MetaDAO has surged in popularity on the back of a horrid backdrop for token markets. Built-in token holder rights, control over the treasury, the lack of instant gratification for the team, and fair launch optics are working in MetaDAO’s favor.

On the flipside, “VC coins” have largely pursued similar playbooks (CEX listings, inflated valuations, no follow through on value accrual) that have resulted in significant value destruction for believers who invested at or around TGE.

But MetaDAO isn’t perfect. It has its kinks, and it still suffers from the broader issue of mercenary capital in crypto. The reality of ICOs is that they are still prone to adverse selection. Startups don’t want to be at the beck and call of a large group of stakeholders from day one.

High quality teams with strong networks and genuine product vision can raise venture capital, which gives them significantly more flexibility to make quick decisions and granularly control outcomes.

This isn’t to say projects that fundraised on MetaDAO couldn’t raise venture funding. Some of them definitely intentionally pursued a fair launch and community first optics. However, as the industry grows and the platform scales, investors need to be cognizant of the wide array of risks they are underwriting.

It’s easy to say you can stomach volatility for the chance to get in on the ground floor. It’s much tougher to follow through.

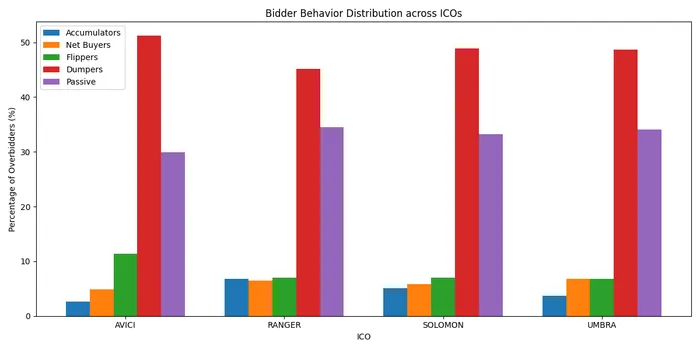

Bucketing ICO participant behavior helps us understand how people actually acted around these events. I used 5 different participant archetypes to attempt to categorize behavior:

- Flippers: Bought and sold the coin around the launch

- Accumulators: Received an ICO allocation, bought liquid tokens with a portion of their refund

- Dumpers: Sold their ICO tokens immediately after launch

- Net Buyers: Created net buy pressure via ICO and AMM, but did sell some tokens overall

- Passive: Didn’t sell ICO tokens, didn’t use the refund either

The single largest group are dumpers; close to 50% of each of the 4 tracked ICOs. Surprise surprise. Classic crypto mercenary capital that saw the ICO as an opportunity to get a quick ROI and leave. These participants very obviously never saw this as more than a lucrative short-term opportunity.

Note: Most MetaDAO raises had associated markets on Polymarket that attempted to predict how much would be raised. It’s very reasonable to assume that there was interplay between large depositors plowing cash into the ICO deposit contracts and PM traders gaming the outcome on Polymarket.

Passives are the second largest group accounting for 30-40% of total participants. This group definitely saw a longer-term opportunity, but wasn’t keen to increase their position size with their refunded USDC.

Flippers on average are the third largest participant cohort, with net buyers and accumulators being the lowest.

None of this should really surprise you. Capital in crypto is always seeking mercenary, short-term opportunities. Industry-wide, this behavior is the leading cause of token market cap deterioration.

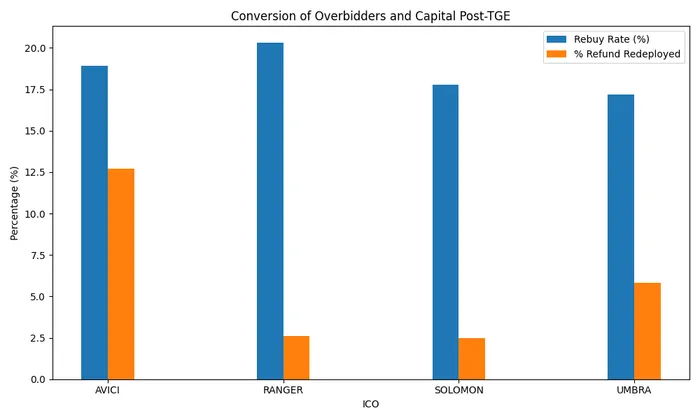

It’s abundantly clear that total committed to MetaDAO ICOs != true interest in buying the coins. Rebuy rates from ICO participants with refund proceeds is between 16-20% for the 4 tracked ICOs. 2.5% to 12.5% (Avici as the outlier) was the range for the percentage of the refund redeployed by liquid buyers.

Success for MetaDAO, in my opinion, is cutting the number of dumpers as a % of participant composition by half – to about 20-25%. Ideally, you would want to see accumulators and net buyers grow. Realistically, another element of success would just be seeing people move from the dumper category to passive i.e. they just hold their original allocation.

But how can MetaDAO actually achieve this?

MetaDAO has been extremely successful in raising capital for projects that choose to fundraise on the platform. It’s the kind of capital they attract that needs to change though. And this is an ongoing issue with every ICO.

On the one hand, if you try to add more constraints to participants (lockups, refunds deployed to LP, etc) you could end up seriously impacting the total amount of capital that gets committed. On the whole, that is a bad thing.

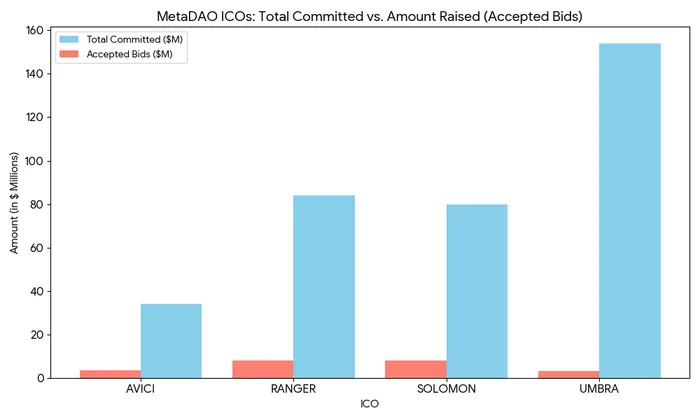

But when you consider total commits against accepted bids, it doesn’t seem all that bad.

The key thing here is that commits are not a true representation of appetite. Commits were people gaming the pro-rated refund process to try and secure a larger piece of the tokens on sale. If Umbra actually raised the full $150 mn, there would be a lot of pissed off participants.

So maybe going the route of more constraints actually plays to MetaDAO’s favor. The only problem is that the pool of long-term aligned capital in crypto is massively overshadowed by the “hot ball of money” that moves from play to play in short periods. However, if MetaDAO wants to be a launchpad for genuine projects with product vision, shrinking the available capital pool to better represent real investors is not the worst thing.

What are some potential mechanisms to deploy here?

- Prophet spoke of an idea where refunds are directed to the token’s LP post-TGE rather than getting directly credited to participants. This is a cool idea in the pursuit of less mercenary participants. It adds a layer of friction that would objectively turn off a lot of pure speculators.

- Lockups are probably not the best idea. They just delay the inevitable. The problem to solve is for getting more long-term aligned capital, not to “punish” people who participate in the ICO.

- More native research and digital road shows. It’s tough to back early stage teams without deep due diligence. Venture investors get access to virtually all of the materials, ideas, and financial projections for startups they prospect. For MetaDAO to be on par with venture markets in attracting long-term capital, help investors build conviction in the product and roadmap via more awareness.