Ethereum Futures Funding Rates Decline as Traders Turn Bearish

AUG 30, 2022 • 4 Min Read

🚨 In Case You Missed It

- Meta expands NFT rollout to Facebook, allowing select users to share NFTs across Facebook and Instagram.

- Temasek Holdings, Singapore’s sovereign wealth fund, announces $100M investment in Animoca Brands.

- Crypto.com accidentally transfers $10.5M to customer asking for a $100 refund.

- Alexis Ohanian, co-founder of Reddit, plans to raise $177.6M for a crypto fund.

📊 Ethereum Futures Funding Rates Decline as Traders Turn Bearish

- Funding rates for perpetual futures on ETH hit a low of -0.024% on August 27th. This level was last seen in June-2021 and was followed by a massive short-squeeze in July-2021.

- Funding rates are periodic payments made to/by long or short traders based on the difference between perpetual contract prices and spot market prices.

- When rates are positive, long traders pay short traders. This implies that traders are generally bullish as they are willing to pay the funding rate to keep their long positions open. On the other hand, negative rates imply that traders are generally bearish.

- Perpetual futures open interest is also rising since the June capitulation, peaking at $6.8 billion on August 13th. Open interest has remained above $5 billion, most of which is likely to be short as funding rates have flipped negative from August 14th.

- Negative funding rates may also indicate that traders are hedging spot ETH positions to remain delta neutral. This is a popular strategy that allows spot ETH holders to mitigate any downside risk heading into the Merge, while still collecting any airdrop from a potential proof-of-work hard fork.

- The upcoming Merge is divided into two stages, beginning with a network upgrade called Bellatrix on September 6th.

- Later, the Paris upgrade will shift the execution layer from proof-of-work to proof-of-stake when the Terminal Total Difficulty (TTD) reaches a value of 58750000000000000000000. This is expected to occur between September 10-20th. You can track the TTD and remaining time until the Merge here.

- For more on post-Merge Ethereum, Delphi members can read our Delphi Pro report here.

⚡SushiSwap’s Lingering Troubles

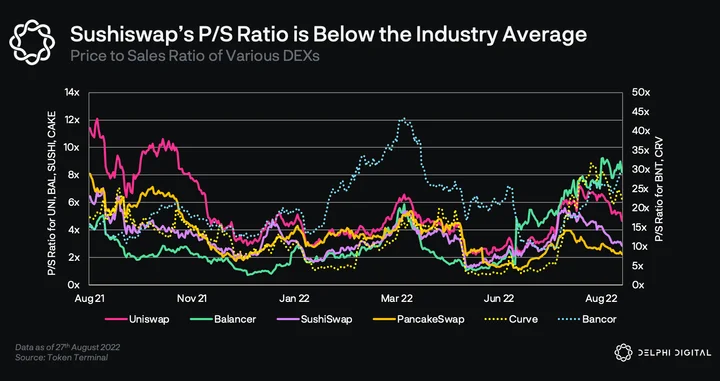

- From a valuation perspective, SUSHI trades at a discount to its peers. Its price-to-sales ratio is ~3x compared to Uniswap’s 5x and Balancer’s 8x.

- While this may be viewed as relatively cheap, it also reflects its declining fundamentals and indicates lower growth and low investor confidence in the future.

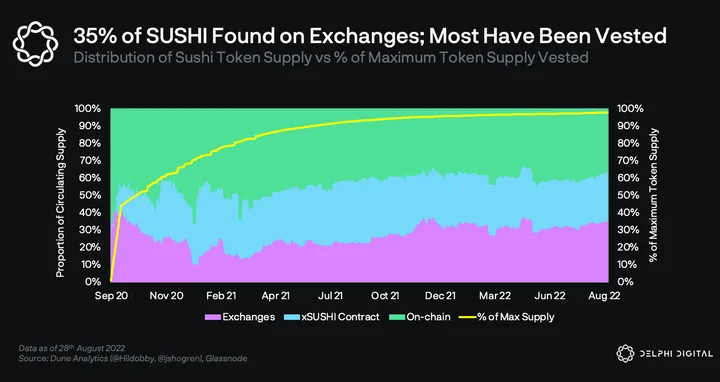

- Another reason for the depressed price could be sell pressure from liquidity mining rewards, which has certainly contributed to SUSHI’s 95% decline from ATHs.

- A considerable amount (35%) of circulating SUSHI is found on centralized exchanges, and the remainder is held on-chain.

- Vested SUSHI rewards began to unlock and finished vesting in October 2021. This likely resulted in an increase in centralized exchange balances during that period.

- Currently about 28% of SUSHI is staked in the xSUSHI staking contract where stakers earn a cut of trading fees. This number is down from 35% during the same time last year.

- The total dollar value of SUSHI staked in the xSUSHI contract decreased exponentially due to the price drop of the SUSHI token, but returns on staking have stayed fairly consistent in the high single digits.

- For more on Sushi, Delphi members can read our Delphi Pro report here.

🐣 Notable Tweets

App Chains for On-Chain Order Books

1/ IMO there’s essentially no way to make the economics of an on-chain order book sustainable. At least in a general purpose chain

IMO the only solution is an order book specific appchain with application aware pricing. A general purpose chain can’t profitably host an order book

— Doug Colkitt (🐊,🐊) (@0xdoug) Aug 30, 2022

Bots in Web3 Games

after analyzing 60+ games and services, we found 200 000 bots. on average, every web3 game has 40% bots.

link to the database with the results at the end of a thread 🧵

— Levan (@LevanKvirkvelia) Aug 30, 2022

Bull Thesis on Cosmos Hub

1/ Cosmos Hub – A Rising Tide Lifts All Cosmos Boats 🚤🪐

Cosmos Hub is getting a major facelift and the entire ecosystem is underestimating it. My thesis is that the Cosmos Hub 2.0 upgrade, ICS & ICA will start a sustained bull market in the Cosmos ecosystem in 2023.

A 🧵

— Xave Meegan (@0xave) Aug 29, 2022

Get access to complete market coverage, institutional-grade reports, calls with our analysts and access to the Delphi community.

Sign up for Delphi Pro here.

0 Comments