BTC Pain, UST Turbulence, & Intro to Token Sinks

MAY 11, 2022 • 7 Min Read

Chart of The Day: BTC Holders Extend Losses

- Note: Glassnode separates BTC holders into two classifications. Short-Term Holders (STHs) of BTC have held BTC in their wallets for less than 155 days. Long-Term Holders (LTHs) have held BTC in their wallets for more than 155 days.

- BTC has extended its move downwards to retest 30k as macro uncertainties continue to exert pressure on prices. BTC holders are beginning to feel the pain as combined STH and LTH losses are at 44%, which hasn’t been recorded since 2020.

- LTHs continue to accumulate BTC, absorbing 13.56M of supply–the highest it has ever been despite 31% of LTHs experiencing losses.

- The price of BTC also fell below $30.7k, which was the average price of MicroStrategy’s BTC purchase. MicroStrategy says it will only be at risk of liquidation if BTC is at $3,562.

Flash Update: Macro, Crypto, & Terra

[Excerpt from May. 10th Flash Updates]

- Souring sentiment and worsening macro headwinds have exacerbated the selloff in equity markets, with the S&P 500 now trading at its lowest level in over a year. Analysts are slashing price targets at their fastest pace in two years as many past high-flying growth stocks find themselves 30-40% off their highs. Gone is the supportive backdrop of the 2010s that propelled asset prices to new heights, instead replaced by surging consumer costs and deteriorating financial conditions.

- Consumers and investors alike are facing the highest CPI prints in 40 years. The proliferation of higher consumer prices has made its way into everyday conversation, which has narrowed the Fed’s fight to just one enemy above all: inflation. And their latest rhetoric implies little will stand in their way to stop it. Early rate hikes have not yet had an effect on inflation, though they will once demand really starts to slow. The narrative of a vibrant and growing economy still exists – at least to some degree – if you look at labor shortages alone. In reality, rumors of layoffs have started to circulate while corporate earnings have started to disappoint. Asset prices are starting to come to terms with this new reality. Liquidity concerns still exist, which is another risk the Fed’s balance sheet roll off won’t help with.

- The last several weeks have seen these shifts manifest themselves in equity prices. Many tech stocks are down 70%+, with the S&P 500 Index off 18% from its peak. The SPX has printed fresh lows on the year as investors come to terms with this unwind. The next obvious macro structure support is likely 3250-3400 should SPX lose 4000; another leg lower to the top of that range would imply a ~30% drawdown from its early January peak.

Luna, UST, and Anchor

- This report is being written in real-time so the numbers used are meant to be as accurate as possible while being delivered in a timely manner. Please excuse any discrepancies.

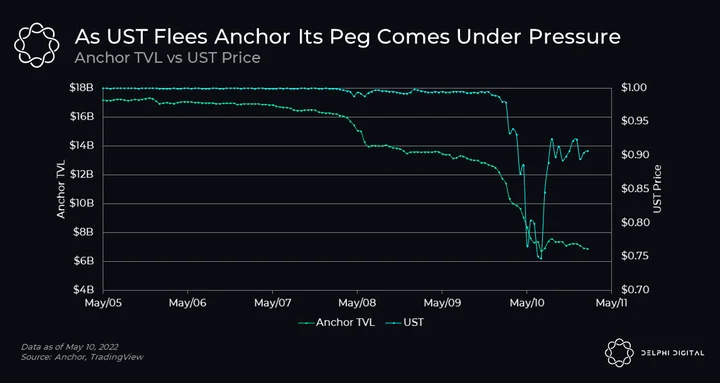

- With an unflattering macro and crypto backdrop, UST started fleeing Anchor on May 7th shedding nearly $2.3B in deposits within 48 hours. With the reasonable assumption that UST leaving Anchor is entirely exiting the Terra ecosystem this is quite a lot of sell pressure to absorb. These events lead to the UST peg beginning to break down, hovering around 99 cents.

- On May 9th the situation accelerated rapidly with an additional ~$5B worth of UST leaving Anchor. UST looking to exit the system has 3 main options:

- Use the native LUNA burn/mint mechanism to redeem 1 UST for $1 worth of LUNA (more on this later).

- Using decentralized exchange liquidity the largest source being Curve which had ~$550M worth of 3CRV to be used as exit liquidity.

- Selling UST on centralized exchanges with the main markets being Binance and FTX.

- With ~$550M worth of liquidity on Curve, LFG having ~$2B worth of reserves and the native mint/burn mechanism only being able to handle ~$300M a day in redemptions this still leaves billions of UST that potentially wanted to exit the system unaccounted for. This caused a pretty drastic break in the UST peg wicking down to as low as 61 cents on Binance.

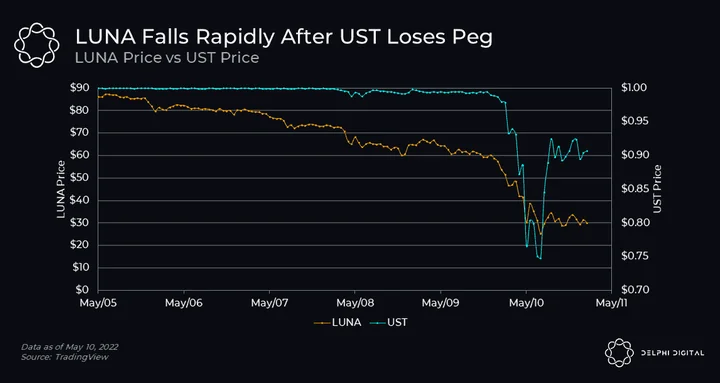

- The UST peg breakdown caused a massive sell-off in LUNA from both speculators worried about the entire system and structural selling from LUNA’s natural mint/burn mechanism.

- For those who aren’t familiar, when UST is trading > $1 then you can use $1 worth of LUNA to mint 1 UST, thus increasing UST supply and capturing an arbitrage opportunity (by selling the newly minted UST above $1). Similarly when UST is trading < $1 you can use 1 UST to mint $1 worth of LUNA, increasing the LUNA supply and capturing an arbitrage (by selling the newly minted LUNA).

- This is how the mechanism works in theory and during normal market conditions. In reality and during non-normal conditions, this system can only handle a certain amount of volume. Let’s break down the actual mechanism behind the scenes:

- The mint/burn mechanism is expressed through a virtual automated market maker (vAMM) that simulates $50M worth of stablecoin liquidity and $50M worth of LUNA liquidity in a standard X*Y=K pool. During normal market conditions and when the pool is balanced 50/50, users should be able to execute their LUNA/UST minting and burning at very close to the 1 UST for $1 worth of LUNA rate described earlier. But during a depegging event, there is a significant amount of flow in one direction, redeeming UST (worth less than $1) for $1 worth of LUNA. This flow drains LUNA from the vAMM and arbitragers need to wait for liquidity to refill in order to continue. Over time the vAMM replenishes its reserves pushing the pool towards equilibrium at a fixed rate known as the recovery period, currently 36 blocks (3.6 minutes). The base amount of liquidity in the vAMM and recovery period acts as a natural limit to the amount of burning/minting that can happen in a short period of time. Jump Trading discusses the pool in more depth in this governance post, where they estimate the capacity of the pool to be ~$300M per day with acceptable slippage. You can monitor this vAMM here to watch the arbitrage happening in real time.

- A depeg of this depth and length is unprecedented for UST so it is difficult to know what will happen. We do know that as long as UST trades off its peg there will be continued minting and forced selling of LUNA by arbitrageurs. At the time of publishing, a UST dollar is at $0.72 and LUNA has fallen 93.4% in the past 24 hours to $1.03.

- For more, Delphi members can see the full Delphi Report here.

STEPN Sprinting Away

[Excerpt from a Delphi Pro Report]

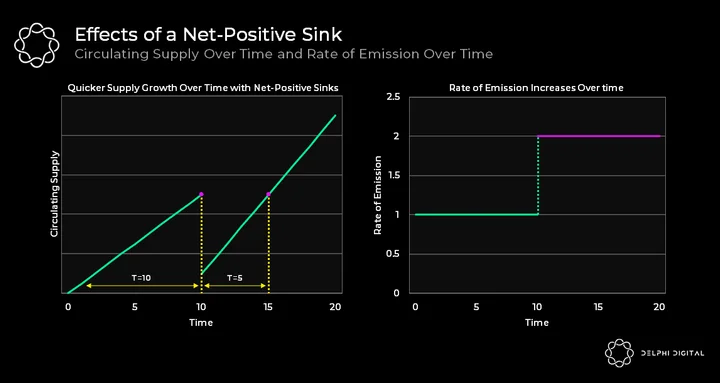

- Sinks have a crucial role in game economy design as a means to remove excess resources, or currencies, from the economy. However, if the sink eventually leads to more emissions in the long run, it eventually leads to an even more inflationary scenario for the resource/token.

- To move towards a more granular definition of sinks, we introduce a novel concept in game economy design – which has become a particularly relevant topic to the long-term success of play-to-earn and play-and-earn economies.

- A net-positive sink is a sink that reduces a resource’s circulating supply while increasing the currency’s rate of emission. The name “net-positive sink” comes from the fact it has a net-positive effect on the emission rate of the resource, implying an increase in inflationary pressure on the currency. These sinks may not achieve the goal of a sink in the long run, which is to help balance any inflationary pressure on a currency.

- For more, Delphi members can see the full Delphi Report here.

Notable Tweets

Blockchain Gaming Deal Value Hits $1.6B

— Blockchain-powered gaming again shows impressive YoY growth metrics: the total number of deals was up 11x YoY, while the total deal value was even stronger at 19.4x YoY ($1.6B vs. $83m); 50% of all Private Investments deal value deployed in Q1’22 associated with Blockchain.

—InvestGame (@InvestGameNet) May 11, 2022

LFG $1B Financing Fell Through

The Block Larry Cermak says LFG’s $1 billion financing plan has failed. He previously said that Terra aims to raise $1-1.5 billion to “save” UST. Jump, Celsius and Jane St. have committed (about $700 million), but Alameda has not.

—Wu Blockchain (@WuBlockchain) May 11, 2022

Napster Acquired by Hivemind and Algorand

ICYMI: Napster acquired by Hivemind, Algorand at undisclosed price

—The Block(@TheBlock__) May 11, 2022

0 Comments