Aave V3: A Multi-Chain Liquidity Protocol

FEB 03, 2022 • 14 Min Read

Report Summary

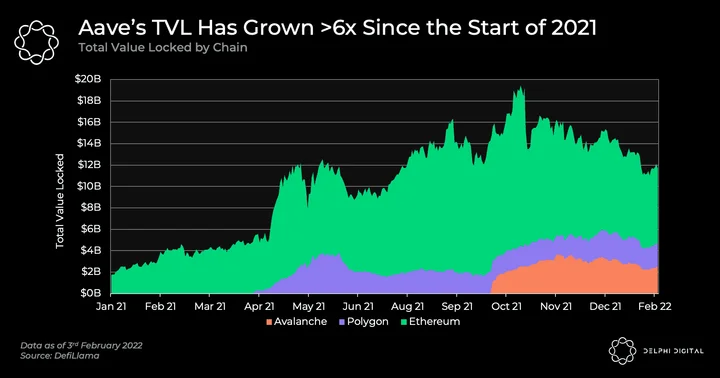

Aave is currently the fourth largest DeFi protocol with ~$15bn in TVL, equating to more than a 6 fold increase since the beginning of 2021. They are the largest cross-collateral money market on Ethereum, Polygon and Avalanche and will soon be deploying on other chains.

Aave v3 has recently launched on testnet and will soon go live with new features such as Portals, High Efficiency Mode and Isolation Mode, among other improvements.

Portals offers whitelisted bridge protocols like Connext, Hop Protocol and Synapse access to credit lines which can be used to facilitate cross-chain transactions when there is insufficient liquidity on the native bridge protocol.

With High Efficiency Mode, users are granted a higher LTV if the borrow and collateral asset falls under the same category as “pegged” assets such as stablecoins. Utilization rates on stablecoins have been consistently high during certain periods of time. Allowing higher LTVs may thus put pressure on this metric and increase liquidity risk for lenders.

Isolation Mode allows select assets to be used as collateral up to a certain debt ceiling. However, borrowers can only borrow stablecoins and may not use another asset as collateral simultaneously. Other solutions to deal with isolated lending markets include Kashi, Fuse and Silo Finance offering varying levels of permissions, market risk, and capital efficiency.

We note that Compound Finance has also recently announced their intention to establish a cross-chain presence to build out “multi-chain share liquidity pools”. Given the competitive landscape, Aave’s ability to innovate and integrate faster remains more crucial than ever.

Introduction

On January 31st, 2023, we released Aave: A Review Of The Fundamentals, offering updated insights on the themes covered here.

For both the seasoned and amateur DeFi user alike, Aave is a protocol that needs no introduction. The non-custodial money market is one of the oldest DeFi protocols around and yet it has constantly been at the forefront of innovation. From pioneering flash loans to rate switching under Aave v2 and, more recently, the plethora of upgrades proposed under Aave v3, which we will explore throughout this post. But first, let’s take a moment to appreciate how far Aave has come before we discuss where it’s headed.

Aave is currently the fourth largest DeFi protocol with ~$15bn in TVL, equating to more than a 6 fold increase since the beginning of 2021. This growth is due, in no small part, to their cross-chain expansion efforts on Avalanche and Polygon, where it has cemented itself as the leading money market on both chains. The team will soon deploy on Arbitrum while also setting their sights on Boba, Optimism and Starkware. With the imminent launch of Aave v3, it wouldn’t be surprising to see them launch on a few other chains either to continue amassing liquidity. This brings us to the first key feature of Aave v3 – Portals.

Key Features of Aave v3

Portals

The first iteration of Portals is a non-user facing piece of liquidity infrastructure. It offers whitelisted bridge protocols like Connext, Hop Protocol and Synapse access to credit lines which can be used to facilitate cross-chain transactions. Importantly, this credit line will only be tapped when there is insufficient native liquidity to support the moves.

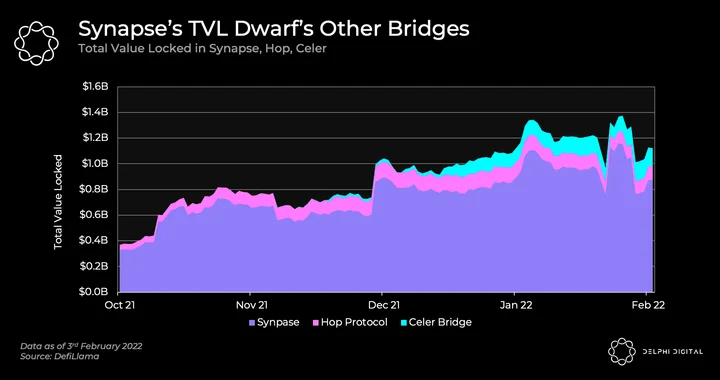

Before we dive deeper into what that means, we first need to be aware that liquidity, a vital component for a bridging protocol’s success, is often subsidized via incentives. The impact of a liquidity mining program is clearly evident in the chart below when looking at how much market share Synapse has attained relative to the field. While the superior UX of Synapse has also played a role we should note that this is partly a result of its centralized nature at the moment, although efforts are already being made to decentralize its operations.

With the advantages of liquidity mining in mind, it should make sense that whitelisted bridge protocols without a token stand to benefit greatly from the launch of Portals. They’ll now have access to just-in-time liquidity without having to rely on subsidizing LPs with token emissions. It’s also a win-win situation for Aave v3 depositors given the improved capital efficiency of having yet another source of revenue added.

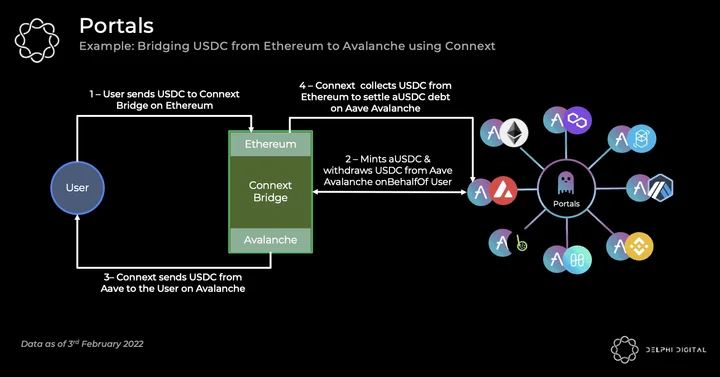

Below, we’ve provided a sample scenario for how this will work. Consider a user who wants to bridge USDC from Ethereum to Avalanche via the Connext bridge. If Connext doesn’t have enough liquidity to fulfill the transaction on Avalanche, it will tap into Aave’s liquidity on Avalanche by minting unbacked aUSDC onBehalfOf the user and withdrawing USDC from Aave on Avalanche. Subsequently, Connext will periodically collect the USDC from Ethereum to settle the debt incurred from minting unbacked aUSDC on Avalanche. The following diagram illustrates how the process works.

In the event that liquidity becomes scarce on Avalanche, Aave’s interest rate computation module will move interest rates up on Avalanche to ensure people are incentivized to deposit. Since Portals is not a trustless feature (yet), Aave’s governance is also expected to introduce a credit limit cap, and only reputable protocols will be whitelisted to avoid introducing too much risk into the system.

If risks are properly managed, Portals is most definitely a net positive for Aave, liquidity providers and bridge protocols. A new business model should arise from this development, as bridge protocols provide the infrastructure while Aave v3 provides the liquidity that is needed to power that infrastructure instead of having to perpetually subsidize liquidity with token emissions.

Here’s a dank meme highlighting the difference between the two different liquidity sourcing models.

As the multi-chain narrative takes shape in 2022, Aave is well positioned to expand its total addressable market to bridging protocols like Synapse, Hop Protocol, etc., in a addition to users of its flash loan product. In terms of monetization, two different fee models are currently under discussion in Aave’s governance forum. You can check the thread out here to stay up to date with the discussion.

We will now move on to talk about two major improvements coming to Aave’s lending markets – high-efficiency mode and isolation mode.

High-Efficiency Mode

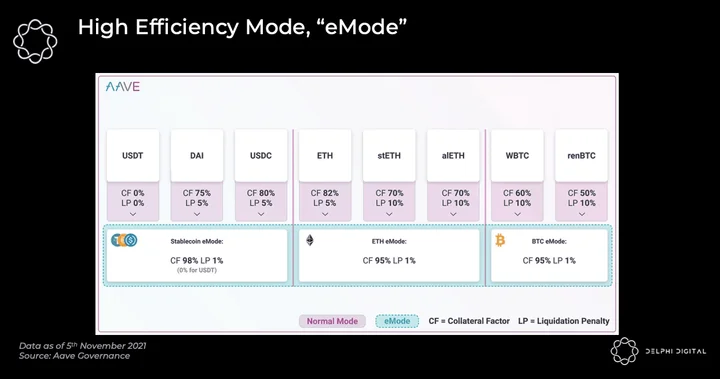

With high-efficiency mode or “eMode”, borrowers can enjoy a higher LTV on their collateral deposits on the condition that both the deposited and borrowed assets fall under the same category. According to Aave, -” A “category” typically refers to a set of assets pegged to the same underlying asset—for example, stablecoins pegged to USD, assets pegged to ETH, etc.”

Higher borrowing power is made possible due to the high correlation between pegged assets compared to unpegged assets. This reduces the likelihood of default/liquidation since both the collateral and borrowed assets would move in tandem. Hence the protocol can afford to give borrowers a higher LTV without incurring significant risk.

We foresee Aave’s high-efficiency mode driving new capital inflows to Aave as users can make use of capital more efficiently. For instance, they may deposit USDC and borrow USDT to take advantage of USDT denominated farms without going through the hassle of swapping it, which incurs trading fees or slippage. Moreover, an LTV of 95% is unmatched by other money market protocols.

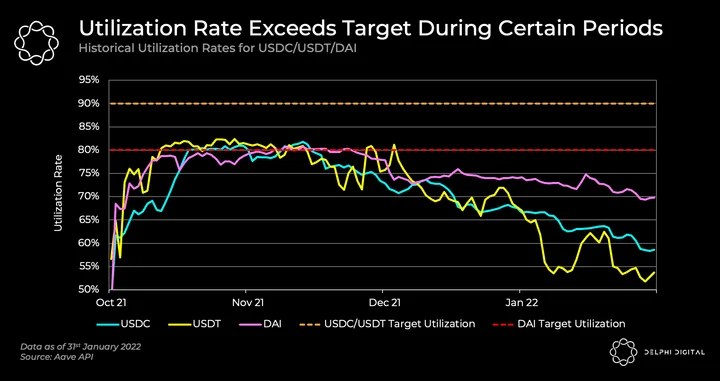

There have been certain time periods where stablecoin utilization rates have come very close to their optimal utilization rates. During the 21 Oct to 20 Nov window last year for instance, utilization rates for USDC, DAI and USDT were at an average of 79-80%, whereas the target utilizations were 90%/80%/90% respectively. Optimal utilization rates are set to mitigate liquidity risk, ensuring there is enough unused capital for depositors to withdraw their funds at any point of time. eMode may thus have a muted effect during certain periods as borrowers are turned away from higher interest rates when utilization exceeds the optimal percentage. Furthermore, as we will see in the next section, isolation mode would put further pressure on stablecoin utilization rates since they are the only assets that borrow against isolated collateral. It seems necessary that Aave increase stablecoin deposits or increase optimal utilization rates in order to cater to this new demand.

Isolation Mode

Cross-collateral money markets are only as safe as their most risky token. As such, protocols have to choose between security or collateral diversification. More conservative lenders like Compound Finance have opted for the former, listing only up to DeFi blue chips. On the other end of the spectrum lies Cream Finance, which has a history of rather liberal collateral listing, as evidenced by a slew of long tail assets and LP tokens on its now-decommissioned Ethereum money market.

This hasn’t played out so well for Cream. Its notoriety for lax listing requirements has made it a key target for exploits. Over the last 12 months, Cream has been hacked 3 times, with 2 out of 3 times attributable to long tail risky assets used as collateral. The most recent exploit involved manipulating the price of a wrapped token, yUSDvault. Interestingly, Cream’s $130m exploit uncovered a potential vulnerability in Aave as well, and the Aave community quickly voted to delist a number of assets as a precaution. Since then, the Cream team has definitively tightened their token listing strategy.

With the latest Cream hack still fresh in memory, we move on to Aave’s next innovation – “isolation mode”. Perhaps as a result of October’s fiasco, Aave introduced isolation mode, allowing users to deposit isolated assets as collateral up to a certain debt threshold.

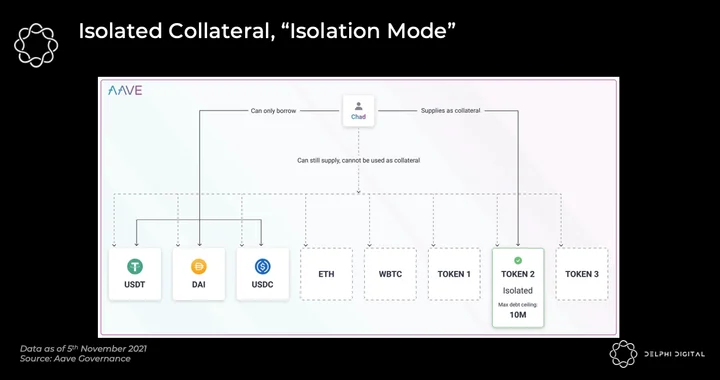

This is how it works: First, someone has to put forth a governance proposal to list an asset as “isolated collateral”. If the vote passes, the asset can be used to borrow certain stablecoins that governance has permissioned to be borrowed, only up to a specified debt ceiling. Once an asset classified as “isolated collateral” is used as collateral, other assets may not be used as collateral.

In the example above, Chad will only be able to borrow USDT, DAI, USDC using Token 2 as collateral. He is not allowed to use his ETH, WBTC, Token 1 or Token 2 as collateral unless he first disables Token 2 as collateral. However, his other deposits will still earn an APY even though they are not used as collateral.

Isolated assets are typically long tail assets that are deemed too risky to be used on a cross-collateral money market. Allowing them to be used as collateral on Aave will contribute to TVL growth, while enforcing a debt ceiling on these risky assets puts a ceiling on the amount of capital at risk. However, since isolation mode forbids the user from using any other asset as collateral, they may experience substantial friction if they have to switch wallets to deposit other tokens. One solution would be to introduce many sub-accounts, similar to Euler finance’s implementation. Users can then toggle between different borrow positions within the same wallet while keeping risk isolated within the sub-account.

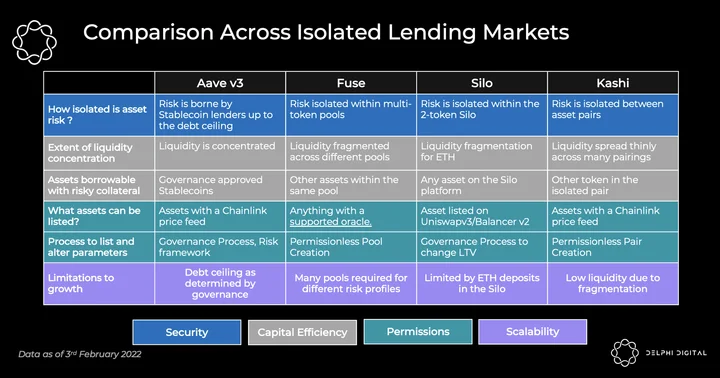

Aave v3’s Isolation Mode isn’t DeFi’s first attempt to alleviate the security risks associated with using risky assets as collateral. Rari Capital, Silo Finance, and Sushi have also ventured into the space with differentiated products. In the next section, we explore their mechanisms and evaluate each solution across key criteria desirable in a money market.

Rari’s Fuse

We wrote about Rari’s Fuse pools last year. For the uninitiated, Fuse allows users to create isolated lending pools with assets of their choice in a permissionless and customizable manner. Pool creators can choose to set parameters such as interest rate curves, oracles, collateral factors like LTV etc. as they please. Each pool is a fork of the compound protocol, meaning that it is its own cross-collateral money market, isolated from another.

The deployment of Fuse has created liquid lending markets for long tail assets, and enabled DAOs like Index Coop and Badger to earn a yield on their otherwise idle treasury. Since going live in March 2021, Fuse has amassed over $600m in total value locked on Ethereum, with over 100 unique lending pools.

However, the merits of customizability also come with its drawbacks. Given that each fuse pool is as safe as the riskiest asset in the pool, an infinite number of pools would be needed to match the varied risk profile of a large user base. This results in liquidity fragmentation as the same assets (e.g. stablecoins) are split across many pools.

Furthermore, giving creators the autonomy to change pool parameters unilaterally introduces a single point of failure. They may also add assets with little liquidity, making the pool vulnerable to price manipulation. Recent exploits of the Float Protocol and Vesper fuse pools are both testament to these risks. Although the isolated pool design succeeded in keeping collateral damage within the exploited pool, we note that the top 2 pools make up over 50% of Fuse’s TVL, with the 5 largest responsible for over 80%, indicating a high concentration of risk.

Sushi’s Kashi

Rari uses isolated lending pools with no cap to the number of assets within each pool. Kashi, on the other hand, uses isolated lending pairs. Between each pair, one side is used as collateral and the other side is lent out. This also means that there are 2 pools for every unique pair of assets, one for when the asset is used as collateral and the other for when the same asset is lent out. With Kashi, anyone can list a token pair as long as there is a chain link price oracle for the asset.

While idiosyncratic asset risk is more insulated than Fuse, Kashi also experiences much more fragmentation as liquidity is spread thinly across many different niche markets. Since liquidity mining incentives for Kashi ended, usage has declined significantly, and TVL stands at less than $20m.

Silo Finance

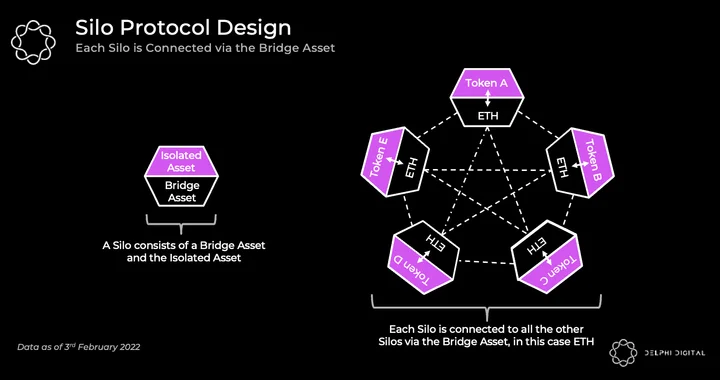

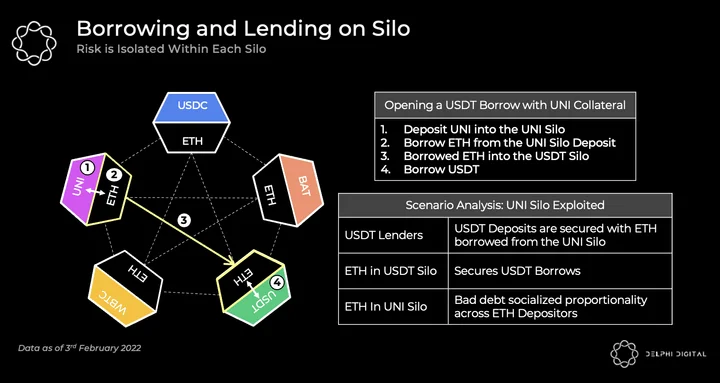

Another project worth highlighting given its unique twist on isolated pairs is Silo finance, the new kid on the block(chain). As its name suggests, the protocol makes use of silos, each of which is an isolated money market. A silo supports 2 types of assets, a bridge asset (we will be using ETH as the bridge asset for simplicity) and another unique token. The bridge asset facilitates lending and borrowing by connecting all silos in the protocol. With the isolated pair design, asset risk is isolated with the specific Silo and insulated from the others, and every borrow is secured by the bridge asset.

Let’s illustrate this with an example. Consider a situation where a user would like to borrow USDT against her UNI collateral. She first has to borrow ETH from the UNI-ETH Silo, then deposit the borrowed ETH into the USDT-ETH silo to borrow USDT. The asset securing her USDT loan is now ETH and not UNI, so USDT lenders are protected from the risk of UNI going bad – in other words, the “new collateral” used to borrow USDT is ETH, not UNI. The burden of bad collateral thus falls on ETH depositors in the UNI silo.

The user effectively has 2 borrow positions open:

- Borrow Position #1: Deposit UNI > Borrow ETH

- Borrow Position #2: Deposit ETH from #1 > Borrow USDT

By extension, for any asset to be used as collateral, users have to deposit ETH into that particular Silo. This means that scalability is reliant on users depositing ETH into a market they trust. Another implication is that ETH liquidity is fragmented over many Silos since it is required as part of the protocol design. For the most part, Silo’s design seems rather sleek, with liquidity concentration for the (non-bridge) assets and risk isolated within a silo.

Earlier this week, Silo came up with a proposal to introduce a stablecoin backed by other stablecoins as a bridge asset – more details here. This would be a welcome addition as users can now borrow a stable asset with little to no fluctuations in is price. The addition of a silo stablecoin makes each Silo a 3-asset pool, consisting of 1 unique non-bridge asset per Silo with 2 bridge assets.

According to the discord, Silo is predicted to launch its public beta in the middle of February once audits are done. It will be interesting to see how the protocol plans to attract ETH depositors to Silos with long tail assets, and how seamless the UX will be given that most borrowers will have 2 borrow positions open at each time.

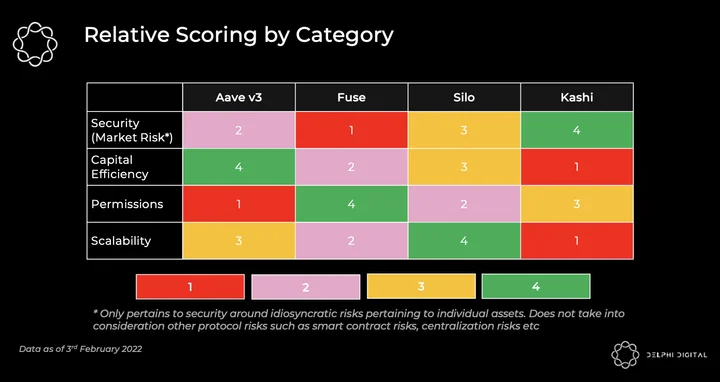

Scoring

Now that we’ve run through each of the solutions and their unique attributes, let’s go back to our money market criteria. We assess the money markets by each category, asking ourselves the following questions to assess each protocol’s strengths and weaknesses for that particular attribute:

- Security*: How isolated is the asset-specific risk?

- Capital Efficiency: To what extent is liquidity concentrated/fragmented? What assets can be borrowed?

- Permissions: What assets can be listed? How permissionless is it to list assets and change lending and borrowing parameters?

- Scalability: Are there features in the design that limit growth in lending and borrowing?

*Note: Security here only pertains to market risk and does not take into consideration other risks like smart contract or counter-party risk.

In the table below, we have ranked the solutions factors relative to each other. A score of 4 represents the best option in its respective category, while a score of 1 represents the worst option.

Readers should take this scoring with a pinch of salt as half of the solutions listed above have not been tried and tested, and thus lack nuance and context. However, we hope these generalized findings are helpful for those with higher preferences in certain categories when choosing a money market to use.

Aave v3 is a welcome improvement as it gives more flexibility and use cases to a traditional money market. More than that, the shift to an infrastructure play captures the current zeitgeist where DeFi tokens have fallen out of favor, and attention has turned to alternative layer 1s and cross-chain interoperability narrative. Other than Aave, Compound has recently announced plans to build out a presence to other chains, with the intention of building out a “multi-chain shared liquidity pools” protocol, and we could see other money markets move in the same direction. The ability to innovate and integrate faster than competitors is thus crucial for Aave. We await to see how they will leverage their competitive edge in an increasingly competitive space.

0 Comments