DYDX Valuation Analysis & DEX Perps Comparison

JUL 24, 2023 • 40 Min Read

Introduction

Self-custody and censorship resistance are seldom the deciding factors for the average user selecting a crypto exchange. The collapse of FTX created a window of opportunity that DEXs have thus far failed to exploit.

Despite that, perpetual DEXs remain one of the products that have shown great product-market fit and continuous innovation in their designs. Moreover, this sector has an extremely good business model that can generate revenue. GMX and GLP alone led the real yield narrative by routing fees to token holders and liquidity providers (LPs). Outside of spot swaps, perpetual DEXs are also one of the easiest ways to eat into CeFi dominance.

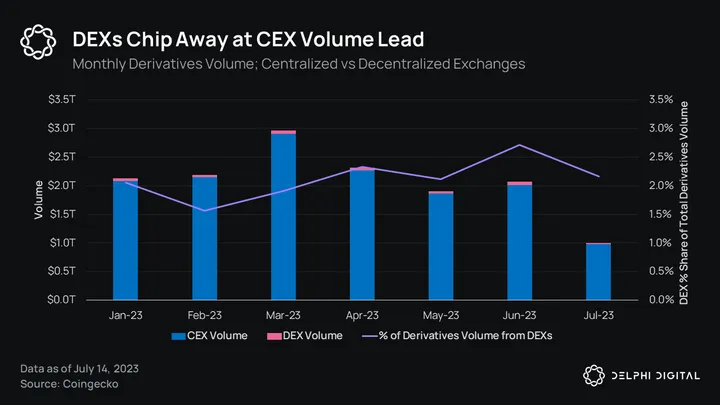

Decentralized exchanges are slowly chipping away at centralized exchange dominance. The graphic above shows that in six months, perpetual DEX volume share went from 2% to 2.1%, with total derivatives volume ranging from $2T to $3T. Perpetual DEXs now hold a tiny 2.1% volume share and have the potential to capture more from their CEX counterparts.

DeFi perps might have the most momentum of any crypto subsector at the moment. Several DEXs are simultaneously on the verge of major improvements that appear to put their offerings on par with CEXs. User experience, asset offerings, and even throughput are becoming areas of opportunity for DEXs.

We’ve identified four projects as favorites to lead the perpetuals space moving forward: dYdX, Synthetix, GMX, and Vertex. The first three are older projects going through another phase of evolution while Vertex is the new kid on the block boasting fresh protocol design.

GMX is moving from an index-esque liquidity pool design (v1) to a more siloed liquidity pool structure (v2) to enable more assets and liquidity. Synthetix is also introducing a fresh take to the way its liquidity backing is structured with v3. And dYdX v4 entails a complete architectural overhaul of how the protocol works to move all components of the exchange on-chain.

Overall, there are some exciting developments in the perpetuals and margin trading space since we last covered it. In this report, we will examine where these projects are, where they are going, and look at the perpetual DEX landscape as a whole.

Before we get into depth on how these protocols work, we will first go through the token economics and potential for value accrual for these projects.

Token Economics and Value Accrual

As a whole, perps have some of the strongest tokens in crypto. Perps tokens often exhibit straightforward value accrual alongside sustainable token utility. Technological advancements in perps should more quickly impact these tokens than those of broader DeFi.

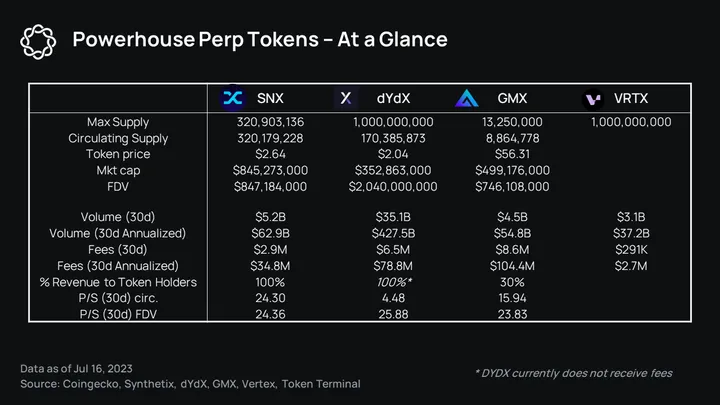

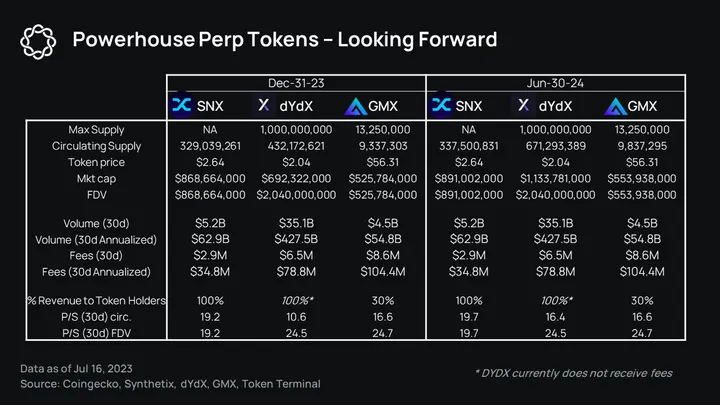

DYDX: The DYDX token has been an outlier to this trend. Since its launch in 2021, the market has relentlessly punished its low floating supply and lack of token utility. Despite having over 50% of the entire DEX perps market share for several years, dYdX has the lowest circulating market cap of the tokens mentioned here by a wide margin.

Currently, with dYdX v3, all trading revenue flows to dYdX Trading, Inc. The DYDX token has little use beyond governance and staking to earn discounts on fees and other platform perks. In dYdX v4, no single entity will be allocated trading revenue, and the dYdX token will be used to secure the dYdX chain with the potential for fee sharing.

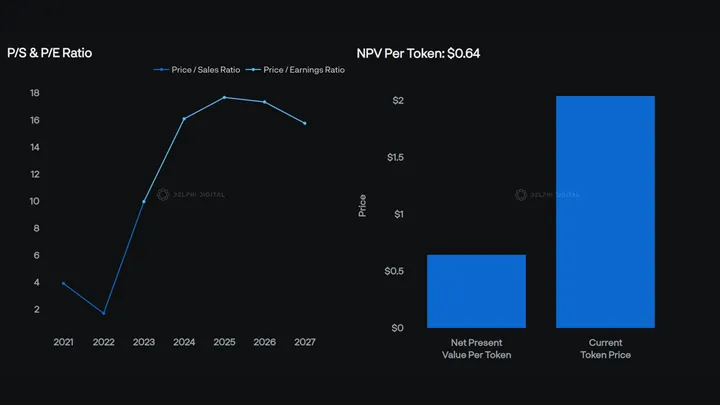

Once staking is live, trading fees will be distributed to validators and delegated stakers. The fee-sharing mechanism has yet to be decided on, but with DYDX’s low circulating float, it is trading at a 4.2x circulating P/S multiple. Assuming a 30-50% range of fee sharing, it will equate to a P/E ratio of 8.34 – 13.9.

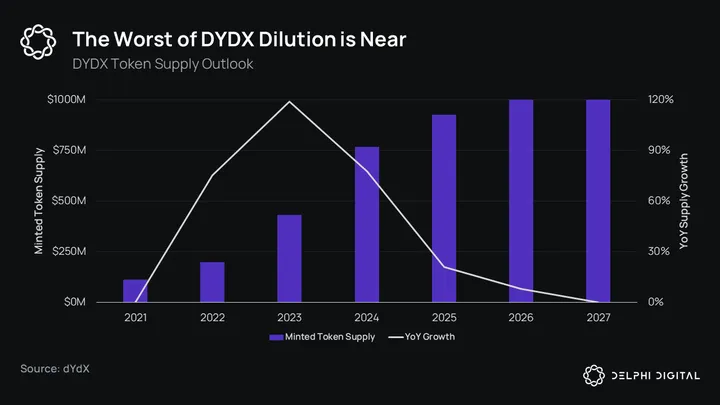

This is fantastic news for DYDX holders. After years of being an afterthought, DYDX will soon have competitive fundamentals with its peers. The other remaining problem is the deluge of ensuing token unlocks.

Employees, investors, and consultants were allocated 50% of the DYDX token supply altogether. 30% of these tokens were originally scheduled to be unlocked in January 2023, upon which vesting would begin. The 150M DYDX unlock was pushed back to December 2023, giving the dYdX token ample time following the v4 release to grow into its lofty valuation before the unlocks begin in December.

But this EOY unlock is still something to be cautious of. The unlock will increase total/circulating DYDX supply by 54%/80% overnight. When benchmarking from the total/circulating supply at the time of writing, DYDX supply will increase by 75%/95%.

GMX: GMX’s supply is difficult to project due to escrowed GMX. There is currently only ~600k GMX vesting across Arbitrum and Avalanche. There is a nominal amount of dilution by way of weekly GMX bonds as well. For this analysis, we took a conservative approach, assuming 60% of the esGMX supply reaches circulation by year-end 2024. This would result in ~2,740 GMX emissions per day, which is in line with the current rate.

SNX: On the surface, one of the more attractive aspects of SNX is the near parity of the circulating supply and total supply. SNX still utilizes a weekly inflation regimen that serves as a subsidy for SNX stakers. Stakers have separate pools of SNX rewards on Optimism and Ethereum, leading to different staking APRs.

SNX currently has the lowest inflation, with emissions based on their staking ratio.

Synthetix has successfully reduced SNX inflation over the past year, with emissions stabilizing at 325k per week for the time being. Per SCCP-211, SNX inflation is now dynamic based on the staking ratio adjusting up/down 5% in relation to the desired range of 60-70% staking ratio. This rate of emissions will continue until SNX v3 tokenomics are finalized by governance. SNX inflation rewards are subject to a one-year vesting period, which further reduces its impact on the token supply.

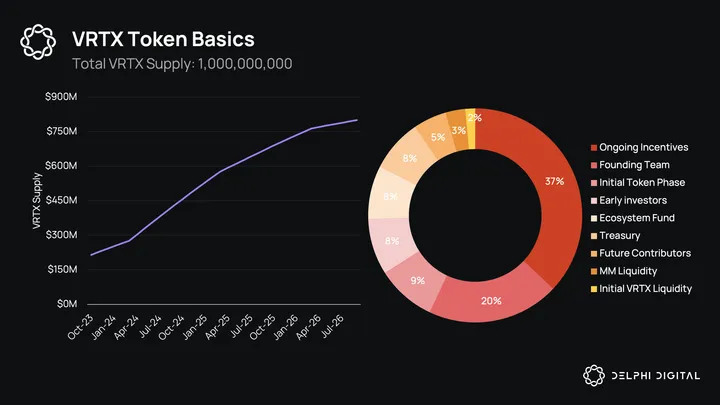

VRTX: Vertex’s native token, VRTX, will go live in October 2023. Despite being the youngest token, VRTX emissions appear reasonable and easy enough for users to navigate. Users will be able to stake the token for liquid xVRTX, which grants governance rights and a share of the protocol revenue and emissions. voVRTX, a non-transferrable token that boosts governance and rewards power, can be obtained by staking VRTX in the insurance fund or using VRTX for trading fees. Users are currently able to earn VRTX via trading rewards in epochs leading up to the release.

VRTX: Vertex’s native token, VRTX, will go live in October 2023. Despite being the youngest token, VRTX emissions appear reasonable and easy enough for users to navigate. Users will be able to stake the token for liquid xVRTX, which grants governance rights and a share of the protocol revenue and emissions. voVRTX, a non-transferrable token that boosts governance and rewards power, can be obtained by staking VRTX in the insurance fund or using VRTX for trading fees. Users are currently able to earn VRTX via trading rewards in epochs leading up to the release.

Exploring Future Value Accretion Potential

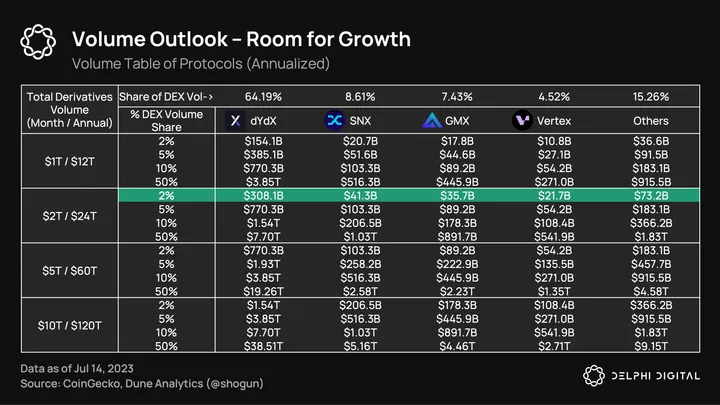

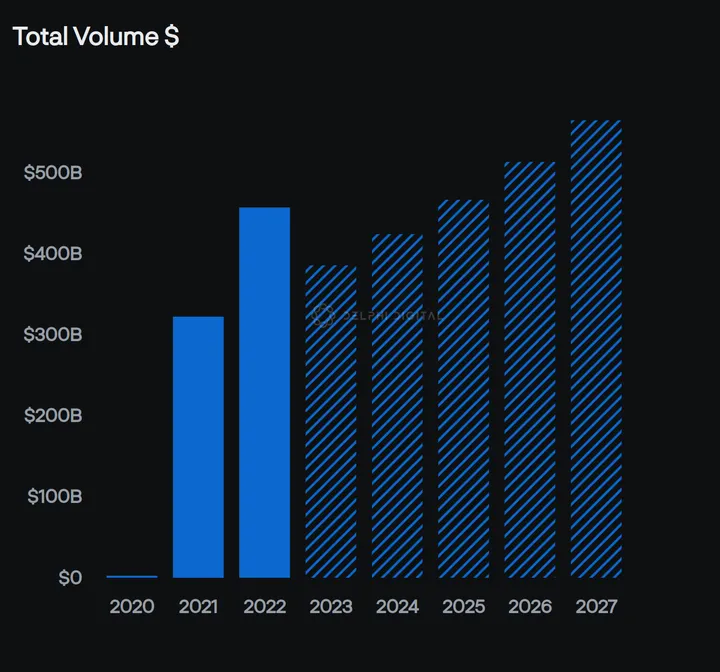

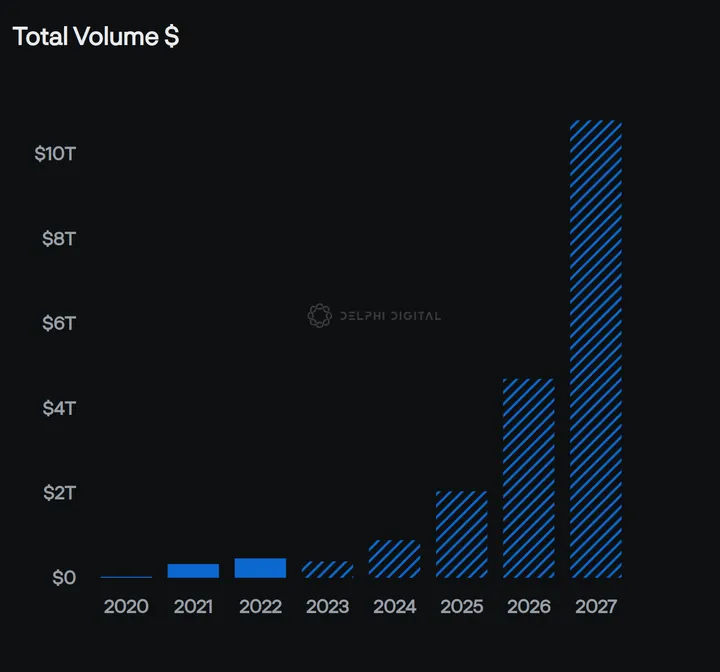

Given the current total monthly derivatives volume of roughly $2T, it could be relatively easy for perp DEXs as a whole to gain traction if broader market sentiment continues to rebound. Any DEX advancements on CEX territory would result in significant increases in volume. A 3% increase in DEX volume share will spur a $470B increase in volume for DEXs at current run rates.

Given the current total monthly derivatives volume of roughly $2T, it could be relatively easy for perp DEXs as a whole to gain traction if broader market sentiment continues to rebound. Any DEX advancements on CEX territory would result in significant increases in volume. A 3% increase in DEX volume share will spur a $470B increase in volume for DEXs at current run rates.

Note: dYdX and SNX fees are based on the average of maker and taker fees. GMX’s fees assume 50% v1 fees and 50% v2 fees, not including borrowing fees.

Note: dYdX and SNX fees are based on the average of maker and taker fees. GMX’s fees assume 50% v1 fees and 50% v2 fees, not including borrowing fees.

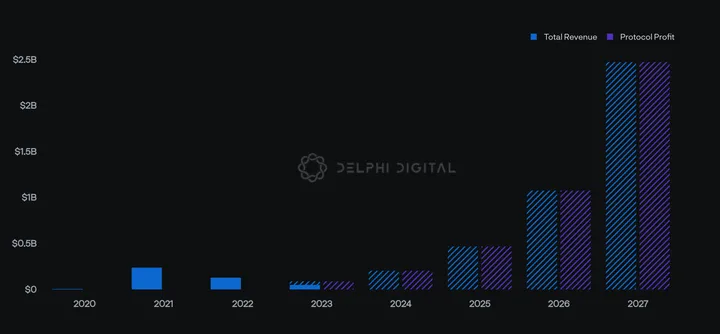

The different fees on each protocol ultimately affect the returns of their stakers. Due to GMX’s high fees, it generates 25% of dYdX’s fees despite only facilitating 12% of dYdX’s volume. However, dYdX could be in a position to profit significantly from fees if it maintains its large market share while total derivatives volume goes up. Even if DEX volume share remains at 2%, dYdX will generate $270M and $539M annually for $5T and $10T monthly derivatives volume, respectively.

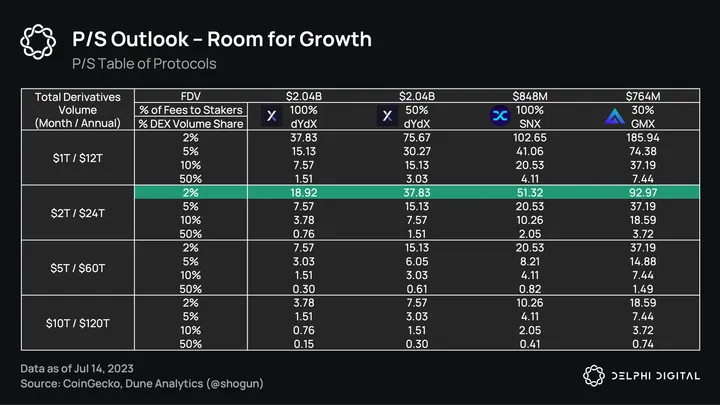

With SNX and GMX already distributing fees to their stakers, dYdX will be next once they’ve launched on v4. Exploring two scenarios where dYdX passes on 100% and 50% of fees to its stakers, it would represent a P/S multiple of 18.92 to 37.83.

With SNX and GMX already distributing fees to their stakers, dYdX will be next once they’ve launched on v4. Exploring two scenarios where dYdX passes on 100% and 50% of fees to its stakers, it would represent a P/S multiple of 18.92 to 37.83.

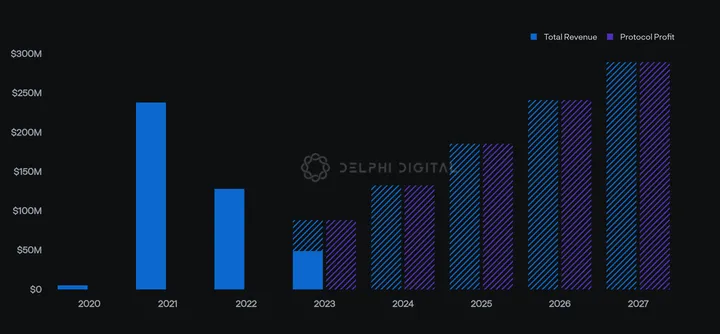

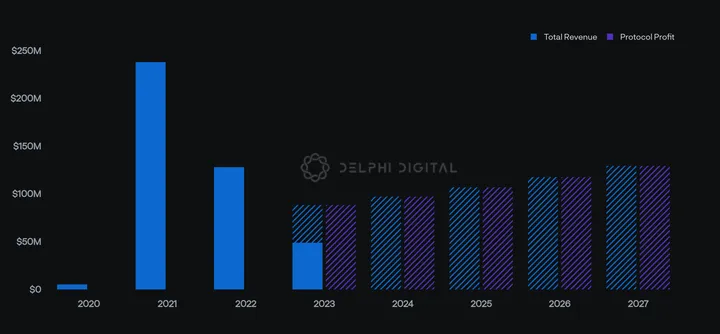

DCF Model on DYDX

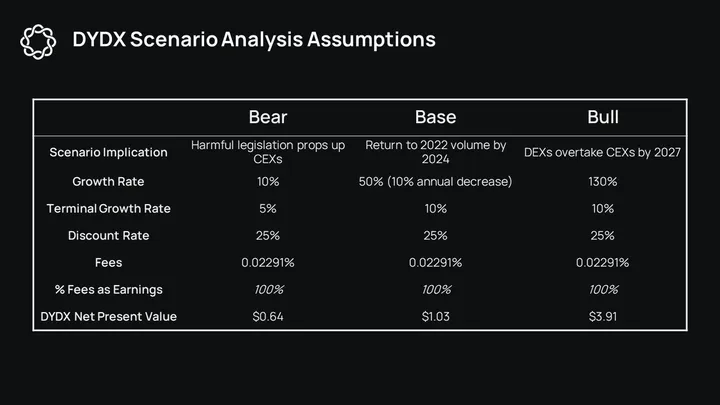

Looming unlocks and a token utility overhaul are thrusting the DYDX token into a renaissance. These factors will be the dominant influence on the token’s trajectory over the next year. We will examine three scenarios and consider the potential for DYDX tailwinds to neutralize the unlocks and dominate the narrative.

For this analysis, 100% of fees are included as earnings. This is not to suggest that dYdX lacks expenses, or that 100% of gross revenue will be distributed to stakers. DAOs are generally far more lightweight than traditional companies, but have several expenses. For dYdX, these could include the costs of running validators, which could reach up to 10% of revenue; an insurance fund; or a marketing budget.

Assuming 100% of protocol revenue is distributed to token holders is optimistic. SNX is the only example of this fee structure. It makes sense for Synthetix because SNX is the sole form of collateral and assumes risk as a temporary counterparty to traders.

GMX acts as more of a vanilla equity token, receiving 30% of fees. Given that DYDX token stakers will secure the network, distributing 50% of the fees or more to stakers is justifiable. Due to the recent revelation that no central entity will benefit from trading fees in dYdX v4 (including dYdX Trading, Inc.), it is likely DYDX will implicitly benefit from the entire pool of revenue, whether it be as a proxy claim on treasury assets or similar.

It has become common to heavily scrutinize a token for its amount of value accrual. In many cases, it is more accurate to think of the token as exposure to a high growth company that just happens to pay a massive dividend. The situation is much more palatable when considered in the context of Amazon and AT&T stock. For these reasons, 100% of fees as earnings offers a good baseline for evaluating a newly productive DYDX token.

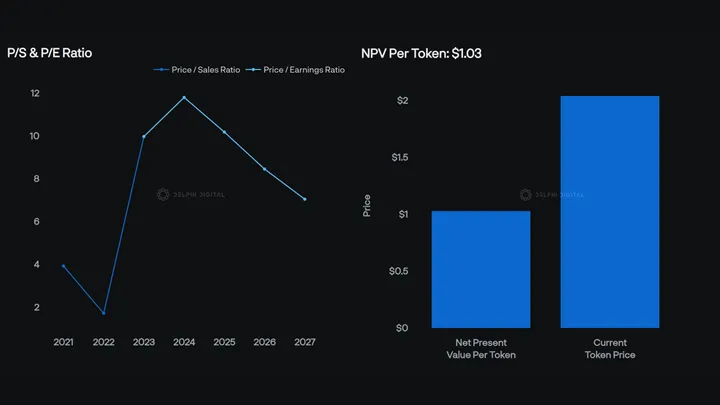

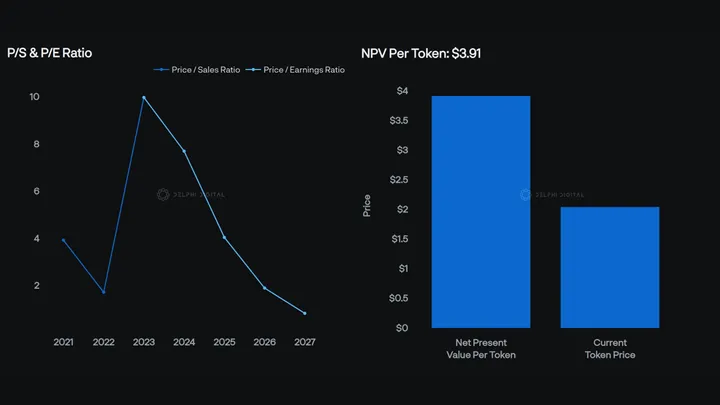

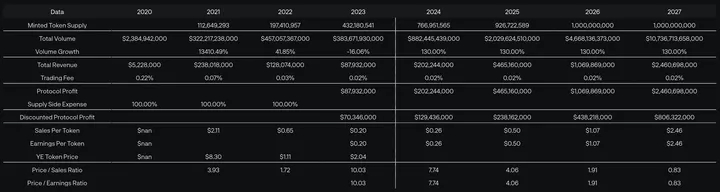

The net present value per token is calculated using the current token supply. This offers a valuable snapshot of DYDX fundamental value at a particular time, but fails to fully incorporate the extreme dilution risk present with the DYDX token at this stage of its lifestyle. An aggressive discount rate of 25% helps to this impact to some degree. The forward looking impact of dilution is better illustrated with the P/S and P/E charts.

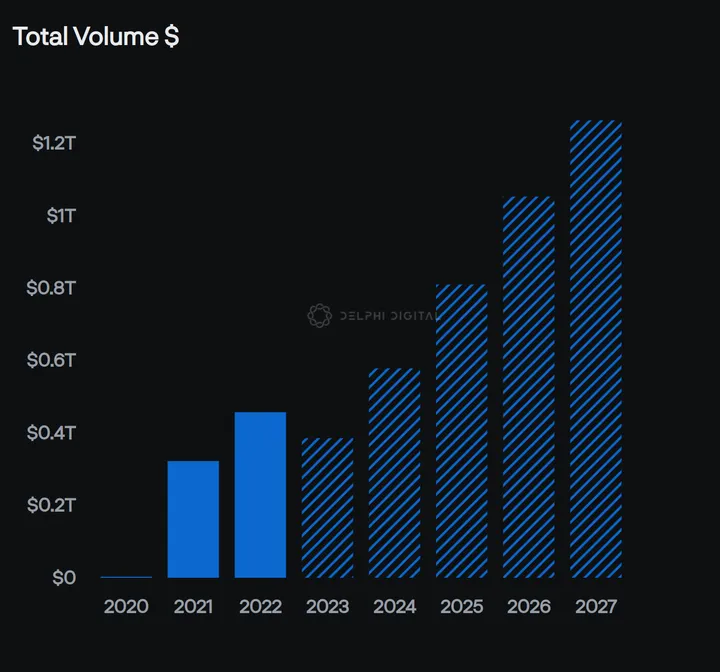

Base Case

The base scenario assumes DEX volumes regains 2022 levels by 2024. An initial growth rate of 50%, declining 10% each year and resting on a 10% terminal growth rate in 2027 achieves 2022 volume and continues with reasonable growth thereafter.

DYDX’s P/S ratio will begin to skyrocket upon its token unlocks in December. DYDX’s dominant market share and value accrual tailwinds are important compensation for its immature token relative to its peers.

Bear Case

In the bear scenario, decentralized perps growth stagnates at 10% in perpetuity. This case would likely arise from harmful legislation that causes a broad retreat to centralized solutions. Advancements in DEX technology would only be realized in select jurisdictions and could fail to ignite a narrative shift.

This would likely have a negative effect on the crypto market as a whole, but the DYDX token would be capable of weathering the storm if it receives a generous portion of fee revenue.

Bull Case

Our bull scenario sees DEXs finally overtake CEXs in total futures volume in 2027. This scenario holds the total futures volume (CEX+DEX) constant, meaning DEX volume is a result of CEX volume migration rather than a growth of total volume. This means the bull case is theoretically feasible regardless of broader market conditions.

Assuming dYdX maintains its 65% market share of perp DEX volume, protocol growth would quickly remedy token dilution concerns, with the P/S dipping below pre-unlock levels in 2025.

Holding volume constant and looking at future dates of interest can be an insightful exercise to understand the impact of upcoming unlocks.

For the time being, SNX looks to be the most well-equipped to benefit from the traction of the underlying protocol. SNX earns 100% of platform fees, and the token serves a unique and valuable utility. Ironically, this is the biggest risk for SNX as Synthetix transitions to v3.

The issue with SNX being the sole form of collateral is the scalability ceiling it causes since the economic bandwidth of the exchange is ultimately constrained by the market cap of SNX. Synthetix v3 introduces additional forms of collateral to back liquidity on the protocol. Onboarding additional collateral types in v3 will offer a huge boost to capital efficiency, but it will call into question the role of the SNX token. SNX could become a neutered token with no utility beyond governance.

Staked SNX is earning in the range of 8-10% in fees at the moment (not including inflationary SNX rewards). If the entire system used ETH as collateral and, by extension, utilized a similar c-ratio to leading money markets, ETH would be able to earn over 30% APR, close to what GLP was making in its heyday but with less risk.

The shift away from SNX as sole collateral is necessary for Synthetix’s long-term viability, but introduces uncertainty for the SNX token.

dYdX represents the opposite situation. DYDX currently functions similarly to centralized exchange tokens, granting discounts on fees and leaderboard shenanigans. The potential to gain a stake in such a profitable business via validator staking could make DYDX one of the most unique tokens in all of crypto. The steep unlock schedule is looming, and dYdX will need to hit the ground running with v4.

Keeping Trading Incentives in Check

After being allocated 9M OP (joint highest along with Perp Protocol), Synthetix was in a very attractive position. Many other projects in the Optimism ecosystem have already distributed their OP allocations.

Synthetix is distributing its OP allocation as trading rewards over the course of 20 weeks. Kwenta is distributing its share in tandem with Synthetix, resulting in a 10% boost to OP rewards when trading with Kwenta. In total, 330k OP per week for 20 weeks will be distributed to traders on Kwenta. At current prices, this equates to ~$75k in OP rewards per day. OP incentives have resulted in a healthy boost to perps volume.

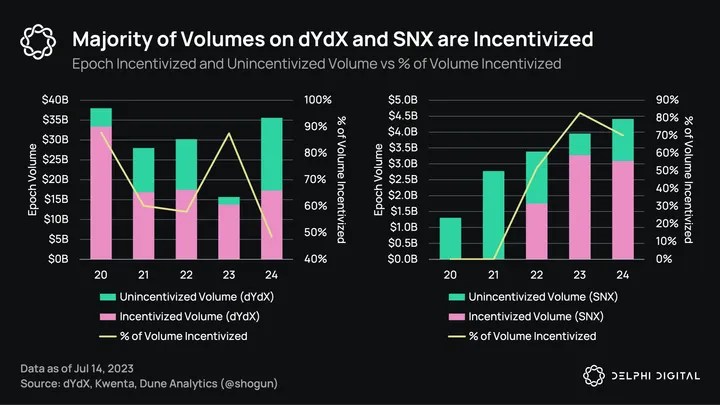

Besides SNX, dYdX has also been rather aggressive with its incentives. It is currently incentivizing trading with 1.58M DYDX tokens (~$3.2M) per epoch (28 days), which translates to $114k of daily incentives.

Note: 1 epoch = 28 days; SNX’s volume and rewards have been adjusted to dYdX’s epoch timeline.

Note: 1 epoch = 28 days; SNX’s volume and rewards have been adjusted to dYdX’s epoch timeline.

Here, we try to estimate how much of volume is incentivized. To do that, we used this formula:

Incentivized Volume = Epoch Average Value of Incentives / (Epoch Fees Earned / Epoch Volume)

Simply put, it uses the average value of incentives divided by the average fee percentage of each epoch.

The majority of dYdX and SNX volumes are incentivized, with some epochs hitting as high as 80-90% of the total epoch volume. Furthermore, it is hard to verify/deny the existence of potential wash traders.

Despite the negative connotations around incentivizing volume, it works to bootstrap volume and fees for the platform, and sometimes, it creates organic growth as well. For example, dYdX incentives were reduced from 2.8M DYDX to 1.5M DYDX after epoch 21, which resulted in an increase in unincentivized volume. This shows that the volume is sticky, even with smaller incentives.

Surprisingly, when comparing unincentivized volumes, GMX’s volumes were really close to or even higher than dYdX’s volume in certain epochs. This is rather surprising, as GMX traders are paying higher opening/closing fees, borrowing fees, and are not rewarded to trade. This shows the stickiness of GMX traders and the impact of zero-slippage execution.

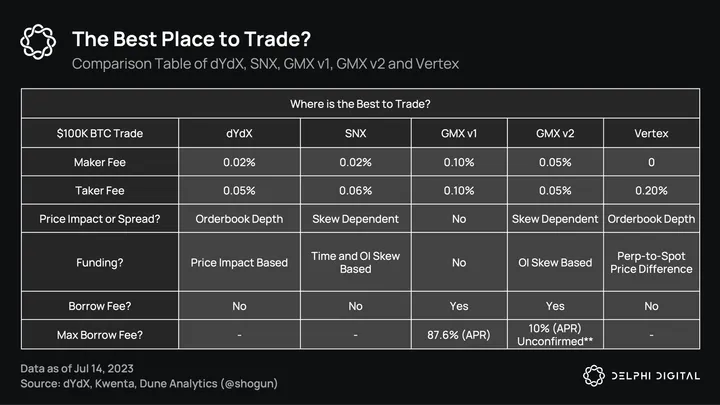

The leading perps DEXs all take somewhat different approaches but come out generally competitive for traders. For a brand-new exchange, Vertex’s trading metrics are staggeringly impressive.

The leading perps DEXs all take somewhat different approaches but come out generally competitive for traders. For a brand-new exchange, Vertex’s trading metrics are staggeringly impressive.Despite GMX v1’s high fees, traders remain there for its zero slippage, which is especially fruitful for traders executing in large size. For a $100k trade, it might make more sense to trade on a DEX that offers the cheapest fees, as all are able to offer instant liquidity for that size.

However, for sizable trades, e.g., a $5M BTC trade, orderbook DEXs do not have sufficient liquidity to execute them immediately, while SNX will incur a significant price impact. Although traders will incur higher fees, GMX v1 will be able to fill that size immediately. Since GMX v2 works similarly to SNX, the price impact might be significant for a sizable trade, dependent on the skew.

Interestingly, despite GMX’s higher fees, they’ve continuously managed to get traders to use their platform. This resulted in them being able to offer good yields on GLP. Perhaps fees can be considered a cost for liquidity.

It’s clear how the core mechanics of each perp DEX contribute to different growth levers and different user experiences. The next part of this report will specifically focus on how each protocol is structured and how they’re evolving.

Exploring Protocol Design

Synthetix

Synthetix perps v1 launched in March 2022 and was marred by wide spreads, limited risk mitigation, and low volume. Synthetix perps v2 hoped to provide lower costs and better risk management.

Since the launch of v2, Synthetix perps have become a serious player in the decentralized perpetuals space with consistent volume and growing market share. Perps v2 offers three key improvements over a traditional oracle-based DEX.

Funding rates: This is used to keep the price of a perpetual futures contract in line with the spot price. Funding rates can be positive or negative and increase as the price of the futures contract diverges from the spot price. Funding rates are paid by the overbought side to the underbought side on an hourly basis. In extreme instances with lopsided demand, the funding rate is exaggerated and can support impressive APRs — over 100% in some instances.

Due to the convenience of entering and exiting large positions with a futures contract versus spot, funding rates are often insightful indicators into the state of the market.

With margin-based trading platforms like GMX, there is always a borrowing cost associated with a trade, which can add up over longer time frames. With funding rates, a user can sometimes earn funding, i.e., be paid to hold a position open, if it balances open interest.

Price impact: Price impact or skew is an important evolution from the oracle design that was vulnerable to oracle manipulation attacks. Without price impact, Synthetix perps are theoretically vulnerable to the same exploit GMX v1 suffered on Avalanche. An exploiter could long/short an asset on Synthetix, and then make the same trade on a CEX. If the trader has adequate size or the asset is illiquid on the CEX, they can move the price on the CEX enough that oracles relay the price and make their on-chain trade profitable.

GMX suffered an attack of this nature in September 2022 on Avalanche. The trader was able to manipulate the price of AVAX on Coinbase such that their zero-slippage trades on GMX were profitable. The trader repeated the cycle with trades of $4M – $5M, earning $565k in total.

GMX suffered an attack of this nature in September 2022 on Avalanche. The trader was able to manipulate the price of AVAX on Coinbase such that their zero-slippage trades on GMX were profitable. The trader repeated the cycle with trades of $4M – $5M, earning $565k in total.

Oracle-based markets will always be vulnerable to oracle manipulation, but price impact significantly reduces its effectiveness.

Off-chain oracles: Synthetix uses on-chain oracles to keep synths pegged to their corresponding asset prices. This leaves the protocol and its users vulnerable to front runners. Perps v2 integrates Pyth Network for off-chain pricing with on-chain verification. This approach mitigates front running and has allowed Synthetix to lower trading fees to 2/6 bps on major pairs, consistent with CEXs.

By integrating both Pyth and Chainlink, Synthetix is effectively decentralizing its oracle solutions, limiting the risk involved with relying on one oracle. Synthetix can also incorporate additional oracles, such as Uniswap v3 TWAP oracles.

Synthetix’s new risk management features have resulted in a balanced LP exposure to long/short open interest. After a volatile start, open interest tends to remain within a tight range around 50%.

Balanced exposure and improved risk management have allowed Synthetix perps to be highly profitable. The graphic above shows the daily profit/loss of Synthetix perps, which is a function of fees earned and exposure to assets in the debt pool as a temporary counterparty. This has meant $6M of cumulative earnings in six months of flows to SNX stakers, who currently act as the sole form of collateral for sUSD.

The success of GMX margin trading has anchored much of DeFi’s DEX momentum over the past cycle, but some drawbacks to the model have begun to surface. GMX often has net long/short exposure of more than 50% of total open interest. Synthetix perps v2 typically has net exposure below 4% of total open interest.

GMX v2 will implement similar risk management features to Synthetix perps. Synthetix perps v2 is significant as an example of the peer to pool model that can work sustainably for both traders and LPs at scale.

Kwenta, Polynomial, and the Role of Front Ends

One of the key differences between Synthetix and GMX v2 is that Synthetix views itself as a derivatives liquidity layer while GMX aims to be a trading platform. This differentiation may seem like splitting hairs, but it results in very different approaches. Synthetix has not bothered to build front ends for its perps product. Although Kwenta dominates the current market, several projects have built on top of Synthetix’s permissionless infrastructure.

Polynomial is exploring building power perps and vaults on top of Synthetix, in addition to a trading front end. Kwenta is building a smart margin system with collateral management and limit orders to provide a more complete trading experience.

For now, all revenue from perps v2 goes to SNX stakers. Ecosystem front ends must provide additional value in order to take in revenue. Fee sharing with front ends is an ongoing spirited discussion within the Synthetix community and could bolster the earnings of front ends in the near future.

Synthetix v3

Under the current Synthetix V2x regime, Synthetix perps are supported by a monolithic pool of SNX stakers. Parameters for the pool, such as liquidation threshold, target ratio, etc., are calibrated by the Spartan Council. SNX is the sole accepted form of collateral. The c-ratio is currently 500% but has ranged from 350-800% over the past few years. The use of SNX as the sole form of collateral has created a unique symbiotic relationship between token holders and the protocol, but it severely limits scalability to the valuation of SNX.

Synthetix v3 will be a complete redesign of the Synthetix ecosystem. While not the focus of this report, Synthetix v3 will have important implications for Synthetix perps. Synthetix v3’s core feature is its differentiated debt pools, made up of a variety of collateral assets. Differentiated debt pools will allow users to seamlessly select markets they will offer or avoid exposure to — without fragmenting liquidity for end users.

Synthetix v3 will function similarly to Rari Capital’s Fuse product. Fuse was a permissionless money market where anyone could deploy a lending market and configure parameters such as supported collateral assets, LTVs, oracles, etc. Bootstrapping liquidity and product-market fit for a lending pool was up to the users. DAOs and prominent Twitter influencers put social capital to work on Fuse, resulting in a unique ecosystem and a strong product for a brief period of time.

Synthetix v3 will function similarly to Rari Capital’s Fuse product. Fuse was a permissionless money market where anyone could deploy a lending market and configure parameters such as supported collateral assets, LTVs, oracles, etc. Bootstrapping liquidity and product-market fit for a lending pool was up to the users. DAOs and prominent Twitter influencers put social capital to work on Fuse, resulting in a unique ecosystem and a strong product for a brief period of time.

Synthetix v3 will work similarly to Fuse, but Synthetix v3 pools will support all types of derivatives and will overlap whenever possible, solving the messy fragmented liquidity issue that was present on Fuse.

Perps v3 is essentially Perps v2 deployed on Synthetix v3. The core perps design will remain unchanged, but the v3 architecture will allow for native cross-margin and cross-chain liquidity.

GMX

GMX has established itself among DEXs through its successful margin trading platform with a UX that is very similar to using perps. Boasting an impressive cumulative trading volume of over $115B from GMX v1, GMX is now poised to build on its previous success with the imminent launch of v2.

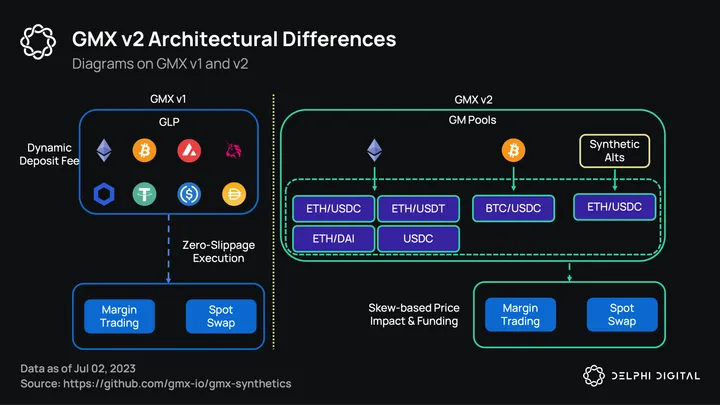

GMX v2 approaches liquidity differently and offers synthetic positions to broaden its asset offerings — something previously limited by the design of GLP.

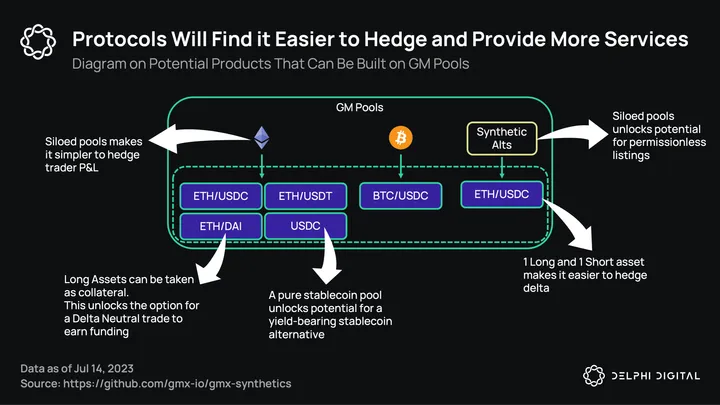

On GMX v1, GLP is comprised of 50% stablecoins and 50% risk assets (ETH, BTC, and others). However, the upcoming GMX v2 will bring about a change to this model with the introduction of GM pools.

On GMX v1, GLP is comprised of 50% stablecoins and 50% risk assets (ETH, BTC, and others). However, the upcoming GMX v2 will bring about a change to this model with the introduction of GM pools.

In contrast to GLP and its multi-asset baskets, GM pools will only hold two types of assets: a long asset and a short asset. Depositors can decide to deposit either only the long/short asset or both in balance. However, if the deposits affect the skew of the pool, depositors will be faced with a price impact upon adding assets. We will elaborate on this later.

In a nutshell, the high-level working of GMX doesn’t change much. GMX v2 will work similarly to v1, with LPs renting spot exposure to traders and earning fees. What mainly changes, as mentioned above, is the way liquidity is structured. Here’s a brief explanation of the different kinds of GM pools that can exist:

Index token paired with the same long asset: e.g., ETH Index might be paired with an ETH/USDC LP or BTC Index with a BTC/USDT LP.

-

This operates similarly to v1 but restricts the long asset to only BTC or ETH, paired with a stablecoin serving as the short asset.

Index token paired solely with stablecoins: e.g., ETH Index paired only with USDC in an LP.

-

This setup creates a synthetic position backed by stablecoins. It’s ideal for LPs who prefer to avoid exposure to volatile assets.

Altcoin index token paired with ETH/stablecoin LP: e.g., BNB Index token paired with ETH (as the long asset) and a stablecoin (as the short asset).

-

This setup creates a synthetic position backed by the ETH/stablecoin LP. This setup is suitable for LPs who desire P&L exposure to altcoins in addition to earning fees. However, these altcoin synthetic positions are more volatile and will carry higher P&L exposure than BTC or ETH positions.

In short, GMX will have different tradable indices that various on-chain assets can back. The asset backing, however, can be structured in different ways that affect the net positioning of LPs.

While GMX v1 offers zero-slippage execution. GMX v2 introduces a price impact based on the skew of LPs and open interest. For clarity:

-

GM pool deposits, withdrawals, and spot swaps are affected by LP asset skews.

-

Margin traders are affected by OI skews. Additionally, funding rates will be introduced to further balance OI.

This skew-based approach aims to maintain a balance among LPs and traders, thereby minimizing unnecessary risks to LPs.

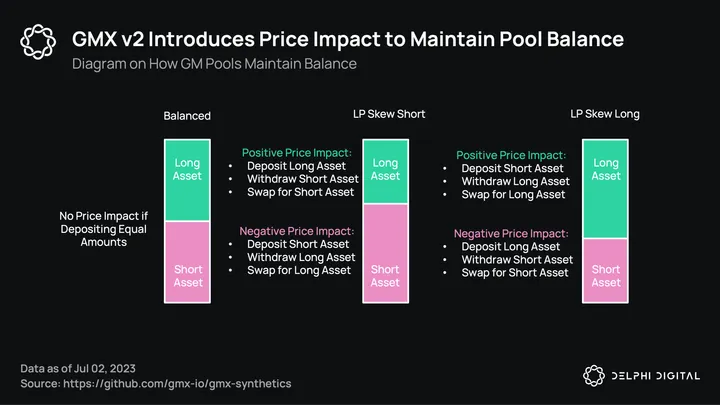

The price impact occurs when an action that causes a skew between the long and short assets within a pool is introduced.

The price impact occurs when an action that causes a skew between the long and short assets within a pool is introduced.

Specifically, when a transaction widens the skew, it incurs a negative price impact. This mechanism serves as a deterrent against amplifying the skew further. Conversely, if a transaction closes the skew, it incurs a positive price impact, acting as an incentive for narrowing the gap.

Here are some examples:

Balanced: Long Asset 50%, Short Asset 50%

-

No price impact if an equal amount of long and short assets are deposited

-

Negative price impact if only long or short assets are deposited

LP Skews to Either Long or Short: e.g., Long Asset 40%, Short Asset 60%

-

No price impact if the ratio of long and short assets is the same as the skew

-

Positive price impact if long assets are deposited (as it closes the skew)

-

Extreme price impact if short assets are deposited (as it worsens the skew)

This mechanism helps to encourage the equilibrium of long and short assets in a pool, ensuring that any skews are resolved by arbitrageurs who stand to profit from positive price impact.

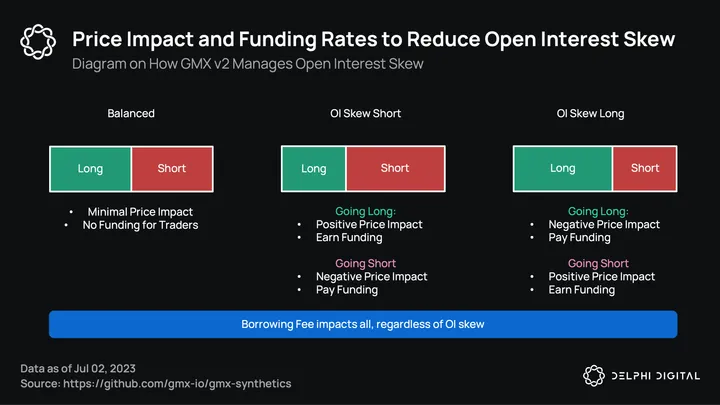

To balance OI skews, a system of price impact and funding rates is introduced. If OI is skewed in a particular direction (for example, long), traders will be encouraged to take the opposite position (in this case, short) through positive price impacts and funding payments.

To balance OI skews, a system of price impact and funding rates is introduced. If OI is skewed in a particular direction (for example, long), traders will be encouraged to take the opposite position (in this case, short) through positive price impacts and funding payments.

Moreover, this disincentivizes further trades that would accentuate the skew. This is achieved by imposing a negative price impact on such trades. In addition, any open positions in the skewed direction will be charged funding. This dual mechanism fosters a balance in trading activities, thus ensuring a healthier and more stable trading ecosystem.

![]() Source: GMX Discord

Source: GMX Discord

For clarity, funding is different from borrowing fees. Borrowing fees affect levered traders, regardless of OI skew. The good news is that borrowing fees could be capped at 10% APR, much lower than GMX v1, which is utilization-based and can go up to 87.6% APR.

Multiple protocols utilize GMX’s GLP to create yield products. These include delta-neutral/minimized vaults, levered GLP positions, and other yield aggregation vaults. Furthermore, GLP has been integrated within money market protocols, allowing it to be used as collateral.

Multiple protocols utilize GMX’s GLP to create yield products. These include delta-neutral/minimized vaults, levered GLP positions, and other yield aggregation vaults. Furthermore, GLP has been integrated within money market protocols, allowing it to be used as collateral.With GMX v2, these protocols might find it much easier to hedge compared to GLP. GM pools bring a few advantages for them:

-

Siloed index tokens make it easier to hedge trader P&L with only the need to consider 1 asset vs. multiple assets on GLP.

-

GM pools only have 1 long asset within the LP to hedge to have minimal delta exposure. However, the stablecoin-only pools may compete with any delta-neutral stablecoin vault. The competition depends on the utilization and performance of that stablecoin pool, and if the ETH/stable pool is able to generate higher fees, depositors will still opt for a delta-neutral alternative with higher returns.

-

Volatile assets like ETH and BTC can be used as collateral; a trader can go short with the asset and create a delta-neutral position. This gives individuals and protocols the opportunity to capture any positive price impact and earn funding until the skew reverses.

-

Stablecoin pools unlock a stablecoin yield product, which can also be safely collateralized without any market delta outside of trader P&L.

Lastly, the siloed pools unlock the potential for permissionless listings. This could include new protocols that could offer perps from day 1. This will be game-changing, as protocols do not need to wait for CEXs to list them. However, this also poses a significant risk, as accurate oracle pricing is still required alongside mitigations needed for market manipulation that will adversely affect LPs.

GMX is launching v2 alongside v1, which has stood the test of time. A big risk factor for the v2 launch is how the dynamic between these two will play out. GLP has become less profitable as GMX has continued to grow. An increase in adversarial traders, perhaps along with an overdue string of bad luck, has seen GLP retrace a large portion of its early gains from traders’ losses.

Cheaper fees and exotic assets on v2 will be attractive for small-to-medium-sized traders, which will likely help prop up GM pool fee earnings. Furthermore, GM pools will be lower risk pools, with limited exposure to traders’ P&L due to their OI balancing mechanism. Because they are designed this way, the reduced risks of providing liquidity could also attract more deposits and dilute fees.

Zero-slippage trades have proven attractive for smart money looking to trade with size. GMX v1 will remain attractive for short-term trades with large sizes, which could exacerbate some of the issues that are emerging with the GLP model. Depositors will also have to weigh the pros and cons of GLP vs. GM pools to decide on a liquidity pool that is suitable for them.

dYdX

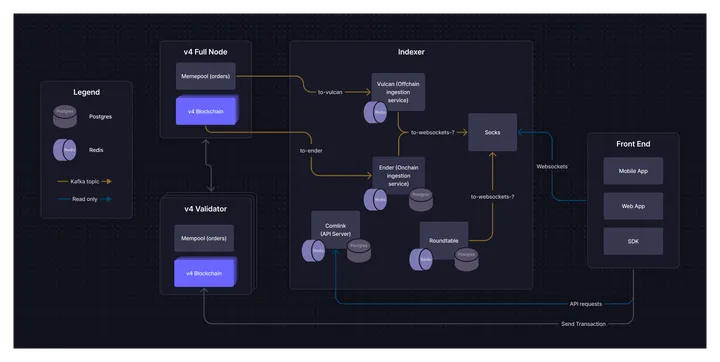

dYdX v3 is a perpetuals DEX built on StarkEx, a ZK rollup, that has done over $980B in cumulative volume and is currently doing $5B to $10B in weekly volume. This makes dYdX one of the most successful perpetual DEXs in the space and the market leader. Despite its success on StarkEx, they’ve decided to launch v4, AKA, dYdX chain, as a standalone L1 app-chain that features a decentralized off-chain orderbook and matching engine. dYdX chain is built based on the Cosmos SDK and CometBFT PoS consensus protocol. Going straight into it, here are the different roles played to keep dYdX decentralized and functional.

Going straight into it, here are the different roles played to keep dYdX decentralized and functional.

Validators are responsible for consensus on dYdX and maintaining the orderbook. The following is a breakdown of their role.

-

Storing orders in an off-chain orderbook.

-

Users will submit orders directly to validators.

-

-

Gossiping transactions to other validators.

-

Propose (the content within the block) and produce new blocks for dYdX chain.

-

This is done through a stake-weighted round-robin mechanism.

-

When an order is matched, the proposer will add it to the proposed block.

-

A consensus vote will then be initiated with 2/3 of the validators by stake weight required to approve the block. The approved block will be committed and added to the blockchain.

-

-

Consensus-based oracle where validators will be required to report prices on every block from sources of their choosing, with a minimum number of sources required.

Full nodes run the v4 application and download the chain history, but they do not participate in consensus. One of their main roles is to support the indexer. Its role includes:

-

Gossiping transactions to other validators

-

Connecting to the validators

-

Processing new committed blocks

Full nodes have a complete view of dYdX and its history to provide data support for the indexer.

An indexer is a collection of read-only services to index and serve blockchain data to users. This is done by reading data from a full node, storing it in a database, and providing the data to end users. An indexer is set in place as validators’ and full nodes’ primary role is to maintain consensus and process blocks and are not optimized to serve queries.

Indexers serve two types of data:

On-chain data represents all data that can be reproduced by reading committed transactions on the dYdX chain. These include:

-

Account balances (USDC)

-

Account positions (open interest)

-

Order fills (trades, liquidations, deleveraging, partially and completely filled orders)

-

Funding rate payments

-

Trade fees

-

Historical oracle prices (spot prices used to compute funding and process liquidations)

-

Long-term order placement and cancellation

-

Conditional order placement and cancellation

Off-chain data represents data that is kept in the mempool on each v4 node. This data is not written to the blockchain. This is short-lasting data on v4 nodes that is lost once the full nodes purge it. This includes:

-

Short-term order placement and cancellations

-

Orderbook of each perpetual exchange pair

-

Indexed order updates before they hit the chain

The indexer makes the on-chain and off-chain data available via its API and websockets to front ends and any other services querying the data.

Front ends will be open-sourced to allow anyone to host front ends for websites, iOS, and Android.

Previously, on dYdX v3, the orderbook and off-chain matching engine were run by dYdX, making it centralized. The architectural changes allow dYdX to move to a decentralized model, allowing anyone to run a validator, full node, and indexer. Moreover, their commitment to open-source creates an environment to support decentralization.

The Move to dYdX v4

User Experience:

dYdX’s strategic shift to the Cosmos ecosystem could initially introduce complexity, given the relative lack of a mature DeFi ecosystem on Cosmos. This might result in a temporary decrease in market share as dYdX v3 is phased out and as the liquidity migration process unfolds.

However, Circle’s Cross-Chain Transfer Protocol (CCTP) enables native USDC bridging to Cosmos, maintaining a familiar user process and minimizing friction. Moreover, dYdX promises a smooth transition to v4, supporting deposits from major chains and accessibility from most wallets. This approach, reminiscent of deposits into a centralized exchange, is likely to be easily adopted by users.

Decentralized Benefits and Increased Token Utility:

With dYdX v4, the platform becomes entirely decentralized and subject to governance by token holders. This enables DYDX token holders to dictate token utilities, add/remove markets, and modify dYdX v4 parameters. Building on its success with perpetuals, the platform could also diversify into spot markets, providing a comprehensive DeFi application with high user retention.

Challenges:

While the transition to dYdX v4 enhances decentralization, several challenges need to be tackled. dYdX must replicate its earlier success and secure the backing of market makers for their orderbook. However, given that both traders and market makers are incentivized with DYDX tokens, the migration is likely to be deemed worthwhile, regardless of the effort involved. Furthermore, they’re reducing DYDX incentives for market makers in exchange for higher rebates, which reduces emissions in exchange for lesser fees paid.

A longer-term challenge involves addressing the UX issues associated with DEXs. Users new to DeFi and wallets may find on-chain transactions daunting. The next wave of user adoption is likely to occur once these complexities are abstracted and made user-friendly.

Additionally, with validators settling transactions, it brings in possibilities of MEV on dYdX v4. dYdX plans to integrate slashing for validators that extract MEV. Also, it looks like dYdX will be integrating Skip Protocol — an MEV infrastructure protocol — to manage MEV on dYdX.

Vertex

Vertex is a hybrid orderbook AMM protocol on Arbitrum. Vertex features unified cross-margin across its spot, perps, and money markets.

Vertex has a unique feature set, which has allowed it to generate $3B in cumulative volume since its launch in April.

-

Universal cross-margin

-

Orderbook/AMM hybrid model

-

Extremely low latency: 5-10 milliseconds, as fast as CEXs

-

Cheap fees: 2 bp spot; 3 bp perps

-

One-click trading

-

Collateralized LP positions

Universal cross-margin is a huge feat for a decentralized exchange. Many other projects are racing to achieve cross-margin on-chain, but Vertex is the first to implement it successfully. Cross-margin is extremely difficult to implement on-chain. All of the issues that plague traditional liquidations — oracle triggers, liquidity to unwind, volatility of assets, gas costs, etc. — are pronounced when building a unified cross-margin system across spot, derivatives, and money markets.

Vertex’s brand is centered around its strong trader UX, which rivals centralized exchanges. Isolated margin and stop losses are the only important features missing, but these will be added soon.

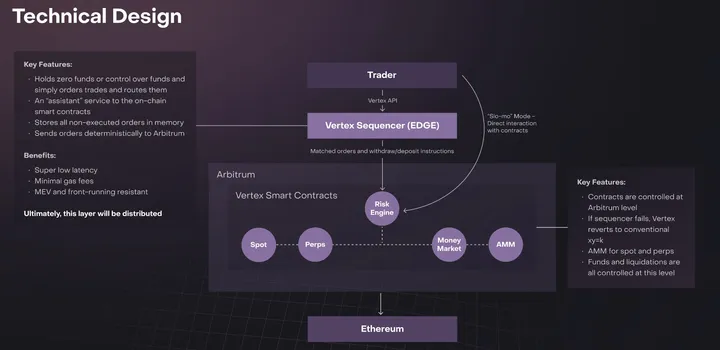

Under the hood, Vertex’s hybrid model consists of spot, perps, money markets, and risk engine smart contracts deployed on Arbitrum. The Vertex Sequencer is an off-chain central-limit orderbook that sits on top of the smart contract layer, allowing Vertex to offer a CEX-like experience with extremely low latency. The Vertex Sequencer runs on an independent node managed by the Vertex team. In the future, the sequencer can be decentralized to up to 5 nodes, elected by Vertex governance.

Under the hood, Vertex’s hybrid model consists of spot, perps, money markets, and risk engine smart contracts deployed on Arbitrum. The Vertex Sequencer is an off-chain central-limit orderbook that sits on top of the smart contract layer, allowing Vertex to offer a CEX-like experience with extremely low latency. The Vertex Sequencer runs on an independent node managed by the Vertex team. In the future, the sequencer can be decentralized to up to 5 nodes, elected by Vertex governance.

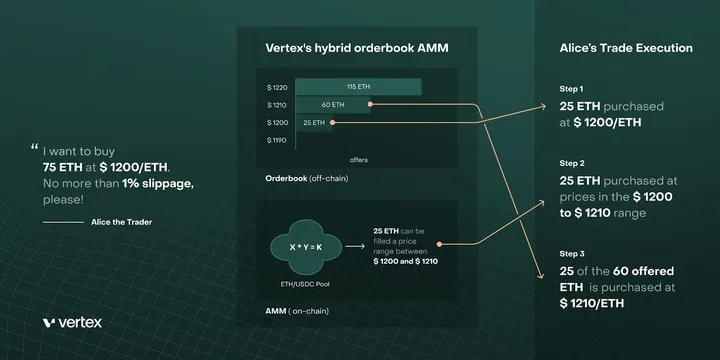

The hybrid model is attractive in its ability to offer the high performance of an orderbook, with the reliability and accessibility of an AMM. Users who wish to operate fully on-chain can utilize “slow-mo mode,” interacting solely with the smart contracts and the AMM.

Users can provide liquidity to spot and perps pools. The liquidity of the AMM operates in conjunction with orderbook liquidity, and orders can be partially filled by each source for best execution. The AMM uses a constant product xy = k formula and is currently live. Perps will use a single-sided vAMM collateralized by USDC, and are not yet available.

Users can provide liquidity to spot and perps pools. The liquidity of the AMM operates in conjunction with orderbook liquidity, and orders can be partially filled by each source for best execution. The AMM uses a constant product xy = k formula and is currently live. Perps will use a single-sided vAMM collateralized by USDC, and are not yet available.

vAMMs have struggled mightily to service perpetual futures since their inception — especially those who parameterized around XYK AMMs. They offer a solution to capital efficiency hurdles, but their issues have been well-documented in prior perpetual futures protocol designs, and most recently with the sunsetting of NFTperp exchange. Vertex’s AMM perps design may have to be reworked before launch.

There appears to be a strong probability that the vAMM perps liquidity provision will be quietly scrapped, given the ambiguity around the design nuances and the partnership with Wintermute as a strategic investor and market maker.

Friction between the AMM and orderbook could become an unavoidable drawback to hybrid models. Ideally, the two function synergistically and offer the best of both worlds to users. But there may be a tendency for the AMM to bootstrap liquidity until the DEX can secure product-market fit and lure market makers to the platform. The AMM arm of the protocol is then relegated to more of a gadget.

Poor liquidity and LP competitiveness could render the AMM unviable for users who wish to interact solely with the smart contracts. Uniswap’s recent FLAIR paper can be interpreted as a preemptive metric for this phase of DeFi. LPs in a constant product AMM alongside professional market makers may struggle and migrate elsewhere.

Vertex is likely competing more with dYdX than liquidity pool-based models such as Synthetix, GMX, and Gains Network. Vertex presents an EVM alternative to dYdX. In practice, it may end up resembling a pure CLOB.

Vertex’s UX is impressive, and the technical achievements are undeniable. Cross-margin brings much-needed capital efficiency to DeFi. Cross-margin will not offer much of a moat, however, with Synthetix, GMX, Aevo, and others following closely behind. Vertex may struggle with a lack of composability, and there remains a lack of clarity around the future for perps liquidity provision.

Other Contenders

Gains Network

Gains Network has continued to grow over 2023 and is a key player in DEX perps. The wide variety of assets available, high leverage, and strong token economics are unique characteristics. Gains Network has become the home of on-chain Forex trading in DeFi. Gains Network may not be the end game for traders due to its 9x profit cap and low open interest caps, but it has carved out a strong niche for itself with the entry-level degen trader. The incumbents GMX and Synthetix are increasingly moving away from this model, leaving Gains to dominate this role. For more on Gains Network, check out our report.Aevo

Aevo is an orderbook-based options and perps exchange built on the Optimism stack. Aevo seeks to be a one-stop-shop for derivatives trading and is currently in open testnet.

Since opening the testnet to the public, users have skyrocketed. Its positioning in the Optimism umbrella could put it up against Synthetix, but there are interesting potential synergies with the soon-merged Ribbon brand and the potential to offer options on smaller cap assets.Additionally, Aevo’s perpetual product works synergistically with its options markets, allowing traders to hedge delta in a single platform. Since the perpetual markets launch, both options and perpetuals volume saw rather significant growth. For more on Aevo, check out our report.

Dark Horses

There are a few other projects with interesting approaches that are a bit early.

-

Vega – Vega is a native blockchain purpose-built for derivatives. It features permissionless asset listing, native liquidity incentives, and no gas costs. There have been several delays in development, but the project is currently live on alpha. For more on Vega, check out our previous coverage.

-

Phoenix – Phoenix is a non-custodial CLOB from Ellipsis Labs, built on Solana. Phoenix is currently in open beta, and could benefit from the recent momentum in the Solana ecosystem.

-

Levana – Levana is a perps exchange on Cosmos with no insolvency risk.

Mapping Out the Competitive Landscape

dYdX has held its position as the incumbent DEX for perpetual contracts, capitalizing on the first-mover advantage to gain substantial traction. It dominates the market share, accounting for daily trading volumes between 40% and 80%. Its closest competitors, Synthetix and GMX, hold approximately 5-30% and 4-24% of the market share, respectively.

Joining the competition, Vertex has quickly secured ~10% of the volume share, marking a noteworthy entry into the market.

Yet, despite the emerging competitors, dYdX has successfully maintained its robust lead. It’s interesting to note that each network appears to have its own dominant player — dYdX reigns on StarkEx, GMX takes the lead on Arbitrum, and Synthetix tops the market on Optimism.

Despite the vibrant competition, trading volumes on perpetual DEXs have largely remained steady without any significant upward trends. Volumes tend to hover around $1B-$2B daily, with occasional spikes.

This stagnant trend in volumes might suggest two possibilities: firstly, there may be a lack of market demand for leverage, and secondly, the adoption of DeFi perpetuals may not be gaining new participants.

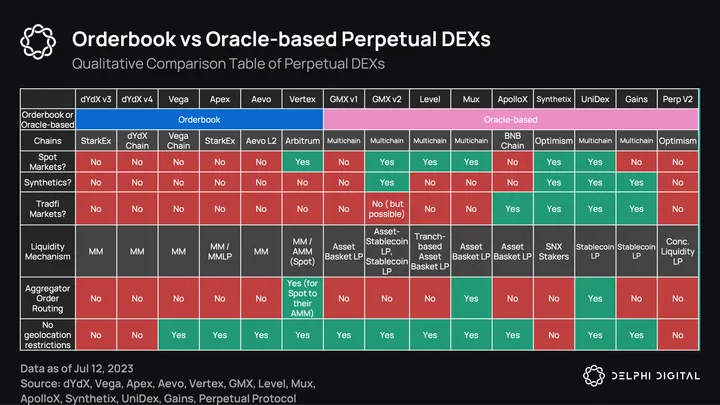

Lastly, here is a more extensive comparison table for users to compare which perpetual DEX will suit them best.

Lastly, here is a more extensive comparison table for users to compare which perpetual DEX will suit them best.

dYdX

Strengths: Industry leader by a long shot. Gaining token utility renaissance and worst of the dilution postponed until December 2023. Token trades at steep circulating market cap discount relative to peers.

Weaknesses: dYdX’s move to Cosmos is a bold one. If it goes perfectly, it could position dYdX as a titan in the Cosmos ecosystem, bootstrapping a lot of the PMF themselves similarly to Uniswap on Ethereum. However, in a time with so many developments elsewhere in the perps space, dYdX could temporarily cede market share to users who wish to remain in the EVM ecosystem.

GMX

Strengths: If trading activity is even remotely sticky, GMX will be in great shape for a long time. GMX has become synonymous with crypto-native leverage trading, is in a power position to bootstrap liquidity for its v2 pools, has a successful business model in the background with v1, and the safety of a Business Source License (BSL) to fend off forks.

Weaknesses: Uncertainty about the dynamic between v1/v2. Long-term use for GMX beyond rent-seeking. Once the DYDX token starts its fee sharing, out of the major protocols — dYdX, SNX, and GNS — GMX extracts the most value without any service.

Synthetix

Strengths: Synthetix has an established, working product that has been successful for about five months. Organic traction prior to the incentive program. There is little risk involved in the core perps design for Synthetix at this juncture. GMX v2 has a similar offering, so Synthetix does not have to worry about an on-chain competitor completely one-upping them.

Weaknesses: Synthetix v3 is an ambitious upgrade that could raise questions about the role of the SNX token.

Vertex

Strengths: Vertex is the first cross-margin perps exchange in DeFi. Though many others are not far behind, the cross-margin will be a growth hack for Vertex for the time being. Its UX is highly impressive.

Weaknesses: From a trader’s perspective, Vertex is the real deal. It is unclear how viable the on-chain aspect (slow-mo mode) of Vertex will be in the long run. If it is underwhelming, Vertex will be unable to penetrate the same markets as Synthetix and GMX and will be going for the EVM dYdX role. Feature-wise, Vertex is only lacking isolated margin and limit orders. When these arrive in future updates, it will be difficult to critique Vertex’s offering.

Conclusion

The decentralized perps space is clearly reaching an inflection point in the battle with centralized exchanges. Synthetix and GMX have established businesses on the cusp of breakthroughs that will add a new dimension to their platforms. dYdX is risking its multi-year dominance with a bold move to a Cosmos app chain. If the transition goes smoothly, a rejuvenated DYDX token could join the elite tier of DeFi tokens. Vertex appears the most likely to challenge these out of the remaining DEXs.

Despite the positive sentiment, CEX volumes still dwarf DEX volumes by a large margin. DEXs will have to continue innovating on the infrastructure, UI, and UX front to compete on the same level as CEXs.

Special thanks to Cheryl Ho for designing the cover image for this report; to Medio Demarco, Ashwath Balakrishnan, and Brian McRae for editing; and to Christian Cioce for assisting with data analysis and visualization.

0 Comments