosystem-wide scale.

Core Concepts: Regulate Centralized Systemically-Important Crypto Institutions, Not Software or Developers

A. Thesis

Our thesis is that crypto-regulation should be focused on preserving the aspects of crypto that make it unique and in need of a distinct regulatory scheme, namely decentralization and disintermediation, instead of focusing on particular technology layers, technology developers, or technology services providers. For this reason, as well as the reasons we describe in more depth below, we propose a regulatory focus on systemically important vertically-integrated crypto enterprises (“VICE”s) that have amassed significant power within the industry and thus are positioned as sources of hidden centralization and systemic risk while also being positioned to adopt, propagate, and enforce best practices within the crypto ecosystem. Examples of such VICEs include institutions that directly or indirectly own, operate, or control systemically important combinations of the following functions:

- owning/operating major crypto infrastructure (RPC nodes, archive nodes, etc.)

- owning/operating major consumer applications or hardware (wallet apps, wallet hardware, etc)

- providing major financing for cryptosystems development or maintenance

- providing major custodial cryptoasset platforms, services, or asset-backed tokens (CEXs, stablecoin issuers, etc.)

- planning/developing/maintaining major crypto protocols (L1 client core development teams, etc.)

- performing major market-making or other major secondary market roles

- owning/operating a major proportion of the means of consensus production (miners, validators, governance tokens etc.) within cryptosystems

In crypto, vertical integration poses distinct systemic risks as it poses the risk of conflicts, engagement in anti-competitive behaviors, and market manipulation as each L1/2 constitutes a microeconomy within the broader crypto ecosystem. We therefore believe that ‘vertical integration’ creates distinct risks and propose that when a particular institution becomes ‘vertically integrated’ by engaging in two or more of the aforementioned types of activities above a certain market share, the institution has become systemically important, either within a systemically important crypto sub-ecosystem or the crypto ecosystem on the whole – and thus poses marketwide systemic risks. To prevent the build-up of undisclosed systemic risk, discourage hidden centralization, foster adoption of best practices, and ensure a level playing field, VICEs could be required to:

- publicly register as systemically important crypto institutions with existing regulatory authorities;

- provide detailed periodic public disclosure of their crypto activities along the dimensions described above;

- provide detailed periodic public disclosure of their holdings/ownership of crypto assets and crypto technologies;

- be subject to heightened standards of due care, due diligence, and management of conflicts of interest and internal controls; and

- be subject to annual compliance audits in relation to the above.

Importantly, this regulatory system should be globally adaptable,[4] rules-based, disclosure-focused, and decentralization-compatible. Crypto necessitates a unique regulatory scheme solely to the extent it retains its unique characteristics.[5] The regulations, in their focus on market health, should reflect antitrust concepts, as uniquely positioned for crypto economic models, to discourage market capture (via disclosure and the imposition of regulatory costs) by systemically important institutions (which centralize power and risk) while minimizing potential risks posed by any such institutions acting singularly or in concert.

B. Lessons from the 2022 Crypto Collapse: Systemic Crypto Risk is Institutional

Crypto has unique premises and characteristics that need to be grappled with, such as how to ensure soundness[6] of decentralized trustless systems. These core tenets require reinforcement for overall market health. In particular, regulating VICEs is both a significant step forward to ensuring safety and soundness and perhaps an obvious one that US regulators are well positioned to pursue as the policy goals around regulating large market actors are consistent with preventing long-acknowledged market risks arising from centralization, monopolistic behaviors, and contagion. We were granted a glimmer of how the market behaviors of large institutions and contagion can impact market stability in 2022 after the collapse of a number of actors allegedly due acts by FTX and Alameda, ending with the collapse of FTX’s empire on the whole. Each of these actors were centralized intermediaries with large market shares performing a host of functions in the crypto space and they interacted with one another as one might expect in traditional markets to create counterparty risk – as lenders, investors, and rehypothecators of customer assets. Unsurprisingly, the implosion of one or more of these actors set off a daisy chain reaction of collapse and insolvency.

However, in a somewhat novel fact pattern, the collateral damage and contagion was more limited and targeted to specific ecosystems within crypto with dependencies on these actors, notably Solana. Yet, the damage across the market was distinctly limited, with even Solana exhibiting a solid recovery. In this way, the collapse served as a real-time litmus test of the degree of dependency around the efforts of one or more centralized actors.[7] Though there are lessons inherent in the scope, spread, and extent of contagion, banking regulators viewed the lack of contagion as a lucky accident based on crypto’s small overall market size or limited exposure of traditional markets. Regulators should perhaps give more credence to the fact that the fragmentation and decentralized nature of the space provides additional market robustness by design. We suggest that this characteristic is both an improvement over traditional markets and one that regulation should seek to enshrine and protect.

As an added benefit, while cryptosystems have many novel aspects, a focus on preserving competition is not a novel construct. U.S. regulators have an abundance of experience in regulating monopolistic behaviors. The U.S. value-system upholds that competition is healthy and produces better outcomes for consumers. Our proposed framework will serve to help bring crypto in a larger public policy framework by policing the behavior of big market actors while addressing and installing actionable regulatory mechanisms to police and deter “decentralization in name only” (DINO) market actors on a macro level. This regulation draws a line in the sand for decentralized tech, through acknowledgment that existing law has assumptions baked into it which are inconsistent with the paradigm shift in crypto and regulates the new risk created based on how things are intended to function. It forms a baseline to push back on regulators applying laws that presume things (must) “function” a certain way (e.g., requiring an intermediary; the intermediary is a person capable of bad acts and a black box) and making room in the assumptions in law to accommodate decentralized trustless structures while/ if there are centralized pieces, which of course there often are, those are deserving of the traditional regulatory gloss.

C. Methodology: Functionalism and Rules vs Layerism and Principles

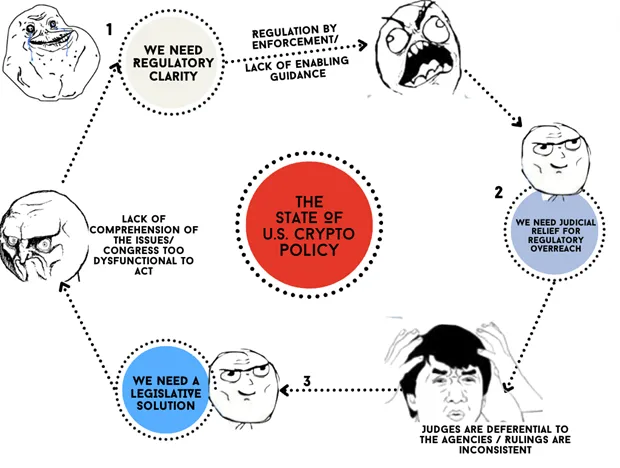

Status Quo: A Problem Statement. We have now spent close to a decade waiting for principles-based guidance to provide clarity to the crypto space. If we, for a moment, stop assuming the calls for regulatory clarity are disingenuous but rather are based on the deep aching need for a viable and compliant path forward, we can start to talk seriously about potential solutions that could serve regulatory goals and the common good.

Principles-based regulation[8] has a reputation for being more flexible and leaving room for continued innovation and change. This has not been the case for crypto in the U.S. As we have learned, principles-based frameworks are also extremely susceptible to regulatory discretion. In situations where flexibility for innovation is needed, credible regulatory engagement of industry is key to counterbalance the inherent costs of regulatory uncertainty these frameworks create.[9] Regulators must also think carefully about proportionality of regulatory requirements across a broad range of interests to preserve opportunities for broad participation. The tradeoff from bright line rules also necessitates somewhat of a reliance on enforcement to dictate the boundaries of acceptable behavior. Enforcement in a healthy principles based-framework must in turn balance fairness and fair notice concerns. Without a credible regulatory culture that has (i) been predictable, responsive, and reasonable and (ii) accountable for its impact on market participants, we have to look seriously at our options to overcome this impasse.[10]

In a sector where regulators have long been given the leash to wield principles-based rules and their flexibility such that they apply wholesale to any and all things, we have had ample time to see the results of such efforts. Notably, they have produced an unworkable situation where regulators focus more on compliance with existing processes than outcomes. They have weaponized ambiguity to impede innovation, block capital formation, and invite chaos as well as disrespect for the rule of law through their unwillingness to embrace any meaningful and sustained effort to develop frameworks[11] to provide a viable path forward. This state of affairs has been made worse by the extreme lack of urgency in providing enabling guidance[12] and the focus on using law as a blocker.[13]

The current state of U.S. crypto policy provides builders and advocates with an absurdist “groundhog day” scenario of looking between the other branches of government for checks and balances on agency power. Without meaningful engagement from either, principles-based regulation has become a king-maker in the U.S. for ambitious heads of regulatory agencies.[14] In the vacuum created by Congress failing to act and judges failing to push back, we now have agencies aggressively seeking to manifest their own rule of law into existence. What has become particularly clear is the need for some level of constraint on agency discretion limiting the ability to take on an “activist” policy making function.[15] We cannot have a system where a regulator’s discretion serves as the sole determinant as to whether new business models can proceed or are deemed per se illegal. Otherwise, as a builder, you are at the whim of each administration’s appointee and left to your fate as to whether you receive a benevolent ruler or not.[16] The fact that economic outcomes are at the mercy of a political appointee picking their favorite way of doing business is antithetical to basic American principles of promoting entrepreneurialism, capitalism, and free markets. Crypto is unlikely to be ‘put back in the bag’. What is more likely is that the industry will continue to grow, although increasingly offshore, while the US loses significant competitive advantages because US regulators have lost the larger plot in their zeal to exterminate it. They ignore the policy rationale behind applying rules (just because you could, should you – does it serve a purpose within the legislative intent of the law)[17] and more broadly, they cite consumer protection as their main impetus but are systemically undermining consumer safety as well as their remaining mandates. America largely attributes its success on the world scale due to its distinctive adherence to the rule of law, belief in capitalism and a free markets approach. We need to reconnect with these key tenets of the American economy and pivot from the unwinnable battle of stomping out a fledgling industry that is actively being brought within public policy frameworks around the world.

In addition to the above cited issues with the U.S. regulatory stance, recent hopes for judicial relief have been quashed. The current state of regulation by enforcement, if and when regulators are challenged in court, is leading to the rise of a patchy common law layer of incoherent and myopic judicial decisions that fail to understand the implications of the ruling and are largely deferential to the regulatory agency enforcement prerogatives.[18] These, combined with the countless settlements of enforcement actions[19] by those parties who choose not to fight or who lack the resources for a protracted battle with the regulators, are now relied upon by courts for persuasive authority.[20] The effect is to rubber stamp the application of principles-based tests beyond credulity and further narrow any U.S. path forward in a timeline where other jurisdictions are moving to propose, receive public comment and pass entire enabling regulatory schemes. While some of this is a product of our federalist system and we may have more coherent outcomes through appeals, this is a very long ways off.

Notably, the majority of these regulatory schemes outside of the U.S. that embrace innovation take functionalist approaches.[21] While we believe a functionalist approach is the correct one (i.e., the focus should be on regulating based on “function,” not all front ends perform the same functions),[22] we should also be very careful not to create barriers to entry and regulatory moats. Although a crypto-specific functionalist approach represents somewhat of a reset in the U.S.,[23] applying a narrowed functionalist approach would have the inherent benefit of breaking this impasse of crypto existing outside of public policy frameworks thereby allowing us to catch up and keep pace with our European counterparts and ensure a cohesive global regulatory landscape.[24] This serves the greater good by keeping the U.S. globally relevant among free market economies in the long term and fostering capital formation in a safe, responsible manner that draws from global lessons learned.[25]

Problems Inherent in Layerism. However, instead of adopting functionalist approaches, we have seen a wave of industry-sponsored U.S. regulatory proposals that double down on principles-based frameworks to subdivide how we regulate based on variations of a “layering” approach.[26] We believe these approaches would do more harm than good. They build on top of existing principles-based regulatory frameworks thereby doubling-down on the problematic discretionary elements of these frameworks. In addition, these proposed approaches reflect certain flawed premises, including: (i) using new sets of principles-based frameworks to subdivide how we regulate based on variations of a “layering” approach (e.g., to focus regulatory attention on the “app layer” as opposed to the “base layer” (or L1))[27] and (ii) burden shifting – attempting to focus regulatory attention and compliance cost on a specific set of actors, without regard to whether those actors can or should bear those burdens. Our position is that these premises are inherently flawed in the following ways:

- it is not feasible to distinguish between the “layers” of a blockchain stack in a coherent, non-superficial way;

- while well intentioned in this respect, these efforts incorrectly assume regulators will refrain from expanding the scope of their oversight to actors or activities where regulation is most disruptive, costly and has few practical benefits; and

- the proposals ignore[28] the follow-on effects of focusing regulatory attention on certain types of actors (i.e. front ends, developers), in that this is likely to create or entrench monopoly, incentivizing regulatory capture and increasing systemic risks from centralization.

With respect to “layerism,” we join calls to fight against proposed regulation that would impose requirements at the base layer that cannot be met. However, outside of a defensive context, we do not think it is a broadly viable strategy to advance as regulators become aware of the levers they can pull at L1. It would be naive to assume regulators will somehow agree to categorically tie their hands behind their backs on regulating the base layer.[29] At the same time, other efforts have sought to establish principles-based frameworks to regulate categories of market actors such as “front ends” or developers without careful thought to the systemic implications of the regulatory moats created.[30] Moats lead to centralization, market capture, and permissioning regimes. Crypto is only distinct from traditional enterprise and in need of separate regulatory treatment through its ability to enable decentralized and disintermediated economic activity, which, if we are crafting a bespoke regulatory framework, should be reinforced and preserved.[31]

Finally, the suggested approaches will not bring clarity and bright lines but rather would “layer” additional principles-based ambiguities on top of the existing principles-based ambiguities. This will only exacerbate the issues we have with regulatory (prosecutorial) discretion and the ability and flexibility to wield law as a blunt weapon.

Our Position. Broadly speaking, if we have a shot at a legislative solution in the US, we strongly believe that any regulatory framework established should be rules-based, enabling, narrow, prescriptive, and clear cut. It should also:

- provide definitively where the existing “frameworks” apply as well as where they do not apply;

- recognize that decentralization and disintermediation is what makes this area unique, seek to regulate around this construct with an eye to preserving it;

- codify safe harbors and de minimis thresholds to preserve innovation and prevent regulatory moats; and

- limit the discretion of regulators in continuing to engage in jurisdictional turf wars.[32]

Recognizing the unique attributes of blockchain networks that justify a bespoke regulatory approach, we suggest a rules-based solution to overcome the existing stalemate in arriving at a workable foundational regulatory regime. Our existing body of laws are based on assumptions – namely, that we can solely conduct economic activity (at scale) through centralized intermediaries. This baseline assumption is antithetical to crypto’s ethos and its value proposition. Any workable regulatory scheme must respect, preserve, and reinforce inherent characteristics of public, permissionless blockchain-based networks, namely decentralization and disintermediation, to meaningfully advance the continuity and health of the space. Such a framework should look to minimize elements of centralization and permissioning while assigning scaled regulatory burden to address risks created to the market actors that (i) cause such risks on a material scale; and (ii) are therefore deserving of (and able to bear) compliance costs.

In the midst of regulatory agencies seeking to rubber stamp existing law onto decentralized technology without regard to whether the same risks apply, the U.S. needs a Congressional reset to engage in a meaningful examination of when the existing law cannot be applied to sensibly address risks. This examination should also be based on “function” rather than apply a wholesale “layer-based” approach focused on where a product, service, or technology sits in the tech stack (base layer, app layer, etc) to be able to address risks coherently. To be clear, we think that crypto specific legislation is essential for clarity but must also be enacted in tandem with (i) efforts to further create regulatory swimlanes; (ii) efforts to modernize existing regulatory and legal frameworks, to ensure that the regulation works with the realities of the technology; and (iii) where needed, regulatory guidance for navigating these frameworks.

The goal of this foundational rules-based framework is to be enabling instead of blocking, the prescriptive elements provide guardrails and sandboxes so that creativity can thrive within these guardrails. However, we acknowledge that any rules-based regime is prone to a level of rigidity that can be problematic. We look at this effort as a means to break the untenable status quo. This is why such regulation must be narrowly tailored to address risks on their face, acknowledging that the underlying risk will be particularized to the type of market actor and activity at hand, while doing as little collateral damage as possible.[33] We can apply these baseline assumptions – that any crypto specific regulation should be rules-based and functionalist to a small number of key areas that need to be addressed to help ensure “fair, orderly and efficient markets” and responsible innovation. By crypto specific, we mean such regulation would be narrowly tailored in that it will be focused on addressing crypto-specific paradigms and resulting risks that are not directly contemplated or otherwise capable of being covered by existing regulatory regimes.[34]

While rules-based legislative efforts have also had their failings in crypto, the fatal flaws of the NY Bitlicense, for instance, were not attributable to the presence of prescriptive measures in and of themselves. The fatal flaws were its overbreadth and the fact that New York chose to regulate a wide swath of crypto-adjacent market actors, from multibillion dollar enterprises to start-ups, uniformly and at the most onerous level as financial institutions/banks. This type of regulation still could make sense as a regulatory regime, if and to the extent the market actor is in fact a bank or custodian and the law is tailored to how they function. The more recent attempts at functionalist approaches fail in that the proposed legislation attempts to place the majority of the regulatory burden on a single category of market actors, such as developers (Lummis) or front ends (SBF DCCPA approach to DeFi) without (i) de minimis carve outs and scaled compliance obligations, or (ii) tailored approaches to address risk based on further analysis of whether such actors can and should bear the regulatory burdens associated, whether the impact would lead to suboptimal results in the market, like monopolies or regulatory moats. Addressing large and important market actors first makes sense on a number of levels – across the board, legislation assumes higher standards of conduct for such institutions commensurate with their size, the importance of the role they play and the harm they could cause. These actors should bear more regulatory burden for the foregoing reasons and have the size, scale, and resources to undertake such levels of compliance.

Our Goals. Within these constructs, this paper series puts together a baseline premise to scope out a set of results-driven regulations to address systemic risk by analyzing and balancing the interests, rights, obligations, and potential conflicts of market participants against public policies that aim to mitigate such risks. In the next installment of this series, we will use a rules-based approach to walk through and frame how new VICE legislation might be crafted in crypto.

In order of priority, we think it is first most important to define VICEs. We have proposed a definition that focuses on vertically integrated enterprises performing multiple functions in systemically important crypto ecosystems at scale. Thought must be given to the thresholds for systemic importance. Once defined, we craft a regulatory approach to VICE market conduct, looking at their functions to address potential catastrophic risks in crypto, ranging from infrastructure providers to monopolists[35] and institutions that are “too big to fail”. We have chosen to address these institutions largely in the wake of lessons learned from 3AC, BlockFi, Celsius, DCG, and most notably FTX. These institutions cause risk and need to be addressed head-on. We have undertaken this effort to show that the response can be enabling and targeted to risk as opposed to the current protectionist, politically-oriented responses – (i) publicity-driven enforcement actions announced beside the dead carcasses of these market actors and (ii) on the Federal level, initiating a widespread denial of service attack aimed at cutting off crypto from the traditional finance sector. These efforts are counterproductive; they continue the U.S. regulatory positioning of being the continual proximate cause of harm to crypto market stability and efficiency as well the cause in fact of harm to the U.S. populace – those they serve.

Our goal here is to break out of these reactive measures, to reframe how we look at a policy solution, and to introduce a proactive framework that identifies and solves for these unique risks. This cannot be done in a vacuum, however – regulators must put in the hard work of producing practical, enabling guidance if they genuinely desire to have the space brought into public policy frameworks as opposed to just producing soundbites for media appearances.

In the interim, we welcome your feedback and thoughts on the premise. We would also like to extend our thanks to our peer reviewers for their valuable feedback to date.

Resources

Annex I – Visual of Blockchain Application Layers

Footnotes

[1] The current U.S. regulatory posture toward crypto is untenable. The impasse amounts to an outright clash of values with regulators largely seeking to reinforce the supremacy of incumbent centralized paradigms. See, e.g. most recently the media statements from the Chair of the U.S. SEC suggesting he views the crypto space (Bitcoin excepted) as essentially illegal and without merit (see Ankush Khardori, NY Mag, Feb 23, 2023, “Can Gary Gensler Survive Crypto Winter? D.C.’s top financial cop on Bankman-Fried blowback”. Cf. various responses from crypto proponents, e.g., @lex_node on Twitter commenting “what’s the plan here” and that Chairman Gensler essentially seems to be seeking to wipe out ~$663B in value.

[2]A shift in public discourse from charged political rhetoric to productive dialogue is essential. This means recognizing our own failings as an industry and proactively advancing the conversation to address substantive and legitimate public policy concerns. As SEC Chairman Gensler is fond of saying, “If we really think the crypto world is going to be part of the future, it needs to come inside a public policy envelope,” see e.g., Bloomberg Daybreak Americas October 15, 2018 media appearance. The question at hand is what the policy envelope looks like – does it constitute an entrenchment of incumbents and a binary decision for crypto proponents to conform to existing norms (which are largely unworkable) or operate in the shadows? Or, instead, as is our hope, is there room for a policy framework that acknowledges there is an “adapt or die” element and recognizes shifting societal norms and values. For commentary around crypto as indicative of a broader societal shift, see, e.g. Gamestop Tale Exposes Regulatory Paternalism and DeFi’s True Value.

[3] We are indeed aware of the irony that the existing antitrust framework is principles-based. However, it is also subject in its application to the same ills described herein, namely uneven application of the law and extreme prosecutorial discretion in its enforcement. It is also subject to a broader set of issues that would need to be addressed in our framework around federal preemption and how the law interacts with other regulatory regimes. As we will build upon in our next paper, we suggest a rules-based application, taking firmer lines on ‘per se’ behaviors that fall within scope with a broader spectrum of remedies.

[4] Capable of being integrated across markets with an eye to reciprocity. We are conscious that a U.S. proposed crypto-specific regulatory scheme should not be so broadly prescriptive and draconian that it is unable to interact coherently with other well-reasoned regulatory regimes. Our focus on regulating specific market actors that touch and impact markets with a U.S. nexus reflects a balance between regulating the behavior of U.S. facing actors while recognizing/respecting the transnational nature of the market and the decentralized nature of the technology.

[5] It will be important to further distinguish what falls within/without this framework – as we will spend more time developing in our next installment, definitionally, when we say crypto, we mean public and permissionless technology.

[6] There is a broader risk set created by the technology, including the need to address security vulnerabilities and hacks. While we aren’t covering infrastructure risk in this paper, for instance, we feel that the principles proposed in our framework constitute the largest and most achievable step toward market stability. Thereafter, addressing and managing risk on-chain can be addressed through disclosure best practices.

[7] See Report of the Cornell SC Johnson College of Business: Cornell Convenes 2022 Roundtable Forum on Digital Assets, Chapter 3, June 6, 2022 (noting that based on quantitative data, DeFi appears to have weathered the downturn without major incident).

[8] “Principles-based regulation relies upon substantive standards or objectives imposed on industry members to achieve legislative purposes. It imposes a general standard for conduct—leaving it to the discretion of regulators to decide if particular conduct should trigger a sanction. On the other hand, rules-based regulation relies upon detailed, prescriptive requirements, specifying in advance what specific actions will be penalized.” Vincent Di Lorenzo, N.Y.U. Journal of Legislation & Public Policy, Principles-Based Regulation and Legislative Congruence (2012).

[9] These dynamics are very well described by Cristie Ford, Principles-Based Securities Regulation: A Research Study Prepared for the Expert Panel on Securities Regulation (12 January 2009).

[10] Id. (describing the concepts in this section in depth).

[11] See William Hinman “Digital Asset Transactions: When Howey Met Gary (Plastic)”, June 14, 2018; see SEC “Framework for Investment Contract Analysis of Digital Assets” (and SEC reversal) as well as variance in how to approach regulating crypto, detailed here; see Commissioner Peirce “Token Safe Harbor Proposal 2.0”, April 13, 2021, which safe harbors have not yet received the consideration they deserved.

[12] We are told that it is simple to comply with existing frameworks, despite fundamental incompatibility of these laws to decentralized models and crypto use cases. Calls that the law is simple, one must simply choose to stop violating the law and seek to comply are uniformly disingenuous. Yet, they persist. See e.g. Kennedy and Crypto, September 8, 2022, (“No honest business need fear the SEC” and “Not liking the message isn’t the same thing as not receiving it.”); as recently as February 2023 (“They were not complying with that basic law“) Chair Gensler on CNBC’s “Squawk Box; SEC Office Hours “Kraken to End Staking-As-A-Service”, Feb 9, 2023 (Chair Gensler suggesting all one has to do is fill out a form on the SEC website); cf. Jesse Powell on Twitter, Feb 9, 2023 (“Oh man, all I had to do was fill out a form on a website and tell people that staking rewards come from staking? Wish I’d seen this video before paying a $30m fine and agreeing to permanently shut down the service in the US. How dumb do I look. Gosh.”).

[13] See LBRY on Twitter, stating that their biggest misjudgment is taking the SEC at their word to come in and talk to them as it made them an easy enforcement target;see examples of threatened enforcement against Coinbase re “Lend” and the SEC enforcement and resulting settlement regarding Kraken’s staking program for enforcement against “good actors’ ‘ that haven’t created harm where the remedy was a shut down or absence of any viable path to market.

[14] Outside of the SEC, other regulators are unwilling to acknowledge the new paradigm, choosing instead to insinuate that because the laws are predicated on the existence and regulation (registration) of intermediaries, the economic activity cannot (and should not) take place outside those constructs. See Chairman Benham Keynote Address, Brookings Institution Webcast on The Future of Crypto Regulation, July 25, 2022 (“Our guiding statute, the Commodity Exchange Act (CEA), and regulations create a principles-based system aimed at accomplishing execution certainty by ensuring transparency, integrity, and security of transactions. We facilitate customer protections through intermediary oversight”.); see Chairman Berkovitz, June 8, 2021, Keynote Address Before FIA and SIFMA-AMG, Asset Management Derivatives Forum 2021 (stating that regulation has been predicated for hundreds of years on regulating intermediaries, “[a] threshold question is whether the public will benefit from disrupting the current financial system that relies extensively on financial intermediaries….A system without intermediaries is a Hobbesian marketplace with each person looking out for themselves….Not only do I think that unlicensed DeFi markets for derivative instruments are a bad idea, I also do not see how they are legal under the CEA. The CEA requires futures contracts to be traded on a designated contract market (DCM) licensed and regulated by the CFTC….DeFi markets, platforms, or websites are not registered as DCMs or SEFs [swap execution facilities]. The CEA does not contain any exception from registration for digital currencies, blockchains, or smart contracts.”)

[15] This is a larger issue in the U.S., see the Supreme Court taking up a challenge against the Consumer Financial Protection Bureau that could serve to limit the power of independent agencies. For a broad overview, see N.Y. Times, Feb. 27, 2023, Supreme Court to Take Up Case on Fate of Consumer Watchdog; see also e.g. Wall Street Journal, Feb. 28, 2023, “Justices Question Role of ‘Major Questions’ Doctrine, for an overview of the public discourse around the “major questions doctrine” as a limit on agency rule (the “major questions doctrine… calls for restricting federal agencies from enacting regulations with vast economic and political significance without first getting explicit direction from Congress”).

[16]The viability of this path is evidenced by the very few successes (less than a handful, if that). Existing registration schemes are also predicated on effecting transfers through the use of transfer agents and those equity securities being exclusively custodied by intermediaries, making them fundamentally incompatible with P2P technology nevermind the lack of SEC approved liquid trading venues. See, e.g. Coinbase, July 21, 2022 Petition for Rulemaking – Digital Asset Securities Regulation (requesting particularized regulatory clarity across a broad spectrum of key areas).

[17] For instance, if the principles-based frameworks defining what falls within securities laws would allow a regulator to colorably apply securities laws, and the aim is adequate disclosure, would consumer-facing laws serve that purpose with less collateral damage?

[18] See Commodity Futures Trading Comm’n v. Ooki Dao, 3:22-cv-05416-WHO (N.D. Cal. Dec. 20, 2022); Sec. & Exch. Comm’n v. Ripple Labs, Inc., 20-CV-10832 (S.D.N.Y. Sep. 21, 2021); Sec. & Exch. Comm’n v. LBRY, Inc., 21-cv-260-PB (D.N.H. Nov. 7, 2022); SEC v. Telegram Grp., No. 19 Civ. 9439 (PKC) (S.D.N.Y. Nov. 25, 2019); U.S. Sec. & Exch. Comm’n v. Kik Interactive Inc., 492 F. Supp. 3d 169 (S.D.N.Y. 2020).

[19] For instance, the NEXO settlement, which is a product of NEXO choosing not to fight the SEC and is now relied upon for persuasive authority, thereby, along with many other administrative proceeding settlements, becoming our body of law). See Nexo Capital Inc., No. 3-21281 (Jan. 19, 2023); Sec. & Exch. Comm’n v. Wahi, 2:22-cv-01009 (W.D. Wash. Nov. 4, 2022).

[20] See, for example, Kraken to Discontinue Unregistered Offer and Sale of Crypto Asset Staking-As-A-Service Program and Pay $30 Million to Settle SEC Charges (Feb. 9, 2023), SEC Charges Poloniex for Operating Unregistered Digital Asset Exchange (Aug. 9, 2021); SEC Charges Decentralized Finance Lender and Top Executives for Raising $30 Million Through Fraudulent Offerings (Aug. 6, 2021); see also BlockFi Agrees to Pay $100 Million in Penalties and Pursue Registration of its Crypto Lending Product (Feb. 14, 2022).

[21] See Australia Token Mapping Consultation Paper, Feb 2023; see also Markets in Crypto Assets (MiCA) and the UK HM Treasury proposed framework “Future financial services regulatory regime for cryptoassets Consultation and call for evidence” February 2023.

[22] See e.g., https://a16zcrypto.com/web3-regulation-apps-not-protocols/; and https://twitter.com/BrianQuintenz/status/1613218843081510920 (arguing for layerism and a focus on front ends) For an in-depth analysis of competing approaches to regulating crypto as it relates to tokens, see “How SEC vs. Ripple Stems from an Age-Old Philosophical Debate: essentialism vs. functionalism, redux”, May 10, 2021.

[23] Meaning that the proposal isn’t intended to build on top of existing bodies of law around securities or commodities designations but is intended to be distinct standalone legislation that addresses market stability on its face. There are academic comparative law arguments that can be applied to regulating distributed networks that are almost immediately global by looking at the problems to be solved (“in reality, as long as institutions are non-universal, only problems can play the role of a constant” across jurisdictions “our analysis should move from a substantive to a functional one and focus on what it does, instead of what it is.”) see e.g., Christopher Wytock, BYU Law Review, Dec. 18, 2019 Legal Origins, Functionalism, and the Future of Comparative Law.

[24] Obviously there are limits to the prospect of a globally coherent regulatory landscape, for instance, governments of countries who are not proponents of free markets would be unwilling to buy into a coordinated approach.

[25] See also indications of crypto responding to U.S. posture by moving offshore (Politico, Crypto firms brace for ‘carpet-bombing moment’ in U.S. as Europe beckons, February 26, 2023)

[26] See Paradigm’s Base Layer Neutrality paper (arguing in the wake of Tornado Cash how regulation might apply but do less collateral damage). We understand the impetus, which is to minimize the amount of collateral damage that any regulation could cause in the context of the proposal, but if applied more broadly, we think we will not be able to focus regulatory attention on the layer closest to end users without regard to its role, function, or importance to the blockchain system or market as a whole.

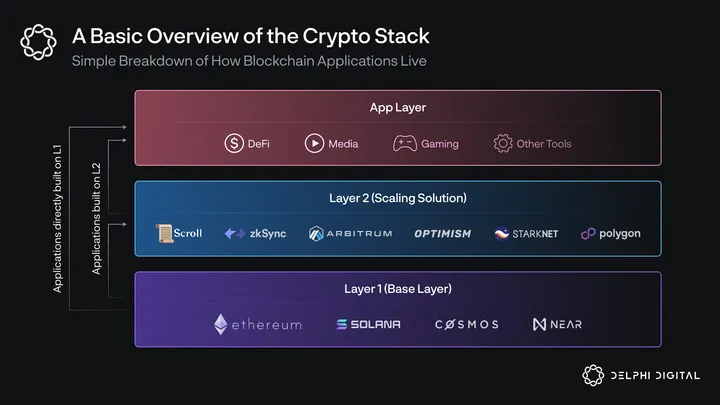

[27] See Annex I for a visual representation of layers in the blockchain tech stack pulled from Delphi Research’s January 4, 2022 report entitled “The Great Reset: Navigating Crypto in 2023”.

[28] At best, the proposers are seeking to shift the burden away from their activities without recognizing or acknowledging the impact. At worst, these are plays for regulatory capture.

[29] In fact, recent regulatory actions and legislative proposals suggest that they will continue to pursue regulation that inadvertently seeks to regulate the base layer as well as various efforts to drive the behaviors of L1 market actors such as validators and miners. See Coincenter Analysis “What is and what is not a sanctionable entity in the Tornado Cash case” discussing is the issues around OFAC sanctions re Tornado Cash, August 15, 2022; see Elizabeth Warren proposed “Digital Asset Anti-Money Laundering Act”, press release; see also Infrastructure Investment and Jobs Act and concern over the imposition of “broker” financial reporting requirements for blockchain infrastructure providers who would not be capable of complying (See e.g., https://financialservices.house.gov/uploadedfiles/2022-12-14_rm_mchenry_letter_to_yellen_final.pdf).

[30] a16z framework “Regulate Web3 Apps, Not Protocols” Series, see, e.g., and Lummis Bill assigning regulatory burdens to software developers as issuers.

[31] See, e.g. Gabriel Shapiro, Defining Decentralization for Law, LeXpunK Reg X and Safe Harbor X framework.

[32] While the same asset can indeed represent a security and a commodity, in practice the different asset classes are regulated in very different and incompatible ways and with different requirements and registration regimes. Layering these regimes produces a confusing, expensive and incoherent result. One of the biggest achievements of any legislative solutions would be to end the turf wars and the calls for multiple-agency registration regimes to layer on to the same asset.

[33] We can imagine a variety of ways to introduce flexibility and minimize the impact of prescriptive regulation, such as de minimis thresholds, safe harbors and definitions that provide clarity on when existing law does not apply but leave room for additional interpretation such as definitions around crypto assets with a catchall for yet to be contemplated functionality that exist within crypto systems under a principle of ejusdim generis (“of the same kind, class, or nature”).

[34] We say this even though there would be a lot of value to giving certainty to classes of market actors by assigning specific regulator to certain market actors performing the same tasks in crypto as they would in traditional finance and then tasking said regulator with providing guidance (ie. crypto specific custodial standards). The reverse has been proposed to date in draft legislation like the DCCPA where legislators skipped over the politics of regulatory turf battles to the detriment of crypto market participants by regulating them in analogous ways to actors in traditional finance while failing to establish swimlanes for regulators, opting instead to 2x the regulatory burden by requiring registrations with both the CFTC and SEC due to a failure to define digital assets and failing to establish de minimis thresholds as they have for traditional finance, with the result of requiring the most onerous level of registrations but with more than one regulator (neither of which have produced much in the way of enabling guidance).

[35] The threshold question of a VICE that constitutes too big to fail is determined relative to the total market size, but we can imagine that crypto L1s may each constitute a distinct submarket where vertical and horizontal integration may be at play and where, at a certain submarket size, we may need to regulate behaviors as well as by total crypto market share statistics.

0 Comments