Arbitrum vs Optimism, Liquidation Cascades, Lido's stETH Depeg

JUN 27, 2022 • 7 Min Read

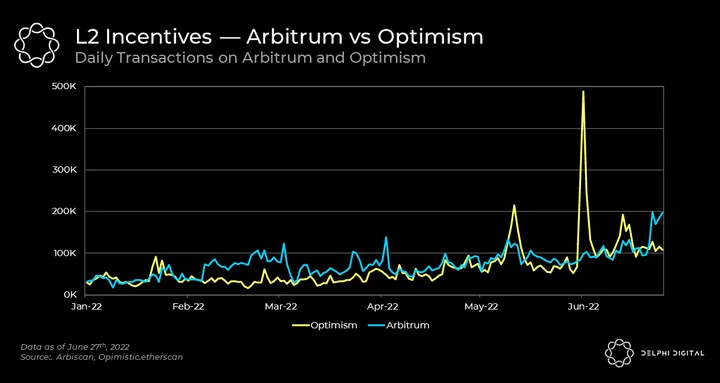

Chart of The Day: Arbitrum vs Optimism

![]()

- Arbitrum and Optimism are the two leading Optimistic rollups for Ethereum.

- Optimism initiated incentives with the $OP airdrop, which attracted users to claim their tokens. However, its daily transactions, which were ~500k during the claim period, have tapered off to around 100k daily transactions. Check if you are eligible for the $OP airdrop here. This is not the end of $OP incentives, as only 5% of supply was airdropped, with 14% more allocated to future rounds.

- As covered in our previous daily, Arbitrum has just started its 8-week event, Arbitrum Odyssey, to attract users to protocols on Arbitrum. Accumulating 13/16 of the Arbitrum Odyssey NFTs will make you eligible for a bonus NFT at the end of the event. This week, users will need to complete tasks using Yield Protocol and GMX to be eligible for week 2’s NFTs. Keep a lookout on Arbitrum’s Twitter for the eligibility criteria.

- The start of Arbitrum Odyssey pushed Arbitrum ahead of Optimism in daily transactions, but the fight is not over as both L2s continue to incentivize users.

- For more on L2s, Delphi members can read our Delphi Pro report on ZK Rollups here!

Bear Market Woes: When Is Enough, Enough?

[Excerpt from a Delphi Insights Report]

- The above chart examines the liquidation cascade from May 2022 and highlights key characteristics of post-liquidation mechanics. We can attempt to apply these principles to the current market situation we are in.

- Note the significant bounce in price on relatively insignificant volume (a result of the liquidation cascade clearing out the order book); the price is finally being bid up once again. In the immediate aftermath of a liquidation event, the order book is ‘essentially’ empty, as the sell pressure from forced liquidations has finally started to subside. The thin nature of the order book allows prices to ‘slip up’ more easily.

- The white box shows the area where buyers attempted one last stand before the final capitulation leg of the cascading downward move. From a pure market structure perspective, this is a very logical area for mean reversion traders from the lows (trying to take advantage of the thin order book dynamic that was just discussed) to take profit initially. Notice how the price was unable to move beyond this area in any significant way.

- Utilized correctly, this framing of the market can be quite helpful in the conditions that we find ourselves in. These market events are often times fantastic mechanical/scalp trading opportunities. The above chart shows the anatomy of the liquidation cascade from May 2022. Using this as a blueprint, it is possible to come up with a game plan for how to deal with the aftermath of future situations.

- For more information, Delphi members can see the full Market Insights here.

The Root of Lido’s stETH Peg Troubles

[Excerpt from a Delphi Pro Report]

- Before we go further, it’s important to note that stETH issued is backed by an equivalent amount of ETH. When withdrawals are enabled, holders will be able to redeem at a 1:1 rate. Once this happens, stETH should realistically keep its peg at 1:1. Every time it deviates, a fairly obvious arbitrage opportunity will present itself.

-

If stETH is trading >1 ETH, users can deposit ETH into Lido and receive stETH in return, selling the stETH into the open market and capturing the spread.

-

If stETH is trading <1 ETH, users can purchase discounted stETH and then redeem it for ETH, selling the ETH into the open market and capturing the spread.

-

- In the meantime, since withdrawals are not enabled yet, stETH maintains its peg to ETH through a Curve StableSwap pool. Recently this StableSwap pool has become imbalanced and stETH is trading at a ~5% discount to ETH. This post will cover how the discount has come to be in the hope of clarifying the situation.

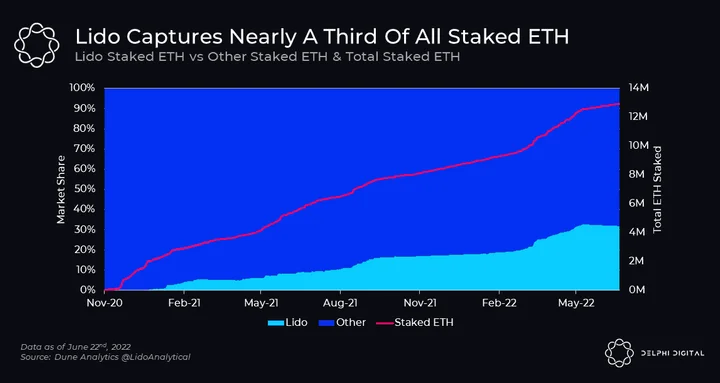

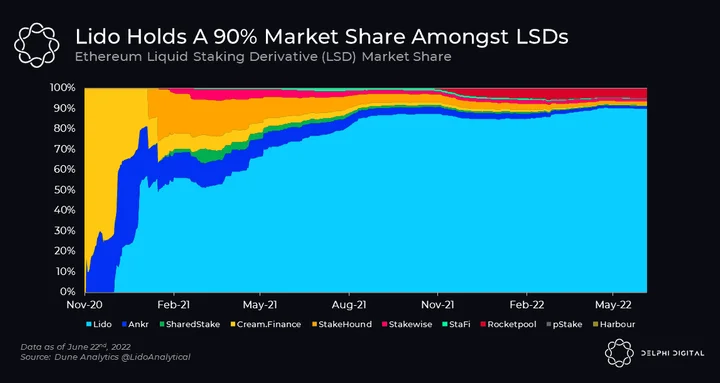

- Firstly, before we jump into the discount, it is important to understand the magnitude of Lido and stETH in regards to Ethereum staking.

- Not only does Lido hold 32% of all staked ETH (~3.3% of the total ETH supply), it’s also the largest liquid staking derivative with ~90% market share. These liquidity and network effects are extremely strong across Ethereum and have allowed stETH to be integrated into both Aave and Maker as a form of collateral. These integrations serve as a massive schelling point for stETH as it slowly becomes interchangeable for ETH within DeFi. At the same time, it carries an underlying yield — currently 4.07%. Aave and Maker have attracted over 1.3M and 0.2M stETH deposits respectively, cumulatively representing over 35% of all stETH in circulation.

- Given stETH’s dominant market position within ETH staking, what has caused its peg to break?

- As we mentioned earlier, stETH is currently not redeemable for ETH yet; it has been keeping its peg through the stETH-ETH StableSwap pool on Curve. At the time of writing our last report on Lido and stETH, the stETH-ETH Curve pool was massive, holding $3.3B of assets with a nearly 50/50 ratio of stETH/ETH. Currently, the Curve pool sits at ~$660M and weights 80/20 in favor of stETH, pricing it at a ~5% discount to ETH.

- So what has led to such a drastic imbalance and what are the implications of this?

- Two large crypto players who have recently been struggling with solvency issues, Celsius and Three Arrows Capital, had significant stETH exposure. Given their problems, they were forced to unwind a large part of their position (hundreds of thousands of stETH), putting significant pressure on the stETH/ETH peg. This de-pegging alongside a larger market sell-off caused participants that were borrowing against their stETH on Aave to begin repaying their loans. In short, the need for immediate liquidity — something stETH cannot offer natively yet — is at the heart of the de-peg.

- Aave added stETH as collateral in Feb. 2022 with an LTV of 73% (vs ETH at 82.5%). The inclusion of stETH on Aave allowed for users to lever their staking yields. Let’s run through how they would do this:

-

-

Deposit stETH on Aave

-

Take an ETH loan

-

Use the loaned ETH to purchase stETH on Curve or convert it to stETH on Lido.

-

Re-deposit the stETH on Aave. (You can continue this cycle depending on your risk tolerance.)

-

- With ETH borrowing rates at ~1.5-2% and stETH yielding ~4%, there is net a +2-2.5% yield on leveraged staking positions. Fear over these positions being liquidated caused many people in the trade to unwind their leverage.

- For more information, Delphi members can see the full Delphi Pro Report here.

Notable Tweets

Harmony Bridge Compromised

1/ The Harmony team has identified a theft occurring this morning on the Horizon bridge amounting to approx. $100MM. We have begun working with national authorities and forensic specialists to identify the culprit and retrieve the stolen funds.

More 🧵

— Harmony 💙 (@harmonyprotocol) June 24, 2022

Lido Votes Against Self-limit

the loudest people for lido to self-limit were, and has always been, non-tokenholders (and bagholders of competing projects) whose opinions do not matter on this subject

https://snapshot.org/#/lido-snapshot.eth/proposal/0x10abedcc563b66b1adee60825e78c387105110fa4a1e7354ab57bc9cc1e675c2

— 찌 G 跻 じ Goblin 𝙎𝙚𝙣𝙥𝙖𝙞 of the 𝙃𝙚𝙣𝙩𝙖𝙞 (@DegenSpartan) June 25, 2022

ETH’s 2nd Testnet Merge on July 6th

– Sepolia Merge is scheduled for ~July 6th. TTD will be shared on Monday and clients should have releases with it announced by EONW.

— Tim Beiko | timbeiko.eth 🐼 (@TimBeiko) June 25, 2022

0 Comments