Report Summary

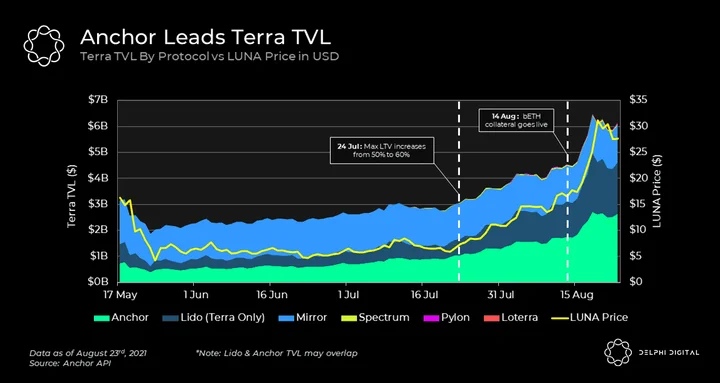

LUNA hit its all time high price today ($34.25), simultaneously lifting Terra’s TVL upward along with it. Terra is now the 3rd largest L1 according to this metric, behind Ethereum & BSC. Within the Terra ecosystem, Anchor is the largest application by TVL, with current levels at ~$2.7b.

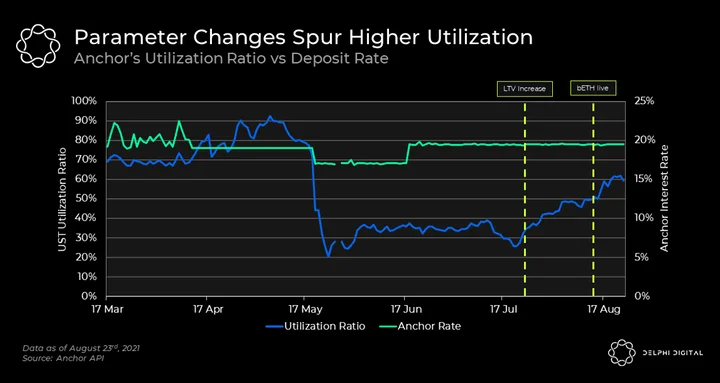

After the market crash in May, Anchor’s UST utilization ratio cut in half as borrowers deleveraged, reducing the total amount of interest borrowers had been paying into Anchor. This, coupled with a disproportionately high amount of UST deposits to support, forced Anchor to eat into its Yield Reserve to maintain the stable rate of 20% offered to lenders.

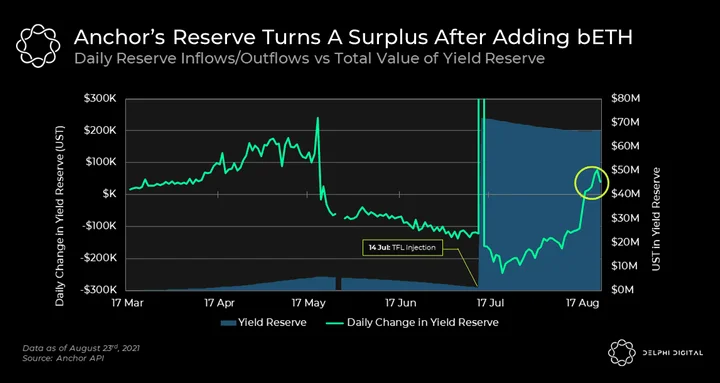

The Yield Reserve was running a deficit after the event and went as low as $1.2m on July 13th. Terraform Labs (“TFL”) intervened and boosted the yield reserve with a capital injection of $70m UST.

The reserve deficit continued until the recent introduction of bETH as collateral which reversed the trend. This is partly because the addition of bETH led to an uptick in the UST utilization ratio, with current levels at ~60%. For context, the low reached in May was ~20%.

The beneficial impact that bETH had on Anchor hints that the future additions of bATOM, bSOL and bDOT should be positive catalysts for the protocol. Any increase to the amount of bAssets posted as collateral, or their PoS yield, directly benefits ANC because 10% of the generated yield is used to buyback the token.

Layer 1 tokens have been in the spotlight lately, with AVAX on a tear while LUNA and SOL hit all time highs. As seen in the chart below, LUNA’s price appreciation has helped propel Terra’s TVL higher, making it the 3rd largest blockchain by this metric after Ethereum and Binance Smart Chain. Among all the protocols live on Terra, Anchor Protocol accounts for the majority of TVL. In this report, we’ll explore Anchor’s growth drivers and underlying mechanics to see what the future holds in store for the protocol.

For the uninitiated, Anchor Protocol is a money market on Terra that specializes in letting people borrow against staked L1 assets. To accomplish this, borrowers first deposit liquid staking derivatives, referred to as bAssets in Anchor, as collateral before they can borrow UST. The UST supply on Anchor is deposited by lenders that want to earn Anchor’s unique stable interest rate of ~20% (it slightly fluctuates around this target rate). The staking yield generated by the bAssets and the interest charged to borrowers is used to pay this stable rate to lenders.

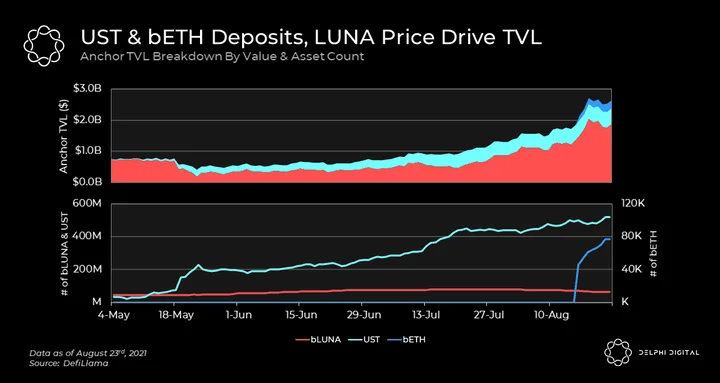

In the chart above, we’ve broken out Anchor’s TVL by asset – bLUNA, UST and bETH. Each has a different story for how it is impacting TVL.

The largest driver of TVL has been bLUNA, although this hasn’t been due to new bLUNA inflows, as illustrated by the flat red line above. Rather, TVL has been lifted by bLUNA’s price appreciation.

UST deposits have gradually risen over the past few months since the sharp upswing in May. That spike was likely the result of either 1) borrowers paying down debt to avoid liquidation or 2) lenders seeking a flight to stability / yield in the midst of the market crash. Regarding that last point, as yields on Ethereum money markets were dropping, Anchor offered a relatively high yield on a stablecoin deposit (UST at ~20%).

bETH is the newcomer to the party, having just been added on August 13. We’ll discuss the positive impact it’s had throughout this post.

TVL alone, however, paints an incomplete picture of Anchor’s health and sustainability. While TVL has been growing over the last few months, the Anchor yield reserve has been running a deficit. After the May market crash, Anchor’s UST utilization ratio essentially cut in half. This decrease can be attributed to borrowers deleveraging their positions.

The utilization ratio is particularly important because the less borrowing that occurs, the less interest that is being generated to pay Anchor’s stable rate of ~20% to lenders. This, coupled with a disproportionately high amount of UST deposits to support, forced Anchor to eat into its Yield Reserve to maintain the stable rate.

The Yield Reserve went as low as $1.2m on July 13th and would have been drained completely in roughly 10 days had Terraform Labs (“TFL”) not intervened. TFL boosted the yield reserve with a capital injection of $70m UST. Since then, the reserve continued to run a deficit until the recent introduction of bETH which reversed the trend. This is partly because the addition of bETH led to an uptick in the UST utilization ratio, with current levels at ~60%. For context, the low reached in May was ~20%.

There are plans to improve Anchor’s capital efficiency by putting idle assets to work which should generate revenue for the protocol, helping reduce the strain on the Yield Reserve. Currently, ~40% of UST deposits sit un-utilized, serving only to drain Anchor’s reserve. Upcoming protocols such as Angel, Orion, and Suberra rely on Anchor’s rate and will likely further skew the supply on deposit, adding stress to the Yield Reserve, albeit more utility to UST as well. A positive counterbalance to this, if the success of bETH is any indicator, will be the future addition of more PoS staking derivatives (bATOM, bSOL, and bDOT) as collateral assets on Anchor.

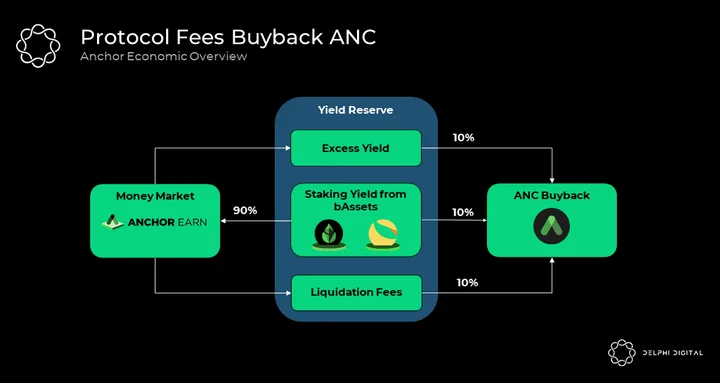

As seen in the diagram above, Anchor has several different levers at play which pay interest to UST depositors, grow the Yield Reserve, and accrue value to ANC. To start, the protocol takes 10% of the staking yield, generated by the bAssets posted as collateral, and uses it to buyback ANC on an ongoing basis, regardless of whether net interest income (after paying depositors) is positive or negative. The remaining 90% is used to pay the Anchor savings rate on UST deposits.

Let’s say, hypothetically, that bAssets are generating so much yield that Anchor could actually pay a 25% rate to UST depositors, even though it only has to pay 20%. That net difference of 5%, or “excess yield”, is sent to the Yield Reserve, of which 10% is then used to buyback ANC as well. Furthermore, the protocol also collects “Liquidation Fees” equivalent to 1% of the liquidated collateral’s value. The Liquidation Fees are sent to the Yield Reserve, where 10% of the fees are also used to buyback ANC.

In summary, any increase to the amount of bAssets posted as collateral or their PoS yield directly benefits ANC, sometimes at the expense of the Yield Reserve. The value accrual mechanics favors holders in the short-term, as there is continuous ANC buy pressure independent of the reserve’s health. Importantly, however, if TFL didn’t step in with a capital injection to bolster the Yield Reserve when it was nearly depleted, ANC could have been adversely affected, although this is all conjecture.

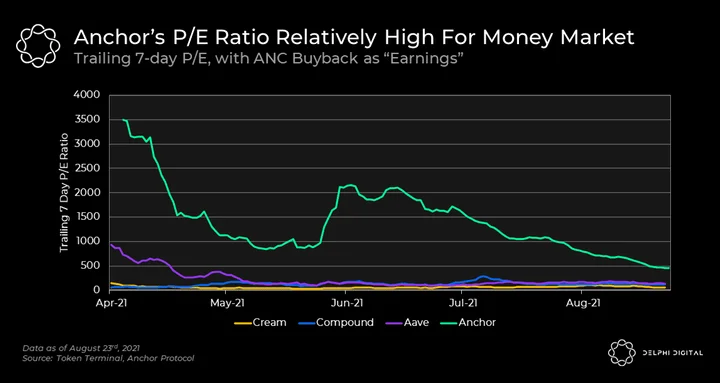

We calculated a price to earnings ratio using ANC buybacks as the denominator. The Trailing 7 day P/E is at ~520x on an annualized basis, which is significantly higher than the major money markets on Ethereum. However, this premium is not unusual for young projects in early stages of growth and development.

We think a number of catalysts may propel Anchor’s growth trajectory including:

- The addition of new bAssets including bATOM, bSOL and bDOT

- New protocols launching on Terra (Mars, etc.) which may create new opportunities to deploy Anchor’s idle capital

- Increased utility of UST cross-chain

Something important to note is that borrowing is currently incentivized by ANC emissions, meaning that borrowers are being paid to lever up. It remains to be seen whether Anchor can sustain this once incentives taper off, although the same point could be raised about every project using its supply to bootstrap adoption. As new collateral types are accepted and UST’s utility continues to grow, we believe Anchor’s value proposition will strengthen over time.

0 Comments