Aave on AVAX, Delta One Farming, & veToken Alternatives

APR 20, 2022 • 8 Min Read

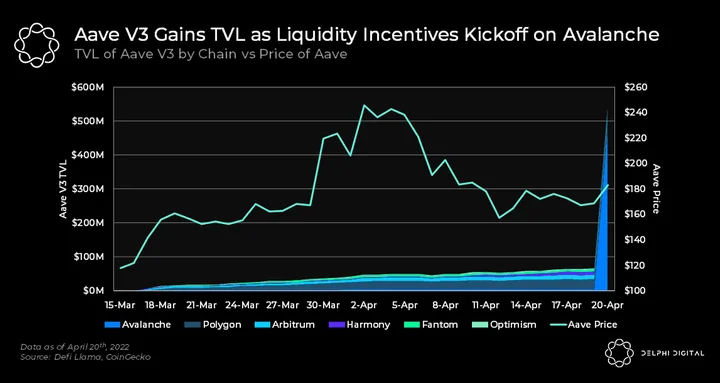

Chart of The Day: Aave V3 TVL Boosted by Avalanche

![]()

- Aave V3 is a new and improved version of the blue-chip money market. Aave V3 introduces two modes to the high-efficiency mode (“eMode”) and Isolation mode.

- eMode will unlock utilization amongst a category of assets, allowing for higher LTV of up to 95% to 98%. According to Aave, -” A “category” typically refers to a set of assets pegged to the same underlying asset—for example, stablecoins pegged to USD, assets pegged to ETH, etc.”

- Isolation Mode will isolate risk for certain assets deemed to be riskier while still unlocking their capital efficiency. Isolation Mode allows select assets to be used as collateral up to a certain debt ceiling. However, borrowers can only borrow stablecoins and may not use another asset as collateral simultaneously. To list an asset as “isolated collateral,” it will be required to go through a governance proposal before being listed.

- With the launch of liquidity mining on Avalanche, capital started flowing into Aave V3 on Avalanche to take advantage of the lucrative yields. TVL spiked from $67M yesterday to $537M today at the time of writing. This is expected to continue going up as the mining rewards are still attractive. Do take note that when supplying USDT and USDC, only the native version is allowed as deposits and the bridge version (USDT.e and USDC.e) are not allowed as deposits.

- To learn more about Aave V3, check out our recent Delphi Pro report here.

Boosted Stablecoin Farm, Delta-Neutral Strategies & Pre-Farming on Bridges

[Excerpt from Apr. 19th Yield Insights]

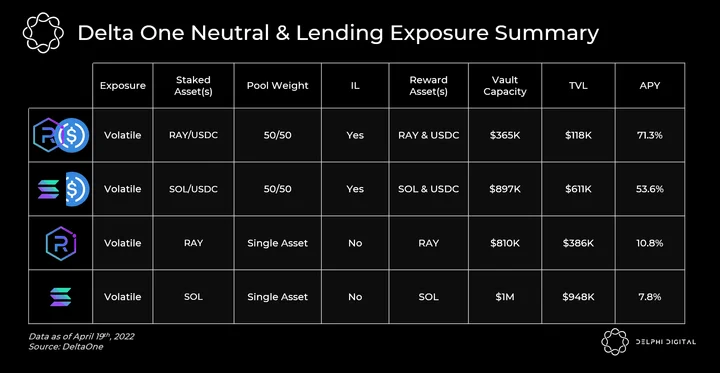

Delta One Farm

- Delta One aims to democratize sustainable yield to the next wave of DeFi users through yield generating structured products and a delta-neutral stablecoin. These delta-neutral and impermanent loss-free farming markets allow users to price their risk, and hedge away unwanted exposure. Learn more about it here.

- Yield Calculations can be found here. To access Delta, you’ll need to connect to a Solana-compatible wallet.

- Bridge: You can deposit and withdraw assets onto the Solana using the Wormhole Portal.

- Tokenomics: When a user deposits assets into a strategy, they get a reserve currency token that represents their share in that Delta strategy’s pool. As Delta Protocol yield farms based on that strategy, its pool increases in value. Thus, the user can hold a non-inflationary reserve currency that is justifiably increasing in value, as it is pegged.

- Delta also offers a stablecoin and wrapped asset suite. Every time a user deposits 1TOK, 1 d-TOK is minted by Delta. Every time 1 TOK is realized in yield profit, 1 d-TOK is minted. Thus, d-TOK is 100% backed by an equivalent amount of TOK in some yield farming strategy pool. For USDC, USDT and CASH, Delta has thus created d-USDC, d-USDT, and d-CASH stablecoins.

- Delta encourages users to withdraw their initial investments + yield in terms of these Delta stables since they do not have any withdrawal fees. These stables will also be listed on Saber for further staking incentives.

- Delta Neutral Strategy: Delta neutral is a portfolio strategy utilizing multiple positions with balancing positive and negative deltas so that the overall delta of the assets in question totals zero. Learn more about it here.

- Risks: If the pool which the strategy utilizes becomes imbalanced, the vault’s smart contract may need to use the user’s funds to buy additional Altcoin tokens to repay the lent amount (plus interest), which can result in a net loss from the initial deposit. All APR and yield numbers are speculative, and no profit is guaranteed by the protocol.

- Whitelist: Since Delta is currently in BETA, you need to join the discord and ask to be whitelisted.

- As always, please exercise extreme caution if you intend to participate in these opportunities. Happy farming everyone!

- For more, Delphi members can see the latest Yield Insights here.

An Alternative Implementation of veToken Economics

[Excerpt from a Delphi Report]

Curve and veToken Economics

- The rise of crypto and tokenization has blown the design space for protocol economics wide open, allowing projects to incentivize specific behaviors. Yet, many DeFi protocols reward all token holders equally, independent of the value they add to the project. More often than not, this involves little to no lockups in exchange for receiving governance power and protocol revenues. We believe the optimal design aims to dilute mercenary capital and speculators, while rewarding value additive and long-term oriented participants.

- One such model we feel encourages this behavior is the vote-escrowed implementation introduced by Curve. This model allows CRV holders to lock up their tokens as vote-escrowed CRV (veCRV) for up to 4 years. The longer a user locks their CRV for, the more veCRV they receive. In exchange for taking on liquidity risk and removing CRV supply from the market (showing their long-term commitment to the platform), veCRV holders are entitled to 3 main benefits:

-

- A prorated share of fees generated by Curve.

- Boosted CRV rewards on liquidity provider positions (up to 2.5x).

- Governance and gauge weight voting power. Importantly, the gauge weight dictates how Curve’s future emissions are distributed.

- The above set of incentives generates a positive flywheel. The more long-term oriented a user is (measured by their veCRV), the more rewards they will receive. This flywheel is one of the most important dynamics of the veToken model and will be explored in detail in the next section.

- The long-term value proposition of Curve is for it to be the deepest, most liquid place to trade stable assets. The goal isn’t necessarily to be the main DEX for everyday swaps, but to empower stablecoin projects to build large liquidity reserves. This means their main users on the supply side are liquidity providers.

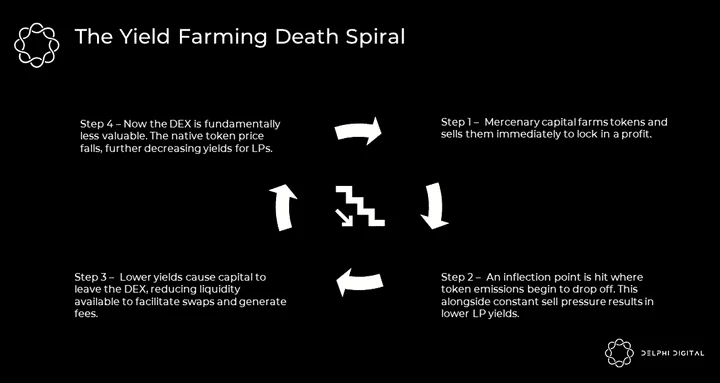

- Many failed yield farming schemes have blown up due to unsustainable token emissions and the proliferation of mercenary capital. The following is an example of what veToken economics aim to avoid:

-

-

An initial liquidity mining program is kicked off and mercenary capital deposits large amounts of money for the sole purpose of farming and dumping rewards.

-

Initially, this has reflexivity to the upside. As TVL and “hype” surrounding the project increases, it causes the token price to appreciate. This can further increase the yields offered on deposits given yields are paid in the native token, thus continuing the cycle.

-

Eventually, an inflection point is reached where token incentives begin decreasing, all the while mercenary capital continues to sell their farmed tokens. This selling alongside token emissions dropping off results in reduced yields for liquidity providers.

-

A reflexive loop to the downside begins to take hold, as liquidity exiting the DEX makes it fundamentally less valuable. Lower liquidity means the DEX can’t support as much trading volume and thus generates fewer fees. This leads to a further depreciation in fundamentals and a decline in the native token price, further lowering yields for LPs.

-

- The veToken model avoids this by aligning liquidity providers with the long-term interest of the protocol.

- For liquidity providers on Curve to capture the 2.5x boost on their rewards, they must hold a certain amount of veCRV relative to their liquidity. This incentivizes LPs not to dump tokens but instead:

-

- Purchase a position of CRV on the open market and lock it.

- Lock part or all of the CRV they receive as rewards for providing liquidity.

- In turn, this encourages liquidity providers on the Curve platform to become long-term stakeholders and supporters of Curve’s success – as opposed to employing mercenary farm-and-dump strategies.

- Furthermore, not only are LPs incentivized to lock up for the 2.5x boost, they are incentivized beyond that to accumulate as much veCRV as possible. This is because veCRV sets the gauge weight, allowing holders to direct emissions to the pools they have capital in (more veCRV = more influence over emissions).

- We have seen the accumulation of CRV play out not only among large LPs, but on a protocol level via Convex. Protocols are tapping into Convex’s large veCRV holdings and accumulating CVX to incentivize their pools in perpetuity, ensuring liquidity over the long term.

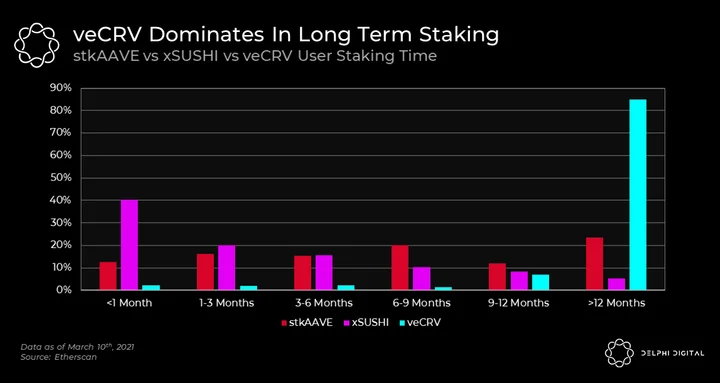

- Through a combination of CRV’s drawn-out distribution schedule (over 300 years, declining 15% per year forever) and veToken economics, it has been able to incentivize a group of very sticky liquidity providers and token holders. This can be illustrated by the time-locked/held between stkAAVE, xSUSHI, and veCRV.

- Beyond economics, veCRV also provides time-weighted governance powers to lockers, which also elegantly aligns incentives (people who lock up the longest have the most influence over governance)

- For more, you can see the full Delphi Report here. It’s free to view!

Notable Tweets

Intr9o to zkLend

StarkNet is an amazing creation of

@StarkWareLtd

on its way to become one of the greatest scaling solutions for Ethereum.I have been looking recently into the most promising DeFi projects on StarkNet and

@zkLend

Caught my attention, here is why 👇🧵👇1/8

—Omar 🔺👁🔺 187 🧹 (@OmarOnChain) April 20, 2022

$USN Leaks

Andre is certainly as engaged in crypto as ever.

No doubt the troll comments will flow below.

But something to think about.

https://t.co/Wj6ANSX6xD

—Noela is building on Near (@noela_crypto) April 20, 2022

BreederDAO Introduces Playcore

WHAT IS PLAYCORE? 🧵

Playcore is your Bloomberg for Blockchain Gaming. It is an analytics and content aggregator for anything and everything play-to-earn and play-and-earn with the goal of educating the community with rich media and data.

— Renz $BREED (@Renz_BDAO) April 20, 2022

0 Comments