ETH Borrow Rate On Aave Rises As Users Position For The Merge

AUG 17, 2022 • 5 Min Read

🚨 In Case You Missed It

- Vitalik says he is in favor of burning the staked ETH of any validator that hypothetically complies with regulators and censors Ethereum at the protocol level.

- Do Kwon, CEO of Terraform Labs, sits for an interview for the first time after UST de-pegged in May-22.

- Jump Crypto announces it will build a new, open-source validator client for Solana, independent from the one built by Solana Labs.

- Genesis, crypto lender and broker, says its CEO Michael Moro will step down in a leadership shuffle. The company will also fire 20% of its 260-person workforce.

- FT reveals that Alex Mashinsky, CEO of crypto lender Celsius, shorted BTC with customer assets ahead of the Jan-22 Fed meeting and incurred losses. Celsius also says it has several offers to inject cash into the company.

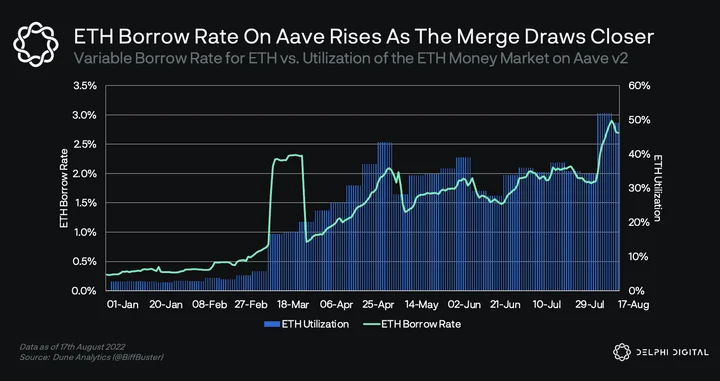

📊 ETH Borrow Rate On Aave Rises As Users Position For The Merge

- On August 14, the variable interest rate for borrowing ETH from Aave v2 climbed up to reach 2.90%, the highest rate since February 2021.

- Meanwhile, the utilization rate of the ETH money market reached an all time high of 52%. This is the percentage of the pool that has been borrowed by other users.

- This comes as a sharp increase from the beginning of this year when the borrow rate was 0.27% and the utilization rate was 2%. This increase is likely the result of users positioning themselves to profit off a potential hard fork of the Ethereum chain.

- When the Merge goes through, many suspect that some miners will fork a new chain that retains Ethereum’s proof-of-work consensus mechanism. If this happens, ETH holders will be airdropped an equivalent ETH-PoW token on the new chain.

- To profit from such a hard fork, users are borrowing as much ETH as they can in order to maximize the number of ETH-PoW tokens airdropped to them. Subsequently, this pushes up the borrowing rate and utilization of ETH on Aave v2.

- Surprisingly, the ETH money market on Compound Finance is offering a net rate of only 0.15% to borrowers (after COMP incentives) with only 3% utilization rate.

- For more on the Merge, you can read our previous Delphi Daily report here.

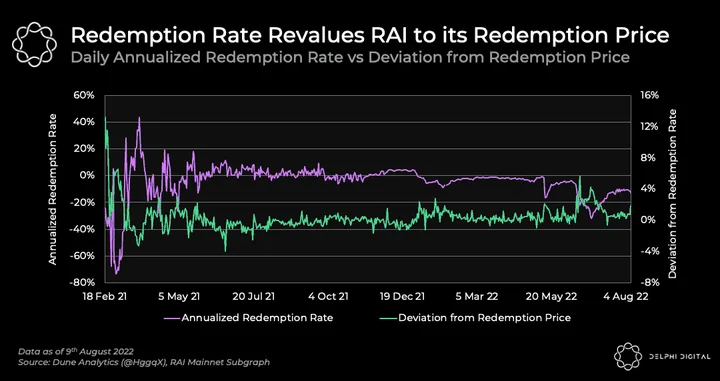

⚡ Is RAI The Decentralized Stablecoin The Market Needs?

- A simplistic way to think about RAI is to see it as similar to Single Collateral DAI (SAI), where users deposit ETH as collateral and mint the corresponding stablecoin.

- A key difference is that while SAI was pegged to $1, RAI’s target price (or redemption price) is not bound to an external reference price like the US dollar. In short, RAI doesn’t perpetually target an explicit price.

- Instead, it has a floating peg that changes according to market forces. When the price on secondary markets (i.e. market price) is the same as the redemption price, the system is in equilibrium.

- Otherwise, the protocol sets a redemption rate to counter price moves and incentivize market participants to return RAI’s market price to the redemption price.

- To really understand this, we need to consider two scenarios: when market price is lower than redemption price, and when market price is higher than redemption price.

- Market Price < Redemption Price

- In this situation, the redemption rate is positive. The positive redemption rate “revalues” RAI, which increases the redemption price every second.

- As RAI’s redemption price increases, it becomes more expensive for borrowers to pay back their debt. The incentive here is for borrowers to repay their loan before the RAI price rises too much.

- Naturally, this would cause borrowers to buy RAI on spot markets so that they can pay back their debt before the market price converges with the redemption price.

- The buying pressure, from both borrowers and speculators, thus drives market price higher and brings it back into equilibrium with the redemption price.

- Market Price > Redemption Price

- Here, the redemption rate turns negative. The negative redemption rate “devalues” RAI, which causes the redemption price to decrease every second.

- As RAI’s redemption price decreases, it becomes cheaper for borrowers to pay back their debt. This creates an incentive for borrowers to mint more RAI, increasing their total amount borrowed.

- With the newly minted RAI, borrowers would then sell it in the spot market because they know they’ll be able to buy it back cheaper later to pay down their debt.

- The selling pressure, from both borrowers and holders, drives the market price lower and brings it back into equilibrium.

- For more, Delphi members can read our Delphi Pro report here.

🐣 Notable Tweets

GNS and the Gains Network

/1 The case study of $GNS

$GNS is the first DEFLATIONARY token that will allow its holders to collect #RealYield🤑

Here’s why you should pay attention to it🧵👇

— The DeFi Investor🦇🔊 (@TheDeFinvestor) Aug 15, 2022

Non-Liquidable Leveraged Farming

Oh? Looks like it’s time for Atlantic Product #5!

Presenting: Atlantics Non-Liquidable Leveraged Farming

Wowza that was a mouthful!

In this thread, we will be covering the first iteration of this product which stands delivered as GLP Leveraged Farming

Watchout @GMX_IO farmers!— 0xSaitama (💎,💎) (@0xsaitama_) Aug 17, 2022

Designing Governance Tokens

New essay! Designing Governance Tokens

I laid out a 3-step framework for teams to think through their governance token design

At the crux of the design: should governance tokens be bought or earned? Well, it depends…

— Alana Levin (@AlanaDLevin) Aug 16, 2022

Get access to four research reports each week with key market coverage.

Sign up for Delphi Insights here.

0 Comments