An Update on Crypto Market Structure: Leverage and Volatility

AUG 16, 2021 • 4 Min Read

Report Summary

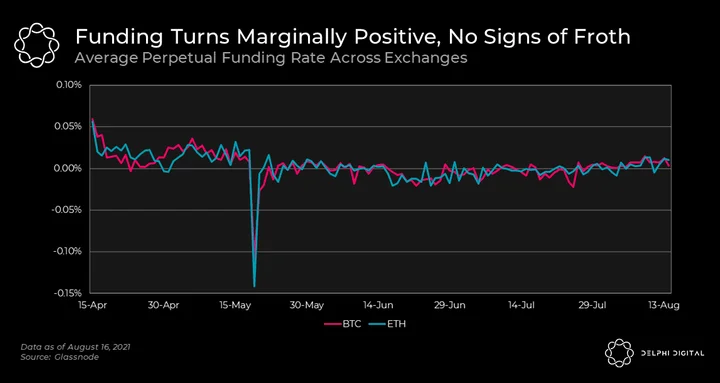

Another sign the market isn’t being propped up by leverage comes from funding data. When funding is positive, it means the perp is trading higher than the spot index for said asset. When funding is negative, the perp is trading at a discount to the spot index. Positive funding implies more buyers than sellers, and negative funding implies the opposite.

In Apr. and May. 2021, we saw funding rates hit insane levels — as high as 0.10% per 8 hours for sustained periods of time. BTC and ETH price were moving vertically; everyone and their mother wanted more exposure to crypto. We all know what happened next. Leveraged buyers tapped out and the market cascaded downwards, fueled by heavy liquidations.

Funding data for the last month paints a bullish picture, as it shows us during this entire rally, funding never really hit exuberant levels. In fact, the funding trend just marginally flipped positive in recent days.

Simply put, current funding data shows us traders have been in no rush to get long BTC, and that frothy conditions are still a way off.

Market Update

The market found strength on the Asia open today, but the European and North American sessions saw sellers take control and push almost everything lower. BTC fell by nearly 2% as the North American session opened today. It was a buzzing weekend though; coins like SOL, YGG, and LUNA hit fresh all-time highs, and DeFi tokens enjoying a bounce too.

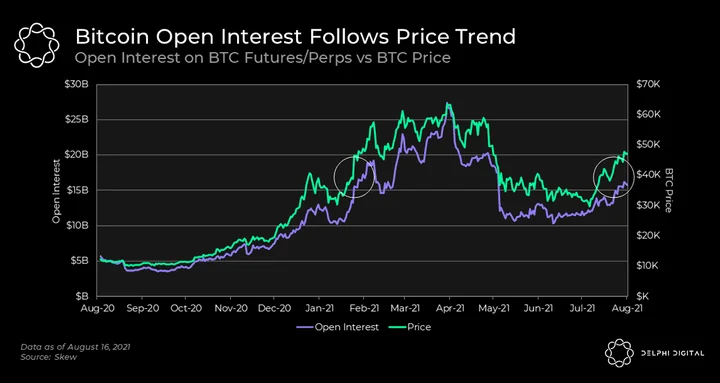

Open Interest Tracks Price, Leverage Proxy

- A pattern you see with crypto markets that differs from other markets is how open interest tracks price. For the most part, this is because the vast majority of BTC open interest accounts for traders who are trying to increase their long exposure and delta-neutral players taking advantage of basis/funding.

- While not perfect, we can use open interest as a rough proxy for the amount of leverage in the market. During this rally we’re seeing a welcome development — price is moving at a faster pace than open interest, implying some degree of doubt from futures/perp traders that this rally is real. Or in crypto terms — a lack of FOMO.

- If BTC continues to rally, it seems reasonable to expect an influx of leveraged capital, perhaps on a clean break of $50K or even as late as ATHs (if it happens this cycle).

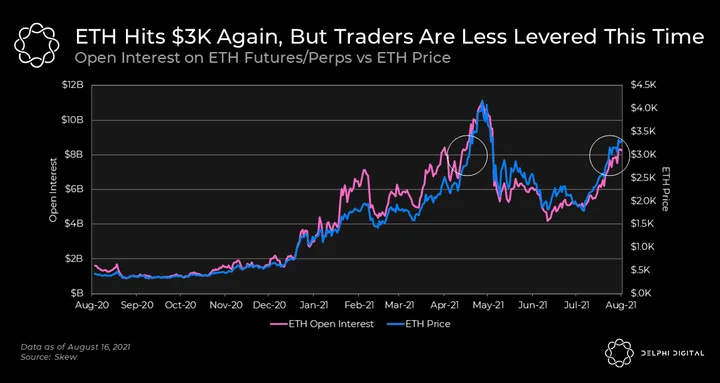

- ETH’s structure looks fairly similar to BTC’s, but the difference between price and open interest growth is a little wider. ETH closed yesterday at $3310 per coin with $8.25 bn in open interest. The first time ETH hit $3300, in May 2021, open interest was just over $10 bn, and trading volume was much, much higher.

- In general, lower leverage implies a healthier market with less fuel for liquidations and stop hunts.

More Signs of Low Leverage

- Another sign the market isn’t being propped up by leverage comes from funding data. When funding is positive, it means the perp is trading higher than the spot index for said asset. When funding is negative, the perp is trading at a discount to the spot index. Positive funding implies more buyers than sellers, and negative funding implies the opposite.

- In Apr. and May. 2021, we saw funding rates hit insane levels — as high as 0.10% per 8 hours for sustained periods of time. BTC and ETH price were moving vertically; everyone and their mother wanted more exposure to crypto. We all know what happened next. Leveraged buyers tapped out and the market cascaded downwards, fueled by heavy liquidations.

- Funding data for the last month paints a bullish picture, as it shows us during this entire rally, funding never really hit exuberant levels. In fact, the funding trend just marginally flipped positive in recent days.

- Simply put, current funding data shows us traders have been in no rush to get long BTC, and that frothy conditions are still a way off.

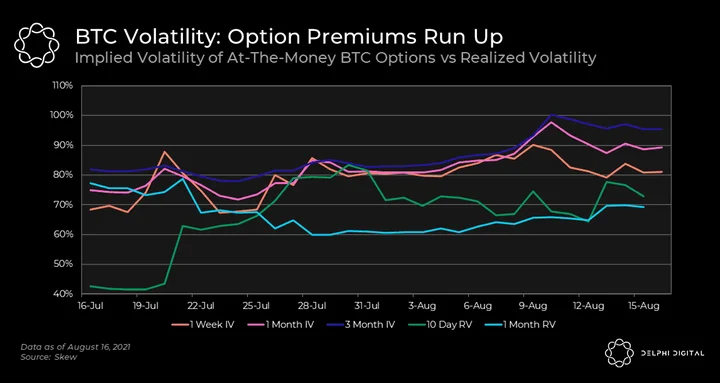

What the Options Market is Saying

- In mid-July, BTC started to trend upwards after a few months of a downtrend and consolidation. This pushed short-term volatility (10 day realized vol) higher, and the options market reflected that data in its pricing of options (IV for 1 week options rose too).

- Term structure for BTC options has widened in recent days. A rise in further dated option IVs (1 month, 3 month) was driven by large call purchases earlier this month. Implied vols have cooled off in recent days, with one-week option IVs falling the furthest. If BTC rallies into the end of August, we could see another burst of short-term call purchases, pushing IV up again. But given relatively higher IVs compared to a few weeks ago, this could also be a sign of a near-term pullback.

- TLDR: option premiums increased as people bought calls to speculate on the upside, but implied vols increasing significantly could signal the market’s expectation of near-term pullback.

Notable Tweets

Perpetual Protocol announces a grant program with $7.5 mn of incentives.

⚡ Summoning Developers and Content Creators!⚡

We’re excited to unveil the launch of the Grants Program!

With a fund of ~$7.5M, the Grants Committee will support projects that drive the adoption of the protocol.

Three projects are funded so far?https://t.co/ehX7BzZT0Z

— Perpetual Protocol | We’re hiring! (@perpprotocol) August 16, 2021

Vitalik on the dangers of coin voting.

Decentralized governance is necessary, but coin voting governance in its current form has many acknowledged and unacknowledged dangers. Augmenting or moving beyond coin voting is a key part of the solution:https://t.co/pZQ4sLAbEy

— vitalik.eth (@VitalikButerin) August 16, 2021

An insight that’s applicable to crypto markets, were liquidity is created early and growth potential is massive.

It’s hard to hold onto a stock that gets expensive when you bought it because it was cheap. Let your thesis evolve with the progress of the business. You can’t keep looking back at your cost basis or you’ll sell.

— Ian Cassel (@iancassel) August 15, 2021

0 Comments