Ostium offers lower cost of leverage and better trade execution for RWAs than traditional brokers or perp DEXs (incl. Hyperliquid). Here’s why.

Before we dive into the data, let’s quickly summarize Ostium’s infra and liquidity mechanism. The magic behind best-in-class execution.

Ostium’s Trading Infrastructure

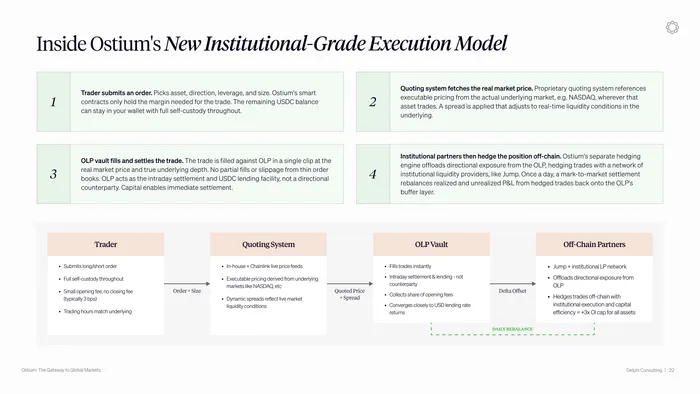

Rather than bootstrapping an onchain order book, Ostium connects onchain trades to the best pricing and deepest liquidity in traditional markets.

Onchain trades are filled against the OLP vault in a single clip at the true underlying market price, but the vault is not the directional counterparty. It acts as the intraday settlement layer and USDC lending facility.

Jump currently serves as the primary institutional hedge and flow integration layer on Ostium, transferring directional exposure from the OLP vault to positions actively managed by MMs. The capital in the OLP simply enables immediate settlement.

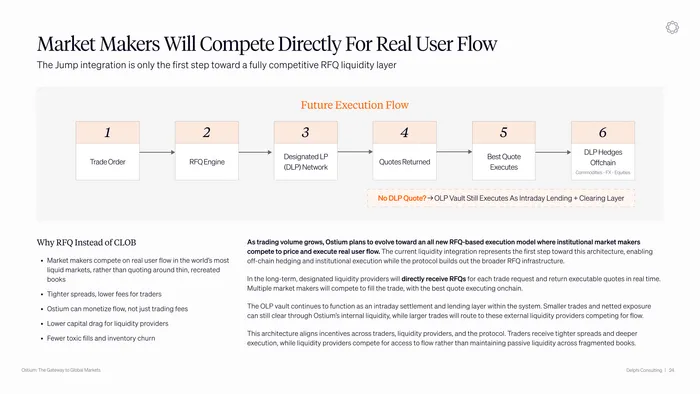

This is the first step towards a fully fleshed out RFQ layer Ostium is evolving into. In the future, designated liquidity providers (DLPs), such as Jump, will directly compete for user flow by providing quotes through Ostium’s RFQ infra. The best quotes will be executed, and the DLP will hedge them offchain.

The OLP vault will continue to function as the intraday settlement and lending layer. For smaller trades or instances where the DLP network provides no quotes, netted exposure will still clear through Ostium’s internal layer. In those cases, the junior liquidity buffer will absorb any gains and losses first while hedging directional flows. Larger trades will be routed to external DLPs competing for flow.

This sounds convoluted but it simply means that Ostium can integrate real market depth into onchain flows. It also means that Ostium is not a perp DEX. Price discovery happens in the real underlying markets, not on Ostium. An amazing perk because there is nothing worse than getting liquidated by a scam wick trading on other perp DEXs while the underlying market barely budges.

With Ostium, Onchain traders get tighter spreads, lower fees, more predictable funding, and best-in-class execution.

1. Trade Depth & Slippage

The lack of onchain liquidity in RWA order books is a real, structural problem. Market makers face basis risk between the perp and the true underlying (different time zones, settlement rails, and funding mechanics). This limits how much capital they are willing to quote in the book. And even if visible depth appears, cancel priority allows that liquidity to vanish just as quickly.

With CLOBs, larger trades are near impossible to execute without significant slippage. Even if you’re trading on Hyperliquid. At scale, order books simply break for RWA perps and cannot absorb institutional flow without material impact.

Ostium’s infra fixes this, simulating a spread that directly reflects real underlying market liquidity. Commodities execute at a flat 1-16 bps range regardless of size, while equities scale modestly. A $100k fill costs 1-5 bps, rising to 6-37 bps for a $1M trade depending on the asset.

2. Cost of Leverage

But depth and slippage are just one side of the equation. The costs you incur while keeping your position open are just as critical. Typically what you know as your funding costs for perps.

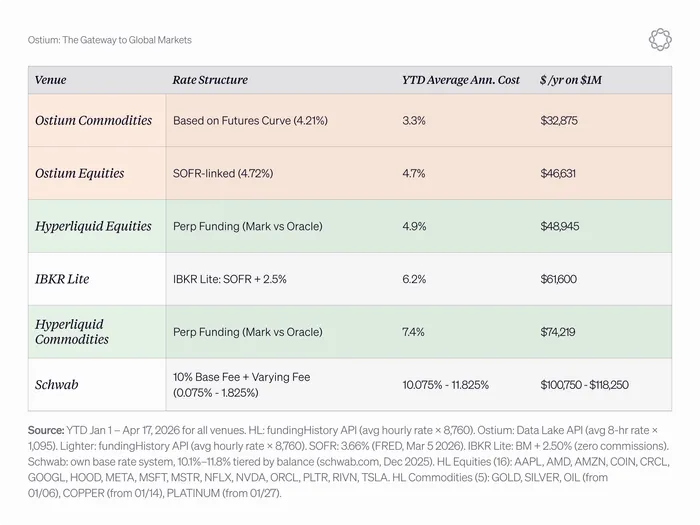

For RWAs, Ostium replaces the funding rate with real carry. The base rate is derived from the underlying market carry for each asset (SOFR, rate differentials, futures-curve shape). Expressed as a predictable rollover fee, it reflects your true cost of holding that asset in the underlying market.

Annualized, the costs you incur on Ostium are significantly lower than the funding rates at other venues.

Ostium’s average cost of carry is less than 5% annually, cheaper than even IBKR’s margin rate. Across comparable exposure, the difference between Ostium and Hyperliquid funding costs can range widely by asset.

For a strategy running a few million dollars, this can easily equate to hundreds of thousands of dollars in costs per year.

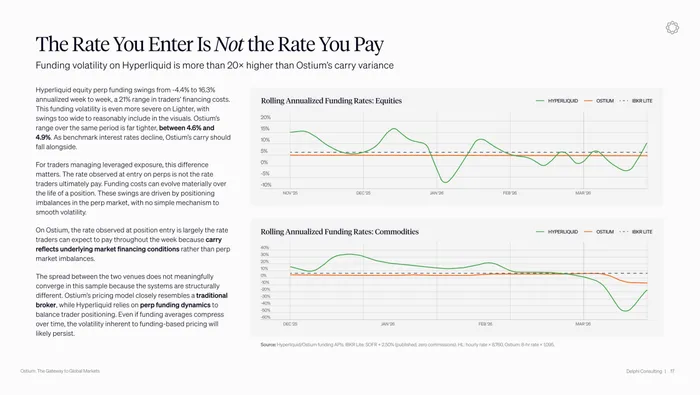

3. Funding Volatility

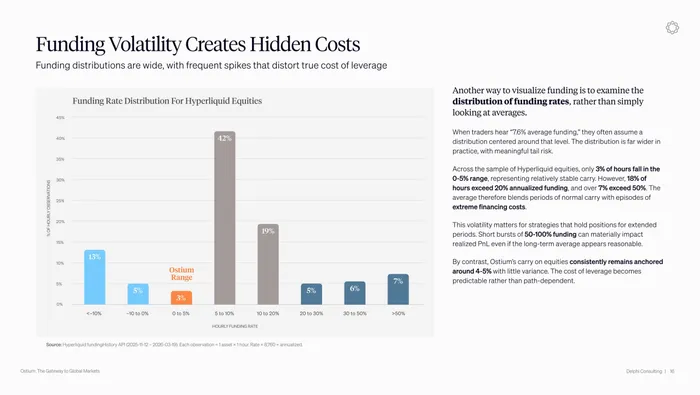

Hyperliquid’s average ~6% annual funding rate across RWAs represents a backward-looking average that masks significant volatility over time.

Funding costs are realized only after a position is opened, but fees can swing significantly during periods of market stress. So instead of looking at averages, visualizing the distribution of funding rates paints a much clearer picture. And here the difference between Ostium and Hyperliquid is even starker.

Ostium’s carry remains anchored with little variance, while Hyperliquid’s rate swings widely. So even if the long-term average reads reasonable, short bursts of high funding can materially impact PnL. Especially detrimental when you keep positions open over longer time periods.

Zooming in on rolling annualized funding rates, Hyperliquid equity perp funding swings from -4.4% to 16.3% annualized week to week. That’s a massive range in your financing costs. Ostium’s range over the same period is far tighter, landing between 4.6% to 4.9%.

TLDR: Funding volatility on Hyperliquid is more than 20x higher than Ostium’s carry variance.

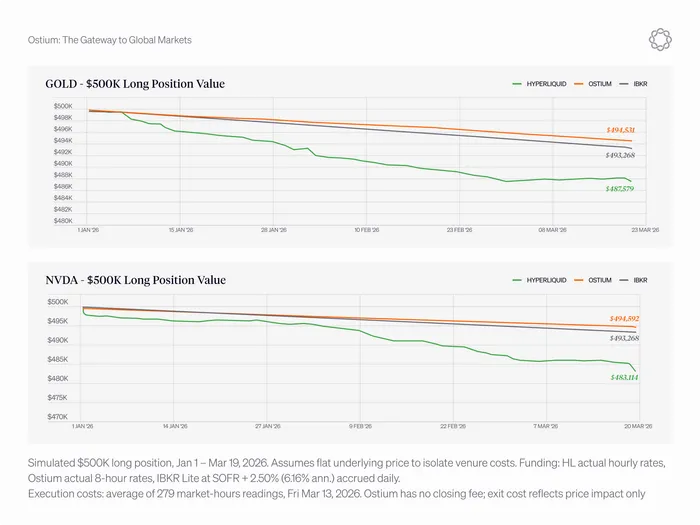

Putting it all together: Venue Choice Drives Real PnL

When you combine funding and execution, costs compound into a clear performance gap.

For example, imagine you have two positions open: a $500k GOLD long and a $500k NVDA long. Assuming no directional move, the charts below isolate the cost of simply entering and holding this exposure from January 1 to March 10, 2026.

On other venues, order book slippage creates an immediate cost on entry while market-driven funding compounds over time. On Ostium, quote-based execution removes entry slippage, and SOFR-linked carry remains stable throughout the trade.

Even compared to IBKR, one of the lowest-cost brokers, Ostium delivers consistently better outcomes over time.

And that’s why Ostium offers lower cost of leverage and better trade execution for RWAs than traditional brokers or perp DEXs, including Hyperliquid.

That’s it for a quick excerpt. Check out our full report that goes much deeper, covering the full comparative analysis, Ostium’s infrastructure and tech stack, and why this new decentralized broker model stands out.