Two of the world’s most consequential non-Western economies moved in the same direction in the same week, and I am not sure the market fully noticed.

On May 19th, Japan’s governing party formally approved a framework called “Next-Generation AI and On-Chain Finance,” designating digital finance as the country’s 18th official growth investment sector. Three days earlier, Saudi Arabia disclosed that the blockchain firm droppRWA had secured $12.5 billion in tokenization mandates, with roughly $3 billion of that slated to go live on-chain during 2026.

The Japanese move is the more structurally interesting one to me. The framework is not just about yen stablecoins, though the major banks MUFG, SMBC, and Mizuho are already targeting live deployment by March 2027. It proposes tokenizing Bank of Japan current account deposits and building wholesale CBDC infrastructure on top of that. The framing from Tokyo is explicitly about monetary footprint. Japan’s influence across Asian payment corridors has been eroding for decades as dollar-denominated rails dominate cross-border settlement. A programmable, yen-native settlement layer is the country’s attempt to make its currency more portable in the region without ceding monetary policy to anyone else. Whether it works is a separate question, but the mechanism is coherent.

The Saudi play is built on different logic. Faisal Monai, who built SADAD’s original payment pipes back in 2004, pointed to a recent weekend when geopolitical tensions shut traditional exchanges while crypto markets kept running. Gulf states drew a practical lesson from that episode, aiming to capture that always-on settlement resilience for sovereign capital markets. DroppRWA already completed what appears to be the world’s first blockchain-based property deed transfer back in February, cutting settlement time from days to seconds. The next phase integrates tokenized ownership directly into Absher and Tawakkalna, the government apps Saudis already use for passports and health records. That is a distribution channel no crypto startup could build on its own.

There is also something worth noting about the contrast with China, which banned onshore RWA tokenization entirely this year. While Gulf states are racing to capture always-on liquidity for their physical assets, Beijing is closing off that channel entirely. Saudi Arabia’s digital economy already reached SAR 495 billion in 2025, representing roughly 15% of GDP, and the Kingdom recorded more than 4,000 commercial blockchain company registrations that year, a 51% year-over-year increase. The direction of travel is not subtle.

For crypto readers, the live question is how porous the boundary stays between these permissioned sovereign layers and the open infrastructure underneath them. The stablecoin primitives, the tokenization standards, and the programmable settlement logic both Japan and Saudi Arabia are borrowing from crypto tooling are composable in ways that point outward. Sovereign stablecoin corridors, once live, create liquidity density in networks that also run permissionless assets. The two layers are not as siloed as the policy documents might imply.

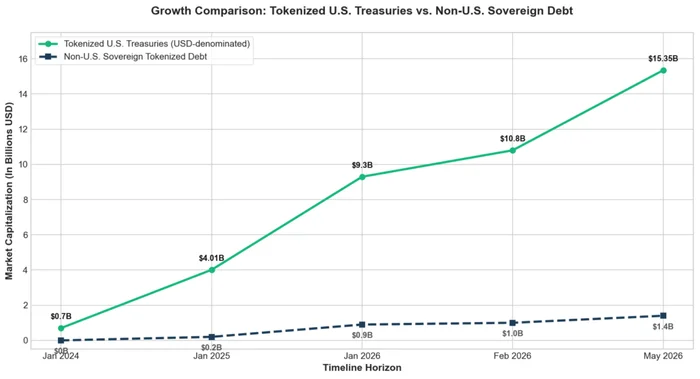

Tokenized US Treasuries hit a record $15.3 billion in May 2026. Total stablecoin market cap is now past $320 billion. The more interesting thing to watch is where the permissionless layer plugs into the state-sanctioned one, and whether that boundary holds.