It’s All About Infra

In our “Year Ahead for Infrastructure” report, we predicted 2023 would be “the year of infrastructure,” and after the conference week in Paris, it’s clear this has become true, almost too true. Paris was highlighted by EthCC and the Modular Summit, with other infra-focused side events during the week. Common themes throughout were MEV, account abstraction (ERC-4337), intents, zk (both for privacy and scaling), rollups, and shared sequencers. In this report, we want to do something different; we’re not going to dive specifically into those concepts, but instead touch on projects that take advantage of them.

Some of these, while purely infra-focused, open up new capabilities for applications, like Circle’s CCTP. Others are more of a mix of DeFi and infra, with Aori and UniswapX highlighting a growing trend toward more “intent-centric” applications. We also touch on Gnosis Pay, an exciting new product in the payments and “crypto rails” space that will further bridge the gap between TradFi and on-chain self-custody. Lastly, we go over the “Endgame” debate between Vitalik (Ethereum), Anatoly (Solana), and Mustafa (Celestia).

As we look towards 2024, we hope to see the pendulum shift back to applications, as the “lack of infra” to support them is becoming less of a hindrance.

UniswapX

UniswapX reinforces a common theme throughout EthCC, the move to an architecture of off-chain execution and on-chain settlement. In other words, a move towards intent-based systems. UniswapX builds off the off-chain execution architecture CowSwap has had for years and follows 1inch (with Fusion) as existing protocols moving towards this model.

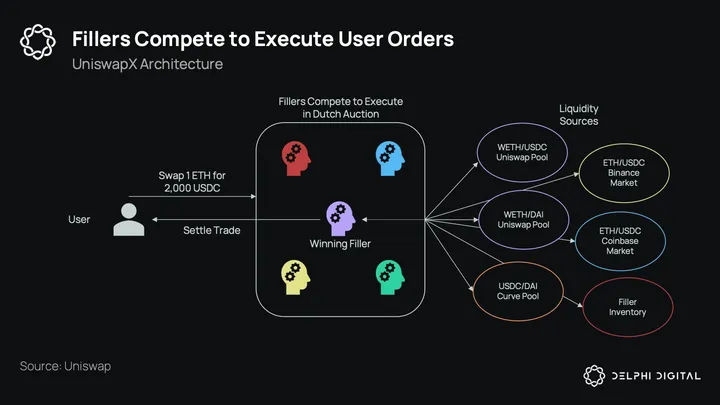

Simply, UniswapX allows users to sign intents (e.g., swap 1 ETH for 2,000 USDC) and then have sophisticated fillers (AKA solvers, market makers, searchers) fill their order off-chain and settle them on-chain. This is a substantially different model from the Uniswap AMM, where users sign execution paths to swap through on-chain AMM pools. With UniswapX, users don’t go through AMMs, at least not themselves. Their orders are routed directly to fillers that utilize both on-chain (AMMs) and off-chain (CEXs, EOF) methods which compete to execute their trade in a Dutch auction.

For users, they don’t have to worry about being sandwiched or front-run, as a filler cannot fill at a price below their limit. The Dutch auction mechanism is similar to 1inch Fusion where fillers can execute at a higher price which declines to the user’s low limit over time. Crucially, and most importantly, UniswapX is agnostic to the method of execution the filler uses. They can swap through Uniswap pools, Balancer pools, Curve pools, aggregators, or even use their own inventory while hedging on centralized exchanges. It is entirely possible for a user to come to Uniswap’s front-end and have their order settled using entirely off-chain liquidity from centralized exchanges.

Also included in UniswapX will be an RFQ (request for quote) model with whitelisted quoters (with aims to be permissionless later). Users can receive quotes from these whitelisted entities (professional market makers) that they can accept to get filled on-chain. In both the Dutch auction and RFQ model, no on-chain liquidity is needed to fill an order, which in some aspects makes Uniswap a front-end for centralized exchange liquidity.

So why a move to this model, is it an admission of defeat for AMMs? For liquid pairs, we would argue yes, as AMMs cannot really compete with centralized exchanges here. Price discovery for liquid assets occurs off-chain, which is then arbitraged on-chain. Swappers are likely to receive worse execution through AMMs, as on-chain pools will be arbed before their orders are executed. The rise of research around CeFi-DeFi arbitrage from the likes of Frontier highlights this well. Users going through X will not be front-run or sandwiched on-chain and can expect to get better prices going through a filler. While their execution is centralized, settlement is not, and that’s what we believe users really care about. How many users would be willing to pay for decentralized execution knowing they’ll get a worse price? This is rhetorical.

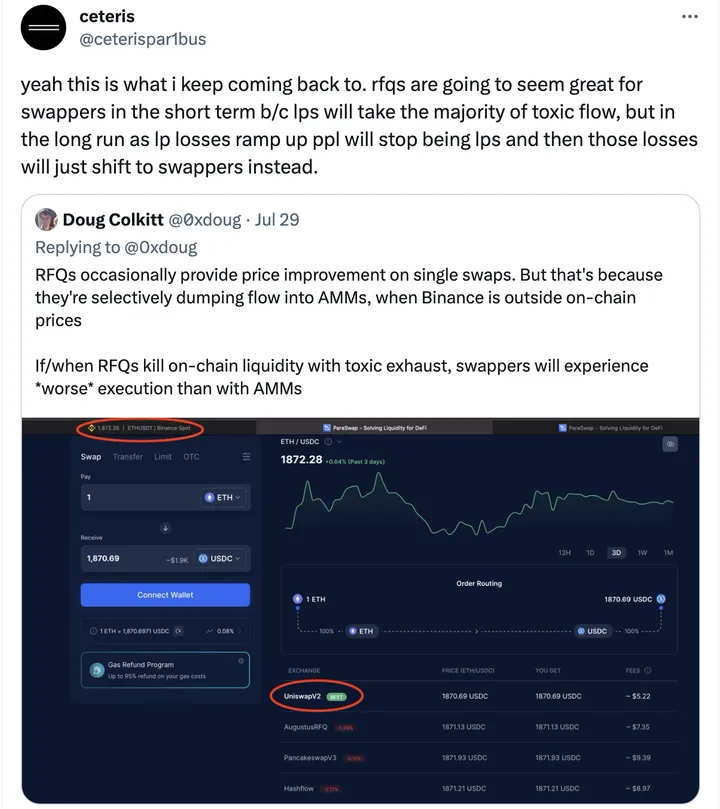

However, it’s no free lunch, as fillers are here to make money. So who’s the biggest loser in this? It clearly seems to be LPs. The shift to an RFQ model will basically turn LPs of liquid AMMs into “toxic exhaust” for the fillers. As swappers’ “non-toxic” flow stops going through AMMs and instead to fillers, toxic flow will start to make up a larger portion of total LP volume. This means less overall trading volume (as they lose the organic flow from users) and mostly being used as a vehicle for fillers to arbitrage. Less volume, more toxic volume, lower fees. The big question is what the long-term implications will be here. Doug Colkitt from Ambient had a thread arguing that RFQs will be worse for users in the long-run, and we think it’s a valid point.

For non-liquid pairs, we still believe AMMs will dominate, but for liquid the trend seems clear. The only real solution to this problem seems to be an on-chain orderbook DEX that can compete with the likes of centralized exchanges, although it is a challenging task; a centralized orderbook will always be faster than a decentralized one. This section is not meant to be a dig at Uniswap, it’s just the reality of trading on-chain today. We expect to see more protocols (especially AMMs) thinking about this and designing alternative solutions (FBAs, JIT liquidity, etc.) as we move forward.

Uniswap Going Cross-Chain

This wasn’t the only announcement around UniswapX though. The other, maybe more exciting angle to UniswapX was the cross-chain swap functionality. While we believe CCTP will disrupt protocol bridges for USDC transfers (we will dive deeper into CCTP later in its section), a similar thing could occur for non-stables with UniswapX. UniswapX will allow users to, for example, swap ETH on Ethereum for AVAX on Avalanche, or MATIC on Polygon. Users will no longer need to go

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments