A Deep Dive on Galaxy Digital's Flagship AI Mining Center Helios

JUN 11, 2025 • 32 Min Read

Note: Market pricing data as of 5/14/25 close; all dollar references herein refer to USD

Executive Summary

Galaxy Digital (“Galaxy” or the “Company”) is a digital asset and AI infrastructure focused holding company. Similar in structure to Berkshire Hathaway,

Galaxy has a book of liquid (i.e. BTC) assets in addition to a portfolio of operating businesses. The digital asset oriented operating businesses include:

- Financial services: Traditional investment banking (i.e. M&A and capital raising advisory), lending, sales and OTC trading, and asset mgmt.

- Staking as a service: Allows asset holders to easily earn rewards from staking their assets to secure the corresponding blockchain

Despite Galaxy’s original emphasis on providing financial services for digital asset related businesses and investors, the crown-jewel of its operating company portfolio is Helios, its flagship data center campus in West Texas. As management openly admits, Galaxy stumbled upon Helios by virtue of good luck. In late 2022, Galaxy purchased Helios for $65MM intending to use the data center for Bitcoin mining. Its former owner Argo Blockchain (a Bitcoin miner) was in desperate need of capital and sold the facility to help stave off bankruptcy. Galaxy subsequently agreed to host Argo’s Bitcoin mining infrastructure at Helios (akin to a sale leaseback transaction), while also purchasing its own mining equipment for use at the site.

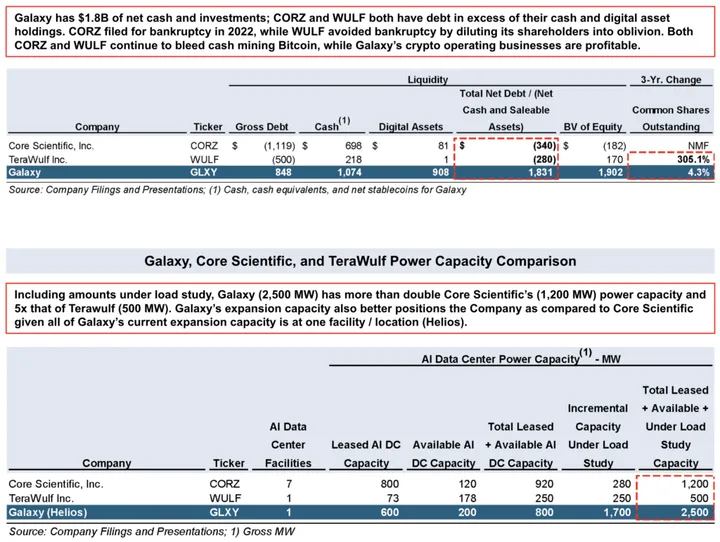

In November 2024, Galaxy announced it had ended its arrangement to host Argo’s Bitcoin mining rigs at Helios and sell its own mining equipment, clearing the physical data center of all Bitcoin mining related infrastructure. Rather than use Helios for Bitcoin mining, Galaxy will host third-party GPUs utilized in AI model training and inference. This business model (owning and operating data centers for use by tenants who bring their own chips and servers) mirrors that of traditional data center REITs (Digital Realty Trust, DLR and Equinix, EQIX). The heightened demand for data center capacity resulting from the proliferation of AI since the launch of ChatGPT in late 2022 has created a significant value creation opportunity at Helios. Helios’s key asset is its 800MW(3) approved power contract with the Texas utility operator, ERCOT. Power is the constraining resource for data center development – Helios’s access to immediate power allows Hyperscaler tenants to bypass the lengthy power approval process (36+ months) in a greenfield development, such to get their AI models up and running as soon as possible. In addition to 800MW of currently approved power, Galaxy has an additional 1.7GW of capacity (for a total of 2.5GW) under various stages of load study at Helios. 800MW of the 1.7GW under load study is expected to be approved in the coming months. By comparison, Digital Realty (DLR; ~$75B enterprise value) has 2.76GW of capacity spread across 308 data centers worldwide (the average DLR data centers is <10MW) – Helios is truly massive.

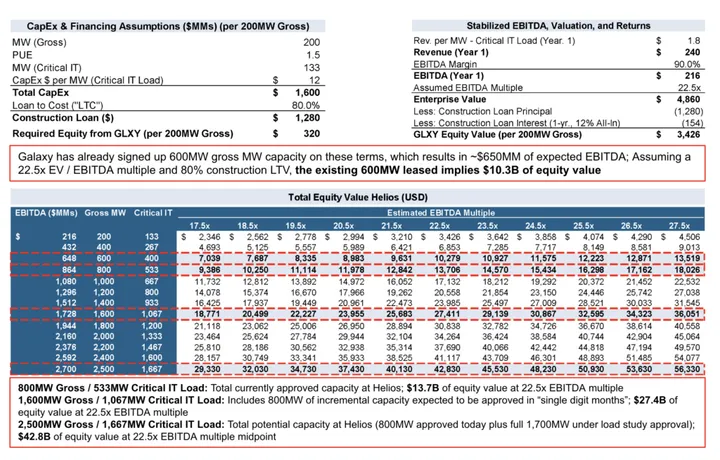

To date, Galaxy has executed agreements to lease ~600MW (3) of its 800MW of currently approved capacity at Helios to a single tenant, CoreWeave. Galaxy’s lease with CoreWeave will commence in phases beginning in early 2026 as the retrofit of the facility to support CoreWeave’s AI infrastructure is completed. CoreWeave will pay $720MM (4) per year (with a 3% annual escalator) in rent to Galaxy plus all related property expenses (triple net lease structure), resulting in a 90% EBITDA margin for Galaxy ($650MM of EBITDA). Galaxy expects to announce the execution of project-level debt financing (i.e. construction loan) in the coming weeks given the significant CapEx required in retrofitting and expanding the Helios campus.

Galaxy’s shares should re-rate as the Company continues to execute on transforming Helios into an AI data center platform. Galaxy’s executed lease (~600MW (3)) with CoreWeave represents less than 25% of the total potential power capacity at Helios (2,500MW). We expect Galaxy to execute leases for the 1,000MW(5) of additional expected available power at Helios within the next year, which would result in 1,600MW (3) of capacity on lease, and $1.7B of EBITDA(6). We believe shares are significantly undervalued, as $1.7B of EBITDA represents our view of the floor amount of EBITDA to be contracted by FYE 2026. Traditional data center REITs’ valuations at 25x EBITDA imply ~$43B of enterprise value at $1.7B of EBITDA, and ~$32B of equity value (reflecting the ~$11B of debt incurred to finance build-out) for Helios. Galaxy has clear visibility into scaling significantly beyond this amount, given Helios’s total potential capacity of 2,500MW and the Company’s intention to acquire and develop additional data center sites. Finally, Galaxy is uplisting from the Toronto Stock Exchange to the NASDAQ tomorrow (May 16, 2025), which serves as another positive catalyst for its shares.

Glossary of Defined Terms

- Critical IT Load: Amount of data center capacity specifically supporting a tenant; excludes power used for backup power capacity and supporting infrastructure

- Gross IT Capacity: Total amount of electrical power a data center has available, including amounts for backup power capacity and supporting infrastructure

- Load Study: Analysis conducted to measure, evaluate, and analyze current and future electrical demand trends to ensure that data center facilities and utility grids have appropriate reliability to meet power needs

- MW: Standard unit of measurement within the power and data center industry; data center capacity is measured in megawatts as a benchmark for the maximum amount of electrical power the facility can deliver to its tenants

- PUE (Power Usage Effectiveness): Gross IT Capacity divided by Critical IT Load; Higher PUE indicates more energy is consumed by non-critical IT loads such as backup power capacity and supporting infrastructure

- Neocloud: New category of cloud service provider specifically designed to provide AI and high-performance, GPU-based computing infrastructure

- Traditional Hyperscaler: Category of the largest cloud service providers including AWS (Amazon), Azure (Microsoft), GCP (Google), and Oracle (OCI). In addition, Meta is considered a Hyperscaler (though they do not provide cloud computing services) given the nature of their massive self- owned and leased data center footprint.

- CoreWeave bills itself as the “AI Hyperscaler” which reflects the fact it is the largest cloud provider focused solely on AI workloads and has $4B+ of annual run-rate revenue

- Triple Net Lease: Lease agreement in which the tenant is responsible for paying all of the property’s operating expenses in addition to base rent, including real estate taxes, building insurance, and maintenance and repair costs

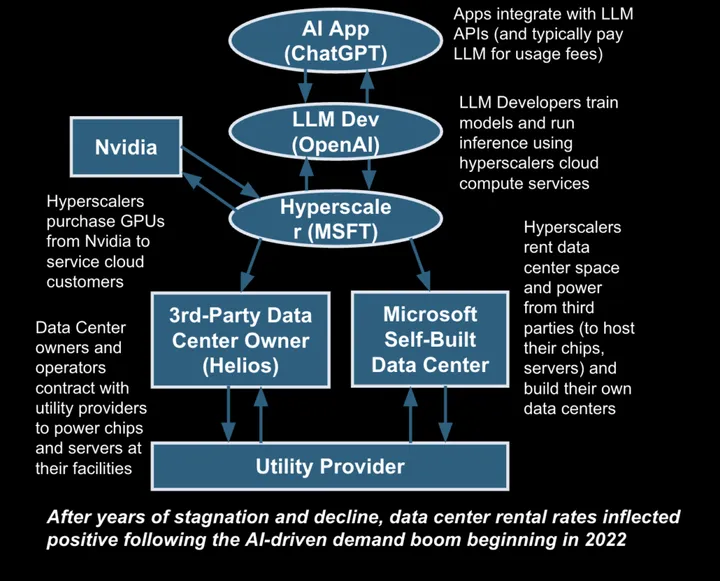

The Value of Power Contracts

The release of ChatGPT by OpenAI in late 2022 spawned an arms race between the major AI Large Language Model (“LLM”) developers, namely OpenAI, Microsoft, Google, Meta, and Anthropic. As AI represents a fundamental shift in computing, these large technology companies are pouring hundreds of billions of dollars annually into the infrastructure required to train and use LLMs. The TAM from AI products and services is likely in the trillions, incentivizing this investment.

The Hyperscalers (Amazon, Microsoft, Google, Meta, Oracle, and CoreWeave) are public cloud service providers and megacap internet companies who provide cloud computing services for external clients and for use in-house. For example, Microsoft’s Azure provides OpenAI with compute capacity for OpenAI’s models, while also powering Microsoft’s own Copilot AI applications. The hyperscalers both construct their own data centers with in-house development teams as well as lease data center space from third-party providers.

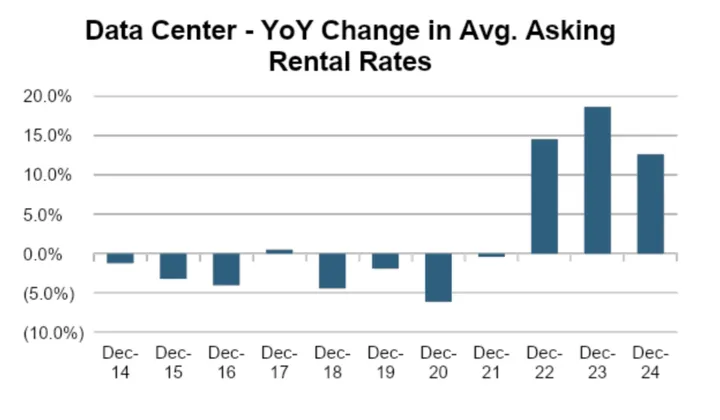

The most significant constraint facing hyperscalers is access to power. Compared to traditional CPU-based computing, AI requires immense computational power. Electricity demand was largely stagnant in the decades leading up to ChatGPT’s release. Structural economic shifts (i.e. the shift away from heavy machinery and manufacturing, and towards a service-based economy) and the adoption of energy efficient technologies resulted in minimal growth in electricity demand from 2007-2022. As such, utilities were unprepared for the recent, AI-driven surge in demand and are struggling to bring new capacity online and satisfy demand. Data centers with existing power contracts now possess a gatekeeping item for hyperscalers in the AI arms race, and obtaining a new grid connection approval for a greenfield development can take 36+ months.

-

“There just is not enough power in the world right now”

– Andy Jassy, CEO of Amazon, Bloomberg 2/27/2025

-

“We have been short power and space”

– Amy Hood, CFO of Microsoft, Earnings Call 1/29/2025

Microsoft is so desperate that they recently announced a deal with Constellation Energy to reopen Three Mile Island. The nuclear power plant, located in Harrisburg, PA, is best known for the 1979 incident considered the worst nuclear power accident in American.

Helios Overview – How Galaxy Can Fill Power Supply Demand Gap

Helios’s characteristics render it ideal for AI use-cases, allowing Galaxy to fill the hyperscale demand gap:

- Massive Scale at a Single Location: Helios’s existing 800MW approved power contract implies a >2% share of all existing US Data Center Capacity(7), at a single location. As previously mentioned, Digital Realty ($DLR), one of the largest data center businesses in the world with an enterprise value of ~$75B, owns 300+ data centers with an avg. of <10MW per location.

- AI Developers and hyperscalers prefer large, centralized facilities (as opposed to smaller, geographically dispersed data centers) given:

- Economic benefits: Economies of scale (i.e. cheaper per unit power sourcing), elimination of egress (data transfer) costs, improved GPU utilization, and elimination of duplicative (i.e. security costs) costs

- Performance benefits: High-bandwidth, low latency connections possible within a single data center reduce model training times; centralization affords simpler model synchronization and improved model consistency

- Resource management: Easier monitoring and management of GPUs, concentration of headcount such as expensive hardware and software engineers facilitates faster problem resolution

-

Meta’s recent announcement on its planned $10B+, 2GW+ data center in northeast Louisiana (its largest to date) further validates the view that hyperscalers prefer large, centralized data centers

- AI Developers and hyperscalers prefer large, centralized facilities (as opposed to smaller, geographically dispersed data centers) given:

- Expansion Potential: Hyperscalers value locations with embedded expansion capacity, as this allows them to scale their cloud service infrastructure in response to underlying end-customer demand signals (as opposed to overcommitting in advance). Helios’s potential capacity of 2.5GW reflects:

-

- 800MW approved interconnection capacity

- 1.7GW of capacity under load study – mgmt. anticipates “800MW of additional approval in the single digit months” (As of May 13, 2025)

- Staggered Development: Galaxy is scheduled to deliver 200MW(3) of capacity to CoreWeave in H1-26 (Phase I), followed by 400MW(3) in 2027 (Phase II). This staggered build-out is optimal, as it allows Galaxy to incorporate the “latest and greatest” electrical infrastructure, cooling solutions, and other design specifications with each tranche of capacity delivered. Nvidia’s requirements as to how to maximize efficiency of their GPUs are ever-changing, as each iteration of chips represents a significant improvement in performance. For example, the latest generation of Nvidia GPUs (Blackwell) consume an inordinate amount of power which far exceeds what traditional air-cooling systems can reliably support. As such, it is beneficial to both Galaxy and future tenants that capacity is brought online in this staggered fashion, which ensures each incremental tranche incorporates the most modern infrastructure.

- Location: Helios’s location in Dickens County, Texas is optimal for AI and hyperscaler tenants due to the following:

- Cheap Energy: Helios is located next to the Cottonwood switching station (one of the largest electrical switches in Texas), which provides for an enormous amount of reliable power

- Proximity to Dallas: Helios is ~250 miles from the Dallas / Fort Worth (“DFW”) metro, the fourth largest metropolitan area in the U.S. Galaxy is constructing long-haul fiber to ensure a 10-15 millisecond travel path to DFW, such that Helios can service AI inference loads which require proximity to large population centers. While hyperscalers have sought out data center capacity in remote areas (i.e. Nebraska, Wisconsin) given major data center hubs such as Northern Virginia are “sold out” on power, these data centers are solely utilized for LLM training. While demand for LLM training capacity should remain robust in the next decade, the ability for data centers to service actual AI application usage, or inference, is a key determinant of a data centers’ longer-term value.

- Texas’s energy regulators are generally considered pro-business and anti-regulation, which has enabled its rapid growth in generation capacity.

- West Texas is rapidly emerging as a data center hub given its abundant land and access to renewable energy resources including solar and wind farms. As incremental data centers are built out in the region, network effects emerge. The existing data centers become more valuable as AI developers, hyperscalers, and enterprises seek out computing resources nearby (due the advantages afforded by lower distances between chips and servers and demand for interconnection between companies).

- Fresh Water Pond: The approximately 10 million gallons of fresh water onsite helps facilitate liquid cooling, which is essentially required for the latest generation of Nvidia GPUs (Blackwell).

Galaxy is the Best Way to Play The BTC Mining to AI Pivot

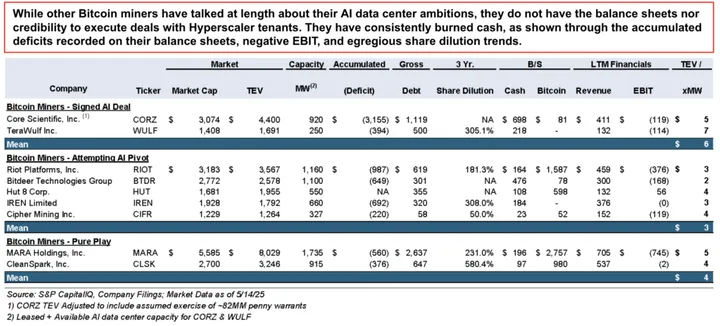

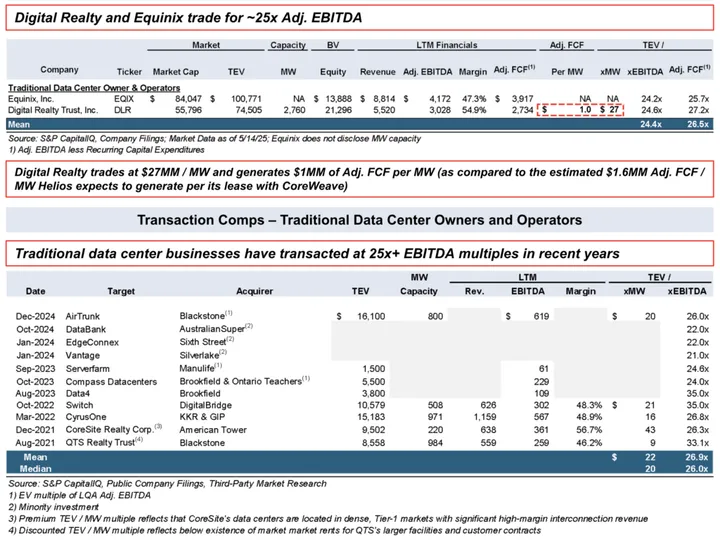

Given the significant valuation premiums associated with traditional data center platforms (25x+ EBITDA and $27MM/MW; see pg. 14) over Bitcoin miners (~$3MM-$5MM/MW EBITDA; see following pg.), many Bitcoin miners are also attempting to pivot towards leasing their data center space and power to AI and Hyperscaler tenants. These Bitcoin miners can be categorized as follows:

- AI Pivot, with signed deals: Core Scientific – CORZ and TeraWulf – WULF

- AI Ambitions, but no signed deals: IREN – IREN, Hut 8 – HUT, Bitdeer –BTDR, Riot Platforms – RIOT, Cipher Mining – CIFR

It should be noted that there are significant hurdles in retrofitting traditional, CPU-based data centers (i.e. the facilities owned by Digital Realty and Equinix) for AI purposes. Traditional data centers are smaller – Digital Realty’s average data center is <10MW, which is inadequate for LLM training purposes. In addition, website hosting and SaaS applications are much less compute intensive than AI, rendering traditional cooling systems and rack densities incompatible with modern AI design specifications. As such, one could argue all the Bitcoin miners appear undervalued relative to the traditional data center businesses on an EV / MW capacity basis (see following pg.). MW capacity is an appropriate metric to assess valuation given data center leases are priced in terms per MW (i.e. $1.5MM of rent, per year, per MW), and thus MW capacity directly impacts a data center providers’ revenue and earnings potential.

Galaxy is the most attractive way to play the “Bitcoin miner pivoting to AI data center operator” investment thesis given the following:

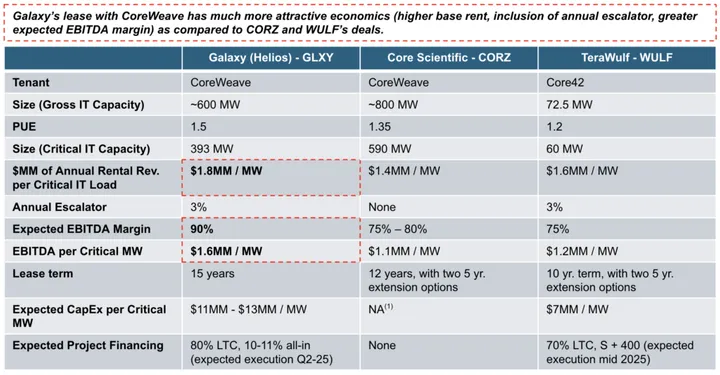

- Most Attractive Signed Deal: Galaxy’s deal is superior to those signed by CORZ and WULF – see pg. 7 for full comparison

- Galaxy’s ability to execute a signed lease agreement is a strong testament to its data center operations’ competency. Other miners have failed to sign deals given concerns over their ability to deliver AI data center capacity in a timely manner –hyperscalers do not believe most other Bitcoin miners have the financial and human capital to rapidly execute upon an extremely complex retrofit project.

-

- Galaxy’s credibility in AI data center development will be significantly improved upon successful execution of Phase I with CoreWeave. Traditional hyperscalers are much more likely to lease data center space and power from Galaxy after validating Galaxy’s ability to deliver on its CoreWeave commitments. Given their size and scale, Traditional Hyperscalers are naturally risk averse – Galaxy’s Phase I execution will demonstrate their AI data center credentials and result in a positive flywheel effect as demand from Traditional Hyperscalers increases.

- Bitcoin miners without signed deals are playing catch-up and facing an uphill battle. Traditional hyperscalers are extremely unlikely to become the first ever tenants for these miners, while Neoclouds will likely prefer to lease space from the players who have established themselves in the data center operations space (i.e. Galaxy, CORZ, and WULF).

- Galaxy’s credibility in AI data center development will be significantly improved upon successful execution of Phase I with CoreWeave. Traditional hyperscalers are much more likely to lease data center space and power from Galaxy after validating Galaxy’s ability to deliver on its CoreWeave commitments. Given their size and scale, Traditional Hyperscalers are naturally risk averse – Galaxy’s Phase I execution will demonstrate their AI data center credentials and result in a positive flywheel effect as demand from Traditional Hyperscalers increases.

- Embedded Expansion Capacity: In addition to the ~600MW (3) to be leased to CoreWeave, Galaxy has 200MW (3) of approved gross IT capacity, and an additional 1.7GW under load study. Galaxy expects approval for an additional 800MW (3) in the coming months. This embedded expansion capacity far exceeds that of the Bitcoin miners who have successfully signed initial AI leasing deals (see pg. 8).

- Balance Sheet Strength: Galaxy’s $1.8B of net cash and investments far exceeds that of any other Bitcoin miner (see 8). Not only does this result in Galaxy possessing the adequate capital to fund the equity portion of its data center retrofit and build-out, but also sends a strong signal to potential hyperscaler tenants that Galaxy has the financial resources to deliver.

- Elimination of Ongoing Bitcoin Mining Operations: Galaxy has completely exited all Bitcoin mining activities to focus solely on its AI data center ambitions, which sends a positive signal to potential Hyperscaler tenants about Galaxy’s focus going forward.

-

Bitcoin mining is a very bad business. It’s extremely cyclical, capital intensive (requiring spend on data center build outs and mining equipment), and all else equal, your revenues decline by 50% every 4 years with each Bitcoin halving.

- It is economically irrational for a miner to engage in Bitcoin mining if they are capable of pivoting to AI data center leasing. The traditional data center model involves no ongoing CapEx to buy mining servers and equipment. It is unsurprising that miners have been cash- incinerating, value-destructive companies that seemingly dilute shareholders to no end. While other miners intend to do both Bitcoin mining and AI data center leasing, Galaxy’s sole focus on the latter is a significant positive.

- Cipher Mining’s CEO hit the nail on the head when discussing the challenges they face attempting to enter the AI data center space as a Bitcoin miner – “It’s not lost on us that if we’re talking to a counterparty with a $1 trillion market cap.. One of the drawbacks of the Bitcoin

-

- Mgmt. team: Mike Novogratz (CEO and Founder) spent decades on Wall St. before founding Galaxy, making partner at Goldman Sachs in 1998 and helping lead Fortress through its IPO in 2007. Chris Ferraro (President and Chief Investment Officer) was a Managing Director at HPS, a leading private credit fund, prior to joining Galaxy.

- Unlike the Bitcoin miner executive teams, Galaxy has created significant shareholder value, growing BV per share from ~$1 in 2018 to ~$6+ as of May 2025(2). Galaxy is the only crypto-related public company to return significant capital shareholders via buybacks. Bitcoin Miners have engaged in relentless dilution to fund the ongoing cash burn of their unprofitable operations.

- Galaxy benefits strongly from the fact its Bitcoin mining operations were never a material part of its operating business.

- Mgmt. is extremely aligned with shareholders given Novogratz is the majority shareholder of Galaxy, owning ~60% of the Company for a ~$5B stake.

- Ferraro’s experience at HPS is highly valuable in building Galaxy’s data center platform. HPS, which was recently announced to be acquired by BlackRock, is known for its ability to execute highly complex financing transactions. The types of deals HPS engages in involve coordination and negotiation across a variety of counterparties (i.e. credit and equity underwriting, legal, tax), which mirrors the work involved in building and leasing data center capacity.

- Novogratz’s honesty about Helios is extremely refreshing. He has repeated numerously that Galaxy was lucky to have acquired Helios right before the AI boom began. Other Bitcoin miner CEOs have attempted to re-write history, and posture as if they had always been building broader data center and digital infrastructure businesses. In reality, these miners had zero intentions to do anything besides mine Bitcoin until ChatGPT was launched.

- Unlike the Bitcoin miner executive teams, Galaxy has created significant shareholder value, growing BV per share from ~$1 in 2018 to ~$6+ as of May 2025(2). Galaxy is the only crypto-related public company to return significant capital shareholders via buybacks. Bitcoin Miners have engaged in relentless dilution to fund the ongoing cash burn of their unprofitable operations.

Galaxy, Core Scientific, and TeraWulf AI Data Center Lease Deal

Galaxy, Core Scientific, and TeraWulf Balance Sheet

CoreWeave Tenant Credit Risk Fears Are Overblown

Galaxy’s valuation ($3.8MM / MW (8)) reflects a sharp discount to the traditional data center operators ($27MM / MW, and ~25x EBITDA). This discount can be partly explained by doubts around CoreWeave’s creditworthiness, given CoreWeave does not have an investment grade credit rating unlike the Traditional Hyperscalers. In short, market participants are ascribing some probability that CoreWeave defaults on its rental obligations to Galaxy.

CoreWeave is a cloud services provider focused solely on artificial intelligence and GPU compute services (a “Neocloud”). As opposed to the Traditional Hyperscaler businesses of AWS, Azure, and Google, which predominantly offer CPU-based computing services, CoreWeave only supplies GPU infrastructure. CoreWeave initially focused on Ethereum mining, running Nvidia GPUs in data centers in exchange for ETH mining rewards.

CoreWeave’s experience operating Nvidia GPUs at scale to mine ETH inadvertently positioned the company perfectly for the subsequent AI-driven explosion in GPU-based computing services. In 2019, CoreWeave began utilizing their GPU fleet to provide AI companies GPU-based cloud computing services.

CoreWeave’s finances came into public view ahead of its March 2025 IPO, with the investment media highly focused on its debt. CoreWeave was also unfortunate in that it listed shortly after the DeepSeek model release in early 2025, which resulted in a sharp pull-back in all AI-related public company valuations. As such, the size of CoreWeave’s IPO was downsized (from $2.7B to $1.5B) and completed at a lower valuation ($23B) than originally desired ($32B).

Fears around CoreWeave’s ability to meet its rental payment obligations to Galaxy are extremely overblown. More specifically:

- CoreWeave’s debt ($8B as of FY24A) reflects the high degree of revenue visibility inherent to its business model. 96% (FY24A) of CoreWeave’s revenue is derived via long-term (4-year weighted avg. length), committed contracts.

-

- $5.8B of CoreWeave’s outstanding debt consists of Delayed Draw Term Loans (“DDTL”). CoreWeave only incurs debt under its DDTL facilities upon signing of a customer contract – debt is drawn to purchase the infrastructure (i.e. GPUs) to service the corresponding customer contract. These DDTL facilities are explicitly enabling Growth CapEx, which is not speculative in nature.

- It is completely rational for CoreWeave to use debt to finance its growth, especially as CoreWeave continues to drive down its debt cost of capital. As of May 2025, CoreWeave was in market for a high-yield bond issuance expected to price below its existing debt facilities.

- Blackstone led CoreWeave’s $7.6MM DDTL 2.0 facility financing in May 2024, which was their largest ever private credit investment. Financial modeling of debt and cash flows is a core competency of any private equity investor. While some criticisms of private equity are fair, CoreWeave bears citing its high debt load are implicitly questioning the thoughtfulness of Blackstone’s credit underwriting and financial modeling. Given the financial and reputational stakes associated with such a large deal, I would be highly surprised if CoreWeave became a troubled credit for Blackstone.

- $5.8B of CoreWeave’s outstanding debt consists of Delayed Draw Term Loans (“DDTL”). CoreWeave only incurs debt under its DDTL facilities upon signing of a customer contract – debt is drawn to purchase the infrastructure (i.e. GPUs) to service the corresponding customer contract. These DDTL facilities are explicitly enabling Growth CapEx, which is not speculative in nature.

-

- CoreWeave’s moat is highly durable.

- CoreWeave’s close relationship with Nvidia (Nvidia purchased $250MM of CoreWeave stock in its IPO and had previously invested $10MM in its private fundraising rounds; Nvidia also purchases compute capacity from CoreWeave for its internal AI activities) is a strategic and competitive advantage. CoreWeave’s priority access to the latest generation of Nvidia GPUs allows CoreWeave to lock in longer term contracts from favorable customers.

- Competitor Neoclouds, such as Nebius and Crusoe, do not have the same level of access as CoreWeave, and thus typically offer short term rentals. A short-term collapse in GPU rental rates would actually benefit CoreWeave, as CoreWeave is insulated from short-term fluctuations given their long-term fixed contracts. Other Neoclouds would face immediate financial distress as their revenues plummet given they reset with daily rental rates. Many of these Neoclouds would go likely out of business, driving down GPU rental supply and a recovery in rental prices.

- Nvidia’s desire to diversify its customer base away from the Traditional Hyperscalers (AWS, Azure, and Google) and towards CoreWeave is completely logical given the Traditional Hyperscalers are attempting to build chips in-house and reduce their

- CoreWeave’s close relationship with Nvidia (Nvidia purchased $250MM of CoreWeave stock in its IPO and had previously invested $10MM in its private fundraising rounds; Nvidia also purchases compute capacity from CoreWeave for its internal AI activities) is a strategic and competitive advantage. CoreWeave’s priority access to the latest generation of Nvidia GPUs allows CoreWeave to lock in longer term contracts from favorable customers.

- CoreWeave’s moat is highly durable.

- CoreWeave’s moat is highly durable (continued)

- The capital intensity involved in purchasing GPUs at scale prohibits other Neoclouds from competing against CoreWeave for the largest deployments. CoreWeave’s recent win with OpenAI ($11.9B contract through 2030) demonstrates that CoreWeave is the only Neocloud competing up-market against the Traditional Hypescalers.

-

-

- CoreWeave’s ability to tap public markets provides a key competitive advantage against Neoclouds (of whom all but one, Nebius – NBIS, are private) given the capital requirements involved in the GPU cloud computing services industry.

- Independent, third-party research firm SemiAnalysis (widely considered to be the pre-eminent, thought leader on all things digital infrastructure and semi-conductors) ranked CoreWeave as the only “Platinum” GPU Cloud company, its highest tier. Traditional Hyperscalers Amazon, Google, Microsoft, and Oracle were ranked either gold or silver, its second and third tiers. SemiAnalysis states:

- “CoreWeave is clearly leading in providing the best GPU cloud experience.. and are entrusted to manage the large-scale GPU infrastructure for AGI labs like OpenAI and MetaAI, high frequency trading firms like Jane Street, and even Nvidia’s internal clusters. CoreWeave is the expert at running large scale GPU clusters reliably.. and is the only Neocloud capable of operating clusters with 10,000 GPUs consistently and reliably. Besides CoreWeave, the only other GPU clouds able to operate (at this size) reliably are the four hyperscalers: Azure (Microsoft), OCI (Oracle), AWS (Amazon), GCP (Google).”

- An additional economic benefit of CoreWeave’s contracts versus those of smaller Neoclouds is the inclusion of customer prepayments. CoreWeave’s customers prepay 15% – 25% of TCV (“total contract value”) prior to receiving any services. This results in a significant net working capital benefit as its cash receipts from customers far exceed revenue recognized, providing an additional financing advantage and highlighting how customers place significant trust in CoreWeave to deliver on long-term commitments.

- The Traditional Hyperscaler businesses are now widely considered some of the best businesses of all time, despite early criticism from analysts and investors. In 2006, one analyst stated “I have yet to see how these investments (in AWS) are producing any profit. They are probably more of a distraction than anything else.” AWS is now generating $117B+ of annualized revenue, with 39% operating margins, growing 17% YoY!

- Long term, Neocloud economics and margins should converge towards that of the Traditional Hyperscalers given the inherent similarities of the business model. If anything, the Neocloud business could become a higher-margin, less-commoditized industry than traditional cloud computing due to the intricacies and nuances involved with operating more complex GPU infrastructure.

-

- Claims that Nvidia GPUs have a useful life of only 1-2 years are misguided. This bearish narrative states that as Nvidia releases new chips every 1-2 years, the older chips immediately become obsolete. As CoreWeave’s stated payback period on their CapEx is 2.5 years, a 1–2-year useful life for Nvidia GPUs implies CoreWeave is fundamentally unprofitable on a unit economic basis. However:

- OpenAI only in 2024 de-commissioned its Volta v100s, which were released in 2017 (suggesting a 7-year useful life)(9)

- Satya Nadella, CEO of Microsoft, stated “You buy the newest for training, and the older go into inference” (10)

- The hyperscalers depreciate their severs and network equipment assuming a 6-year useful life

- CoreWeave’s customer concentration will naturally decline over time as it continues to grow. While Microsoft represented 62% of CoreWeave’s FY24A revenue, this percentage will decline below 50% going forward given the $11.6B contract CoreWeave signed with OpenAI in March 2025.

- Customer concentration in the early stages of a business can be intentional, and positive. By providing Microsoft with GPU cloud services to help Microsoft support its end-customer base (mainly OpenAI), CoreWeave was able to then win OpenAI as a customer directly

- Galaxy expects to close project-level debt financing “in the coming weeks”. This transaction further validates CoreWeave’s credit worthiness given a key component of the lender’s underwriting is around CoreWeave’s ability to pay rent to Galaxy.

- CoreWeave’s positioning as the only neocloud operating at scale makes it a highly strategic asset. Logical strategic buyers of CoreWeave include Nvidia, Softbank, Amazon, Microsoft, Google, Oracle, and OpenAI.

Demand for AI LLM Training Compute and Data Center

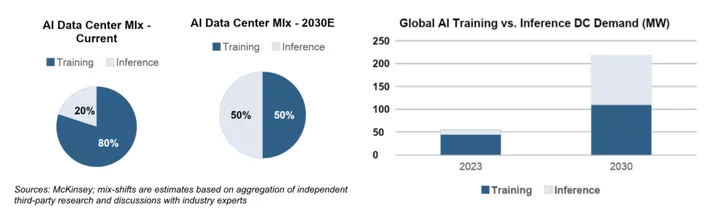

The perceived value of large-scale AI data centers has also come under question due to the misconception that AI LLM training will decline in the coming years. This idea holds that demand for space and power within the massive data centers in remote locations will subside as AI developers shift focus towards application usage, or inference, which requires closer proximity to major metropolitan areas. Proponents argue there are diminishing returns from scaling compute and infrastructure, and that each added increment of scale for LLM training (i.e. employing another 10,000 GPUs) yields smaller performance improvements than the prior. Under this theory, the massive data centers (such as Helios) are less relevant and valuable as their main purpose is hosting LLM training. This view is misguided:

- While the percentage mix of all AI-related compute will shift from training towards inference as AI applications are put into production, the dollar value spent on training will continue to grow. Growth in the overall pie will offset training becoming a smaller piece of that pie. See below.

- Meta’s planned $10B, 2GW+ data center in northeast Louisiana (its largest to date) is widely expected to be used to train Meta’s Llama LLM given it is located outside of the proximity of any major metropolitan area.

- This massive investment exemplifies that the largest AI model developers themselves plan to continue spending massive sums on infrastructure to etch out further performance gains in their models. Per Mark Zuckerberg on Meta’s Q4-2024 earnings call:

- “I continue to think that investing very heavily in CapEx and infra is going to be a strategic advantage over time”

- This massive investment exemplifies that the largest AI model developers themselves plan to continue spending massive sums on infrastructure to etch out further performance gains in their models. Per Mark Zuckerberg on Meta’s Q4-2024 earnings call:

-

Multiple ex-OpenAI executives have gone on to start new AI labs, raising extraordinary sums prior to having a working product, let alone any revenue

- OpenAI co-founder Ilya Sutskever’s company SSI raised $2B at a $32B valuation in March 2025.

- As of April 2025, Ex-OpenAI CTO Mira Murati is reportedly seeking to raise a $2B seed round (!!!) at a $10B valuation for her start up, Thinking Machine Labs

- These staggering sums at astronomical valuations for companies without a penny of revenue highlight that investors will continue to pour money into AI labs training new models. CoreWeave (and thus Galaxy) is extremely well positioned to benefit as startups seek GPU-based cloud infrastructure.

In any event, Helios is capable of servicing AI companies’ inferencing requirements given it is located only ~250 miles from DFW. Galaxy President and CIO Chris Ferraro specifically highlighted that Galaxy purposefully designed its long-haul fiber project to ensure “that we have between 10 and 15 milliseconds travel path back to Dallas, and we have 2 redundant paths that to maintain N+1 connectivity. And that benchmarking was meant to be speed that can service both training and inference loads. And so the idea there was to ensure that even though Helios is in a relatively remote area, that it actually can service and is a good fit for what we think the forward on actual AI load use cases are going to be, so that it’s in play for many years to come.”

Helios Value Creation Opportunity

The value creation opportunity at Helios is enormous; every 200MW gross (133MW Critical IT load assuming 1.5 PUE) leased results in:

- $240MM of revenue ($1.8MM of revenue per MW of critical IT load per CoreWeave lease)

- $216MM of EBITDA (90% EBITDA margin, per mgmt. guidance as lease is structured as Triple Net)

- $4.9MM of enterprise value (assuming 22.5x EBITDA multiple, which represents discount to public and M&A data center comps at ~25x+)

- $3.4B of equity value (assumes 80% LTC construction financing, per mgmt. guidance; 12% rate assumed for purposes of conservatism)

Note: The required equity investment is limited beyond amounts funded for the first 600MW at Helios. At stabilization, the construction loan will be refinanced out with lower cost debt, and refinancing proceeds will exceed the construction loan principal, with excess proceeds “recycled” as equity into new development.

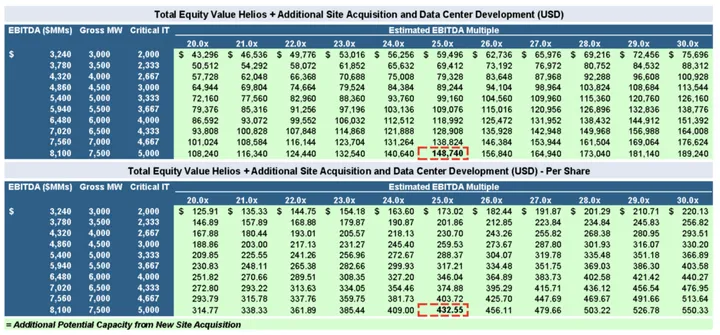

Value Creation Opportunity – Additional Site Acquisition and Development

![]()

Galaxy is actively in the market to acquire and develop additional data center sites beyond its flagship Helios campus. The Company’s pipeline of 40 opportunities has an avg. capacity per site of ~500MW, resulting in 20GW of total pipeline. Per Chris Ferraro on the Q1-2025 earnings call:

- “First and foremost, the most important item on our priority list is executing at Helios with CoreWeave.. (but) given the position we have in the market, we view ourselves as one of only a handful of people who have the right to actually win the space long term. And so building a pipeline of opportunities has been next on our list (as) we will continue to develop Helios in parallel.. Having a platform that is geographically diversified with customer diversity is a long-term goal of ours.”jfe

While management did not explicitly state if the pipeline consists of properties currently used for Bitcoin mining, Galaxy’s ultimate path to success likely resides in purchasing these types of sites given the lower degree of competition encountered in doing so. While competition is fierce for more traditional development opportunities between public REITs (Digital Realty, Equinix, and American Tower) and privately held, PE-backed platforms (Switch, QTS, CyrusOne, Databank), these larger more established players likely have minimal interest in Bitcoin-mining retrofit developments. Galaxy’s main competitors here are Core Scientific, TeraWulf, and the other Bitcoin miners. As previously discussed, these miners simply do not have the financial and human capital to compete effectively versus Galaxy. Sell-side research analysts have alluded towards a massive supply of Bitcoin mining data centers on the market, validating Galaxy’s acquisition pipeline.

Public Trading Comps – Traditional Data Center Owners and Operators

Nasdaq Uplisting Impact

Galaxy initially went public on the Toronto TSX Venture Exchange in August 2018, given its small size ($300MM BV of equity) and Toronto’s venture exchange offering. Mgmt. intended to eventually relist in the US and publicly filed a registration statement on Form S-4 with the U.S. Securities and Exchange Commission (“SEC”) in January 2022. On April 7, 2025, Galaxy announced the effectiveness of the registration statement, with the stock expected to begin trading on the Nasdaq on May 16, 2025. The lengthy ~3-and-a-half-year registration process is attributable to Gary Gensler’s (the SEC Chair from 2021 to 2025 during the Biden administration) overwhelmingly anti-crypto position.

While it is difficult, if not impossible, to accurately quantify the impact of Galaxy’s shares uplisting from the TSX to the Nasdaq, the uplisting should be considerably positive.

- Certain U.S. based investment managers (i.e. long-only mutual funds and ETFs, long/short hedge funds) are unable to currently purchase Galaxy shares due to either (i) fund restrictions on investing in foreign markets or (ii) compliance mandated rules prohibiting investment in stocks below certain volume and liquidity thresholds

- The Nasdaq uplisting naturally increases the universe of potential buyers for Galaxy’s stock

- A Nasdaq listing provides access to the deepest, most liquid capital markets in the world which should result in a lower cost of capital, all else equal.

- Galaxy’s 5-year, $402.5MM Exchangeable Notes were issued in November 2024 at a 37.5% conversion premium and 2.5% interest rate. Roughly a week later, MARA issued $850MM of zero-coupon convertible notes at a 40% conversion premium. Galaxy’s Exchangeable Notes represented a higher all in cost of capital despite its far superior credit profile as compared to MARA, a clear indication of the historical disadvantages posed by its TSX listing. While Galaxy has been consistently profitable since its 2018 listing, growing book value per share from $1.09 in Dec. – 18 to $6+(2), MARA burned over $1B of FCF in 2024 alone against an enterprise value of $5.6B.

- The current lack of bulge bracket (i.e. Goldman, JPM) equity research coverage of Galaxy highlights that the largest banks currently do not believe Galaxy is worth covering as the potential revenues they could earn from market making and capital markets from Galaxy do not outweigh the costs of initiating coverage.

- A Nasdaq listing opens the door for inclusion in U.S. indices, including the S&P 500 and Russell 2000. Coinbase (COIN) closed up roughly 25% on May 13, 2025 upon the announcement of its inclusion in the S&P 500.

- Bill Ackman’s November 8, 2024 tweet about his desire for Universal Music Group to move its primary listing to a U.S. exchange outlines the benefits of a U.S. listing:

- “UMG trades at a large discount to its intrinsic value with limited liquidity in significant part due to it not having its primarily listing on the NYSE or NASDAQ and not being eligible for the S&P500 and other index inclusion.

- “UMG trades at a large discount to its intrinsic value with limited liquidity in significant part due to it not having its primarily listing on the NYSE or NASDAQ and not being eligible for the S&P500 and other index inclusion.

Appendix and Footnotes

- $7.86B market cap ($22.87/share – $BRPHF x 343,865,060 Class and B units) less $1.831B of net cash and investments

- Estimated as of May 12, 2025, per Q1-2025 earnings release on May 13, 2025

- Gross MW Capacity

- For each 200MW of Gross MW Capacity leased to CoreWeave, Galaxy will earn $4.5B of total revenue over a 15-year lease term (which implies $300MM of avg. annual revenue over term of lease). Per Q4-2024 earnings call, first year of revenue (for 200MW Gross) will be $240 million (resulting in $720MM for 600MW Gross), implying rent increases by 3.0% per annum over term of lease

- 200MW of currently approved power capacity plus 800MW expected to be approved “in the single digit months”, per mgmt. on the Q1-2025 earnings call

- Assumes economics are in line with existing CoreWeave lease, which provides for $1.1MM EBITDA per Gross MW and $1.6MM EBITA per Critical IT capacity MW

- U.S. total data center capacity estimated at 33GW via aggregation of various third-party market research reports

- Ascribes zero value to Galaxy’s other operating businesses for conservatism; $6MM TEV divided by 1,600MW of expected approved power by FY26E

- Per Jensen Huang on the BG2 Podcast, released October 13, 2024

- Per Satya Nadella on the BG2 Podcast, released December 12, 2024

Disclaimer

We are investors and are thus naturally biased. As of the time of writing, we have a long position in Galaxy Digital shares and stand to benefit financially if the shares rise in price.

We have a good faith basis for all opinions included within this report.

Like any investor, we intend to maximize potential gains and minimize potential losses on any investment. As such, we may exit or add to our position in Galaxy Digital shares at any time, for any reason. To the extent that we explicitly suggest that Galaxy shares are misvalued, does not mean that we will continue to hold these shares until the Company’s stock price reaches any specific valuation. Our valuations are entirely subjective and constantly subject to change based on a number of factors, including market conditions, our own internal portfolio considerations and risk management, and investor sentiment. Readers should not assume that we will hold our long position for any minimum holding period.

0 Comments