🌅 Welcome!

Bloomberg reports that FTX customers have a slim chance of recovering balances. Elsewhere, Binance creates a recovery fund to help strong projects facing liquidity issues.

Today, we compare the performance of CEX tokens with DEX tokens, and our Research team shares some insights in the aftermath of FTX’s downfall.

This is the Delphi Daily. Let’s dive in.

🚨 In Case You Missed It

- Binance creates a recovery fund to help strong projects facing a liquidity crisis.

- Bloomberg says FTX customers have a slim chance of recovering much of their deposits.

- Crypto.com accidentally sends 320K ETH to Gate.io. Crypto.com CEO says all funds were returned by Gate.io.

- Chiliz announces that 38M CHZ will be used to compensate FTX users that owned CHZ on the platform.

- Curve (fintech company, not the DEX) is in discussions to acquire BlockFi’s credit card customers.

📊 DEX Tokens Outperform CEX Counterparts

- On Nov. 11, the FTX Group of companies filed for Chapter 11 bankruptcy. This included FTX.com, FTX US, Alameda Research, and other affiliated companies.

- Alameda Research, the group’s trading firm, allegedly collateralized illiquid assets in exchange for customer funds deposited on FTX. Ultimately, this led to the group’s downfall.

- These revelations prompted growing concerns about the solvency of other centralized exchanges (CEX), which soon began to see mass withdrawals. The highest net outflows were seen from FTX, OKX, and Bitfinex.

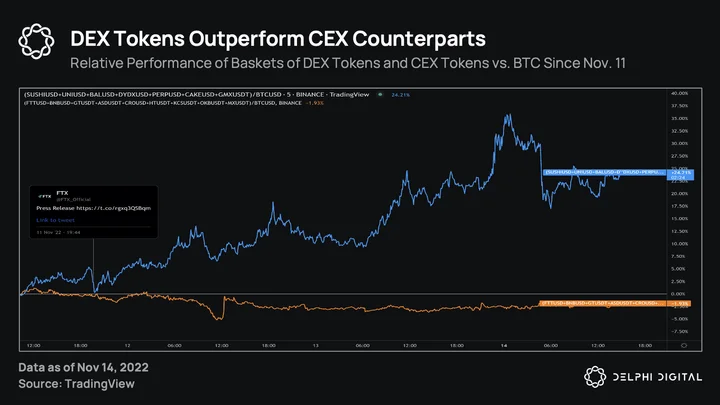

- Tokens issued by CEXs clearly depict these solvency concerns with a stark underperformance over tokens issued by decentralized exchanges (DEX).

- The chart above shows the price performance of a basket of CEX tokens vs. BTC and a basket of DEX tokens vs. BTC. Since the bankruptcy filing, the DEX basket is up 24% whereas the CEX basket is down 2%.

- As trust in centralized intermediaries has eroded, it stands to reason why the DEX basket has greatly outperformed its CEX counterpart.

- The CEX basket consists of FTT, BNB, GT, ASD, CRO, HT, KCS, OKB, and MX while the DEX basket consists of SUSHI, UNI, BAL, DYDX, PERP, CAKE, and GMX.

⚡The Aftermath of FTX’s Downfall

- This past week has been one of the worst we’ve seen in crypto. So much has happened in such a short period of time, it’s difficult to know where to start.

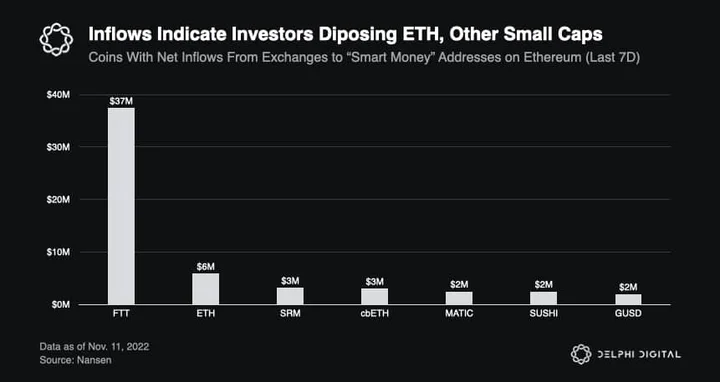

- According to Nansen’s Ethereum exchange flows dashboard, the top coins moving into exchanges from wallets labeled as “smart money” over the last week have been FTT, SRM, cbETH, MATIC, SUSHI, and GUSD. In FTT’s case, just 12 addresses contributed to $37M FTT moving into exchanges.

- The vast majority of FTT flows into exchanges came from addresses labeled as “market makers” on Nansen. Given FTX/Alameda’s alleged use of FTT as collateral, this is not entirely unexpected.

- Lenders trying to offload the FTT collateral may have engaged one of these market makers to dispose of these assets. However, FTX’s deployer address owns 60% of FTT’s total supply

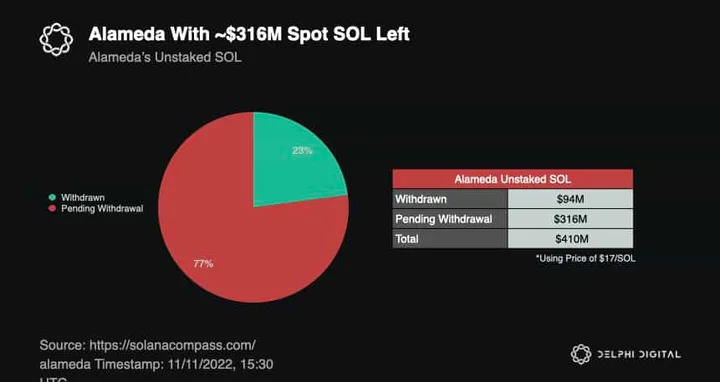

- From an ecosystem perspective, Solana will take the largest hit out of all of them. It’s no secret that FTX and Alameda were huge investors in Solana and thus have large spot SOL positions to liquidate, along with numerous other ecosystem tokens.

- As of the timestamp in the chart above, Alameda still has ~18.6M SOL ($316M) remaining, which was un-staked in epoch 370 (the “pending withdrawal” tokens are free to move now).

- Of course, it is unclear how much of this has already been effectively sold using perps, as at one point they were trading at a ~50% discount to spot ($7 perp vs. $13 spot) on some exchanges.

- The next direct fallout was with the “Solend Whale.” This was an infamous position in Solana DeFi, the largest single borrow of ~$50M USDC against SOL collateral, with a liquidation price of $21.

- With Alameda being one of the largest on-chain liquidity providers on Solana and the extreme price fluctuations in SOL from them needing to sell and accompanying panic, there was risk of a substantial amount of bad debt here.

- The liquidation process happens in chunks of 20%, and while it started off okay, it eventually became significantly undercollateralized as the price of SOL dropped to $12. To illustrate the challenge here, selling 500k SOL (~$9M) on-chain currently incurs 62% slippage.

- For more on the aftermath of FTX’s downfall, Delphi members can read our Delphi Pro report here.

🐣 Notable Tweets

Mark Cuban on Smart Contracts

A basic question. Why have I invested in crypto? Because I believe Smart Contracts will have a significant impact in creating valuable applications. I have said from day 1, the value of a token is derived from the applications that run on its platform and the utility they create

NFT Projects Affected by FTX Fallout

Spent some time digging into which NFT projects were significantly affected (or not) by the FTX blowup.

The findings have been both encouraging & sad

Here’s what I found so far:

0 Comments