State of Lending in DeFi

DeFi lending and borrowing protocols have seen a resurgence in activity, with borrowing volume having grown from the low of $3.3 billion in Q1 2023 to $11.5 billion by the end of Q1 2024.

At the same time there is increasing demand for whitelisting more long-tail assets as collateral. However, lending protocols like Aave cannot service this demand as adding new assets increases risks in their multi-asset pools significantly. These protocols thus require various risk management tools such as supply/borrow caps, conservative loan-to-value (LTV), and heavy liquidation penalties to manage these additive risks. Meanwhile, isolated lending pools offer more flexibility in asset selection, but suffer from fragmentation of liquidity and are capital inefficient as rehypothecation is severely limited in such a design.

Since Q4 2023, we’ve seen a resurgence in DeFi lending innovations that largely cater to a wider asset base and allow users to customize their risk exposure. The protocols represent a shift from purely “permissionless” to “modular” lending. These protocols aim to become base layer primitives with their modular architectures highlighting the flexibility and adaptability of these platforms, encouraging innovation in building more end-user-centric products.

The two protocols at the forefront of this shift towards modular lending are Morpho and Euler. In the following report, we explore the design and tradeoffs of these two protocols, their unique features, improvements over legacy lending and the conditions needed for modular lending to take over DeFi money markets.

Morpho

Morpho was originally launched as an Optimizer on top of Compound and Aave and successfully became the 3rd largest lending platform on Ethereum with over $1 billion in deposits. Morpho Optimizer enhanced the efficiency of the interest rate model by directly matching borrowers and lenders. Peer-to-peer matching improves the interest rates for both parties as compared to the underlying pool rates as the utilisation of funds reaches 100% with none of the spread being captured by Morpho protocol. However, Morpho’s growth was fundamentally limited by the design of these underlying lending pools.

The Morpho team subsequently decided to tackle the broader limitations of DeFi money markets and built a new solution to address some of the prominent issues. This resulted in the development of Morpho Blue. It is a base layer protocol that allows high flexibility and modularity in the creation of lending markets. However, the high complexity generated as a result of this high flexibility needs to be abstracted away from the end user to compete with passive lending protocols. Morpho Blue needs to be complemented by abstraction layers on top of the primitive Blue markets, allowing for a more accessible DeFi ecosystem.

Modular lending is the combination of a base layer primitive with high flexibility in market creation and abstraction layers to handle the complexities to improve usability for a wide range of user personas. Morpho’s solution to develop Modular lending markets consists of 2 separate offerings – Morpho Blue and Meta Morpho.

Morpho Blue

Morpho Blue is the primitive protocol for the creation of permissionless isolated lending markets. An Isolated lending pool refers to a lending market between just 2 assets – one collateral and one borrowable asset with independent risk management. The Morpho Blue protocol simplifies the setup of isolated markets and requires users to just select:

- A loan asset

- A collateral asset

- Oracle

- Liquidation Loan-To-Value (LLTV) or Max LTV

- Interest rate model (IRM)

This contrasts with existing lending platforms (e.g. Aave, Compound) that require governance approval for asset listing, parameter changes and assets to be pooled into a single lending pool thus sharing risk across the protocol. In Morpho Blue, each parameter mentioned above is selected at market creation and the parameter persists in perpetuity and is immutable. The LLTV and interest rate model have to be selected from a limited set of options approved by Morpho Governance. Once a market is created, users can interact with certainty that these parameters for the market won’t change as long as Ethereum exists. Here we will break down all of the features of Morpho Blue in detail.

Liquidation Mechanism

Just like other lending protocols, when the Loan-To-Value (LTV) for an account on a Blue market exceeds the pre-determined Liquidation Loan-To-Value (LLTV), the account’s position can be partially or completely liquidated. However, on Morpho Blue, the LLTV selected during market creation is limited to governance-approved LLTV options.

The LLTV whitelisting is done at the protocol level through governance as extremely high LLTV can lead to bad debt in times of high volatility causing losses for lenders of those markets. Similarly, extremely low LLTV values are prohibitive for borrowers to participate and can lead to a high frequency of liquidations.

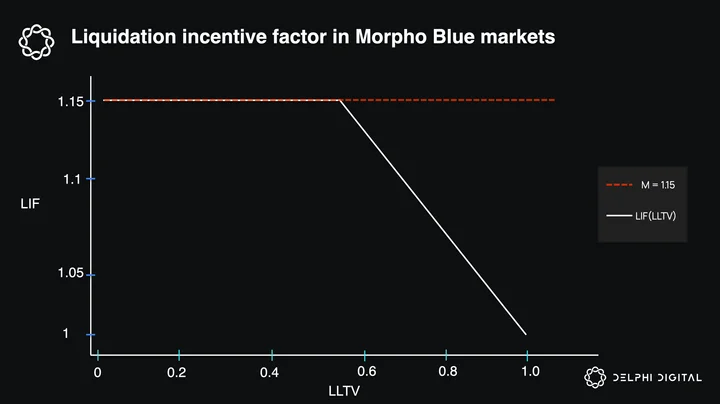

Anyone can perform this liquidation by repaying the account’s debt in exchange for the equivalent amount in the market’s collateral asset, along with an additional incentive. The additional incentive called the Liquidation incentive factor (LIF) is calculated as a function of the markets’ LLTV (where β = 0.3 & M = 1.15)

LIF = min (M, 1/( β * LLTV + 1 – β) )

An important improvement introduced in the Morpho liquidation mechanism is their bad debt management. The liquidation mechanism socializes the losses proportionally among all the lenders in the pool. This immediate loss realization for the lenders instead of the pool accruing bad debt helps avoid the risk of liquidity runs that have affected other lending pools in the past.

Oracle Agnostic

Enacting the aforementioned liquidations and determining the maximum borrowing capacity of a user requir

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments