BTC Calls, Upcoming NFT Mints, & The Frax Expansion

MAR 10, 2022 • 7 Min Read

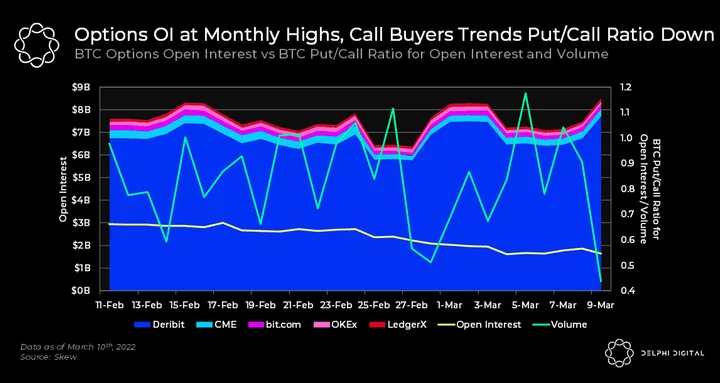

Chart of The Day: BTC Call Buyers Start Piling In

- The put/call ratio for BTC open interest hit a 6-month high of 0.69 in Feb. 2022, as bearish market sentiments sent traders to buy puts. Since that peak, however, it has started to fall sharply to 0.55.

- Yesterday, the volume-adjusted put/call ratio hit its monthly lows of 0.44, as the volume for calls spiked. Deribit traders were buying up Apr. 29 BTC calls for $42k, $50k, and $60k strikes. This boosted the notional value for Apr. 29 calls up to $193M on Deribit.

- This might indicate that traders are turning bullish, even in an uncertain macro environment. All eyes will be on the CPI release today as economists predict inflation to rise to 7.8%.

- Delphi members can see our latest Monthly Chartbook for more macro coverage.

Solana NFTs & Magic Eden

Solana NFTs & Magic Eden Report

[Excerpt from our Mar. 9 NFT Insights]

- Please note that this is purely for informational purposes only. This is not investment advice and does not represent an endorsement of any particular project. Minting of new projects is high-risk. The projects chosen below are subjective and determined by the author based on ones they find most interesting, have sparked early interest from other NFT participants, and are ones the author would mint themselves (though we do stress to DYOR given the risk associated with any new NFT drop).

- SoundMint Vinyls is the membership token for SoundMint, a generative music platform. Music NFTs are a niche but growing sub-sector of NFTs. Holders will receive benefits including platform earnings, exclusive partnerships/merchandise and priority access to SoundMint shows. The mint is open to WE ARE KLOUD NFT holders. There are 3 rarity tiers to the collection: Mint, Gold & Onyx, available depending on how many WE ARE KLOUD NFTs you hold. Notably, since the announcement of SoundMint Vinyls yesterday, the average price for WE ARE KLOUD NFTs has nearly doubled from ~0.10E to 0.20E.

- GNSS (Generative Nature Synthetic Species) is a generative art project by MGXS, a well-known generative artist that creates robot art and works with RTFKT studios. It will be a fully public sale with no whitelist. Your seeds can be burnt to generate 1 NFT; you will have 10 chances to accept or pass & generate a new one. Rarities will thus be determined by the collective decisions of the community.

- Kibatsu Mecha is a collection of fun hand-generated, animated robot NFTs. This is the genesis collection based on the lore of Megacity Kibatsu, a world and story developed by US-based artist-animator Jerry Liu. There is no promised roadmap except that the team is dedicated to continue developing the Kibatsu brand. Allowlist is through giveaways, contests & partnerships with other projects.

Kibatsu Mecha

- The Citadel is a strategy game set in space and inspired by Eve Online, an OG MMORPG. This game has been in development for months and is expected to launch in March with a fully playable game on mint as well as a library of community resources for builders and players (read the extensive whitepaper here). I like that the team has been heads-down building and growing the community organically. Whitelist allocations are awarded selectively. (Genesis Citizen role on discord)

- Everai is an anime-style, hero-based universe in development since August 2021. It is developed by Screenshot Labs, comprising of a team of engineers and artists developing web3 experiences. They have collaborated with creators like Mehdi Aouichaoui (lead animator, works include One Piece, Star Wars Vision) & Quentin Pointillart (video game artistic director previously working with Square Enix). Game of Blocks holders can get on the mintlist.

- For more, Delphi members can see our latest NFT Insights here.

Frax Controls Its Stack

Frax Controls Its Stack Report

[Excerpt from a Delphi Pro Report]

- FRAX is a hybrid algorithmic stablecoin whose model is similar to that of UST. However, while UST is now 7.5% backed by exogenous collateral (i.e. BTC), FRAX is 84.5% directly backed by exogenous collateral, making it less reliant on the algorithmic component. This model is in contrast to an overcollateralized stablecoin such as DAI, whose CR ranges from 101-175%. Importantly, FRAX’s collateralization ratio is not static, but rather increases or decreases based on demand for the stablecoin

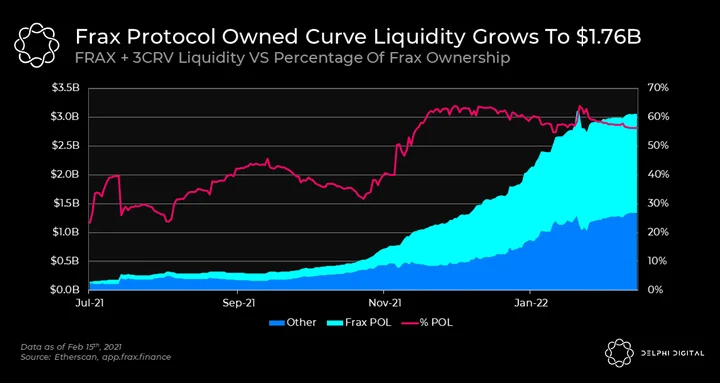

- FRAX + 3CRV has amassed a large liquidity pool on Curve worth nearly $3B. This does a few things. First and foremost, this makes FRAX extremely liquid on-chain and has contributed to a rock-solid peg. Given its amplification parameter, this Curve pool can absorb hundreds of millions in selling pressure without pushing FRAX off its peg. Secondly, since ~58% of this liquidity is owned by the protocol, it allows FRAX to run one of the most profitable farming operations in all of crypto from CRV and CVX emissions. Thirdly, it gives FRAX unique flexibility to run its Curve AMO strategy, which will be explained below.

- The Curve AMO consists of three main stages:

-

De-collateralize: The market is pricing FRAX >$1, signaling heightened demand. This allows FRAX to lower its CR. The protocol places idle collateral and newly minted protocol-owned FRAX into the FRAX + 3CRV pool.

- Re-collateralize: The market is pricing FRAX <= $0.99, signaling less demand. This causes FRAX to increase its CR. The protocol withdraws excess FRAX from the pool first and burns it, then withdraws USDC to increase FRAX’s CR.

-

Market Operations: The pool is balanced and accrues transaction fees, in addition to CRV + CVX rewards by placing the LP shares in Convex.

- In order to help understand how this Curve AMO collateralizes FRAX, let’s break down some supply expansion / contraction scenarios in a bit more depth. The Curve AMO holds $1.765B (875M FRAX + 890M 3CRV), which counts as collateral towards the overall FRAX supply. Given that $875m of the AMO is in FRAX, this naturally raises the question – “how does FRAX collateralize FRAX?”. Is this some type of collateral inception?

- Well, if you think about how that 875M FRAX enters the circulating supply, you’ll realize that users would first need to swap 3CRV for FRAX at 1:1 rate. This action automatically collateralizes the FRAX entering circulation and, if repeated, pushes the balance of 3CRV higher. Once the amount of 3CRV is greater than the amount of FRAX in the pool, the price of FRAX moves above $1. With FRAX trading above $1, the Curve AMO can mint additional protocol owned FRAX into the pool benefiting from seigniorage. This is the expansionary or “de-collateralize” stage.

- What about if users are instead swapping FRAX to 3CRV? By doing this you are again swapping 3CRV to FRAX at a 1:1 rate, essentially removing FRAX from circulation. You lower the FRAX supply on the open market by selling it back into the pool, causing the protocol to lose access to the 3CRV collateral that comes out as a result. If enough FRAX is sold back to the Curve pool, to the point where its price breaks down to $0.99 or lower, then the Curve AMO enters the “re-collateralize” stage. In essence, Frax has integrated its stability model into a Curve pool, providing it deep on-chain liquidity while also farming CRV and CVX emissions at the same time!

- To learn more about Frax, Delphi Pro members can read the full report here.

Notable Tweets

Optimism Introduces Cannon

Cannon (CANNON CANNON CANNON) is our next-gen fault proof architecture, and it’s coming soon.

It enables optimal data costs.

It effortlessly preserves EVM equivalence.

Its very first bug bounty goes live today. 💥

— Optimism 🔴✨@optimismPBC) March 10, 2022

Thread on Data Availability

1/ 🧵

How and why “data availability (DA)” became the sexiest topic in #Ethereum land, the #l222 space, and for #rollups— MT (@mt_1466) March 8, 2022

Pro-Crypto President for South Korea

ICYMI: Yoon Suk-yeol, who pledged to deregulate South Korea’s crypto sector, wins presidential election

— The Block (@TheBlock__) March 10, 2022

0 Comments