ETH Staking, Lido Monopoly, Intro to OPtimism

MAY 31, 2022 • 7 Min Read

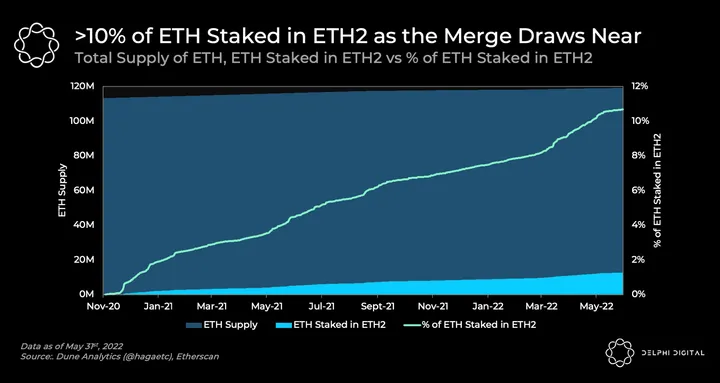

Chart of The Day: >10% of ETH Staked in ETH2

- For those unfamiliar, Ethereum is set to merge its Beacon Chain with Mainnet, which will transition Ethereum from a Proof-of-Work blockchain to a Proof-of-Stake blockchain. The merge will reduce reward emissions as miners will no longer participate in the consensus mechanism, and transaction fees will flow towards ETH stakers. With the reduction in emissions alongside EIP-1559 burns, Ethereum will likely become net-deflationary post-merge. The merge is expected to happen this year, with Vitalik revealing targets for August and Ethereum’s roadmap showing Q3/Q4 2022.

- >12M ETH, representing >10% of ETH’s supply is staked on ETH2 as the merge approaches. The ramp-up is likely due to more validators wanting to participate in securing the network and also yield farmers that want to maximize yields in a low yield environment.

- ETH staked in ETH2 currently earns ~4% APR, which is expected to double or triple post-merge as the transaction fees will be directed towards stakers. Furthermore, degen farmers can leverage up to 3x equivalent of stETH to boost yields through Aave or DeFiSaver. However, leverage does have risks, which was recently demonstrated by the stETH depeg causing the liquidation of over-levered positions.

- All eyes will be on the Ropsten Testnet, ETH’s longest-lived Proof-of-Work testnet, which is expected to merge by June 8th.

- For more on Ethereum, you can check out our Delphi Report on Danksharding here. Pss… It’s available for everyone!

The Lido ‘Monopoly’ and The ICS721 Standard

[Excerpt from a Delphi Insights Report]

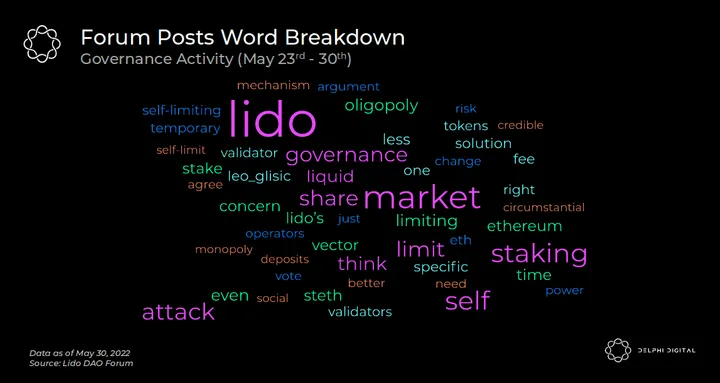

- Synopsis: In response to criticisms from the likes of Vitalik, Superphiz, and Danny Ryan, who argue that liquid staking protocols should have a limited stake in a chain, Lido developer Vsh, has created a thread where Lido DAO can debate whether they should self limit their stake on the Ethereum network. Lido controls 30% of all staked ETH, according to the forum thread. Some feel it may become a centralizing force for Ethereum and pose a risk to the entire ecosystem.

- Forum Arguments for Limiting: Some in the forum see the utility in Lido limiting its stake. One user argues that a temporary limit is reasonable, but only to allow time for competitors to catch up. Other users wonder how long Ethereum will allow Lido to exist as a potential threat to its decentralization – especially if it controls a large portion of the stake. They worry that Ethereum could hard fork and slash Lido validators in the name of decentralization.

- Forum Arguments Against Limiting: Twitter thread king, Adam Cochrane, argued that Lido limiting itself would allow for less altruistic competitors to emerge and steal its market share. He cites centralized exchanges as being the main competitive threat to Lido. He feels that Lido should instead work on building centralization guardrails rather than limiting itself. Some users feel that the argument that Lido should limit itself lacks nuance and understanding of Lido’s incentives – with one user posting a lengthy, technical rebuttal. Additionally, Adam reminds everyone that stETH doesn’t represent ETH staked in a single host, so Lido controlling a large percentage of stETH is immaterial. Sadcat argues that the proposed solutions disproportionately harm Lido and instead proposes a deposit fee when Lido’s stETH share is above a certain threshold. However, Cobie presents a strong argument that changing fee structures for users who can’t exit is potentially fraudulent. He also points out that if a system requires DApps to act altruistically, it probably won’t survive when mercenary capital enters the space.

- Our Position: Although we are sympathetic to both views in this debate, we generally agree with Cobie and Adam’s arguments. Lido’s validator set, which uses the ETH, is generally decentralized, with the ETH spread around to different validator groups. And as Cobie says, if a protocol needs to limit itself for the base layer’s security, the base layer is fragile and won’t survive mercenary capital entering the space. Lido actively limiting itself until competitors show up seems short-sighted, as those competitors may not act altruistically and would seek to monopolize liquid staking. Instead, Lido should develop the internal ‘guardrails’ that users in the forum have mentioned and Lido is currently working on. Another consideration against the threat of Lido centralization is if someone gained control of the network through Lido and enacted damaging practices like multi-block reorgs, or censoring transactions, it would most likely kill the value of the network. This would reduce the value controlled by the validators and potentially cause capital to flee the ecosystem. So taking over a Lido monopoly may be feasible, but there doesn’t seem to be much incentive. We have tried our best to summarize this debate, but we have not done it credit here. We highly recommend that anyone holding ETH, stETH, LDO, or any Ethereum token give this thread a read. Ethereum’s move to PoS affects the entire network, especially how it intersects with liquid staking, and those interacting with it or holding wealth secured by it should follow this thread.

- For more, Delphi members can see the full DAO Insights here.

Glass Half Full on OPtimism

[Excerpt from a Delphi Pro Report]

- OP launched with an initial total supply of 4.3B tokens inflating at 2%/year. 1.3B tokens (~30% of the supply) will be unlocked initially and consists of:

- Airdrop 1: 215M

- OP Stimpack Phase 0: 36M

- OP Stimpack Phase 1: 195M

- RetroPGF: 859M

RetroPGF

- The main responsibility of the Citizen’s House is the governance of retroPGF. This fund retroactively distributes funding to projects which guarantee a form of compensation for good actors. The mechanism was initially set forth by Vitalik who describes the motivation behind it as “it’s easier to agree on what was useful than what will be useful.” The goal of retroPGF is to financially incentivize the development of public goods in a sustainable and objective way. Public goods can be thought of as products/services that although many want to use no one wants to pay for; oftentimes due to the free-rider problem.

- The first iteration of retroPGF distribution was Oct 2021 when $1M was distributed to 58 projects. Top reward recipients included $51k to Ethersjs (compact, feature-complete library to interact with the Ethereum blockchain) and $45k to go-ethereum (Go implementation of the Ethereum protocol). Both projects are free resources that have all bettered the Ethereum community while operating with no expected rewards.

- As a self-operating mechanism, it’s vital for RetroPGF to generate sustainable revenue. This begs the question of where these funds come from. There are 3 revenue sources in play here:

- 20% of the initial OP supply + 2% yearly inflation: This initial allocation is distributed at the discretion of the Citizens’ House.

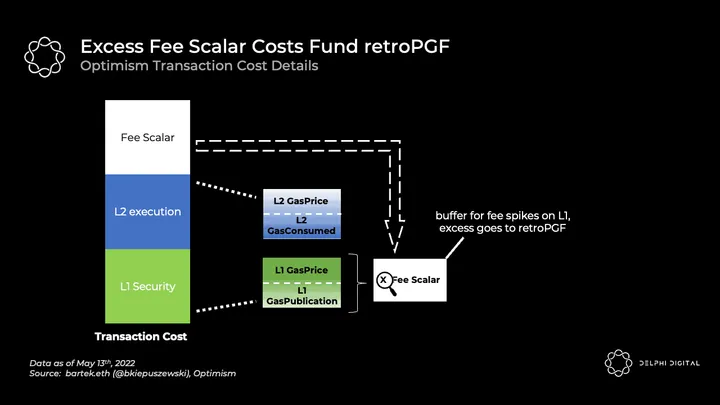

- Fee Scalar: a multiplier on the estimated L1 security cost (currently set at 1.5x) to account for Ethereum’s gas price volatility. Sometimes there’s no discrepancy in gas costs and the charged premium is left unused. Rather than being returned to the user, excess fees go directly to funding retroPGF.

- For more, Delphi Members can see the full Delphi Pro Report here.

Notable Tweets

Ropsten Testnet to Merge

📣 Ropsten Merge Announcement 📣

Ethereum’s longest lived PoW testnet is moving to Proof of Stake! A new beacon chain has been launched today, and The Merge is expected around June 8th on the network.

Node Operators: this is the first dress rehearsal💃

— Tim Beiko | timbeiko.eth 🐼 (@TimBeiko) May 30, 2022

DeFi Saver Launches on Arbitrum & Optimism

We’re LIVE on

@Arbitrum

and

@OptimismPBC

!🥳DeFi Saver is now available on optimistic rollups with support for

@AaveAave

v3, new integration with

@LiFiprotocol

and our regular partners

@0xProject

,

@AlchemyPlatform

and

@TenderlyApp

.#L222 is here.

Read:

— DeFi Saver (@DeFiSaver) May 31, 2022

Velodrome on Optimism

Velodrome is an AMM designed as the central trading and liquidity marketplace on

@optimismPBC

.It is the next evolution of the

@solidlyexchange

model introduced by Andew Cronje.Launching on May 31st with 10+ partners, it will kick start #OPSummer.

Need a 101?👇🧵

— Velodrome (🚴,🚴) (@VelodromeFi) May 29, 2022

0 Comments