The S&P 500 Index on Tuesday experienced its largest daily loss of 2023. In 2022, there were 23 daily losses that exceeded -2.0%, while 2021 only saw 5 such occurrences.

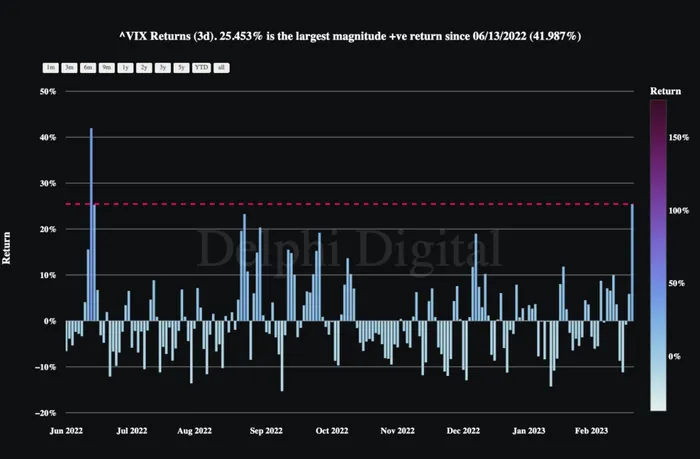

The Volatility Index (VIX) just printed its strongest 3-day return in more than 8 months, signaling that uncertainty is returning to traditional markets.

Dating back to 1990, there have been 161 occurrences of a 3-day gain in the VIX of at least 25%. Interestingly, the mean and median performance over the next 10 market sessions remain subdued. There is only a 31% chance that the relative performance over the following 10 sessions will be positive. The two most notable outliers to the upside occurred in August 2015 and January 2018.

Of course anything can happen, but it begs the question: Is this time different?