Report Summary

Aurora is the EVM implemented as a smart contract on Near.

Rainbow Bridge is trustless and was built by the Near/Aurora teams.

The May 1st attack on the bridge was successfully thwarted, proving optimistic assumptions in practice.

TVL has hit >$1B, money markets Bastion and Aurigami have kickstarted ecosystem.

Usage is heavily incentivized through Aurora Labs covering gas fees and new DeFi protocol tokens.

Composability with Near native applications starting to be integrated, made possible by cross contract calls.

AURORA token is purely used as an incentive mechanism at this point, subsidizing the DAO’s validator and upcoming governance staking for ecosystem grants.

What is Aurora?

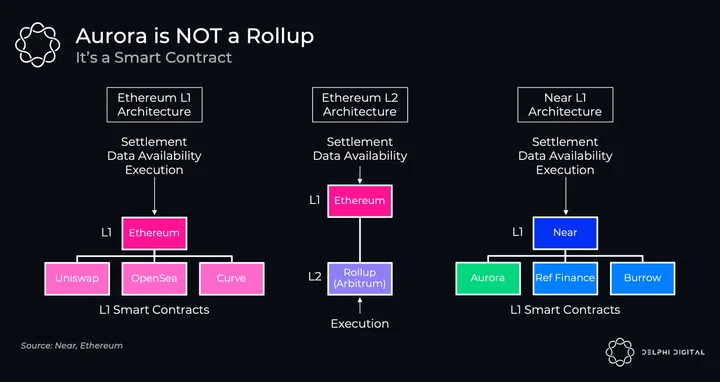

Aurora is the EVM (Ethereum Virtual Machine) implemented as a smart contract on Near. An important distinction here is that it is a smart contract on an L1, not a rollup posting to an L1. Before diving further we should have a high-level understanding of Near, the sharded blockchain that Aurora is built on.

Ok, so what is Near?

Near is the latest L1 to garner attention in crypto due to its $800M+ ecosystem fund and the momentum of Aurora. A PoS chain with dynamic sharding and 2 second finality, it is viewed in some aspect as the ETH 2.0 roadmap. There are differences, however, as Near’s use of dynamic sharding is how it plans to scale vs Ethereum being rollup-centric. Another big difference vs other ecosystems is that they are not trying to depend on one environment or language. While Rust is the main language native to Near, if a developer wants to use the EVM (Aurora), Substrate (Octopus Network), JavaScript, whatever, they can. From a user perspective the goal is that they will be able to use apps built using any of these languages seamlessly. Cross-contract calls are what allow Near to compose like this, and there are already some things happening between Near native apps and Aurora.

The Economics of NEAR

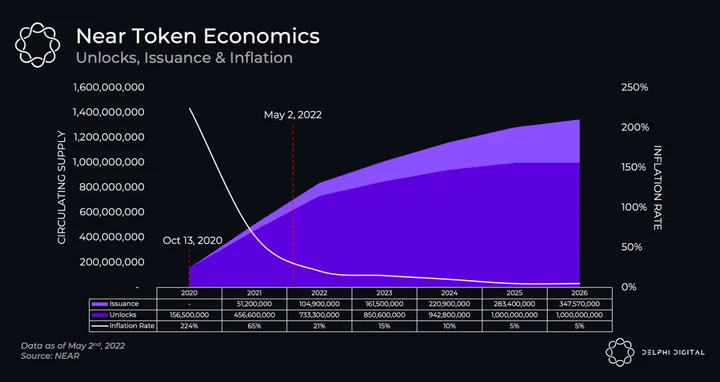

Near has one of the more unique token economics and will be important to understand when discussing the Aurora DAO’s Near validator in the second half of this report. Near economics are as follows:

- Create 5% new supply a year: 0.5% for protocol development, 4.5% to stakers/validators

- Burn 70% of transaction fees, give 30% of transaction fees to creator of contract

- Require locked NEAR to pay for storing on-chain data

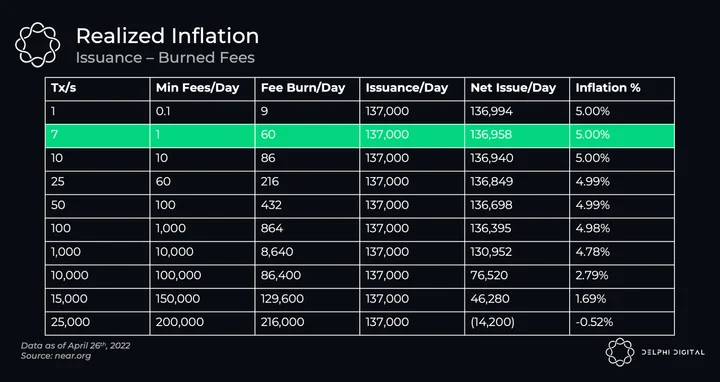

Let’s touch on each of these. The first one is simple, every year 5% new supply is created with 4.5% going to validators. This is the sole source of income for validators/stakers (outside of potential MEV). Since burning transaction fees and the token sink from storage costs benefit all holders of NEAR equally, there is no extra benefit given to validators. Thus, validator income is predictable when denominated in NEAR.

Secondly, no transaction fees go to validators. They are either burnt (70%) or sent to the contract responsible for the activity (30%). Fee burning is a popular value accrual method with many blockchains implementing some form of EIP-1559. The difference here is that, while tips on Ethereum go to miners/validators with the base fee burnt, and 50% of fees on Solana go to validators with the other 50% burnt, on NEAR none of them do. NEAR is EIP-1559 without being able to add a tip! While this sounds great in theory, without a way for two users to bid on competing transactions an off-chain/black market will develop. This is strictly worse than a pure fee market and one I believe Near will eventually have to change. A blockchain cannot avoid MEV. The 30% that is not burnt is sent to the developer of the contract. On a chain like Ethereum, none of the fees actually go to the apps that are generating them. While OpenSea and Uniswap generate millions of Ethereum fees per day, it is all either burnt or goes to validators with the app getting nothing. The top protocols are subsidizing the rest of the chain. Near rewards apps for their activity. Again, like the fee burn, while this sounds great in theory there are some potential issues. 1) there is no incentive to make contracts cheaper for users (it is the opposite), and 2) it puts pressure on contracts to pay back costs to users. In fact, this is what Aurora does today! Part of the reason they run a Near validator, which we will get to later, is to cover Rainbow bridge fees and Near transaction fees for their users. So, while validators do not make income from fees today, I believe it is quite likely they will in the future and the fee economics of Near will be changed. If you are interested in a longer read on this topic I would recommend Hasu’s piece Transaction fee economics in NEAR and the resulting discussion on the Near forum.

Lastly we have storage costs, the requirement to stake/lock NEAR in a contract to pay for the data that is stored on-chain. This is another notable difference to the Ethereum fee model, in which storage is paid up-front in a one-time transaction fee, meaning the validators who did not get this fee when the transaction was created still need to store this data in the future. Requiring contract owners to lock NEAR for storage takes NEAR out of circulation, directly increasing validators’ yield by reducing supply available to stake (thus earning more of the 4.5% yearly issuance). Of course, taking NEAR out of circulation benefits all holders of NEAR, similar to the burning of transaction fees. Owners of contracts can remove/delete data to unstake tokens but this will be immaterial considering the amount of data that continues to/will be stored on-chain.

In the near-term there are still quite a few token unlocks over the next few years, resulting in double-digit inflation until 2025. From then onwards, all new supply will be the 5% issuance. Today, validators are earning ~10.6% yield as 446M NEAR are staked earning ~50M NEAR. It’s important to note that many market data sites will show a very high FDV for NEAR as they do not account for storage or transaction fees. Remember, 70% of fees are burned, and NEAR must be taken out of circulation for storage.

However, any meaningful decrease of inflation from fees and storage should not be expected soon. Currently, Near processes ~7 transactions per second, the majority coming from Aurora. This is not due to limits of the blockchain but just a demand issue. For comparison, Ethereum is 13 tx/s, Avalanche 9 tx/s, and Solana 230 tx/s (non-voting). It is possible that Near can hit these milestones in the future as crypto adoption continues to grow, but for now the burn is immaterial. Now that we have a high-level understanding of the Near blockchain and its token economics, let’s dive into Aurora.

Back to Aurora

As said prior, Aurora is the EVM deployed as a smart contract on Near. Since it is a smart contract it does not need a separate validator set or to rely on sequencers and verifiers like a rollup (although it does need relayers). Aurora shares the same security like any other contract on Near. This means that there is a lot of work removed for Aurora: it does not need to get separate validators, worry about consensus, storage, or any other tasks that a blockchain would need to handle.

Being implemented as the EVM means developers can use all of the normal tooling available in the Ethereum ecosystem and the look and feel of Aurora will be the same. Users can simply use Metamask and pay gas fees in ETH and developers have access to tools like Truffle and Hardhat for their smart contracts written in Solidity or Vyper. It is the same Ethereum experience but on Near. Now, while ETH is the native asset in Aurora and used for gas, the Near blockchain only accepts NEAR, and so Aurora needs to use relayers to make this experience work. The process is as follows:

- User signs an Ethereum transaction (e.g. with Metamask) and sends to the RPC

- RPC wraps the tx into a Near tx and sends to the Aurora contract on Near

- Transaction is verified and the original tx is sent to the Aurora engine contract

- Aurora engine contract parses the tx and executes it, calculating gas in ETH

- ETH is paid to RPC for tx

In simple terms, what has happened is that NEAR was used for gas (paid by the relayer) to execute the contract on Near with the relayer collecting ETH from the Aurora user. In a rational, completely free market, we would expect the ETH collected from the Aurora user to be slightly more than the relayer paid in gas fees on Near (to compensate for the service). While anyone can run a relayer, right now this process is heavily incentivized by the Aurora Labs RPC. Transactions were 100% subsidized (i.e. free) in the past, but in February there was an emergency update to implement 1 gwei minimum gas due to excessive load (bots) from a new game called MoonFarmers (games and nft mints tend to be the worst offenders). There is little incentive for someone to run their own relayer and pay the full NEAR gas fee while Aurora is subsidizing. Aurora wants to subsidize gas fees in perpetuity and is one of the main reasons for running the Aurora validator (to be discussed later). Combine this with Near’s sharding technology and mostly empty blockspace at the moment and you have an enticing environment for EVM developers.

As should be clear, while Aurora looks and feels like the EVM, and many users will be onboarded from Ethereum, it is not really an Ethereum scaling solution as all settlement, data availability, and execution is on Near. In other words, all of the economic value on Aurora flows to the NEAR token, not ETH. You could probably call it an EVM scaling solution though.

Looking at the most active contracts on Near, Aurora has more activity than all else combined. This speaks to the network effect of the EVM and the preference current crypto users and developers have for it. One could argue that the EVM is cannibalistic to creating developer mindshare on the native chain and is a trap that L1’s should seek to avoid. Solana and Cosmos are the only ecosystems that have been able to avoid this. Is it a good tool to get users and developers on your chain? Absolutely. Is it the best tool to develop a robust developer ecosystem native to an L1? Unclear. Yes, this is a controversial topic and not everyone agrees. Take for instance the Avalanche team, who believes the EVM has “won” but that their scaling strategy with subnets is better than Ethereum’s with rollups. Near is kind of in the middle of the extremes, taking a more neutral approach and will onboard whatever language people desire to build with.

Also important to touch on is where the tokens on Aurora are actually created. When someone wants to create a token should they be minted on Ethereum, Near, or Aurora? The answer, which may be surprising, is Ethereum. This is what allows Aurora to integrate assets as if they are native to Aurora. It is not possible to mint a token on Aurora and then bridge it to Ethereum. If you have ever bridged stablecoins to Avalanche (or just used Avalanche in general) you will notice that they have both “USDC” and “USDC.e”. USDC is native USDC to avalanche, and USDC.e is wrapped USDC bridged from Ethereum. While the assets on Aurora are still wrapped, they feel like native assets because their contract is on Ethereum and are secured by the Rainbow Bridge. This means ETH on Aurora is the same as ETH on Ethereum, and USDC on Aurora is the same as USDC on Ethereum. Aurora as it is implemented is not possible without the Rainbow Bridge. This is the most important infrastructure in the whole process and is what makes the eco work. It is one of the best live bridges today.

Getting to Aurora – a Trustless Bridge

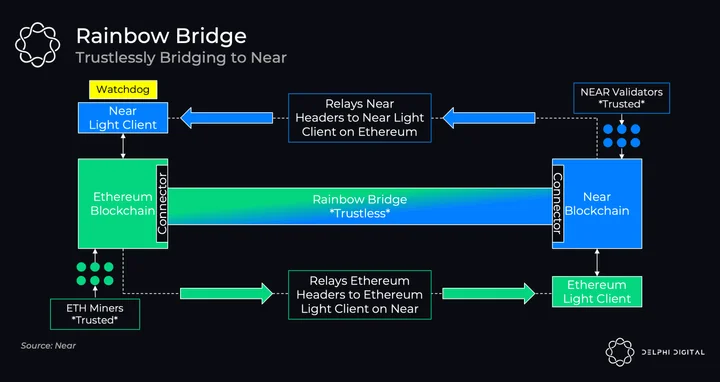

Not all bridges are built equal, and the Rainbow Bridge best exemplifies that. Built by the same team who built Near and Aurora, the Rainbow Bridge is a fully trustless bridge that allows users to bridge assets from Ethereum to Near and Aurora. What does trustless mean, and how does it differ from other bridges? It means that the operators of the bridge are not an added third party. The only two groups that a user needs to trust are:

- Miners on Ethereum

- Validators on Near

That’s it. This differs from other bridges that are actively live today, where not only do you need to trust each chain’s validators, but you also need to trust a PoA/multisig controlling the bridge. An unfortunate recent example of this is the Axie Ronin bridge, where a hacker was able to compromise 5/9 addresses in the multi-sig and drain the bridge of all it’s funds. It didn’t matter how secure the blockchains on either side of the bridge were, the multisig was the weak link. This is not possible on the Rainbow Bridge. Let’s break down the main components.

- A Near light client is implemented as a smart contract on Ethereum

- An Ethereum light client is implemented as a smart contract on Near

- Relayers that read and send the block headers to the other chain

- Connectors that prove the cryptographic hash of the transfer by utilizing the light clients

- Watchers that monitor and submit fraud proofs when needed (eg. May 1 attack attempt)

The flow is this:

- User deposits asset (e.g. ETH) on Ethereum side

- Rainbow bridge tells connector on Ethereum to lock ETH in vault

- Rainbow bridge calculates a cryptographic proof that this happened

- Relayer sends Ethereum block headers to Light Client on Near (20 blocks)

- Rainbow bridge asks connector on Near to create this ETH

- Cryptographic proof of tx is provided

- Connector looks up block headers through Light Client to verify proof independently

- Once proofs match and are confirmed, ETH is minted on Near

After this process is complete you have the native ETH locked in the vault on the Ethereum side and an equivalent amount of ETH minted on the Near side. Nowhere in this process was trust in a separate group of validators or third party. To send back to Ethereum, the ETH is burned on the Near side and released from the vault on the Ethereum side. Another benefit of this bridge is that it’s not just for transferring assets, it’s also a messaging protocol. Since the bridge is generic, any information that is cryptographically provable on Near can be used on Ethereum, and vice versa. Things like transaction details, inclusion of a transaction in a block, state of a contract, etc. can all be sent between the chains. You could bridge NFT’s and even vote on one chain with your assets on the other.

Now there are still risks with this setup as the Rainbow Bridge is an “Optimistic Bridge” when going to Ethereum. This is because verifying the validator signatures from Near is prohibitively expensive and so the Near client on Ethereum verifies everything in the header except the signature. This design relies on watchdogs to submit fraud proofs if a header has been submitted with an invalid signature. This happened on May 1st! What happened here?

- Attacker submitted contract to become relayer (permissionless) and sent fraudulent Near blocks to Ethereum

- Watchdogs noticed the block submitted did not happen on Near and sent fraud proof

- MEV bots saw the watchdog transaction and front-ran it, taking the bounty for themselves

- Fraudulent block was rolled back, attack thwarted

Fraud proofs have been discussed at length in crypto research, mostly in regards to Optimistic Rollups. There have been many critiques around them, most notably that watchdogs would not do their job or that miners would collude and censor the fraud proof. What actually happened here is that not only did miners not censor the fraud proof, they frontran it! It’s very encouraging to see these optimistic assumptions hold up in practice and protect a bridge holding $1.6B of funds. If you’re wondering why the bridge is still considered trustless when watchdogs are needed, it’s because anyone can be a watchdog, you don’t have to rely on them if you submit the fraud proofs yourself. Of course, more watchdogs are better and the Aurora team used this attack to tighten up security and make attempts even more expensive.

From a technical standpoint, the Near/Aurora/Rainbow team should be recognized for their expertise. While “EVM on another chain” may not be the most promising value prop, the Rainbow Bridge is well built and highlights that these are serious builders who know what they’re doing.

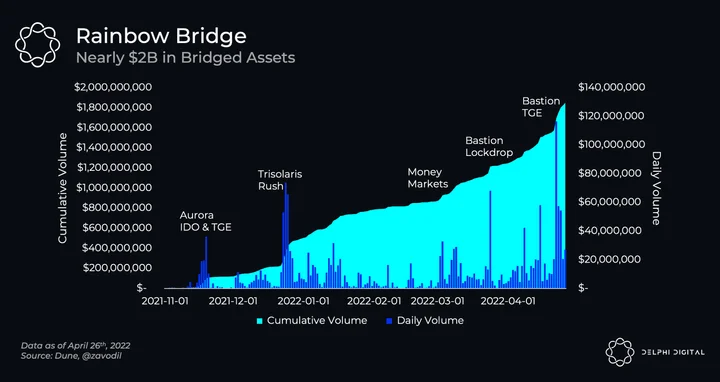

While the bridge has been live for a year now, usage did not pick up until the Aurora IDO and token launch. Since mid-November 2021 there have been ~$2B of assets transferred through the bridge. This counts transactions in both directions, but ~75% of transactions are transfers from Ethereum to Near/Aurora. Also, while a transfer from Ethereum is approximately 10 minutes (20 blocks), transfers to Ethereum are much longer (up to 16 hours). For this reason other bridges which are quicker and charge a fee (like Synapse) are used for outflows more frequently. Notable events on the chart are the IDO, Trisolaris incentives boost (including Allbridge integration and LUNA pools), money market launches, Bastion lockdrop event, and Bastion token launch.

The DeFi Ecosystem

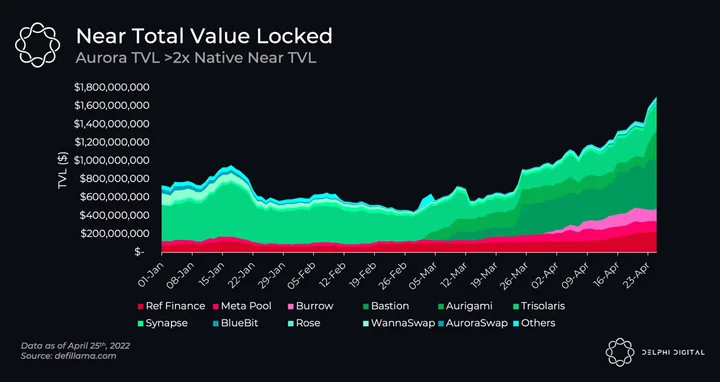

The Aurora ecosystem will look familiar to other EVM chains but in its infancy. Back in November, Trisolaris (a Sushiswap fork) was pretty much the only used protocol on Aurora and nearly the entirety of Aurora’s $150M TVL. This was mostly the case throughout 2022 until the launch of two more primitives – the money markets Bastion and Aurigami. From the end of February until now these two have driven Aurora’s TVL by $1B to sit at ~$1.4B total. The Aurora EVM has close to 3x the native Near TVL today (in fact, if you go to DefiLlama, Aurora shows up in the main section whereas you need to dig through the filter to find Near).

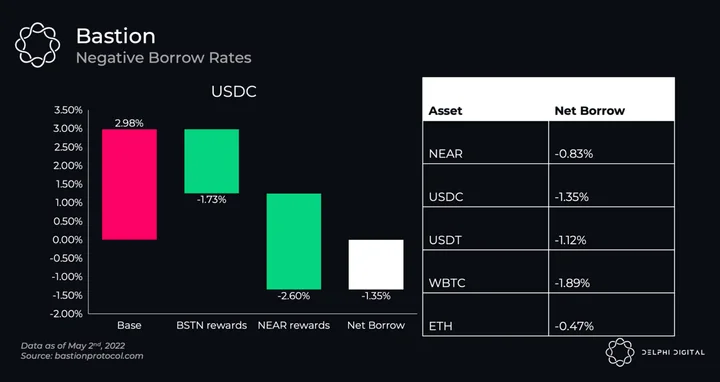

Bastion has been, by far, the largest driver of capital to Aurora. Their lockdrop hit $300M in March and they announced a $9M raise from notable funds a few weeks later. Due to the lockdrop and heavy incentives on the platform there is a negative borrow on stablecoins at -1.5%. This makes Bastion one of the cheapest places to borrow in crypto and will continue to drive more capital to Aurora. Other money markets can’t compete with a negative borrow and being the same EVM experience people are familiar with, the switch is simple (just bridge and change Metamask to the pre-populated Aurora RPC). This bootstrapping/paying for liquidity phase by Bastion has kicked Aurora activity into the next gear. While not organic usage, it will spur activity nonetheless and continue to drive users. The other money market, Aurigami, is in a similar boat to Bastion as having just done their own raise in February and their public IDO upcoming on May 5. Money markets are arguably the most important primitive before an ecosystem can start to grow and Aurora now has two that combine for ~$1B at extremely attractive rates. The ecosystem is going through an explosive phase but has been driven by three protocols so far: Trisolaris, Bastion & Aurigami. With Near’s $800M+ ecosystem fund, AURORA incentives from the DAO (i.e. cheap fees), and continued venture capital interest, it’s unlikely the momentum will stop. You can check out the full ecosystem here.

Recently, Aurora has started integrating with Near native protocols Meta Pool and Ref Finance. Meta Pool is the main liquid staking protocol on Near, allowing users to use staked NEAR in DeFi (you can check out the Solana Liquid Staking piece to better understand how these work). stNEAR launched in 2021, and when Trisolaris originally added support on Aurora this year, users needed to send assets to Near, deposit NEAR for stNEAR on Meta Pool, and then send back to Aurora. This was a cumbersome process as Near is a completely different experience (not EVM, can’t use Metamask) and setting up an account required using a centralized exchange. In mid-April Meta Pool simplified this by integrating the Rainbow Bridge for cross contract calls, allowing users to get stNEAR without leaving Aurora (Note – the Rainbow Bridge is not actually needed for cross contract calls, the UI just signs the required transaction). Ref Finance, the largest AMM/DEX native to Near, is launching a similar feature in May; an aggregator on Ref facilitating swaps using liquidity from both Ref on Near and Trisolaris on Aurora. This means native Near users can tap into Aurora’s liquidity using their Near address, never having to actually interact with Aurora directly. These cross contract calls highlight the kind of composability you can get between the Near and Aurora ecosystems. Ref’s TVL has tripled since the second week of April, most recently driven by the anticipation for and launch of Near’s new stablecoin, USN.

Near’s Stable – USN

We should touch on the new stablecoin launched on Near by Decentral Bank Dao because

- It’s topical (YOU GET A STABLECOIN! YOU GET A STABLECOIN! EVERYBODY GETS A STABLECOIN!!!)

- Native stablecoins are heavily incentivized and drive activity to the eco

- Aurora protocols have already announced incentives

USN is a mashup between UST and FRAX. First, people will be able to mint USN by swapping NEAR at a 1:1 ratio. The same arbitrage that UST has will be in place: if USN is <$1 on the market you can sell to the Decentral Bank for $1 in NEAR. If it is trading >$1 you can buy for $1 in NEAR and sell on market. The NEAR that is used to mint USN is then staked to earn the NEAR staking yield and distributed to holders of USN, funding a minimum ~11% yield for USN. This part is a hybrid LUNA/Anchor model, combining the minting of the stable using the native (LUNA seignorage) and the bLUNA deposits in Anchor funding the UST yield. It has been mentioned that because NEAR isn’t burned like LUNA that it means USN is overcollateralized and LUNA is not. This is not the correct framing as the mechanism is mostly the same; LUNA can be re-minted when UST is sold. The only difference is USN combining the Anchor part directly into the creation of the stable.

The second portion of the design is additional backing in the form of USDT. Users will be able to mint USN using USDT, meaning a portion of the supply will be matched from an asset/liability standpoint, albeit with centralized assets.

According to the whitepaper the reserve will be collateralized 2:1 with USDT and NEAR, decaying over time. This decay is similar to the FRAX model, the difference being that FRAX uses its own governance token for the algorithmic part whereas USN uses the L1’s native asset NEAR (which has other uses outside of being USN backing). A safe zone to start reducing the ratio is modelled at 1B USN which would mean $1B NEAR and $1B USDT. It is not clear if this is the exact plan nor where they would get $1B USDT from, so until more specifics are released we cannot be sure of the exact mechanics. More details should be released in the coming days.

Incentives have been announced for the three main money markets in the Near ecosystem: Bastion & Aurigami on Aurora and Burrow on Near. Users will be able to mint and deposit to earn a minimum of 11% yield with extra protocol incentives on top. This could challenge UST yields and at a minimum will be one of the best places for yields on stablecoins. With the negative borrow on money markets it seems likely that recursive borrowing will increase the USN supply quite quickly (deposit USN → borrow USDC at negative rate → swap USDC for USN → deposit USN → borrow USDC at negative rate). This could be mitigated somewhat if USN is onboarded to isolated pools and borrowing becomes less incentivized. With the current bear market backdrop and overall low yields in crypto, USN should attract capital. It will have competition though as it looks like UST is coming to Bastion as well.

Aurora DAO

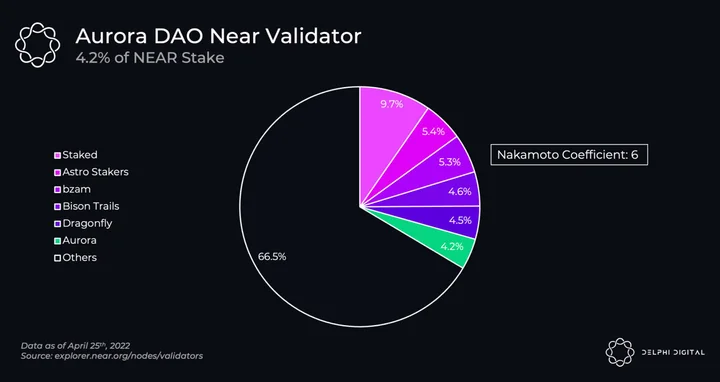

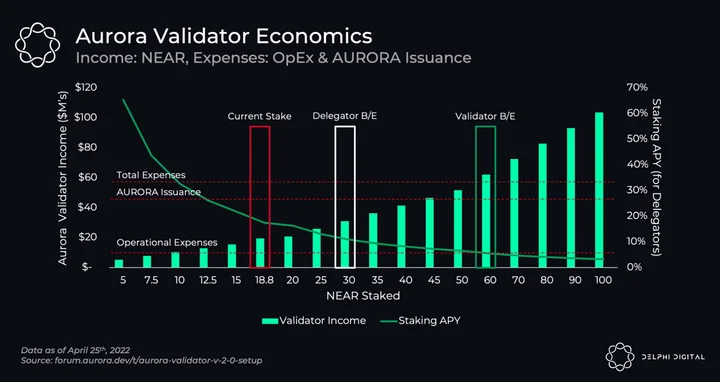

If you recall from earlier in this report, Aurora subsidizes all of the gas fees that their relayer pays. To do this, 3% of the token supply (30M AURORA, ~$250M at current prices) was set aside to incentivize delegations to their validator. Launched in January, the Aurora Validator is already the 6th largest in the ecosystem and is part of Near’s Nakamoto Coefficient (validators that make up >33% of stake). As a reminder, this is a Near validator. Aurora does not have validators. This is the Aurora DAO running a validator on the Near blockchain. The launch coincided with Near’s release of Staking Farms, allowing projects to run Near validators and incentivize usage with their native token. Users delegate their NEAR tokens to the Aurora validator and get paid AURORA tokens, not NEAR, in return. It is meant to give a greater distribution of a project’s token supply to the Near ecosystem and allow them to bootstrap a validator, but as we will see, the economics of running a Stake Farm are quite poor.

Let’s have a little refresher on the Near economics. Validators earn 4.5% issuance but no transaction fees. Right now it is a yield of about 10.6% for running a validator. The way the Aurora validator works is that it takes a 100% fee (all of the NEAR rewards) and pays stakers AURORA instead. These NEAR rewards are then used to cover the gas fees (paid by the Aurora relayer) and the Rainbow Bridge. Another important aspect to note here is that with a Stake Farm 30% of the NEAR rewards are burned.

Aurora’s operational expenses for Near gas fees and the bridge cost ~$12M/year. At current stake, the validator is making ~$19M in NEAR rewards. From this perspective the validator is profitable and covering the operational costs of running Aurora. However, when including AURORA incentives it is impossible to make a real profit under Near’s economics. Why? Someone delegating to the Aurora validator must demand a return greater than the 10.6% yield. Since Aurora earns all the NEAR, the yield is made up for in AURORA tokens. The validator has an 18.8M NEAR delegation and is paying 5M AURORA tokens/year, meaning it is paying ~$2.35 for every $1 of NEAR it earns. Taking into account the 30% NEAR burn, the Aurora validator is making around 7%, but delegators will still demand >10.6%. As no transaction fees go to validators, there is no scenario where this would become a profitable endeavour. At 30M NEAR staked the yield of the validator would be ~10.6%, meaning delegators would break-even compared to other validators, but Aurora needs ~double this amount staked to earn a real profit. These two competing market forces make this an impossibility in a rational market. In a vacuum, Aurora would be better off just swapping AURORA from the DAO for NEAR at a cost of 1:1 instead of the 2.35:1 it is currently doing.

So why is Aurora doing this? One reason is to grow the Aurora ecosystem. It is thought that by distributing the token to more users it will decentralize the ownership and get more people interested in Aurora. Of course, a purely profit focused investor could just sell the farmed tokens for NEAR and re-delegate, compounding to earn the higher APR. Eventually one would expect that after being a reliable validator in the ecosystem they will be able to retain stake without offering extra rewards. In the long run the DAO could have a normal validator with a 10% fee cut, standard across the eco. In crypto, projects tend to not think of issuing their native token as an expense, but this is a mistake. The only rational argument for offering these rewards is purely as bootstrapping until the DAO can self-sustain it by turning off AURORA rewards. You could also take a more myopic view and see this as a ploy for Aurora to take over the network, although considering the Near team created Aurora and the Rainbow Bridge, it is unlikely (but still worth noting!). With 30M allocated to the validator it still has a lot of runway, but I would expect this debate to come up again in the Aurora community before that’s depleted.

The Economics of AURORA

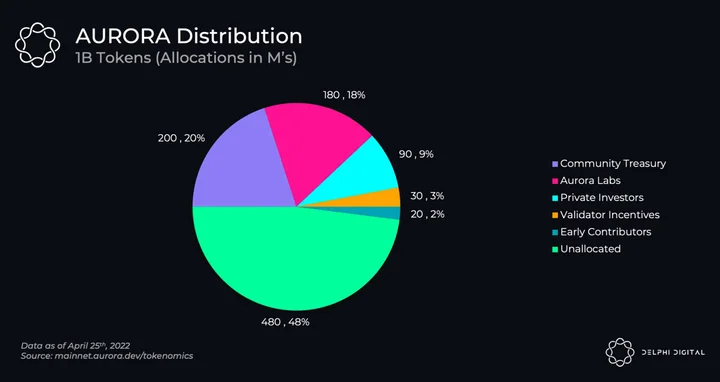

At this point you are probably wondering, wait… if gas is paid in NEAR, and validation is done by Near validators, and the UX on Aurora has users paying gas in ETH, then what is AURORA for? As of now, nothing, but upcoming it will be used to vote on use of the treasury’s funds. First, the supply breakdown.

About half of the token supply is allocated with the other half up for future use.

- 20% Community treasury used for their Jet Platform (outlined below)

- 18% Aurora Labs (2% unlocked in IDO and used for farming rewards, 16% start unlocking in November 2022 for 2 years linear)

- 9% Private investors (new unlock schedule extended through to November 2024)

- 3% Validator Incentive (highlighted in prior section)

- 2% Early eco contributors

- 48% Unallocated

Right now the float is very small (2.3% circulating) consisting of tokens from the IDO, farming rewards, validator rewards, and some advisor tokens. At $7.24 on May 2nd it has a FDV of $7.24B, down from $35B at the peak in January. For comparison, Near’s current market cap is $8B and projected 2032 market cap is $20B (based on issuance with no burn). There has been a lot of pressure on Aurora’s token as it has only been used for incentives. Without a real value accrual driver plus upcoming unlocks it will likely continue to be. The first main use for the token is the upcoming Jet platform, and it will work like this:

- Users stake AURORA

- Protocols that want funding put up proposals

- AURORA holders vote

- Approved projects get AURORA from DAO treasury and potentially NEAR from the Near Foundation & Proximity labs

- Stakers get project tokens & AURORA tokens from the treasury

While there are more nuances/details, that’s the gist of it. In Aurora’s own words, they want to be a “Kickstarter” type platform for the ecosystem, and 20% of the token supply has been allocated for it. You may have noticed that the only uses for AURORA mentioned so far are incentives; incentives to bootstrap the validator and incentives to bootstrap the ecosystem. Obviously this cannot be a long-term use for the token as there will need to be some sort of real earning potential in the future for it to have value today. So how could value flow back to AURORA? According to Aurora, Rainbow Bridge transfer fees and fast transfer fees, additional fees on the contract, a private transaction service from their validator, and farming locked funds in the Rainbow Bridge. The simplest value accrual method, however, may be the Aurora Labs RPC. Aurora subsidizes NEAR fees for users but in the future could make a small fee for handling the service and convenience. So while there is no clear near-term path there will be options, but will need to wrestle with users used to subsidized fees. The token that will undoubtedly benefit from Aurora’s activity is NEAR.

Will Familiarity and Incentives Drive Lasting Demand?

Aurora is a novel implementation of the EVM, but the Rainbow Bridge is the main innovation. The entire ecosystem does not work without it. In the near-term, Aurora will likely attract more capital, users and devs as it’s cheap, familiar, and will have attractive yields. Will this be enough to create a larger, longer lasting ecosystem on Near? Can Aurora be used as a bootstrapping tool to bring capital over from Ethereum and then start composing with Near native applications (like Ref Finance), drawing users and developers into the Near ecosystem? Or will Aurora just be another EVM chain that people go for yields before moving onto the next one?

I find it difficult to imagine a future where the EVM is dominant and another ecosystem outside Ethereum benefits the most from it, but that doesn’t mean they can’t benefit from it, and it doesn’t mean it’s not a good strategy to get users. Near’s strategy of allowing any language and then composing them is super interesting; it may be tougher to build a devoted group in one language but you will be able to accommodate substantially more. The Rainbow Bridge allows Aurora to look and feel like any other Ethereum L2, and it will be cheaper than the Ethereum L2’s as it doesn’t settle on Ethereum (Optimistic rollup fees are usually ~$0.50-$3, depending on how congested L1 is). It’s already close to the TVL on Arbitrum and is doing ~4x the transactions per day while significantly surpassing Optimism on both fronts. Token launches should help propel those ecosystems but the backing from Near & low fees will keep Aurora in the mix. It should also be said that Aurora is not just an EVM fork where the block size is raised and that’s it. The build is sound and there’s no better way to highlight this than the Rainbow Bridge, which allows full composability with Ethereum. However, if Aurora is Near’s only regularly used environment in a couple years I would see that as a disappointment. If it leads to long lasting organic demand on Near outside of the EVM, a large success. It got the ball rolling, bringing over $1B+ liquidity and starting to compose with Near native apps. What will that mean for its competitiveness vs Ethereum L2’s, and what will that mean for the future of Near?

0 Comments