BlackRock

The SEC is suing Ripple and the lawsuit is expected to come to fruition soon. Ripple’s lawyers have been advocating for the public disclosure of the Hinman documents, which consist of internal communications within the SEC regarding the agency’s discussions and considerations of the speech given by former SEC official William Hinman where he asserted that Ethereum is not a security.

XRP has been claiming the public release of the Hinman documents would be a big win for them, and this week those documents were released. Naturally, this case is very important as the SEC will likely look to use a potential XRP loss here as precedent for future lawsuits.

The crypto market finds itself in a position where regulatory uncertainty is at an all-time high, and while the fruition of this case could provide clarity, it’s more likely to create even more confusion. The market also has a catalyst with the potential to have a seismic impact.

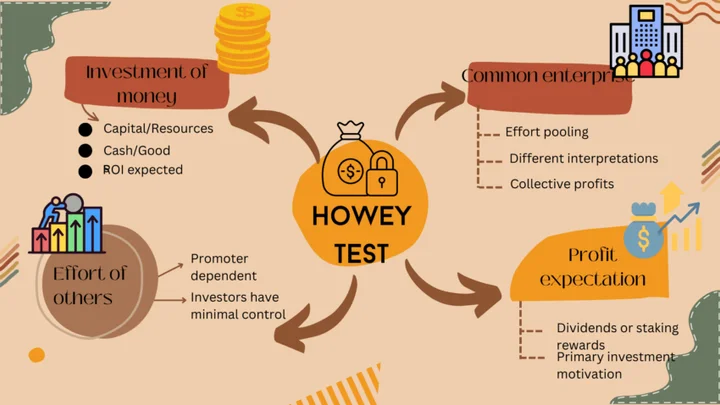

The SEC is attempting to use The Howey Test as the barometer for whether a digital asset is or is not a security. The Howey Test (as explained in our digest from 2 weeks ago) is simple:

(BeInCrypto)

- Is there an investment of money?

- Is there a reasonable expectation of profits?

- Is the investment in a common enterprise?

- Is it reliant on the efforts of a promoter or third party?

If there is an asset that is exchanged between two parties, and the asset is exchanged while meeting these 4 conditions, then the asset is a security and it falls under the jurisdiction of the SEC.

Let’s go through the 4.

1. Investment of money.

This one is pretty straightforward for many market participants. Generally, when most people buy bitcoin, they are buying because they think it will appreciate in value and that will benefit you in one way or another. Now, part of the value prop of bitcoin is that it enables efficient permissionless cross-border money transfers, self-custody and access to a decentralized network that no single party is in control of. This foundation is the most primitive use case of cryptocurrency in general, with many more use cases being built every day. While it’s reasonable to assume that a lot of market participants purchase cryptocurrency to speculate on its value, it’s equally reasonable to assume that a lot of market participants purchase cryptocurrency to USE it as well.

2. Expectation of profit.

Again, this is pretty similar to the first rule when applied to various coins. The underlying value of public permissionless networks is the utility that they provide to users. Let’s say there’s a new crypto game that rewards users for playing the game in some fashion. But, there is a gameplay component that rewards users for spending those rewards. If I enjoy the game and think it is viable, I may purchase those tokens to both use in the game, and hold as an investment. When I purchase those tokens, I may not know exactly what my plan is with how many of the tokens I will spend/use, I just know that I want to participate in the network in one way or another, via exposure or spend. Naturally, each purchaser of a token will have their own various reasons for purchase.

3. Common enterprise.

The common enterprise rule is important for clarity around expectations. For example, when there are multiple different investors that pool their money together to participate in an investment contract, it is likely that they all were operating under the same assumption of expectations for that contract. When a new crypto project raises funds, it generally is raising funds through some sort of “contract” that sets expectations. What is contentious though is when the token itself is trading on secondary markets, does a contract still exist between buyers of these tokens and the “common enterprise” ? Surely, the nature of that “contract” can change. For example, when Ethereum had an ICO, it raised money from investors with the promise of something from a central group of promoters. But, what about now? If we know that Ethereum is decentralized, who would be on the other side of the contract if someone decides to buy some ETH?

4. Efforts of a promoter or third party.

This is probably the most important of the 4, and I’ll explain why. Mainly, the purpose of the SEC is to keep our markets efficient. If fraud occurs, somebody *has* to be held accountable. If there were no repercussions for fraud, there would be no incentive to build honest businesses with valuable use cases. When the SEC punishes bad actors, good actors are rewarded and innovation is able to thrive. What makes cryptocurrency so unique, is the idea that digital assets can actually achieve a certain level of decentralization, where there is no lone actor who could commit massive fraud to destroy a network. Bitcoin and Ethereum are the most obvious examples here, where there is no one person in the world who can take those networks down, and thus be held accountable for their actions. The same is more true with an established Layer-1, and less true with a pre-seed DeFi protocol raising money from investors.

Tying it all together, if there is a group of people that invest their money together in something, with an expectation of profit that is reliant on a third party…that investment contract is likely a security as defined by the howey test. And naturally, a law created in 1946 around orange groves is difficult to apply to public permissionless networks.

The heart of the nuance here lies within that generally it takes a centralized effort to pursue and achieve decentralization. What begins as a centralized contract between two parties can evolve into a decentralized network of participants. One argument against this idea is that the initial party who is promoting the network, by default will always be *the* promoter of that network because of their exposure to the network itself. In essence, if a team were to reserve 20% of the token supply for themselves, this signals to market participants that the team is incentivized to promote the network and thus all of the team’s efforts stand as network promoters no matter how decentralized the protocol becomes.

In fact, this was what the SEC argued in its lawsuit against LBRY that did declare LBRY a security. Here was what the court ruled: “The problem for LBRY is not just that a reasonable purchaser of LBC would understand that the tokens being offered represented investment opportunities – even if LBRY never said a word about it. It is that, by retaining hundreds of millions of LBC for itself, LBRY also signaled that it was motivated to work tirelessly to improve the value of its blockchain for itself and any LBC purchasers.

This structure, which any reasonable purchaser would understand, would lead purchasers of LBC to expect that they too would profit from their holdings of LBC as a result of LBRY’s assiduous efforts.” Now, this is where the Hinman documents come into play. Hinman himself did agree with this interpretation, stating “Has this person or group retained a stake or other interest in the digital asset such that it would be motivated to expend efforts to cause an increase in value in the digital asset?” as a determining factor for security classification.

This then received 2 internal SEC comments by the Office of General Counsel (OGC) and T&M stating “Why is this factor relevant and how would it be applied?” along with “This does not seem relevant.” As a biased crypto enthusiast, I would say I do actually agree that the exposure to the token itself can become less relevant over time. If a centralized project were to hire someone for marketing purposes, and then pay them in USD…the actions of that marketer are not suddenly less promoter-like simply because they don’t have a stake in that digital asset. I would then say that what actually matters is the *effort* itself, to which the SEC would say it’s the assumed motivation of *any* effort at all.

This then received 2 internal SEC comments by the Office of General Counsel (OGC) and T&M stating “Why is this factor relevant and how would it be applied?” along with “This does not seem relevant.” As a biased crypto enthusiast, I would say I do actually agree that the exposure to the token itself can become less relevant over time. If a centralized project were to hire someone for marketing purposes, and then pay them in USD…the actions of that marketer are not suddenly less promoter-like simply because they don’t have a stake in that digital asset. I would then say that what actually matters is the *effort* itself, to which the SEC would say it’s the assumed motivation of *any* effort at all.

At this point, I’d point out that there is a difference between effort and power. With bitcoin, there is no single party that wields enough power to set investor expectations. Bitcoin is an isolated network with an anonymous founder who hasn’t been seen in more than 12 years. DeFi on the other hand has a completely different set of players, interests and rules. The Ethereum Virtual Machine (EVM) enabled the advent of smart contracts, introducing a permissionless environment for developers to build applications on top of, similar to the internet.

The core innovation here was the ability for truly decentralized applications to be built for users. Uniswap, for example, is a decentralized exchange that features an automated market maker that lets users exchange with one another permissionlessly. The Ethereum Virtual Machine enabled Uniswap to be created, something that could not have been built on top of Bitcoin. Uniswap itself makes Ethereum more valuable, because Uniswap enables more activity to occur on top of Ethereum.

And this itself is the value proposition of Ethereum. In its current state, it can act as infrastructure for other things to be built on top of it, and maybe those things will make it more valuable. Plus, nobody can shut it down! Nobody is in control of Ethereum, you could make the argument that Vitalik is in charge, but if anything he is more the steward of an uncontrollable ship that he is doing his best to point the sails in the right direction of. The underlying value of Ethereum is derived from its utility of *being decentralized*.

There is no singular “effort” that you can point to that drives a common expectation, because nobody is actually in control. Even if Vitalik had massive exposure to Ethereum itself, which he does, his stake doesn’t give him a meaningful increase in actual power over the protocol. He would need to own so much Ethereum that he could dictate the outcomes of governance votes. If that were the case, then yes, it would be reasonable to assume that he *is* in charge, and Ethereum wouldn’t be decentralized. But, what is the margin of token exposure that actually would make one actor have control over a protocol? 50%? I have no idea, but this may be a good question for regulators to ask.

And here we are, looking at a spectrum of decentralization to determine which regulatory body should oversee these assets. There are only 3 problems with this:

1. Most coins are different from one another

2. The pace of innovation is accelerating

3. Decentralization is subjective

- Most coins are different from one another.

You have Layer 1s, Layer 2s, Decentralized Exchanges, Lending Pools, AI coins (?), veTokens, Real-World Assets and many many more categories all with varying consensus mechanisms, tokenomics, governance designs and utilities. The complexity involved with any regulatory body to attempt to spend the resources to go case-by-case and determine what is and isn’t a security is simply impossible.

- The pace of innovation is accelerating.

The beauty of permissionless innovation…is that exactly! The innovation is permissionless and nobody knows what is going to be created next. Even if a regulatory body were somehow able to go case-by-case with every meaningful cryptocurrency, they would always be in a state of cat and mouse, trying to understand the complexities of the next novel protocol and token design. Code moves faster than regulators, and that is a feature not a bug.

- Decentralization is subjective.

There is no actual definition of decentralization for any regulatory body to refer to. A protocol, in theory, could go from being centralized to decentralized and then back to centralized. Gathering consensus over an asset’s decentralization classification is extremely difficult as has been made glaringly obvious over the past few months.

Right now, all of these problems are actually amplified by a lack of guidance by regulatory bodies. The current stance of the SEC, in which they attempt to apply the Howey test to determine whether a cryptocurrency is or isn’t a security, should almost be disqualifying towards taking their judgment seriously. This idea of regulation by enforcement, and to attempt to retrofit this law from 1946 towards digital assets in 2023 is genuinely counterproductive and much more harmful to the United States than it will ever be to this global industry.

Good actors are punished if they attempt to register with the SEC, and bad actors are rewarded by just simply engaging in fraud with no repercussions. A clear definition of decentralization needs to be established to act as a north star for the crypto ecosystem to aspire towards, along with a barometer for regulatory bodies to use. The United States currently benefits heavily from the global financial system, and they are rightfully concerned by the implications that decentralization presents. Regardless of the outcome of the Ripple lawsuit, which Ripple seems likely to lose… this approach of regulation by enforcement simply won’t work.

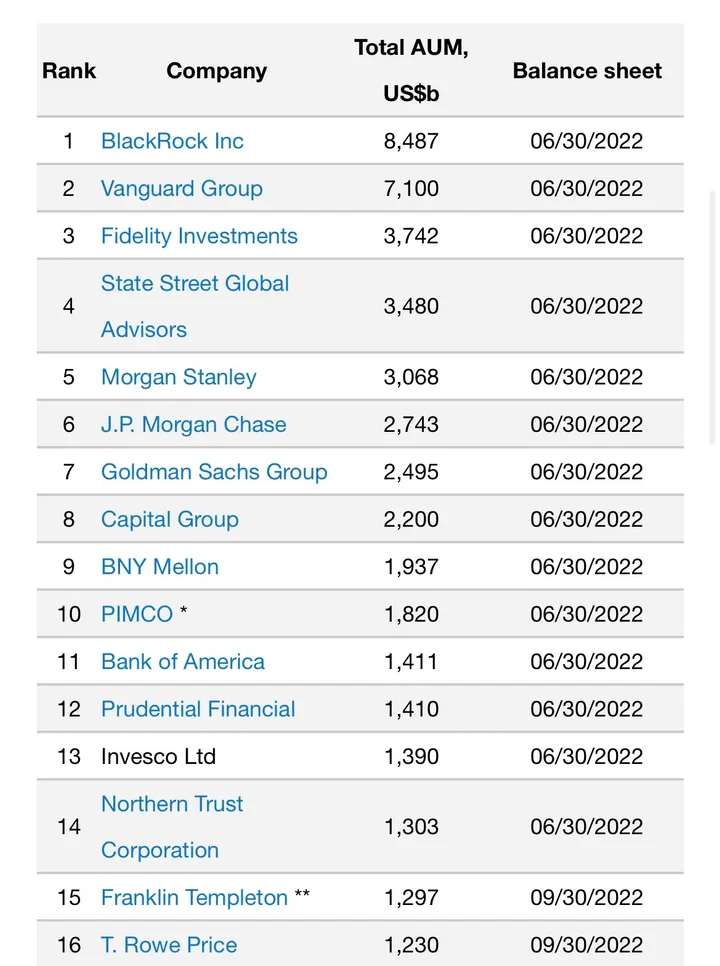

This week, BlackRock, the world’s largest asset manager (AUM $8.5T) filed for a bitcoin ETF that would allow investors to safely get exposure to Bitcoin.

Here’s a fun fact: BlackRock’s record of getting ETFs approved by the SEC is 575-1.

Yes, decentralization does present a risk for the United States; however, attempting to regulate the industry down to zero presents an even bigger risk– one in which a new global financial system is built without them.

😭 Meme of the Week

📖 Delphi Reads (Alpha Feed Unlocked)

Reddit’s NFT initiative can be seen as a slow catalyst for NFT adoption and blockchain usage. While the numbers are modest, they are still significant! Especially considering the overall low number of active NFT participants during the current market cycle. Teng walks us through Reddit’s successful implementation of NFT avatars.

When researching Jito for the Solana report we noticed a recent uptick in MEV, and what looked like an outlier epoch with 142 SOL in MEV rewards paid. Since then, that epoch looks like anything but an outlier. Ceteris sheds light on Jito’s validator adoption and the start of a new trend.

Uniswap v4 was announced, ushering in the next chapter of decentralized exchange design. Jordan boils down Uniswap v4 to two key improvements: hooks and advanced architecture.

0 Comments