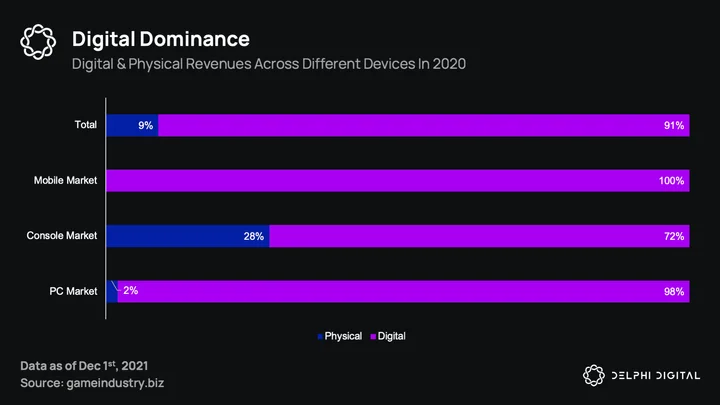

In 2020, 91% of the $175B gaming industry revenues came from digital sales. Things are only expected to go up from here, with the market for digital games estimated to reach $560B by 2028.

Digital distribution platforms play a pivotal role in this growth as they help onboard more developers and aid players in discovering the best content. As such, this report looks at the past, the present, and the future of digital distribution and where Web3 fits into it.

To better understand the opportunities and challenges facing blockchain-powered new entrants, we analyze Epic’s uphill battle against Steam, showcase four key groups of Web3 platforms, and highlight strategies that have the most potential in the short to long-term future.

State of the Traditional Gaming Market

Inception

Before diving into the current digital distribution landscape of games and the future of Web3 distribution, it is important to first understand how far we have come. In the early 1980s, companies like GameLine and Intellivision allowed console owners (Atari 2600/PlayCable) to buy specialized cartridges, dial-up, and rent games or play directly via a cable TV connection. In 1987, Nintendo released its disk writer kiosks. This Japan-only release allowed players to visit these kiosks and copy any available games to a floppy disk that could then be kept forever and played on their Famicom console (known in western markets as the NES).

Further Developments

In the 1990s, developers started using Bulletin Board Systems (BBS) (originally used to upload game demos) to allow gamers to purchase digital keys and directly download the full game. The BBS model is widely accepted as the first iteration of the PC digital distribution model we know today.

However, issues surrounding slow internet connections, high costs, and low distribution prevented any of these early distribution channels from taking off. Physical game distribution continued to hold the majority of the market share.

Along with improvements to internet accessibility and performance came the rise of downloadable content (DLC) on consoles and early digital distribution services on PC from companies like Stardock, which developed its distribution platform, Impulse, that later sold to GameStop.

Mass Adoption

From 2004 to today, multiple companies have adopted the digital distribution service model, including Steam, Good Old Games (GOG.com), EA’s Origin, and the Epic Games Store (EGS). Post-2010, the adoption of mobile gaming resulted in the meteoric rise of Apple’s App Store (for iOS devices) and Google’s Play Store (for Android devices). By 2020, 91% of the total $175B game industry revenue came from digital sales.

The Current Landscape

The proliferation of digital distribution services across all gaming hardware has shifted gaming culture. Gamers no longer visit their local game shops to buy the latest games, instead opting to download content online. So, where does that leave us now?

The current landscape of digital distribution platforms is made up of a handful of critical players spread across the different gaming hardware sectors. To analyze the competitiveness of the new Web3 players and how they fit into the whole ecosystem, it helps to look at how the incumbents are competing for market share and which areas offer the most upside potential.

Mobile Dominance

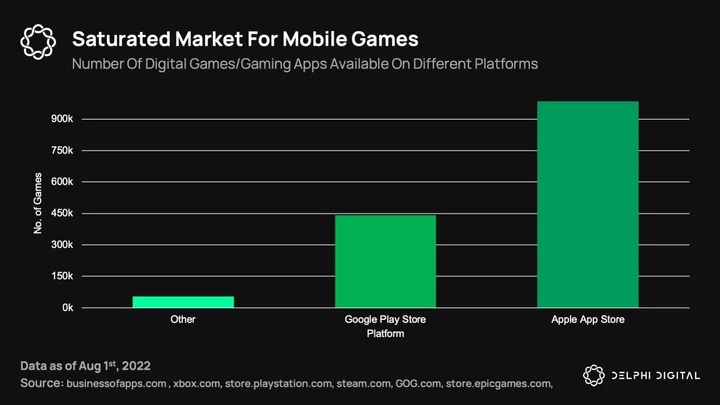

Taking the largest share of the gaming market due to its relatively low barriers to entry, mobile is an attractive hardware option for all developers and publishers. It also represents the most prominent digital distribution market, with around 1.5M games spread across Apple’s App Store and the Google Play Store.

As seen in the chart below, the number of games available on both the App Store and Play Store amount to 96% of all available games on any other distribution channel. Both mobile platforms are highly saturated, leading to discoverability issues and increasing user acquisition and retention costs. That being said, Apple recently approved the sale/trading of NFTs within apps listed on its App Store, making this a promising option for Web3 teams looking to gain access to the ~1B iPhone users (provided they don’t mind bending the knee and succumbing to new guideline limitations).

Lack of Clarity for Consoles

The console market lags behind other segments, with digital sales amounting to 72% of total revenues. However, a major contributing factor to this lower figure is likely due to hardware memory constraints. A standard PS5 has just over 600GB available for downloadable content. To put this into perspective, the latest downloadable version of Call of Duty: Black Ops Cold War required more than 130GB of storage.

Each one of the market leaders has its own proprietary digital distribution service for current-gen hardware. The Nintendo Switch has the Nintendo eShop, the PS4/PS5 have the PlayStation Store, and the Xbox One/Series X & S have the Xbox Store. It should be mentioned that Xbox also has the Xbox Game Pass, where more than 300 games can be downloaded and played for a monthly fee (Xbox reportedly brought in $2.9B in revenue from Game Pass subscriptions in 2021).

However, Microsoft, and by extension, Xbox, took a hard stance against the use of NFTs within their games. In July, Sony shared a similar sentiment, releasing a statement clarifying that the digital collectibles featured in the PlayStation Stars program were “Definitely not NFTs. Definitely not.” However, in August, the company went on to release a survey to gauge PlayStation users’ interest in NFTs during Evo. Nintendo has also expressed interest in NFTs, but the focus is more on developments toward a Nintendo metaverse. This all goes to show that Web3 developers will most likely need to wait for further updates before engaging in a console-first approach.

Potential for PC

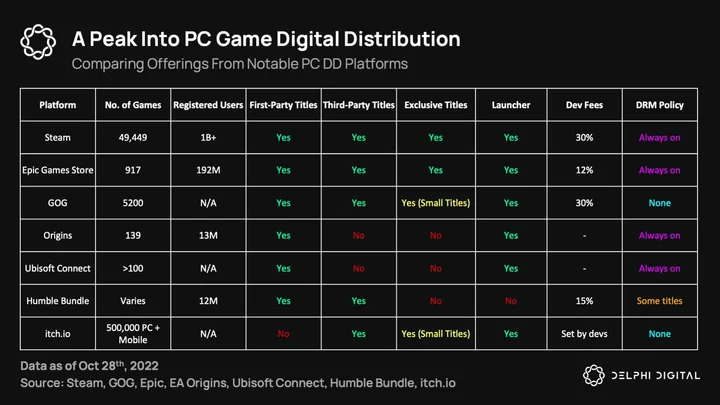

The PC digital games market is predicted to grow steadily over the next five years, reaching $19.33B by 2026. The PC market has a diverse selection of digital distribution platforms to choose from, all providing the same core service. The main differences that generally result in a user picking one platform over another are:

- Social features and community activity

- The number of available games

- The number of exclusive titles on offer

- The presence/absence of a Digital Rights Management (DRM) policy

It should also be mentioned that the fees paid by developers for the privilege of listing on these platforms vary, but the industry standard is widely considered to be 30%. Although this has little consequence for the end user, the difference in earnings received by game teams could be the deciding factor when choosing which platform to launch on.

Additionally, some platforms like EA Origin (soon to be rebranded to the EA PC App) and Ubisoft Connect have chosen to only offer first-party titles. Other platforms have taken a more novel approach, carving out their niche next to other, more funded incumbents.

Humble Bundle, for example, introduced a pay-what-you-want model and allowed users to donate a portion of their purchases to charity. Itch.io has also taken a different approach by focusing almost entirely on indie titles. This provides another option to teams with small budgets and allows developers to set their own DRM policies/fees.

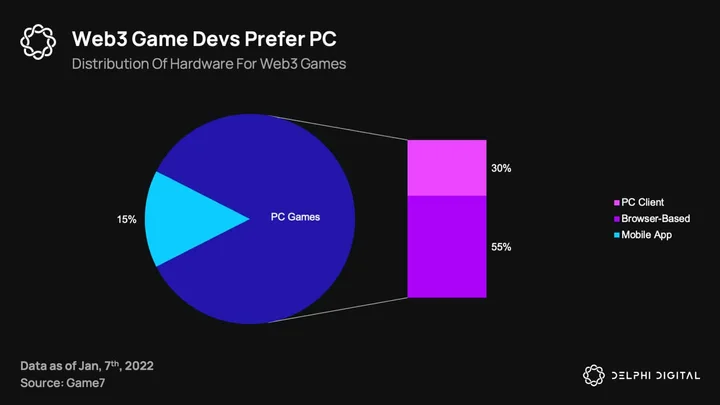

Despite companies like Steam taking a strong stance against the use of blockchain on their platforms, Web3 developers still have the propensity to build games designed for a PC-first launch (including browser-based games).

For this reason, and due to the previously mentioned discoverability challenges on mobile and unclear positioning of console providers, this report will continue to focus on analyzing the current selection of Web3-native digital distribution platforms focused on the PC market and how they match up to the Web2 competition.

Web3 Landscape

When examining the Web3 landscape, it quickly becomes apparent that due to the nascent nature of the industry, things are not as clearly laid out as they are in the traditional digital distribution market. It is also important to preface this by outlining two key challenges preventing the widespread adoption of blockchain-based games; high barriers to entry and discoverability.

Which Chain to Choose?

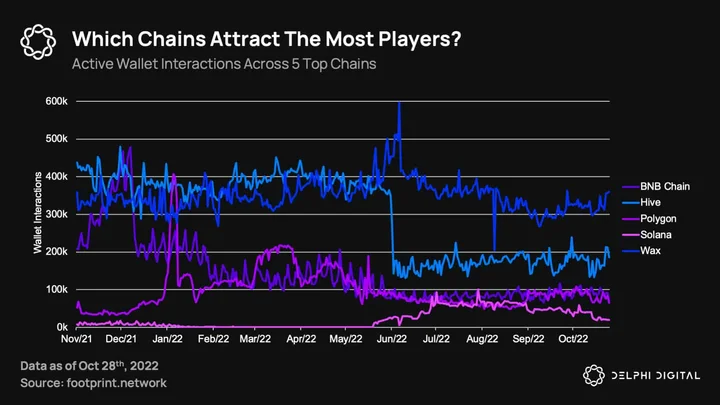

The story starts with the battle of the blockchains, where the most prominent providers are fighting among one another to offer the most funding, the fastest and cheapest transactions, the highest level of support, and the best suite of SDKs/APIs to attract more game developers into Web3. You can read more about which chains are best suited for gaming in our previous report on the subject here.

The chart above illustrates the number of active wallets interacting with gaming protocols, which can be taken as rough insight (wallet interactions do not equate to active players) into the interest in gaming throughout each of the largest blockchains.

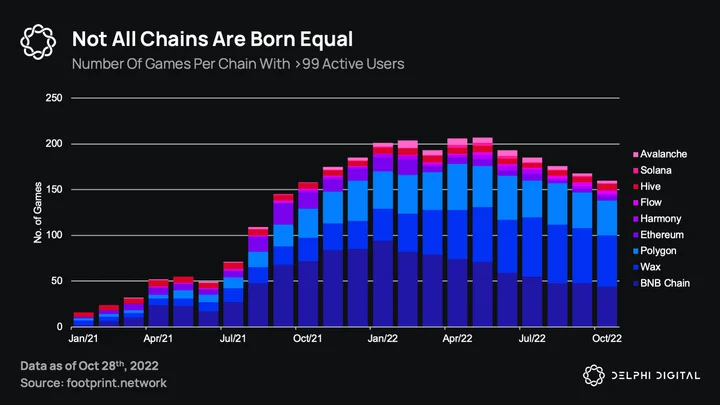

Interactions on Hive and WAX are dominated by three games: Splinterlands, Alien Worlds, and Farmers World, which slightly skew the chart. However, it is encouraging to see the “underdog” Solana slowly catching up to the more established gaming chains, BNB and Polygon, which both see many new games being deployed each month (see below).

Platform-as-a-Service

There are a plethora of platforms that offer services specifically designed to attract gaming teams. Projects like Enjin, Stardust, and Fractal offer features to make it easier for developers to incorporate blockchain elements into their games and improve the onboarding process. Custodial Web3 wallets, social sign-ins, first and third-party marketplace integrations, and tournament integrations are all ways these platforms help to reduce barriers to entry.

However, despite creating a smoother experience to encourage more experienced gaming teams to join Web3, on the user side, these platforms still primarily cater to retail investors as opposed to real gamers.

Fractal is a good example; the Solana-based NFT marketplace never planned to compete directly with the likes of OpenSea. Instead, the platform has taken a game-centric approach to become the open amusement park of Web3 — a one-stop shop for players to engage with different games within the same ecosystem.

Through its curation process, Fractal hopes to become a discovery platform that attracts high-quality games and gamers. The challenge here is that the platform’s current focus is on NFT mints and trading. As such, it is still uncertain how successful the platform will be in improving discoverability and player onboarding, since that is not their core focus, or if the existing user base will be interested in engaging with these games on a deeper level.

Web3 Distribution Platforms

Enter Web3 digital distribution platforms that focus predominantly on discoverability and player engagement. With a rapidly increasing number of playable blockchain games, and many more due to launch over the next 12-24 months, would-be Web3 gamers ask: where should I invest my time and money?

Like the console market, most traditional gaming platforms have kept NFTs at arm’s length as they wait for the market to mature. In their current iteration, several factors such as technological infrastructure, gameplay mechanics, and community culture represent a stark contrast to their traditional Web2 counterparts. This begs the question of whether a Web3-native distribution platform would be better suited to provide value to game devs and players.

Four Key Subgroups

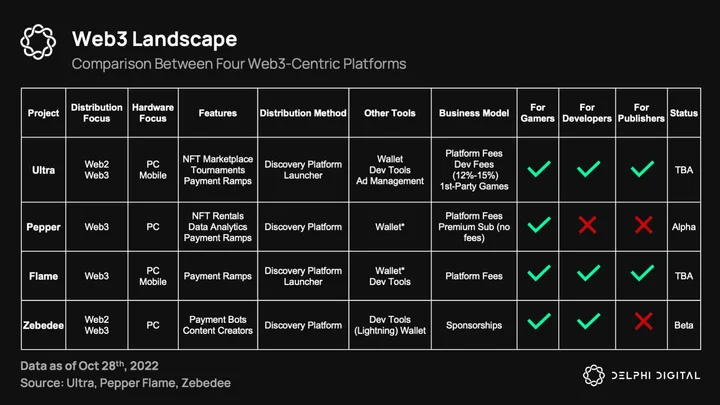

Several teams are building the “Steam of Web3.” Although this phrase is thrown around quite haphazardly, we will highlight four projects paving their own unique path to becoming the hub for Web3 gaming.

Flame, the Purist

Developed by Ryu Games, Flame is a consumer-centric discovery platform and Web3 game launcher. Ryu initially helped mobile developers implement cash tournaments in their games, and has since gone on to develop a Web3 game alongside Flame. In June, they were joined by Rick Ellis, the original lead developer of Steam, who will act as the Chief Product Officer.

Flame can be described as the purest option within this list, with three guiding pillars: usability, discoverability, and trust. The focus is simple, build a platform that makes onboarding into Web3 as frictionless as possible. The core offering will remain as similar to incumbent Web2 platforms as possible but focused solely on blockchain-powered games. The open beta will launch at the end of the year, and users can expect several “no frills” features upon launch:

- Non-custodial wallet with single sign-on (third-party integration)

- NFT marketplace (third-party integration)

- Fiat on/off-ramp

- Game launcher

A clear trend across all projects on this list is to abstract blockchain hassles as much as possible. Players don’t want to worry about setting up a wallet and paying gas fees, so this should be considered the bare minimum for any project. Most projects have removed gas fees altogether, following ImmutableX’s process of relaying gas fees and moving the costs over to other areas, such as trading/withdrawal fees.

Unlike the large incumbents, which have had years to build reputation, trust, and demand from developers, Flame and similar competitors such as Elixir have had to use other strategies like making developer fees void as an additional incentive. After all, without any games, how do they hope to attract the number of users necessary for network effects to take place?

To date, Flame has announced around 50 games that will be available upon launch, and curation is already a potential concern. Web3 distribution platforms do not have the luxury of selecting only the best games; there quite simply aren’t enough of them. So to have a diverse offering, many platforms have succumbed to quantity over quality (more on this later).

The Ultra Ecosystem

Ultra Games is Ultra’s first-party game distribution platform and launcher focused on onboarding the masses into Web3. Where Ultra Games differs is in several subtle but potentially impactful ways. Let’s start by touching upon the Ultra ecosystem, which the team has been adding to since 2017.

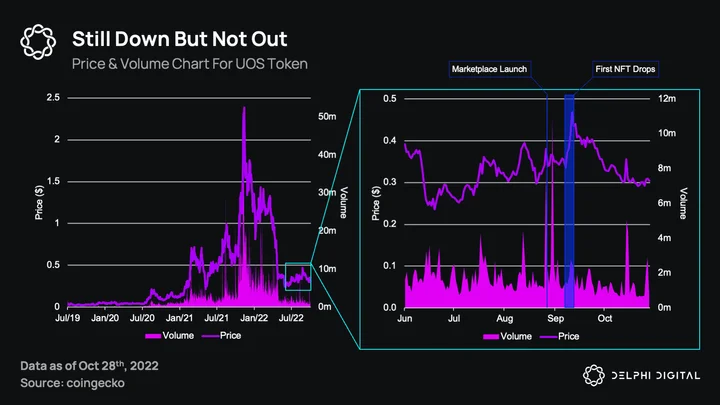

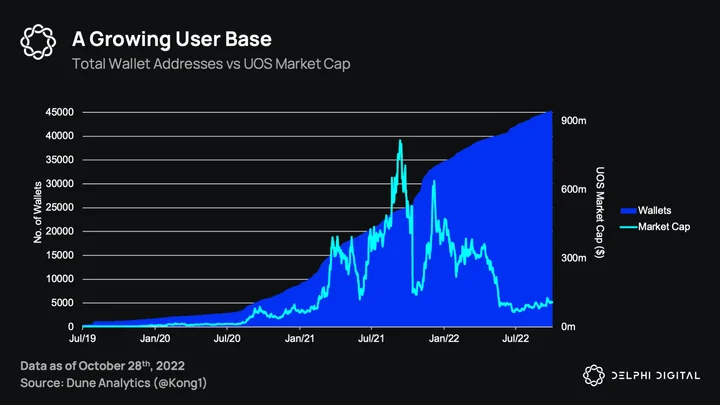

Ultra currently consists of its custom EOSIO blockchain, the UOS token, a low-friction non-custodial wallet, the UNIQ NFT marketplace (beta), and the soon-to-be-released Ultra Games launcher and Ultra Arena. The most recent consumer-facing product released by the project was the UNIQ NFT Marketplace.

In the build-up to the marketplace’s launch on Aug. 29th, the price of UOS saw an initial increase of 21% followed by an additional pump of 46% during the release of the first few UNIQ NFT collections (purchasable only in UOS) from Sept. 7th-11th. This event also resulted in the highest levels of trading volume for UOS in the past 99 days.

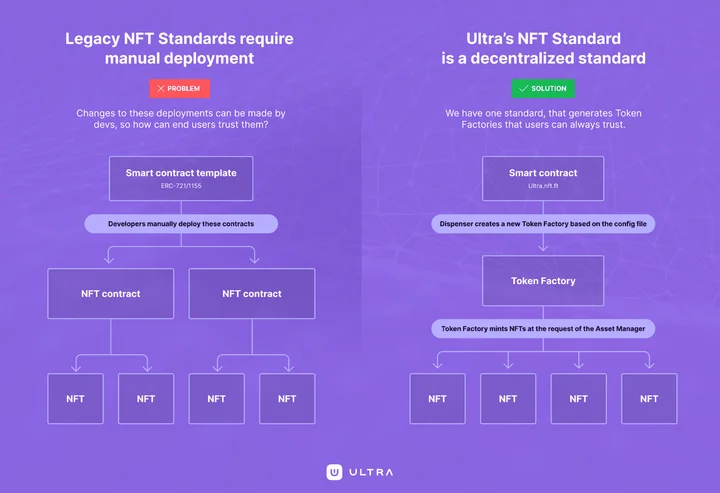

UNIQ NFTs will play an essential role throughout many of the projects listed on the Ultra Games platform. The team has designed a new NFT standard that allows studios to control asset distribution efficiently, along with the expected functionality to buy, sell, and trade both in-game assets and preowned games. Using UNIQ NFTs as the de facto medium to produce and distribute player-owned assets presents several benefits to creators and users, with the platform’s stakeholders being split into three subgroups:

- Asset creators

- Asset managers

- Asset owners

Asset creators follow the standards provided by Ultra to create a Token Factory (TF), and use a predefined series of parameters for collection size, royalties, etc. They can then assign themselves or a separate entity as the asset manager who executes the order to allow an NFT to be minted by an asset owner.

Once created, a TF cannot be altered, ensuring the immutability of an owner’s assets. Furthermore, this approach provides peace of mind to asset owners. They trust the UNIQ contract standard, which alleviates some of the hassles and costs associated with blockchain contract creation/maintenance for developers.

The UNIQ marketplace is still in beta, and thus only offers a set of basic minimum features (buy/sell/transfer) along with allowing asset creators to set the price of their NFTs in fiat currency (still purchased in UOS). Future updates are coming, and some of the more interesting ones to keep note of are:

- Redeem codes (special offers/gifts distributed by the platform, partners, and influencers)

- Price secondary NFT prices in fiat

- Game tokenization, allowing for the sale of second-hand games

The next big release from Ultra will come from its first-party distribution dashboard + launcher, Ultra Games. At its core, Ultra Games offers players a safe place to come and play the best games (sound familiar?). They differ from the competition in how they plan to offer Web2 and Web3 games side-by-side, with 2,500 games already confirmed (including a few exclusive titles).

Another differentiator is the ability for users to re-sell their games as NFTs, an interesting move that aims to bridge this once almost $100M market (it has dropped a considerable amount since 2019) into the digital realm and pay developers for the privilege. Only time will tell if future generations of gamers will be interested in what many assume to be the “old way of doing things.” Still, it does present potential upside for lower-income households and additional revenue streams for developers.

Ultra has been building its ecosystem for the past ~5 years; this is a long time compared to the <1 year it will take Flame to go to market. The team argues that this was necessary, as existing gamers are already spoiled for choice in the Web2 market, requiring the platform to go above and beyond the competition (including Steam) in providing value to both players and developers.

It is worth noting that Ultra Games is the only project on this list to charge developers a 15% fee (12% with the referral bonus). Whether or not the additional technical support and infrastructure justify this added cost when Epic Games Store (EGS) has a much larger user base and the same fee structure is yet to be determined.

Pepper Pivots to Find its Niche

Pepper is the black sheep of the group that started as the typical Steam clone with added Web3 functionality, but recently pivoted to redefine its value offering. Instead of creating a platform for players that solely focuses on discoverability and easy onboarding, Pepper has decided to become the Web3 gaming-centric analytics platform for player earners.

The words play-to-earn are now often associated with a “too good to be true” type of game design that struggles with balancing the amount of value extracted with that which is recirculated. This report is not meant to be a retrospective look at the state of Web3 gaming and where it is going. If that is what you want, read our “The Future of (Crypto) Gaming” report. The point is that many have grown wary of play-to-earn and have shifted focus to games that put fun first.

The team behind Pepper believes that there will always be a place for play-to-earn. More importantly, where there are financial incentives, there will be min-max players who seek to maximize their earning potential. In this vein, Pepper will provide this subset of players with a suite of analytical tools to help them assess their assets holdings and better strategize their path to profits.

Pepper, and platforms with a similar focus like Playio and PlayCore, will use on-chain data to analyze where money flows and how players can best allocate their funds — initially offering users basic tools to monitor and analyze their asset portfolios. Over time, this toolset will expand to include features allowing players to perfect their metagame with arbitrage alerts, game overviews, and enough charts for you to never open an excel sheet again.

I know what you’re thinking — this doesn’t sound much like a distribution platform — and you are half correct. Pepper is no longer what you would call a typical digital distribution platform. Despite this, they are carving out a niche that caters to a particular type of gamer. The platform will still aim to reduce friction as much as possible by allowing for SSO cross-chain wallet creation (thanks to their partnership with Wallet Connect), and will work to help educate users on the risks/rewards of financially-driven Web3 gaming models.

If games like Axie Infinity and STEPN have taught us anything, financial incentives can convert a sizable number of people who never previously considered themselves gamers. Pepper could help indirectly onboard these users into many of the games listed on its platform. By providing value to players, they will be more open to exploring what else is on offer.

ZEBEDEE Puts a FinTech Foot Forward

ZEBEDEE is somewhat similar to Pepper in that the platform has matured since its conception three years ago. In its current form, the project is self-described as a FinTech company for gaming that supports crypto payment integrations within new and existing games. ZEBEDEE started as a wallet solution but quickly expanded into game development and more.

What stands out about ZEBEDEE is how they have fully committed to building out the existing Bitcoin ecosystem. They argue that Bitcoin is the most widely-adopted cryptocurrency. It has a robust network that has never gone down in 13 years, maintains a relatively more stable price than other coins, and allows for more reasonable in-game earnings (no future 100x here). It should also be noted that ZEBEDEE is highly focused on hyper-casual mobile games (although PC games are also featured on the platform), which is something none of the other platforms have fully embraced yet.

Since ZEBEDEE is using the Lightning Network, the payment features utilized throughout their various offerings can still benefit from fast transaction speeds and low fees. Additionally, the project opted to use Satoshis (sats) (1 BTC = 100,000,000 sats) for pricing on the platform to facilitate microtransactions.

Like the other projects on this list, ZEBEDEE has taken a two-pronged business model approach, developing features that appeal to both developers and end users with the current list of offerings consisting of:

- The ZEBEDEE app (which includes the first-party custodial wallet and game discovery dashboard)

- SDKs and APIs for game developers to integrate crypto payments

- Developer Dashboard for developers to better manage their games

- ZBD Telegram and Discord payment bots

- ZBD Login (a universal login (SSO) system)

- ZBD Gamertag

- ZBD Streamer

- ZBD Infuse

We have seen how reducing the barriers for new developers to be onboarded into Web3 can help to produce a larger quantity of good games (which will likely incentivize more players to join), but let’s take a deeper look into what ZEBEDEE is doing to attract gamers directly via ZBD Gamertag, ZBD Streamer, and ZBD Infuse.

The ZBD Gamertag is a straightforward feature that enables anyone who downloads the app to create their own username that is instantaneously connected to a private Lightning Network wallet. Furthermore, this account is now able to send and receive funds using the Telegram and Discord bots or any of the other 20 compatible Lightning Network wallets and generate a unique static QR code with the same functionality. What does this have to do with gaming, you say?

This is where ZBD Streamer comes in. This free-to-use payment application has been designed to allow gaming content streamers to import their QR code onto any streaming platform, immediately enabling sats donations with 0 fees and a minimum of 1 sat payments (roughly $0.00005).

ZBD Infuse allows existing games to integrate ZEBEDEE’s play-to-earn functionalities. The team has used the PC-based application to create their own CS:GO server that enables in-game sats earnings for players based on their score, with more games expected to be launched soon.

In many respects, ZEBEDEE’s complete ecosystem strategy resembles what Ultra is building, in that they offer a suite of value-add features for developers and players. However, because their core competencies lie in payment systems, and not the discovery platform, their user growth strategy is more similar to Pepper.

As more developers and streamers integrate with ZEBEDEE, they will attract more players focused on the earning/payment features on offer. These players, who now have a cross-game wallet, will want to use the platform to find the best earning opportunities or the most enjoyable games to spend their Bitcoin.

Platform Before Players

The blatantly obvious difference between the Web3 approach to distribution platforms and how traditional incumbents approached the market is in the order of development. Valve released several hit games (Half-Life, Team Fortress, and Counter Strike) before creating Steam in 2003 to push updates to their first-party titles. In 2005, Steam went on to include third-party titles on the platform, and by 2007, the platform had 15M active users and more than 200 games (this grew to 40M users by 2011).

Similarly, Epic used Fortnite’s success to immediately convert players into users on the EGS (launched in 2018). They have since spent hundreds of millions securing exclusive titles for the platform to capture some of Steam’s approximate 50-70% market share.

However, excluding a few short-lived successes, Web3 has yet to see any strong breakout titles, leading to teams first building out the platform-level infrastructure. This approach strongly resembles what we saw in the early 1990s, when platforms believed that the players would come but were thwarted by technical limitations.

That being said, those same limitations are now a thing of the past. An approach to focusing first on reducing barriers for game developers and players may provide these platforms with a competitive advantage. Will this be the catalyst for the first big Web3 game to onboard the masses?

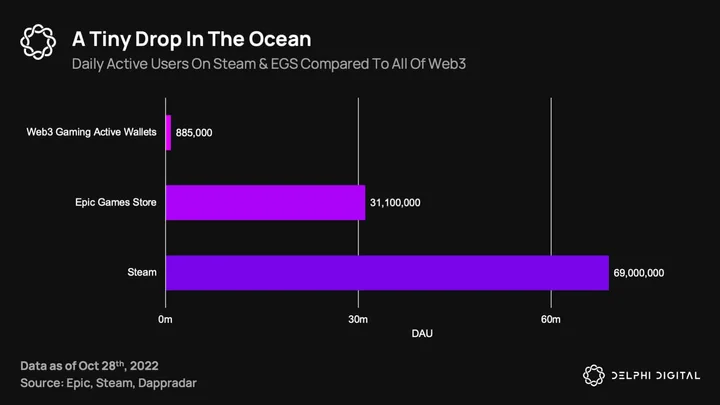

There are currently just under 900k daily active wallets interacting with Web3 gaming dApps. This figure reached over 1.4M at the height of the bull market in November 2021. Active wallets do not directly correlate to active players, but even if they did, these numbers still pale in comparison to the more than 3B global gamers.

EGS vs. Steam

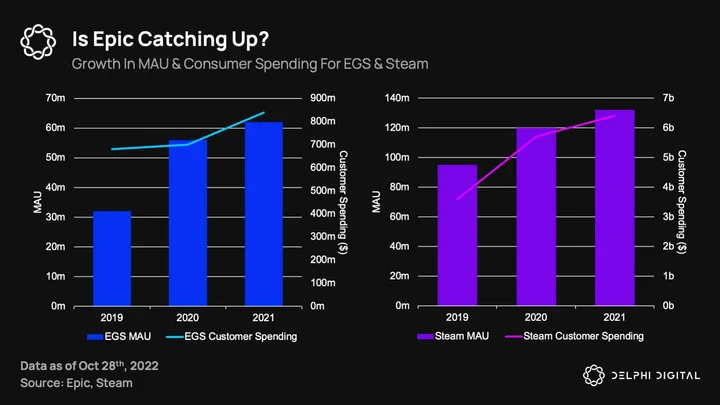

To further analyze the opportunities and challenges facing these Web3 distribution platforms, it is helpful to look back and evaluate EGS’ uphill battle against Steam. Steam has been the market leader since the early 2010s, and in recent years, has seen accelerated growth thanks to the COVID pandemic, with the platform growing 74% over the past three years. In 2021, Steam grew 11%, outpacing the entire game industry’s 7.3% for that same year.

This is to say that EGS needed to do more than rely on Fortnite’s chart-topping success. They needed a solid strategy and a compelling value proposition to incentivize users to switch.

For developers, EGS lowered their fees to 12% (18% less than the industry average) and released Epic Online Services (EOS) for free, which enables cross-platform, cross-play, and a host of other social features.

For gamers, they offered free premium games each week (763M free games were claimed by users in 2021). Additionally, Epic spent $444M in 2020 to secure exclusive titles that are not permitted to launch on Steam for at least one year.

This aggressive user acquisition strategy has seen total registered users increase by 77%, but this didn’t come without drawbacks. The platform suffered net losses of $181M, $273M, and $139M in 2019, 2020, and 2021, respectively, and Epic does not expect the platform to be profitable until 2024. The question is, what impact has this investment had on EGS’ growth compared to Steam?

2020 was a year of growth for these two platforms, just in different ways. EGS saw monthly active users increase by 75% compared to Steam’s 26%. However, this could be due to the large number of free and exclusive games distributed by the platform, seeing as customer spending on Steam grew 58% compared to EGS’ measly 3% (although EGS did see spending increase 20% in 2021 compared to Steam’s 12%). So what are the key takeaways for Web3 builders?

Takeaways for Web3

First and foremost, the digital games industry will only get bigger, with some estimates stating that digital games will become a $560B market by 2028. As lockdown and console shortages become a thing of the past, Steam will likely end the year near pre-covid revenue levels. However, the platform set three new records for the total number of concurrent players, two in January and one in October, which took the number to more than 30M.

Steam continues to update its features to improve the user experience, and the EGS has started to list blockchain games on the platform in anticipation of a Web3 revolution. With the competition not slowing down, how can Web3 platforms hope to have a fighting chance?

ZEBEDEE and Pepper are in a position of indirect competition, and thus have a little more breathing room to focus on their target market. However, Ultra Games and Flame see themselves as direct competitors to EGS and Steam. Glancing past the fact that they will be taking a more decentralized approach, what can they do to have a chance of capturing any meaningful market share?

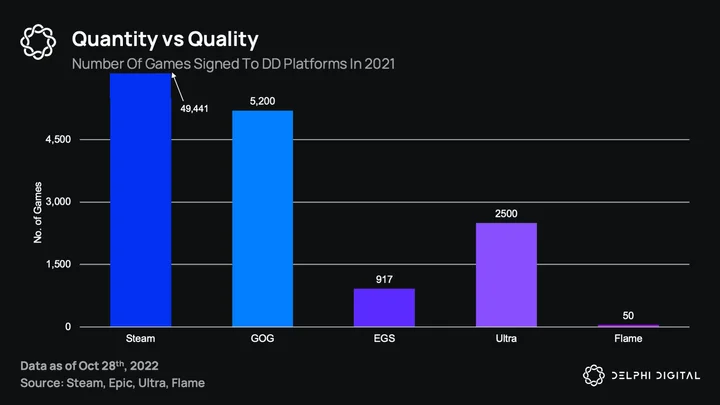

Quantity vs. Quality

As previously mentioned, EGS’ strategy to provide users with free premium games and exclusive titles is a winning formula for active user growth. However, it is unlikely that any Web3 companies in this report have enough capital to employ such a costly strategy.

In 2022, Ryu Games (Flame) raised $2.7M, and Pepper has completed funding in an undisclosed seed round. ZEBEDEE raised $46.5M in series A and B rounds in 2021, and Ultra raised $5M during their ICO in 2019, later raising an additional ~$1M from other revenue streams.

That being said, Steam doesn’t focus on free games, but on providing its users with the widest variety of games. So, is quantity better than quality?

One of the biggest complaints about the Steam platform is the lack of curation. Similarly, we have already touched upon the difficulties surrounding discoverability on mobile platforms like the Apple App Store or Google Play Store. Unfortunately, as Web3 gaming is still in its infancy, platforms are not in a position to be picky.

GOG has been praised for its more curated approach, and they still have more than double the games of the closest Web3 competitor. Because there isn’t enough choice in the current Web3 market, more importance will be placed on the number of total blockchain gaming users, with the upper hand potentially going to platforms that secure the most popular exclusive titles (like what Ultra is trying to do).

User Acquisition

The last piece to the puzzle is the number of users ready to engage in these platforms. We have already covered the Web2 competition (quick reminder: EGS had 192M registered users as of 2021, and Steam has >1B), and due to the majority of Web3 platforms still being in development, Ultra and ZEBEDEE have first-mover advantage here.

Despite the rocky market conditions, Ultra has managed to amass over 40,000 unique Ultra wallet addresses. The Ultra wallet plays a pivotal part in the entire ecosystem, so when Ultra Games launches later this year, these users will already be familiar with the ecosystem, and a portion of them will be immediately converted into platform users.

ZEBEDEE is in an even better position, with their app already live and multiple games fully integrated within it. At the time of writing this, the app has 100k downloads on the Google Play Store, but it is unclear how active these users are, and reviews would indicate that the experience is not yet void of issues.

A large and sustainable user base is the crucial ingredient Web3 platforms are missing. Savvy marketing and strong partnerships will likely provide the most upside to these platforms in the near term. In the mid to long term, if they wish to compete with EGS, they will need to either deliver an objectively better experience to players or carve out their own Web3-centric niche.

Summary

Digital distribution for video games has gone through many iterations over the past ~40 years, but only in the last 10 years did we see significant uptake from players. Estimates now indicate that digital games are the norm, and incumbents fiercely fight for market share.

The inception of blockchain gaming saw an opportunity for Web3-native platforms to design tailored services to help alleviate some of the more pressing pain points facing blockchain-based games and Web3 gamers. However, these early-stage platforms have not followed their predecessors’ footsteps, and are launching before any notable first-party breakout successes.

There may be little historical evidence that a platform-before-players approach will deliver any meaningful results in the long term. However, teams that can carve out their niche or encourage user growth by means not accessible to traditional Web2 incumbents may have a competitive advantage. Alternatively, those that onboard the largest selection of popular Web3 games and exclusive titles, coupled with good marketing, may find the most success in the short to mid term.

0 Comments