Google started rolling out its Personal Intelligence feature to Gemini users across much of the world this week. The feature pulls across Gmail, Calendar, Drive, Photos, YouTube, Maps, and Search to give answers shaped around whatever your account already knows about you. Europe did not get it. The EEA, Switzerland, and the UK were excluded, with no date given for when (or if) they will be added in.

However, this restrictive behavior should not be in any way surprising. OpenAI’s ChatGPT is currently being analyzed under the EU’s Digital Services Act after crossing the threshold that would designate it as a “Very Large Online Platform,” and tag it with a whole new set of regulatory obligations. ChatGPT Health has been sitting in a restricted beta that skips the continent entirely. The Personal Intelligence rollout fits into the same pattern, where the more ambitious AI features either launch very late in Europe or don’t launch at all.

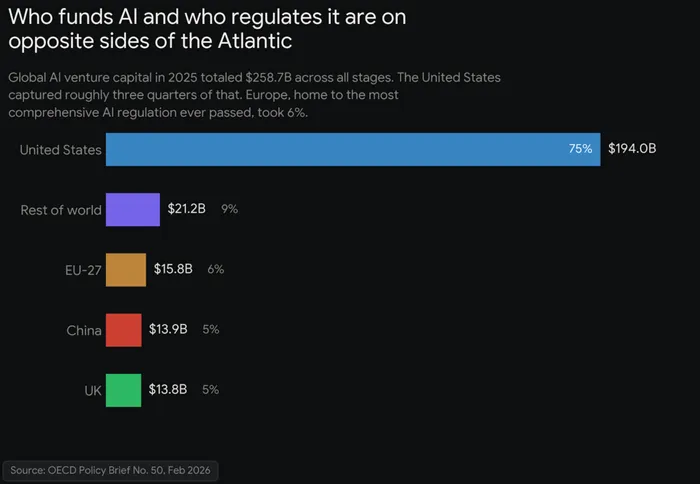

These assistants get their edge by stitching a user’s data across one vendor’s apps. The deeper the wiring, the bigger the regulatory surface. The European Union’s GDPR consent rules around cross-service profiling, DMA restrictions on gatekeepers combining data across core platform services, and the AI Act’s general purpose provisions all hit at the same seam. If your product needs ambient access to a user’s mail, calendar, photos, and search history to work, then the cost of shipping into a tightly regulated market gets expensive fast, and the easier move is to hold the launch.

I believe that the interesting read-through here is on where the design constraints line up. A lot of what decentralized AI has been quietly building maps onto a problem that is starting to show up on the centralized side. The frontier stack is looking splintered by jurisdiction, and that gives the permissionless stack a demand-side reason to exist that goes beyond the narrative.

I do think one has to be careful about the framing though, because decentralized AI is still behind on model quality by a pretty wide margin. You are not about to swap out Gemini for a Bittensor subnet and have anyone notice a difference. The centralized alternative is no longer one product for everyone. Once the US, Europe, and Asia all end up running materially different versions of the same assistant (or in some cases, no version at all), the case for a portable, compute-agnostic architecture gets easier to make.

Crypto AI has mostly been framed for the past two years as a supply-side story. Cheaper GPUs, token incentives, open weights. The Personal Intelligence launch is one of the clearer tells that the demand side is also moving. European users who want frontier assistants are going to have to look elsewhere for the time being as the gap widens. Any stack that treats jurisdictional bypass as a core feature, whether through leveraging market dominance or using loopholes like the U.S. CLOUD Act, becomes a lot more attractive the longer this fragmentation lasts. It’s worth keeping an eye on how this plays out, because it’s the kind of slow structural tailwind that tends to get priced in late.