A Post Mortem of Last Week's Flash Crash

DEC 06, 2021 • 5 Min Read

The Great Deleveraging

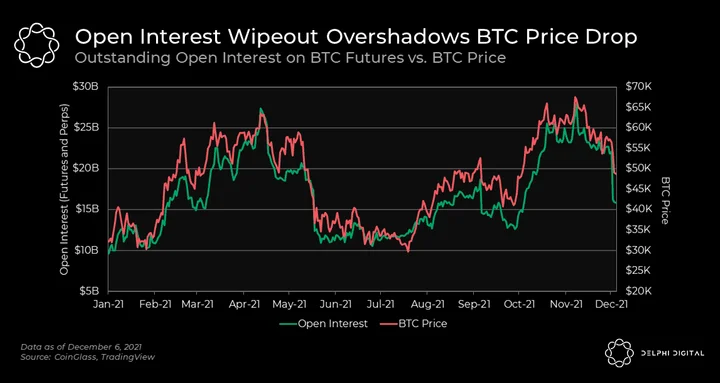

- Leveraged longs took a senseless beating over the last week — and it was perhaps overdue. BTC’s open interest on perps/futures fell from just under $30B in late November to just over $15B today. Sentiment has taken a turn for the worse, and it seems like the market is all but lost. But historically, deep deleveraging events (like this one) pave the path for bullish setups.

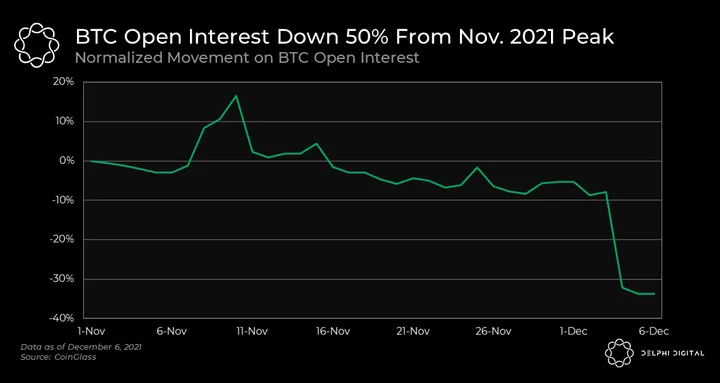

- From the November peak to today, BTC open interest is down a whopping 50% — and this is over the span of just a few weeks. There’s logic behind why open interest and its composition matter. Too many leveraged longs and a lack of spot buying is a sign that a market is peaking. When there’s nobody left to buy/long, price momentum to the upside is severely limited (the same applies to heavy shorting preceding bottoms). Wiping out some of this open interest gives the market a reset.

- 50% is not a small number, despite the fact that all market data in crypto looks whimsical to a portfolio manager at Goldman. While this doesn’t mean we’ve found a bottom with certainty, the probabilities over the mid-term are currently in favor of patient bulls. However, the most likely outcome is a sideways market for the next month or so, at least until the market finds its footing again.

A Short-Lived Liquidity Crisis Emerges

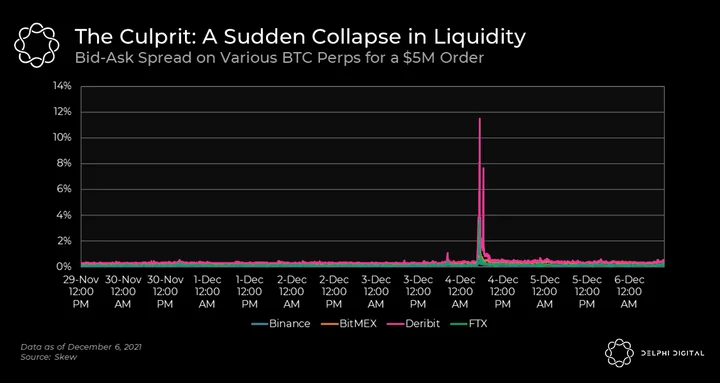

- Well, what really caused prices to fall so quickly? The answer to that is an utter collapse in market microstructure, as well as news surrounding Evergrande’s imminent default and Chinese policymakers reaction to growing economic risks.

- The bid-ask spread for a $5M order in perp markets ranges from 0.1% to 0.5% (on bad days). On this occasion, spreads for a $5M order momentarily rose as high as 2% on Binance, 4.2% on FTX, 4% on BitMEX, and 11% on Deribit.

- For once, this calamity was catalyzed on spot markets, where a few entities market sold a large amount of BTC over a very short time period. In essence, these large sell orders ate through buy walls. And with price cascading, market makers were probably unwilling to provide liquidity until they could figure out what was happening. A few moments later, with BTC bouncing off $42K, normality resumed. Alas, this was a short-lived liquidity crisis that escalated bearish overtones.

Funding Rates Crash From Q4 High

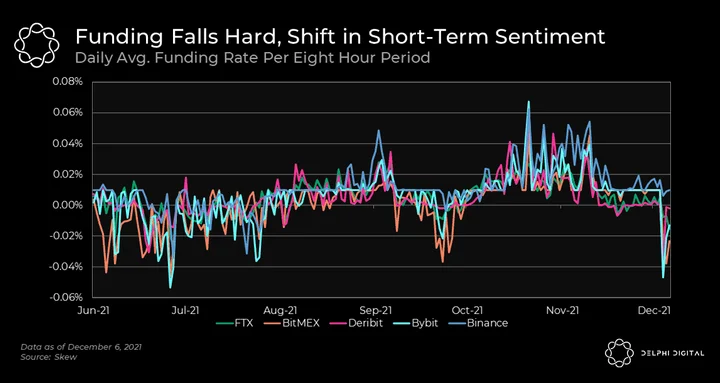

- Most market participants in crypto don’t care if it was liquidity concerns or bad news from China that caused the crash. Funding rates turned negative as levered longs were wiped out, and sentiment has been understandably poor since. The crypto market (and all markets, really) are sensitive to behavioral factors, so a mid-term collapse in sentiment would not be surprising if things don’t pick up soon.

- On the bright side, funding rates going negative is also indicative of flushing out froth. BTC funding cratered to levels last seen in Aug. 2021 — just before it rallied from the $40Ks into a new all-time high.

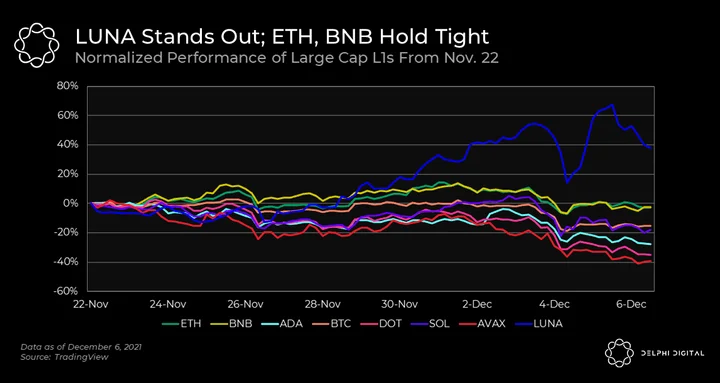

A Lunar Eclipse

- LUNA looks to be a moon mission as the only top 10 coin in the green over the last two weeks — granted it just broke into the top 10. It’s tough to say what’s causing this increased appetite for LUNA, but our best guess is it’s a reaction to the proposal to burn 90M LUNA and mint 3-4B UST.

- Despite erratic performance across the market, ETH and BNB are holding much better than other large caps (barring LUNA) — something we noticed earlier last week. Whether it’s heavy bidding or just an unwillingness from holders to sell, both of these coins have held up extremely well.

- Note that the chart above catches the top of AVAX but not the other coins as it’s indexed to Nov. 22. AVAX was closing in on new highs around then while the rest had already put in a local top. However, it’s evident that ETH and BNB have held through this entire dip with more resilience than most large coins. If things do turn around from here, both of them should outperform their peers.

Notable Tweets

How to survive crypto winters

Bear markets sharpen the mind. If you don’t have a clear, well-developed thesis, a wild price swing will have the rug pulled out from under you. Fwiw – don’t think we’re in a bear but these micro market cycles have the same effecthttps://t.co/3zF9htH6QD

— Santa-iago R Santos | #9159 ??⚡️ (@santiagoroel) December 6, 2021

What’s popping with DeFi?

1/ This week in #DeFi, a thread?

There is $101b locked in DeFi on #Ethereum @deversifi launches rewards program$DPI November rebalance @AlchemixFi II coming soon@Bancor V3 launches@defiprime lists @xdefi_wallet @layer3xyz announces new @OlympusDAO bounties

— Crypto Gucci ??| crypto-gucci.eth (@CryptoGucci) December 6, 2021

An interesting read on NFTs, IP ownership, and copyright laws

1/ @BoredApeYC giving IP rights to people through NFT is moot.. under US law there is a formal process to transfer IP and NFT isn’t it.. the author of the work still owns the IP… https://t.co/8RZEj6cXjW

— RYDER RIPPS (@ryder_ripps) December 5, 2021

0 Comments