Withdrawals Are (Almost) Here

Do you hear that? That’s the sound of 17M ETH getting ready to be withdrawn from staking, nearly $30B of ETH supply previously locked up coming onto the market ready to be sold.

Or at least, that is what you may think if you’ve wandered into certain parts of crypto Twitter. While it is true that a large portion (15%) of ETH supply will be able to be unstaked from the Beacon Chain for the first time since the end of 2020, the implications are not that simple. There is a lot of nuance to Shanghai; this post will aim to distill it down the best we can.

Note — all $ conversions for ETH in this report use a price of $1,600.

Note 2 — A week after this report was published Lido announced that stETH withdrawals would be delayed ~1 month after Shanghai. This doesn’t change any medium to long-term implications but will have some effect on the short-term.

Partial vs. Full Withdrawals

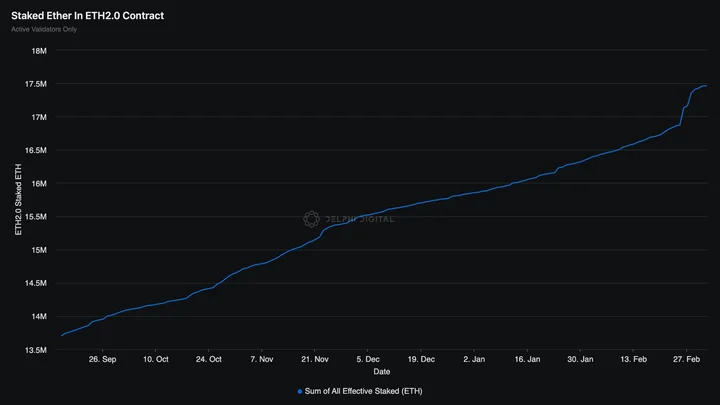

Shanghai is a hard fork tentatively slated for the second week of April that will enable withdrawals of validators from the Beacon Chain for the first time. The Beacon Chain has been in deposit-only mode since it went live at the end of 2020, and over the past 2+ years has had ~17M ETH deposited (in 32 ETH increments) and ~1M of accrued staking rewards earned. Immediately after the hard fork, this ETH can be unstaked/withdrawn, but with notable caveats.

First, staking rewards and the deposited 32 ETH/validator are considered separately. Staking rewards fall into the “partial” withdrawals bucket. These will be automatically swept to an Ethereum address after Shanghai and be able to be spent as soon as received. Withdrawing the rewards and the 32 ETH balance falls under a “full” withdrawal. These have stricter rate-limiting rules (i.e., churn) on the amount that can exit per day.

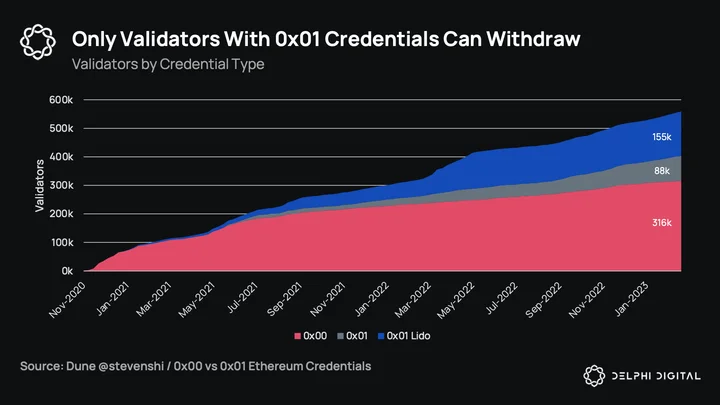

Second, ETH can only be withdrawn (both full and partial) if validators have updated their credential prefixes to the 0x01 format from 0x00. The technicals here are not that important for the purposes of this report, but note that most validators have 0x00 and will need to switch. Lido has been the largest adopter of 0x01 and will be prioritized when withdrawals are activated.

Partial rewards will have an immediate impact on ETH’s circulating supply, while full withdrawals will be a more drawn-out process with counteracting forces.

Partial Withdrawals

Breaking down the partial withdrawals, we get:

-

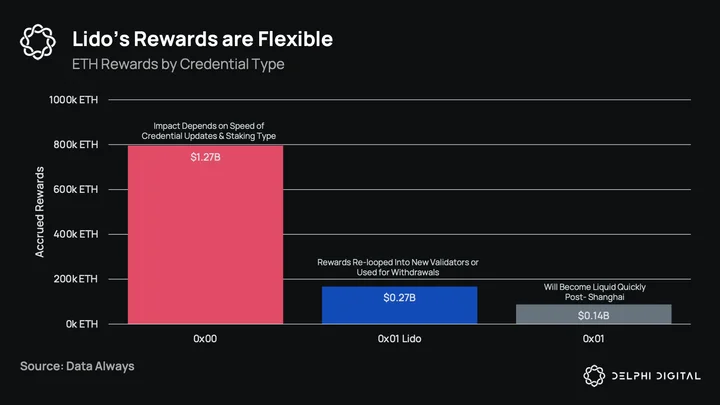

796k ETH ($1.3B) currently non-withdrawable due to 0x00 credentials

-

167k ETH ($0.3B) withdrawable to Lido validators

-

87k ETH ($0.14B) withdrawable to others

Lido has some flexibility with their rewards: they can use them to process stETH redemptions or they can re-loop these into new validators depending on the amount of stETH that wants to exit. For the others that have updated to 0x01, we can expect some selling pressure when they receive rewards. ETH validators cannot compound their stake (i.e., there is no difference in APR if you have 32 or 36 ETH staked) and so this ETH will find its way somewhere rather quickly. Whether that is into liquid staking tokens, stablecoins, or anything else is a guess. As for the largest portion, validators still need to update their credentials. While it’s just a one-time change, the process is important to get correct because there is no changing the address after the fact (seriously, don’t mess this up validators).

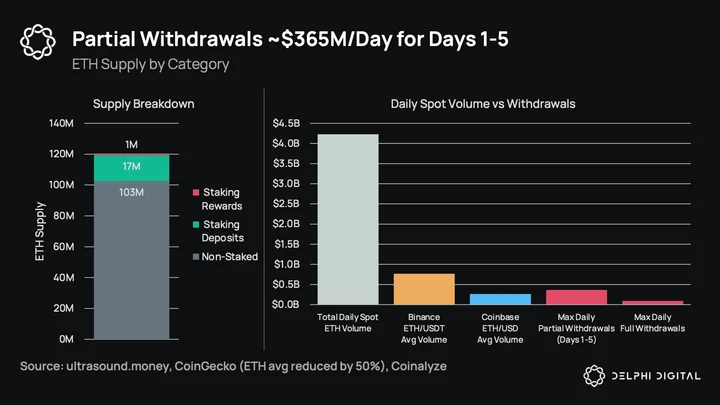

Partial withdrawals will be processed at a rate of 16 partial withdrawals/slot (12 seconds), so with 7.2k slots/day, and assuming everyone’s updated to 0x01, we can expect partial withdrawals for ~115k validators/day. To run through the whole validator set (~530k) will take about 4-5 days. This would be ~228k ETH ($365M) per day, although a bit lower on day 1 as Lido will be prioritized and has lower relative rewards.

Full Withdrawals

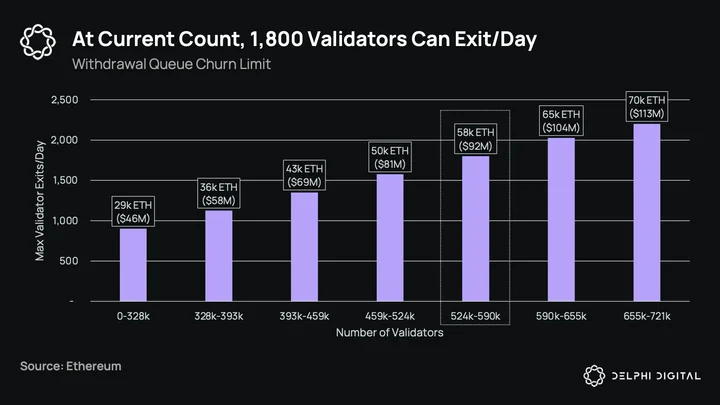

Full withdrawals are similar to partial in that they’ll be part of the same queue above. If, during the automatic processing of partial withdrawals, the validator is marked as “exited,” then a full withdrawal of their balance + rewards will be performed. The main difference here is that full withdrawals are more rate-limited, with a maximum number of exits per epoch depending on the validator count. At the current count of ~530k, this means 8 exits per epoch (1,800/day) equating to 58k ETH/$92M per day. To illustrate, withdrawing the entire validator set of 530k would take 516 days under the hypothetical extreme scenario of max daily withdrawals and no inflows. While that will obviously not happen, it is likely that full withdrawals will outpace deposits for a month or so before settling into the expected consistent uptrend (will touch on this later).

One group we know will be exiting early are the slashed and voluntarily withdrawn validators. There are about 1,150 of them with combined balances of ~37k ETH ($59M). The voluntary validators are essentially jumping the line, foregoing any potential ETH rewards over the final few months to ensure an early exit. Seeing as they are front-running the exit, it is likely that some of these are looking to exit entirely, while others may just want their ETH to be more liquid and used in DeFi (i.e., swap for or mint a liquid staking token).

Implications for ETH

Now that we understand Shanghai and the mechanics around it, we’ll look at the implications for ETH and Ethereum, both in the short and long-term. While the short-term implications around withdrawals may be more topical, we believe the mid and long-term ones are more interesting.

Visualizing Potential Sell Pressure

We’ve gone over what the rough numbers may be for partial and full withdrawals, but this is only so valuable without context. First, the partial withdrawals of ~1M ETH make up 0.80% of the total supply and the staked deposits ~14.5%. Second, if we look at estimated partial withdrawals and full withdrawals/day compared to ETH spot volumes, we have:

-

Partial

-

4.5-9.0% of total daily spot (CoinGecko data)

-

47% of Binance daily ETH/USDT volume (a bit less if including BUSD pairs)

-

138% of Coinbase daily ETH/USD volume (average of trailing 30 days)

-

-

Full

-

1-2% of total daily spot

-

12% of Binance daily ETH/USDT

-

35% of Coinbase daily ETH/USD

-

These numbers may seem pretty high at first, and they are, but we should consider a few things. First, the partial withdrawals are going to be fully processed in ~5 days. After that, they have no impact. Second, this assumes all partial withdrawals are sold to USD, but this is not consistent with how PoS actors behave on other chains (they usually just continue compounding). We mentioned above how solo stakers can’t compound their rewards, but they can just buy a liquid staking token with their rewards instead. Still, there’s a chance that a large amount of partial withdrawals will be sold purely because people expect others to do the same, becoming somewhat of a self-fulfilling prophecy. Lastly, we expect staking deposits to increase post-Shanghai, which will be a strong counter-balancing effect.

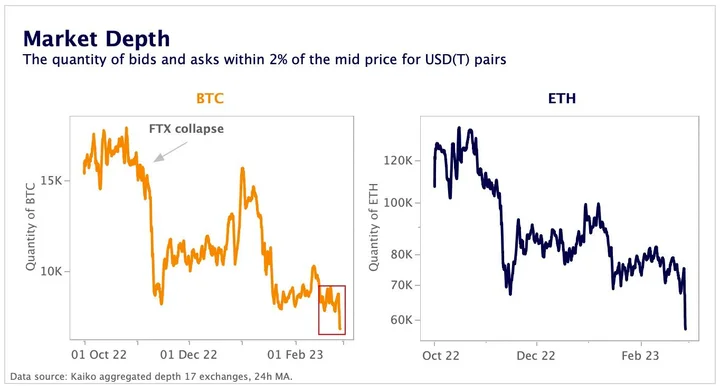

There’s also the fact that liquidity has dried up considerably over the past few months, with the 2% market depth down from 120k ETH in October to 60k today. If Shanghai was in the middle of the bull market with ample liquidity, we would probably consider it a non-event. And while it still may be, the odds of larger-than-expected moves are possible given current conditions. Of course, low liquidity does not indicate a particular direction, it just increases the odds of a large move.

The Demand/Deposit Side of the Equation

With all this being said, we have so far only focused on one side of the equation: supply. But there is the demand side to Shanghai as well — rather than seeing it as an unlocking event, seeing it as a de-risking event that will cause a surge in staked ETH instead. There are multiple reasons to see Shanghai in this light, the two most important being:

-

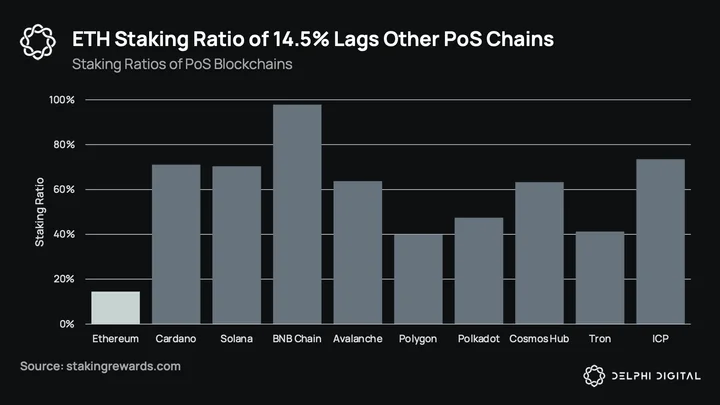

ETH’s staking ratio of 14.5% pales in comparison to other PoS networks

-

Duration risk of both solo stake and liquid staking tokens is reduced considerably

While we do not expect ETH’s staking ratio to get as high as other protocols, we do expect it to trend up to ~30% or more over the next couple of years. There are a few reasons we don’t expect it to get as high as others anytime soon, such as:

-

Most PoS networks launch with a % of locked supply staking; Ethereum launched as PoW and has transitioned over time

-

No in-protocol delegation adds some amount of friction to staking (have to buy a liquid staking token if delegating, can’t delegate native ETH)

-

WETH sits in AMMs and acts as a router asset in DeFi

-

L2s attract native ETH on multiple bridges, as L2s use ETH for gas

-

Early participants don’t want to trigger tax consequences

-

Staking APR gets quite diluted at 30%+ staking rates

None of these reasons are too prohibitive individually, but together they will likely put a cap on staking. The staking rate won’t really change Ethereum’s security properties in a practical sense, it is more so the implications for yields and liquid staking tokens’ potential.

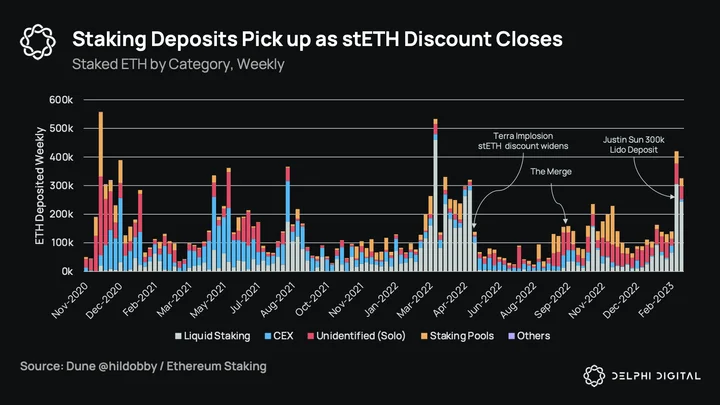

The amount staked also took a jump at the end of February, mostly led by Justin Sun depositing nearly 300k ETH ($0.5B) into Lido at the end of February. Why His Excellency would deposit so much one month before Shanghai is not clear (if you’ve waited this long, why not wait a few more weeks?), but it is a vote of confidence for Lido and by extension Ethereum (chart below courtesy of our new Datahub).

Deposits have been trending up in 2023 after going through a lull in the summer of 2022. There were two reasons for this lull.

First, the Terra implosion caused Lido’s stETH token to trade at a significant discount to par as it was widely used as collateral throughout the ecosystem and had to be sold on the open market (no redemption mechanism) to meet these liquidations. Both Terra’s collapse and 3AC’s a month later contributed significantly to the heavy discount. If you look at the chart below, there was not only a reduction in Lido deposits, but a decline across all liquid staking and staking pools as buying stETH at 0.93-0.98 made more sense than depositing new ETH at a 1:1 ratio. All staking deposits had the same duration & liquidity risk, so the only reasons to deposit ETH were if you wanted to solo stake or not take on smart contract or Lido-specific risks with stETH.

Second, the Merge was the much more important de-risking event on the staking withdrawals timeline. While there was another lull around the FTX collapse 2 months after the Merge (again due to forced selling from a large hedge fund), deposits have been trending up post-Merge and throughout 2023 as we approach Shanghai.

We can use this historical deposit flow to model out some potential scenarios on total staked ETH supply. While we expect the rate of inflows to be > outflows for the next couple years, it will most likely be reversed for the first month or so after Shanghai. Why? The exits will be front-loaded. If 10% of the stake wants to withdraw post-Shanghai, then it will take ~32 days for them to exit and require deposits of 57.6k ETH per day to offset, a rate that deposits didn’t even hit during the peak month of March 2022. As for how we came up with 10%, we first need to look at stake distribution by entity.

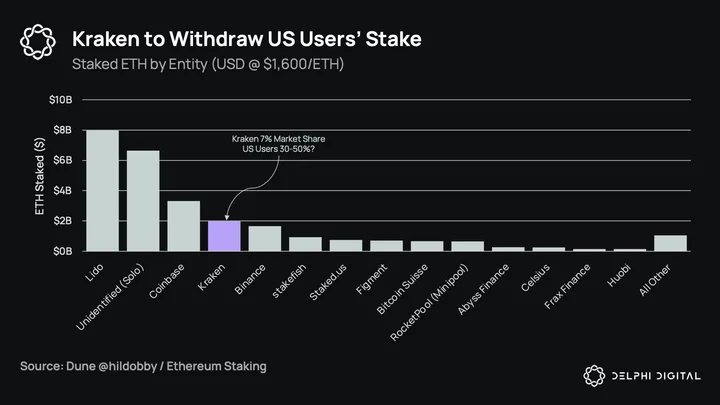

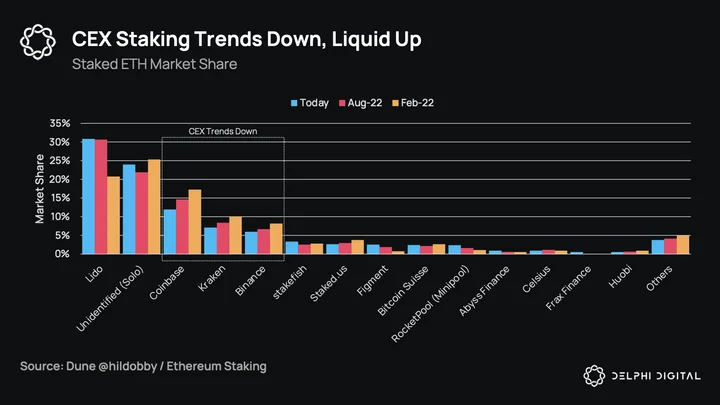

Breaking down stake distribution by entity tells us a few things. First, Lido is massive. Second, solo stakers make up ~1/4 of the total, with CEXs, liquid staking and staking pools ~3/4. Third, Kraken’s forced withdrawals for US users (thanks Gary) make up ~3.5%. Our base case of 10% withdrawals is broken down as follows:

-

3.5%: Kraken US users’ stake will be automatically withdrawn (estimate 50% of Kraken’s total stake).

-

2.5%: Conservatively expecting ~10% of solo stakers to exit. We feel that some of these will not want to continue dealing with the maintenance of running a validator and also prefer the mobility that liquid staking provides. These are predominantly early depositors who would have been taking advantage of a much higher APR in early days, so they were not necessarily validating for altruistic reasons.

-

1.0%: Celsius, who needs the ETH for bankruptcy proceedings.

-

3.0%: Mix of staking pools, liquid staking, and CEXs. While these buckets make up 75% of stake, there is unlikely to be a large amount of “real” withdrawals here, as any withdrawals from staking pools, liquid staking tokens, or CEXs will likely just be shifted into competitors. The liquid staking race is the #1 thing to watch post-Shanghai.

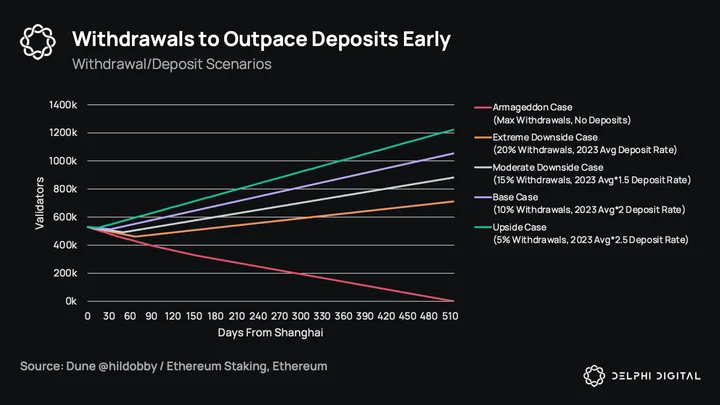

We’ve modeled some scenarios in the chart below to better illustrate this.

-

Armageddon Case: Max daily withdrawals with no deposits. This is not a possible scenario (barring the end of the world, I guess?), and is only used to illustrate the time to exit the entire validator set.

-

Extreme Downside Case: 20% of validators exit. Deposits stay at their 2023 average deposit rate of 560 validators per day. Highly unlikely.

-

Moderate Downside Case: 15% of validators exit. Deposit rate is 2023 avg * 1.5 (= 840 validators/day).

-

Base Case: 10% of validators exit. Deposit rate is 2023 avg * 2 (= 1,120 validators/day).

-

Upside Case: 5% of validators exit. Deposit rate is 2023 avg * 2.5 (= 1,400 validators/day).

Note that once the early front-loaded withdrawals are done, there will be some % exiting per day in perpetuity. To keep this simple, we assumed the deposit rate as the net inflow/outflow rate after the early withdrawals are done.

While impossible to predict, we believe something that looks like our base case makes sense, as this would give us 25-30% of supply staked by 2025 and lines up with other estimates. Obviously, there is some “nice round number” effect to the 10% base estimate. The reader should not get too hung up on the exact number, and note that it won’t look exactly as uniform as above (as there is likely to be some volatility shortly after Shanghai due to exits and deposits that have been waiting).

With that being said, it’s hard to see any substantial downside of “real” (i.e., not re-deposited into other staking categories) withdrawals more than 15%. First, the largest liquid staking token stETH is already trading back to par. If stETH was still trading around 0.95, we would expect a heavier amount of withdrawals. But since there is no arb to close, this seems much less likely. Second, while we could see the pending withdrawals grow shortly after Shanghai, it’s likely that a large % of these will just be shifted into other staking sources as noted above, having no real net-effect. The risk to the deposit rate is also to the upside, as Shanghai will have been completely de-risked.

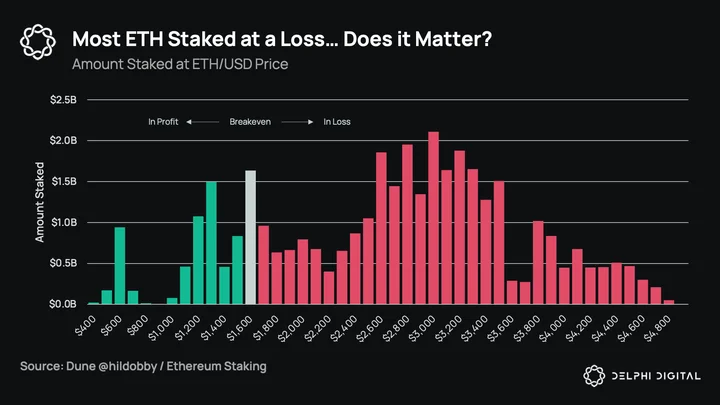

Predicting flows is tough, and something we have seen floated around is the behavioral economics angle of the cost basis of deposited ETH. First, we question if this even matters. Second, we split by category and consider the practical differences between them.

Cost Basis of Staked ETH

Does the cost basis of ETH deposits matter? The theory goes something like this: most staking deposits are underwater, therefore people will withdraw and cut their losses. But is it that simple? We could have a behavioral economics debate around emotional biases like loss-aversion and argue that stakers at a loss are actually more likely to hold, but we’d rather spend time breaking down the cost basis of the actual staking categories and show why this analysis does not matter in any practical sense regardless.

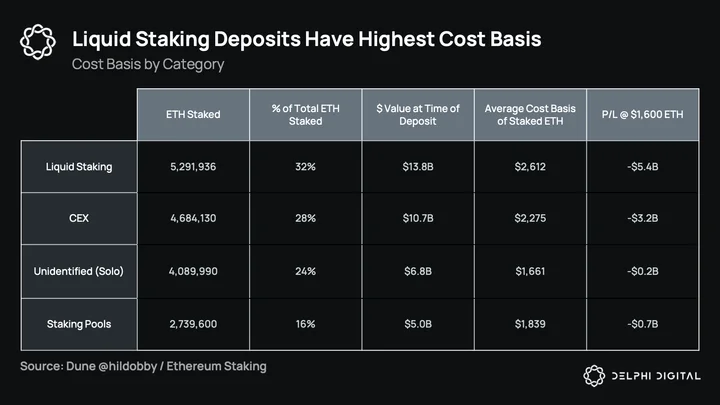

It’s important to remember that there are 4 main categories of staking: liquid staking (32%), CEXs (28%), solo (24%), and staking pools (16%). The two buckets with the highest cost basis which make up 60% of the supply are liquid staking and CEXs. This is important because the cost basis of staked ETH for these is largely irrelevant. Liquid staking tokens trade on the open market, so the “real” cost basis of people who hold them is constantly changing. If someone wanted to sell at a loss, they could have already, and at a price close to par.

For CEXs, some have their own “ETH2” markets, and Coinbase (the largest CEX staker) has converted ~1.1M/2.1M (~53%) into their LST cbETH. cbETH, while it did trade at a 6% discount at the end of the year, now trades 1-2% from par. Binance’s BETH is in a similar boat, and while not an LST, does trade on Binance (0.986/ETH at time of writing). We touched on Kraken’s dynamics before.

Solo stakers, as we’ve highlighted, could exit due to the length of time they’ve been validating, and early stakers will have accrued the most rewards at the lowest cost basis. The most important trend to monitor post-Shanghai is the mix. Decentralized LSTs make up 32% of staked ETH today. What will it be a year after withdrawals?

Liquid Staking Implications

First off, if you haven’t read it yet, I would recommend our ETH Liquid Staking report from January for a deeper dive than this section will entail.

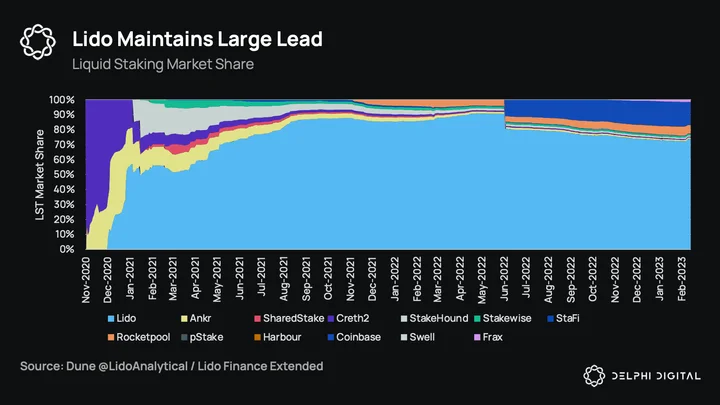

The most notable change in staking distribution over the past year has been the continued increase of market share from Lido, the declining share of CEXs, and recent growth from pools like Stakefish, Figment, and LSTs like RocketPool and Frax. Kraken’s 7% market share is an open question; will the stake of US users flow to Coinbase or LSTs? This is ~$1B of stake if our assumption of Kraken’s geographic distribution is correct.

If our hypothesis that solo staking and CEX staking will decline becomes validated, then the chart below will be the one to watch. While RocketPool (+11.3% 30-day growth) and Frax (+29.3% 30-day growth) have seen strong momentum lately, the reality is that they still pale in comparison to Lido. Lido has 77% of the LST market, and with Coinbase’s cbETH placing second with 16%, this leaves just 7% for the other decentralized LSTs outside of Lido. RocketPool will be making it easy for solo stakers to migrate after Shanghai, and Frax continues to offer the highest APR due to their Convex & Curve voting power. But liquidity trumps all, and LSTs become more useful the larger they get, something Lido’s stETH benefits the most from.

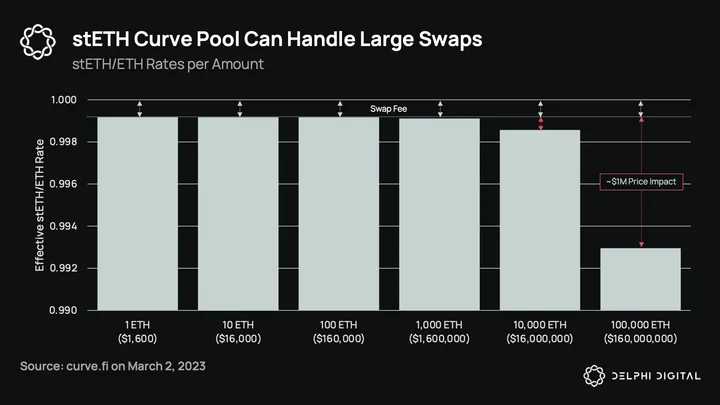

So, for the purposes of Shanghai, our LST question is rather simple: will there be large withdrawals from stETH? While other LSTs can certainly continue to gain share from deposits, the only way to seriously challenge Lido would be via large stETH redemptions. As we touched on earlier, stETH traded down as low as 0.93 during the summer of 2022, and even more recently after FTX. But in 2023, it’s closed the gap, and stETH now trades around par, highlighting that there will be no arb to close when withdrawals open.

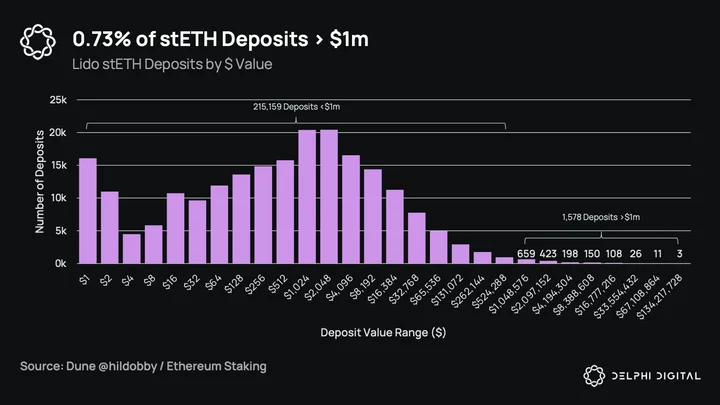

To illustrate this further, we can look at the actual cost to exit stETH positions. Anyone who holds $1M or less stETH can exit with an immaterial price impact, an effective rate of >0.999. Even for swaps of 10k ETH ($16M), holders can still exit for a few bps. It is not until we get to larger, 6-figure ETH/9-figure USD swaps that the impact becomes material. If any large redemptions were to happen, they would most likely come from this group. The only reason I can think of why a smaller user would wait to redeem instead of swapping today at par is potential tax considerations on redeeming vs. swapping, although it is not clear if there is even a distinction here for tax purposes anyway (not tax advice, not a tax lawyer, etc.).

So, how many stETH deposits were of this size? Less than 10. While deposits will not map 1:1 to current holdings, it is close enough for our purposes. The biggest wildcard is if someone wants to create a narrative around an LST competitor, buying up an LST governance token before withdrawing stETH and depositing to said competitor. There is of course no way to know if this is being considered or in what magnitude, but it is something to watch. If we see some large stETH redemptions early on, rumors will start to swirl. One side will be warning of large ETH spot selling while others will speculate on where the ETH will be deposited to.

1-2 months post-Shanghai, we’ll have a better idea of any imminent LST landscape shakeup, and then we can start to consider longer-term implications such as:

-

stETH on L2s is ~2% of stETH’s supply, how much will this increase by?

-

Coinbase is launching their own L2. Is part of the strategy here to get cbETH more adoption, starting with integrations on Base before expanding to others?

-

Does stETH or another LST become the preferred pair in AMM pools over WETH? While WETH is lower risk, it does not generate any yield. WETH will, of course, always be the most liquid, but we could see more pools opt for LST pairs instead.

-

If stETH ends up with a monopoly on LSTs, does it make it too big to fail? If you think about an LST, one of the main purposes is to increase leverage in the ecosystem. A bug in stETH would be catastrophic to Ethereum DeFi, and if large enough could require a chain fork.

-

Re-staking through Eigenlayer? We already know Eigenlayer will be accepting LSTs for collateral, but how many opportunities will actually arise, and who will be the first to create a standardized/whitelisted Eigenlayer LST?

Outside of longer-term impacts to LSTs, Shanghai brings changes to Ethereum’s ecosystem in and of itself.

Structural Longer-Term Impacts

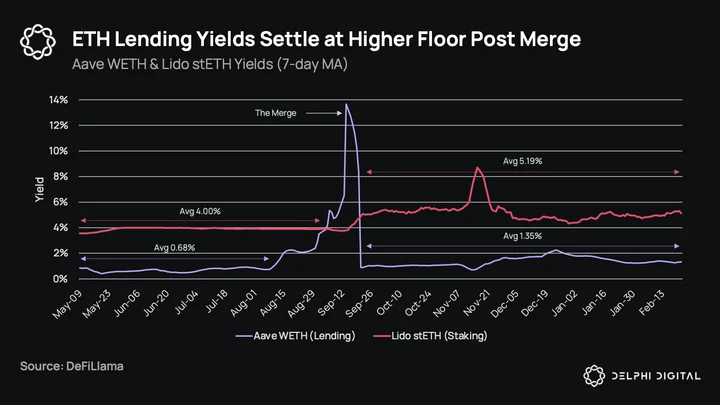

A post-Merge, post-Shanghai PoS Ethereum looks a lot different than what we’ve been used to over the years. The main difference, which has broad implications throughout DeFi, is a higher base yield on lending ETH and by extension a perpetually higher hurdle rate for participating in Ethereum DeFi. If you think of the ETH yield as the Ethereum economy’s risk-free rate, it’s now been permanently adjusted higher. In the PoW days, lending ETH generated almost no yield, but the calculus shifts with PoS. Especially now that LSTs will have less peg risk, we’ll see the leveraged stETH trade (deposit stETH, borrow ETH, swap to stETH, deposit stETH) increase. This will lift up base yields on ETH throughout DeFi, requiring other, riskier strategies to offer even higher yields to compensate. This is a long-term change to DeFi dynamics that will not reverse. The other effect from this is that an increase in the LST leveraged trade strategy increases systemic risks to DeFi for reasons mentioned in the last section.

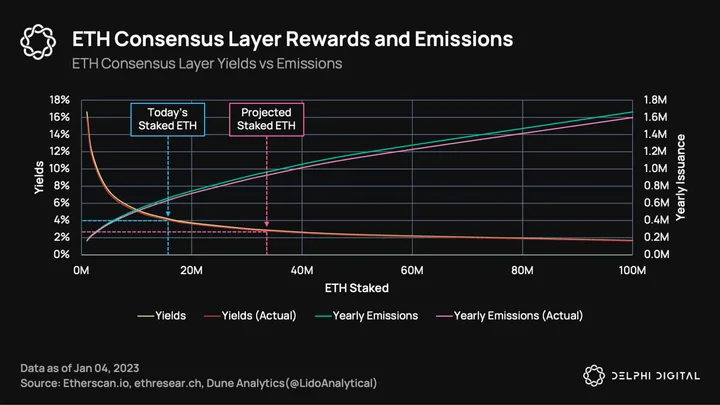

The other main change is what has been the general theme of this report: a higher long-term staking rate. As the amount of ETH staked rises, the amount of ETH issued increases, albeit at a declining rate. ETH staking rewards are split between the consensus layer (CL) and execution layer (EL). CL rewards are currently 4%, but if our projections on staked ETH hold true, will decline to ~2% over the coming years.

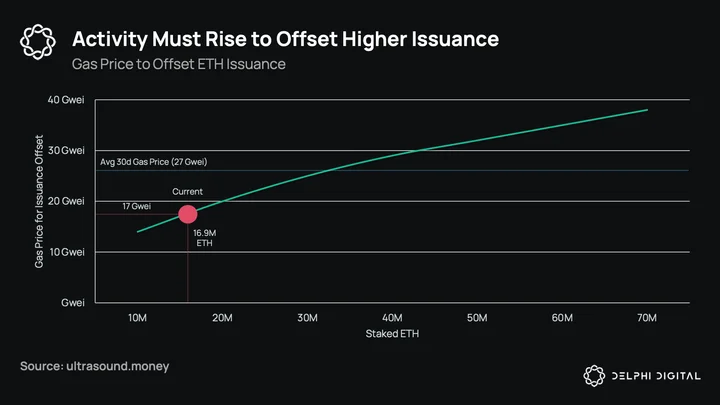

The main impact here, outside of a lower staking yield, is that it increases the floor gas price that the Ethereum L1 needs to sustain to have a net reduction in supply (i.e., the Ultrasound Money meme). At today’s 15% staking ratio, Ethereum needs to sustain a 17 gwei gas price to be deflationary. As we get higher, this approaches 30+, although since issuance increases at a declining rate, so does the gas price to offset.

I would argue that whether or not ETH is deflationary is not too relevant (it’s just diluting non-stakers), but the deflation/Ultrasound Money meme can be powerful, so people will want to see a deflationary ETH regardless.

Shanghai Is Coming

So, where does this leave us? Will Shanghai be a non-event? While we are excited to see Shanghai officially transition Ethereum into its PoS future, we wouldn’t be too surprised if there were fireworks around the event. The partial withdrawals are significant when compared to current market conditions, and there is no way to tell how much capital is on the sidelines waiting for a post-Shanghai world to enter. Bears would focus on the billions in potential unlocks and say it’s too much for the market to absorb. Bulls would say it’s priced in and point to ETHBTC trading down 3.3% YTD while the rest of the market has outperformed. Whatever side you’re on, know the dynamics at play.

Brace yourselves, Shanghai is coming.

Special thanks to Jose Villacrez for designing the cover image for this report and to Can Gurel and Brian McRae for editing.

0 Comments