Exploring Base's Role in the Growing Onchain Economy

NOV 26, 2024 • 35 Min Read

Report Summary

The report titled “Base – Onchain Economy Report” highlights the explosive growth of the onchain economy in 2024, emphasizing the role of Layer 2 (L2) solutions like Base in driving innovation and adoption. Below are the key takeaways:

1. Onchain Economy Growth:

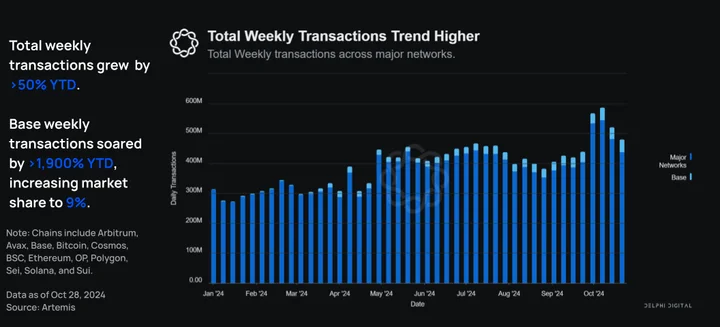

- Transactions & Activity: Onchain weekly transactions increased by over 60% YTD to 531M, with Base’s daily transactions surging 1,900% to 7.7M.

- Active Addresses: Weekly active addresses across major networks grew 240% YTD to 65.6M; Base’s weekly active addresses increased 2,100%, reaching 6.5M.

- TVL Expansion: Total Value Locked (TVL) in the onchain ecosystem rose by 110% to $87.9B, with Base’s TVL increasing by 470% to $2.77B.

2. Diverse Onchain Use Cases:

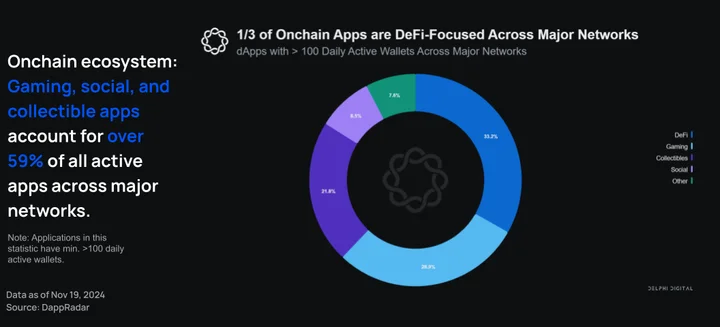

- Non-DeFi Applications: 66% of active onchain apps are non-DeFi, including gaming, social, and digital collectibles.

- NFT Evolution: Base saw a 500% increase in NFT mints, signaling a shift from speculative trading to utility-driven use cases.

3. Stablecoin Surge:

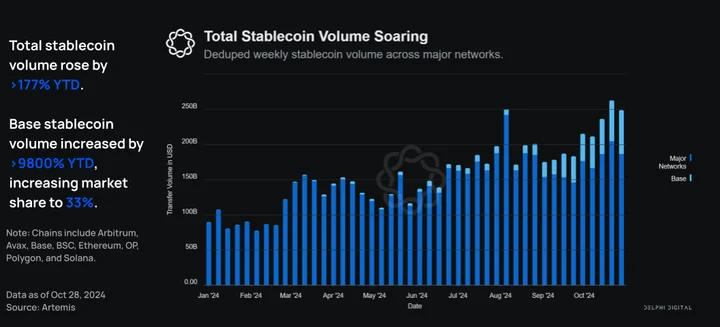

- Market Growth: Weekly stablecoin volume increased 235% YTD to $302B, with Base capturing 33% of the market share.

- Base Stablecoins: Base’s stablecoin market cap grew by 1,800% YTD to $3.3B.

4. Institutional Adoption:

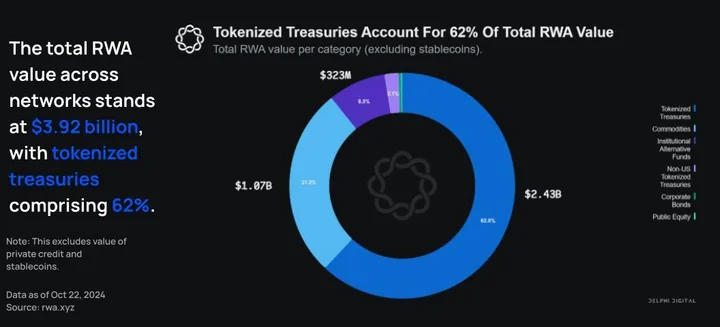

- Real-World Assets (RWAs): RWA value grew 50% YTD to $13.25B, with tokenized treasuries making up 62%. Base is positioned to capture future RWA growth.

5. Base’s Rapid Growth:

- Transaction Affordability: Base fees dropped 95%, enabling sub-cent transactions, fueling activity and adoption.

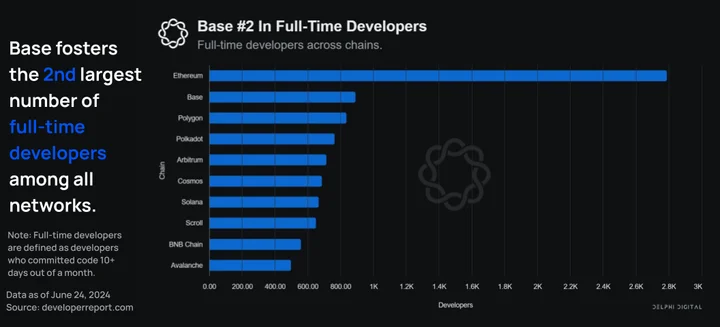

- Developer Ecosystem: Base ranks #2 in active full-time developers (900+), fostering app diversity and innovation.

6. Emerging Sectors:

- Gaming: Games like Frenpet are driving adoption through simple, accessible experiences.

- DeFi: Protocols like Aerodrome dominate DeFi on Base, accounting for over 40% of its TVL.

- Social Apps: Projects such as Farcaster Frames expand composable, onchain social interactions.

Conclusion:

The onchain economy is evolving beyond speculation, driven by innovations in stablecoins, Layer 2 solutions, and diverse use cases. Base’s success exemplifies this shift, with its growth in user activity, application diversity, and infrastructure signaling a thriving and maturing ecosystem.

Key Takeaways

- Onchain key metrics across major networks*

- >60% YTD increase in total weekly onchain transactions, to 531M

- 240% YTD increase in Weekly Active Addresses, to 65.6M.

- 110% YTD increase in TVL, to $87.9B.

- New onchain use cases beyond financial speculation are evolving:

- 66% of all active onchain applications are non-DeFi, such as gaming, social, and digital collectibles. DeFi apps account for 33% of onchain apps on major networks.

- Onchain stablecoin weekly volume has increased over 200% YTD:

- Weekly stablecoin transfer volume is at 302B, up >235% YTD.

- Stablecoin market cap has reached $186.2B, up 38% from $134B in January.

- Base stablecoin market cap has reached $3.3B, up over 1,800% from $170M in January.

- Institutional adoption of RWAs:

- Total real world asset value, excluding private credit, stands at $3.92B across major networks – with tokenized treasuries comprising 62%.

- Year-to-date, the total value of RWAs is up over 50%, from $8.3B to $13.25B.

- Base onchain activity metrics are soaring YTD:

- Base daily transactions are up 1,900%, ascending from 372,000 to over 7.7M in November.

- Base weekly active addresses increased by 2,000%, to 6.5M.

- Base activity growth has been driven by a 95% decrease in average transaction fees since January.

*Included major networks: Bitcoin, Ethereum, Solana, Arbitrum, Avax, Base, Binance Smart Chain (BSC), Cosmos, Optimism, Polygon, Sei, and Sui.

Data in Key Takeaways is updated through November 19, 2024. Most data throughout the report below covers the period from January 2024 to October 2024.

Introduction

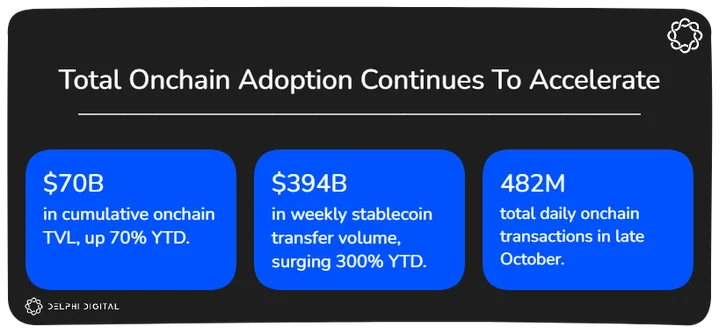

The onchain economy has grown significantly in 2024, with daily transactions up more than 50% YTD, and a 70% increase in onchain total value locked (TVL), bringing the total TVL across major networks to over $70 billion. These major networks include Bitcoin, Ethereum, Solana, Arbitrum, Avax, Base, Binance Smart Chain (BSC), Cosmos, Optimism, Polygon, Sei, and Sui. The WEF predicts that 10% of the global GDP will be onchain by 2027, further supported by reports from the IMF and World Bank about a global shift towards digital infrastructure.

This report dives into the recent growth of the onchain economy as of October 2024, and analyzes several use cases behind that growth, including stablecoins, layer 2s (L2s), collectibles, social media, gaming, DeFi, and institutional adoption. Overall, the data is clear: the onchain economy is growing rapidly.

This report also dives into the recent growth of Base, an Ethereum Layer 2 (L2) incubated by Coinbase which has since seen significant growth since it launched its mainnet on August 9, 2023.

“Base is a secure, low-cost, builder-friendly Ethereum L2 built to bring a billion users, and a million developers onchain, with an ecosystem of onchain applications.”

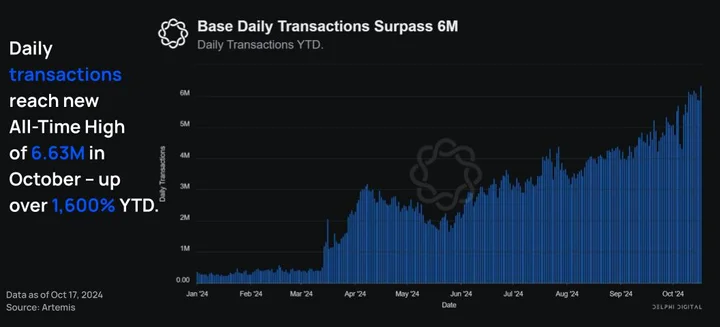

In the ~1 year the chain has been live, it has positioned itself at the forefront of the L2 space. During this time, the Base team has contributed to several onchain advancements: driving rollup transactions to sub-cent fees through EIP-4844, creating smart wallets to ease account abstraction, contributing to the Superchain stack, and plenty more. Daily transactions on Base are up 1,600% since the start of January, ascending from 372,000 to over 6.63M in October. Across many of the metrics analyzed, Base is growing faster relative to the total onchain economy, such as TVL, active addresses, and transactions.

The growth of the onchain economy extends beyond financial speculation. 66% of all active onchain applications are non-DeFi, such as gaming, social, and digital collectibles. DeFi apps account for 33% of onchain apps on major networks.

With new use cases continuing to emerge, and developers and users continuing to come onchain, the onchain economy is poised to accelerate in the coming months and years.

Total Onchain Economy

Total Onchain Metrics

Total Onchain TVL

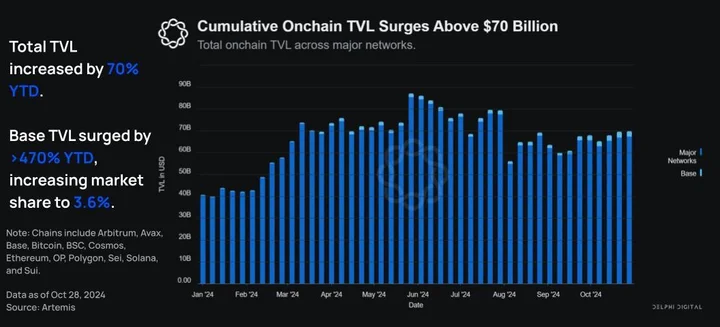

Total Value Locked (TVL) is a metric used to assess the amount of capital allocated into smart contracts on a specific network. Year-to-date, cumulative TVL across networks has increased from $41B to >$70B, a gain of 70%. As of November 19, 110% increase in TVL, to $87.9B.

As total TVL onchain surges, Base’s growth in particular stands out. Base onchain TVL increased from $439M in Jan. 2024 to $2.51B at the end of Oct. 2024 – a 470% increase. Subsequently, Baseʼs market share rose from 1.07% of total onchain TVL to 3.59%.

It is worth noting that while onchain growth is being driven by Base, this is primarily in the form of active addresses and stablecoin volume. This is because onchain TVL on Base remains relatively low compared to other major networks – reflecting the greater mix of non-monetary use cases on Base.

This significant uptick originates from the Base’s general increased usage, but more specifically, the rise in popularity of Aerodrome, which is currently >40% of the TVL on Base.

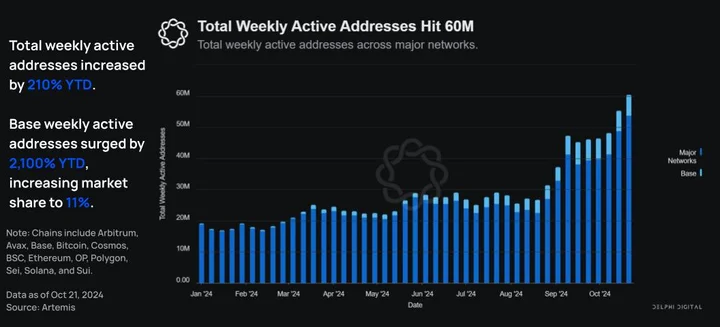

Total Onchain Active Addresses

Year-to-date, total weekly active addresses have gone from 19.3M to ~60M, an increase of 210%. As of November 19, 240% increase in Weekly Active Addresses, to 65.6M.

Note: As a reminder, active addresses refer to active interacting addresses of projectʼs revenue-generating smart contracts over a given period of time. Active Addresses do not equate to weekly active Users, as users may create and operate multiple wallet addresses.

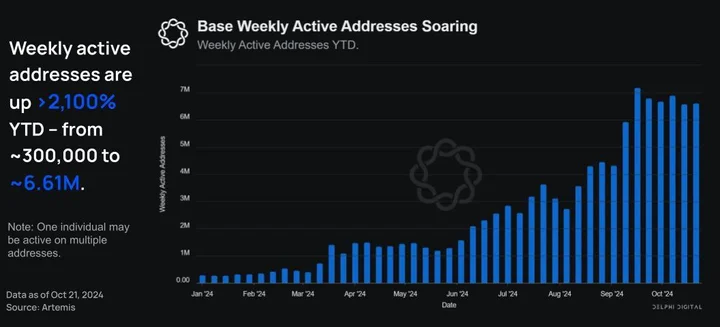

Simultaneously, Base has gone from 300,000 weekly active addresses in January to 6.61M at the end of October, an increase of 2,100%. This has increased Baseʼs market share of total onchain weekly active addresses from 1.6% to 11%.

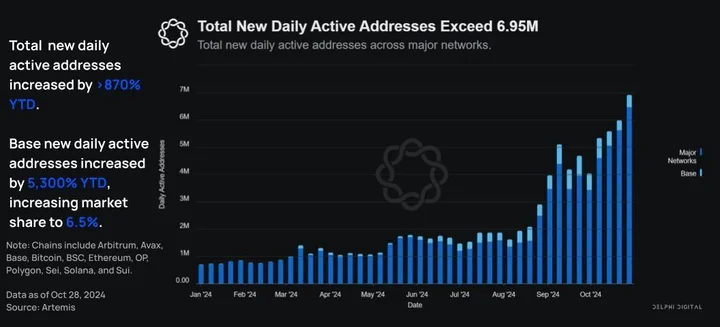

Note: Daily new addresses refer to newly created interacting addresses on a 24h rolling period, which interact with revenue-generating smart contracts. These addresses have previously not denoted any onchain activity on the network.

Year-to-date, total new daily active addresses have gone from 710,000 to 6.95M, a gain of 879%.

In the same timeframe, Base went from 8,320 new daily active addresses at the start of the year to 450,000 at the end of October, a gain of 5,300%. This has increased Baseʼs market share from 1.2% to 6.5%.

Total Onchain Transaction Count

Transaction count is quantified by assessing the number of transactions made in a given timeframe.

Year-to-date, cumulative weekly transactions have gone from 315M at the start of the year to 482M, a gain of over 50%. As of November 19, >60% YTD increase in total weekly onchain transactions, to 531m.

In the same timeframe, Base has gone from 2.1M daily transactions at the start of the year to 42.34M at the end of October, a gain of over 1,900%. This has increased Baseʼs market share from .67% to 9%.

The large increase in Base daily transactions is indicative of the network’s rising popularity and affordability, but the broader trend also emphasizes that Base can be successful while enabling other networks to be successful (e.g., other networks in the Superchain).

Total Deduped Stablecoin Volume

One key area of onchain economy growth is stablecoins, which enable onchain assets to move seamlessly around the world at a fraction of the cost of traditional finance. Year-to-date, total deduped onchain stablecoin weekly volume has gone from $89.7B to $249B, a gain of over 177%.

As of November 11, weekly stablecoin transfer volume is at 302B, up >235% YTD.

Note: Deduplicated stablecoin volume is quantified by assessing the cumulative sum of stablecoin transfer values while removing duplicates. The removal of duplicates is integral to analyzing an accurate volume figure. A duplicate is a transfer deemed to be uneconomic activity, such as CEX transfers, bot activities, wash trading, and non-payment wallet transfers.

Stablecoin growth is also rapidly accelerating on Base: in that same timeframe, Base’s cumulative weekly stablecoin volume went from $620M at the start of January to $62B at the end of October, a gain of >9,800%. This has increased Baseʼs market share from 0.7% to 33%, a multiple of 47x.

As of November 11, Base’s cumulative weekly stablecoin volume increased from $620M at the start of January to $55B in November, a gain of >8,800%. This has increased Base’s market share from .7% to 18%.

This increase in Base stablecoin volume is representative of Base’s efforts to increase network capacity while driving down costs. As a result, Base is well positioned to process mass payments between consumers and merchants utilizing stablecoins as a universal medium of exchange.

Institutional Adoption

Institutional adoption of onchain public permissionless networks is integral to the long term success of the broader crypto ecosystem, and is in its early innings. Bitcoin and Ethereum Spot ETFs were approved in January and June 2024, but have already seen massive adoption– surpassing $24B total net flows. While we expect the ETF trend to grow considerably from here, this is merely Web2 wrapping Web3 products. Tokenization, which can be thought of as moving traditional web2 assets natively onchain is the future for Institutions and is seeing tremendous attention across both world governments and the private sector. In order to access all of web3, institutions require scalable, secure, and appropriately licensed market infrastructure.

Total RWA Value

Real-world assets (RWAs) are digital tokens that represent physical assets or financial instruments on a blockchain. This includes things like real estate, art, and commodities. Tokenizing RWAs onchain allows for fractional ownership and opens up new possibilities for trading, investing, and ownership. The growth of RWA is one key driver behind onchain economy growth.

Several different metrics can be assessed to determine the growth of institutional adoption. Presently, the best metric to view is total RWA growth, as it depicts real capital at stake onchain.

- Total real world asset value, excluding private credit and stablecoins, across networks stands at $3.92 billion, with tokenized treasuries comprising 62%.

- Year-to-date, the total value of RWAs is up over 50%, from $8.3B to $13.25B.

- Ethereum secures >$3B in RWAs.

The data from RWA.xyz shows that RWAs are seeing considerable growth and will continue to increase as more institutions come onchain.

Breakdown of Rise in Tokenized Value by Category

With the successful approval of Bitcoin Spot ETFs, the institutional focus has shifted to the tokenization of RWAs.

A famous quote from Larry Fink, the CEO and Founder of BlackRock, summarizes the institutional sentiment quite well:

“ETFs are step one in the technological revolution

in the financial markets, step two is going to be

the tokenization of every financial asset.ˮ

There have been major pushes to tokenize financial assets and allow it to benefit from access to a non-restricted onchain economy. As seen by major traditional finance institutions like Blackrock and Franklin Templeton, who have begun to issue RWAs onchain.

Currently, Tokenized Treasuries make up the bulk of issued RWAs, with commodities second:

As of November 19, total real world asset value, excluding private credit, across networks stands at $3.92B, with tokenized treasuries comprising 62%.

The rise in tokenized treasuries has mainly been on the Ethereum L1, surpassing $1.5B. Only $4.5M in tokenized treasuries have been issued on Base, but this area is ripe for growth. As the network matures and further decentralizes itself through achieving the next stage (stages are decentralization levels), Base will be well-positioned for the influx of assets coming onchain.

Onchain Developers

Onchain developers are a key part of the onchain ecosystem– an active developer ecosystem fosters the creation of innovative applications that can attract users to a network and retain them.

Commonly, the number of full-time developers on each chain is seen as the most important metric gauging developer activity. As of the latest Developer Report from 6/24, Base ranks #2 with over 900 total active full-time developers, only behind Ethereum with ~2800.

Note: Full-time developers are defined as developers who committed code 10+ days out of a month.

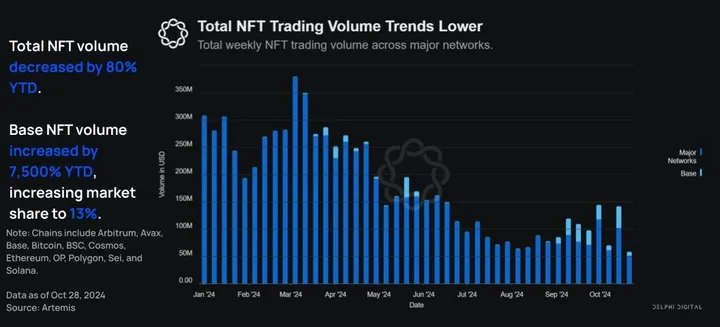

Total Onchain NFT Trading Volume

NFT Trading Volume is quantified by calculating the sum of NFT trading volume in the given timeframe. Year-to-date, cumulative weekly NFT volume has decreased from 309M to 59M, or ~80%.

In that same timeframe, base cumulative NFT volume has gone from ~100,000 at the start of January to 7.66M, a gain of over 7,500%. This has increased Baseʼs market share from .003% to 13%. This NFT growth on Base is primarily driven by the promotion of free or low-cost NFTs, rather than speculative NFT trading activity, indicating a shift in the focus of the NFT market in recent years.

While NFT trading volume across the major networks has been trending lower because of market conditions and many high-profile NFTs going down ~80% in value, Base NFT volume is up significantly. This is largely because Base NFTs were practically nonexistent at the start of the year, and now their volume figure is more in line with the overall market for NFTs.

Deep-Dive on Base

In general, Base is seeing accelerated growth at a time when the entire onchain space is growing. More importantly, Baseʼs market share across all analyzed metrics have increased by multiples year-to-date, showcasing the chainsʼ stark relative strength as well as outperformance in regards to economic growth and user adoption.

For example:

- Daily transactions are up 1,600% since the start of January, ascending from 372,000 to over 6.63M in October.

- > 50% YTD increase in total daily transactions.

- >2100% YTD increase in weekly active addresses.

- >70% YTD total-value-locked increase.

This is also a testament to the effort Base and other development teams have made to build beneficial applications and networks boosting the growth of the total onchain economy.

While Base is growing faster than other networks across all following metrics, it should be noted that most major networks have seen an uptick in usage year-to- date, indicating that the collective effort to bring people onchain is benefiting all networks.

Increase in Base User Activity Year-to-Date

The data from January 2024 to October 2024 tells a singular story: Base adoption is skyrocketing.

Weekly active addresses and transactions on Base are steadily increasing, up >2,100% and >1,600% respectively from January to October 2024. Impressive progress showing that Base is effectively onboarding users, and expanding onchain adoption globally.

Itʼs important to note that weekly active addresses do not equate to weekly active users, as users may create and operate multiple wallet addresses, meaning the correspondence is not 1:1. Nonetheless, it serves as a useful metric for assessing a chainʼs overall activity level, especially when filtering for addresses interacting with revenue generating smart contracts as done throughout this report.

In 2024, weekly active addresses on Base surged from 300,000 in January, to 6.61M by the end of October, peaking at an all-time high of 7.19M on September 16. This growth represents a year-to-date increase of over 2,100%.

Note: Base weekly active addresses refer to the number of unique addresses which have interacted with a revenue-generating smart contract deployed on Base. One individual may be active on multiple addresses.

As of November 19, Base weekly active addresses increased by 2,000%, to over 6.5m.

These initiatives have successfully fostered an evolving ecosystem. Combined with the massive reduction in transaction fees post EIP-4844 (typical fees are now <1 cent), Base has become a very attractive chain to interact with both from a user and developer perspective.

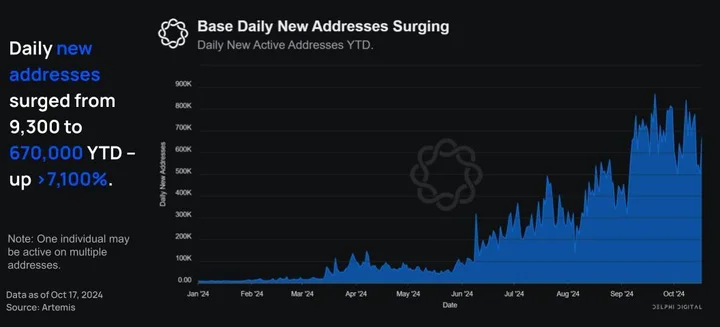

Year-to-date, Base daily new addresses have grown from 9,300 in January to 670,000 by the end of October after reaching an all-time high of 867,700 on September 20th. This growth marks an increase of over 7,100% since the start of the year.

Note: Base daily new addresses refer to the number of new addresses which have interacted with a revenue-generating smart contract deployed on Base for the first time (not indicating any prior onchain activity on Base).

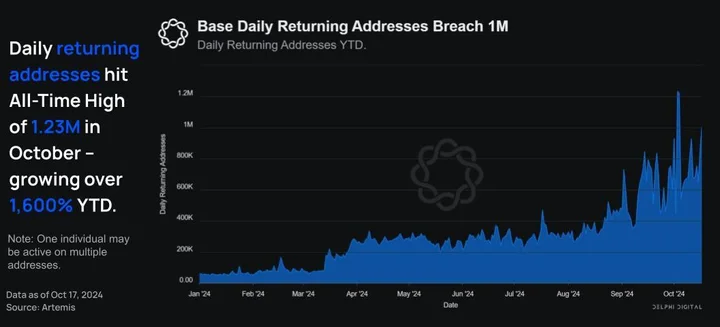

Simultaneously, Base’s daily returning addresses rose from 59,000 in January to over 1M in October – with a peak of 1.23M on October 3rd. Equivalent to a year-to-date increase of over 1,600%, a strong sign of robust user retention on top of explosive activity growth.

Note: Base daily returning addresses refer to the number of interacting addresses which have previously interacted with a revenue-generating smart contract deployed on Base.

An example of driving onchain activity on Base is the Onchain Summer initiative, a program designed to celebrate and showcase onchain innovation – including for music, art, food, and gaming. The initiative encourages participation by showcasing compelling onchain projects in Base’s ecosystem. This effort contributed to bringing users onchain, as evidenced by the surging growth in onchain activity.

Another element supporting Base’s success are diverse marketing campaigns spanning wide target audiences, such as advertisements on Liquid Death boxes to promote onchain activity.

Separately, Coinbase has launched cbBTC, a wrapped Bitcoin token, on Base. By prioritizing cbBTC adoption on Base, they helped solidify Base as the leading ecosystem for the most secure onchain, wrapped Bitcoin.

Initiatives like cbBTC and Onchain Summer help to bring the masses onchain. And once they are here, they stay, as highlighted by the returning active addresses.

Growth in Base Transactions driven by decreasing fees

Unsurprisingly, daily onchain transactions have soared alongside the rise in active addresses.

As of November 19, daily transactions are up 1,900%, to over 7.7M.

In particular, daily transactions are up 1,600% since the start of January, ascending from 372,000 to over 6.63M in October. Seeing similar trends on both the active addresses & transactions proves that the Base economy is becoming the onchain hub in the rollup landscape.

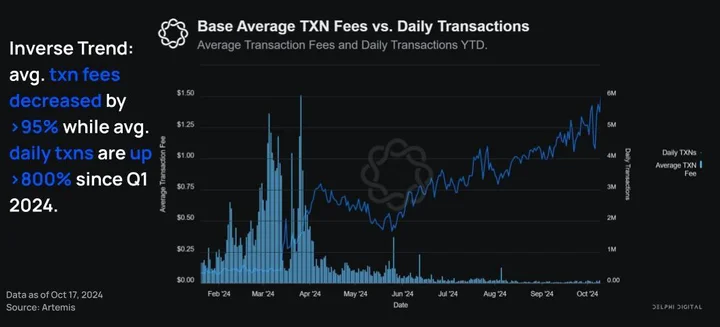

Contrary to web2 dynamics, the cost of doing business on Base has decreased despite soaring demand. The average transaction fee on Base decreased from $0.44 in Q1 to $0.019 as of October 17, a drop of over 95%. While this is in part because of EIP-4844, the scaling efforts Base has been making (such as raising the gas limit) play an important role in driving costs down.

To put it into perspective, the average transaction fee has decreased by over 95% year-to-date while average daily transactions surged by 800%, from 615,000 in Q1 to 5.6M average daily transactions in October. These low fees make onchain technology more accessible, and encourage more builders and users to come onchain.

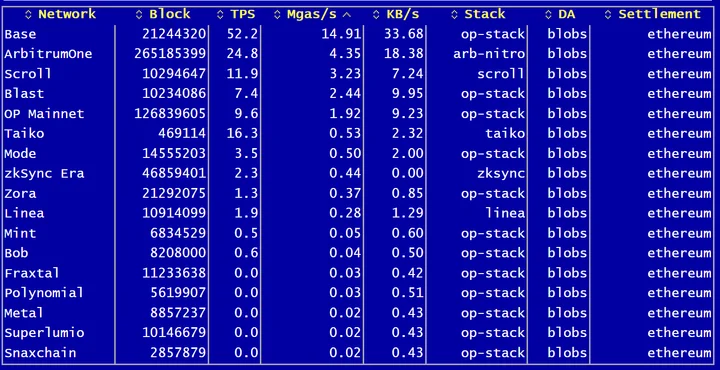

On a different note, Base is currently the #1 gas consumer of rollups using blobs, consistently having > 50 transactions per second and >13 mgas/s of consumption.

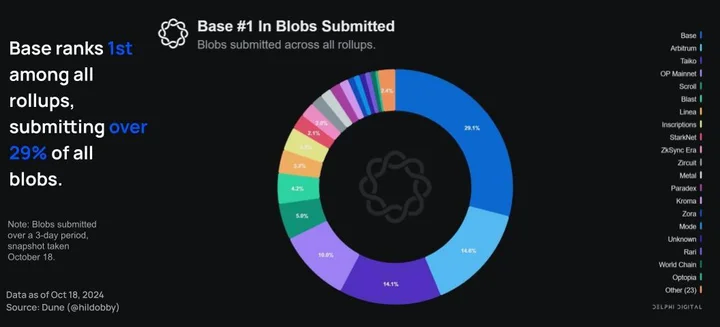

Base’s submissions of >29% of all blobs showcase the substantial demand for Base blockspace, a result of the chain’s explosive growth.

However, this may pose issues in the future. If the maximum number of blobs is not increased in a future upgrade, the current cap may hinder Base’s growth.

Growth in Base Economic Value and Total Value Locked Year-to-Date

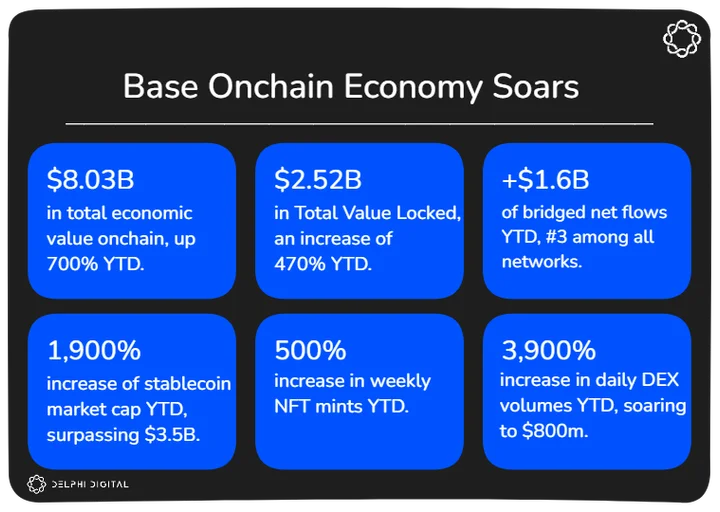

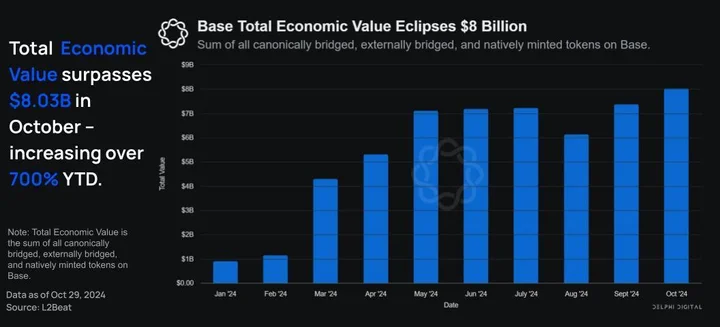

Year-to-date, Base total economic value is up from $900M in January to $8.03B at the end of October, a 792% increase. This figure positions Base as the second-largest L2 by this metric, ranking only behind Arbitrum.

Note: Total Economic Value refers to the sum of all canonically bridged, externally bridged, and natively minted tokens

Notably, this type of growth is unmatched and is the fastest a network has accumulated over $8B in Total Economic Value (only 16 months!). We anticipate this chart in economic value to maintain itʼs course as rollups are expected to continue seeing significant inflows over the next few years.

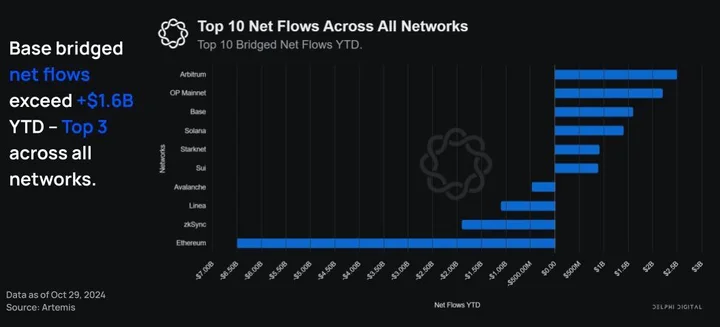

Furthermore, Base is #3 in net flows (nominal, not %) with $1.6B year-to-date across all networks, while Ethereum saw net outflows of $6.5B. It is important to acknowledge, that the majority of outflows experienced by Ethereum were mainly capital migrations to rollups, indicating that capital flow largely stayed within the EVM ecosystem rather than moving outside it.

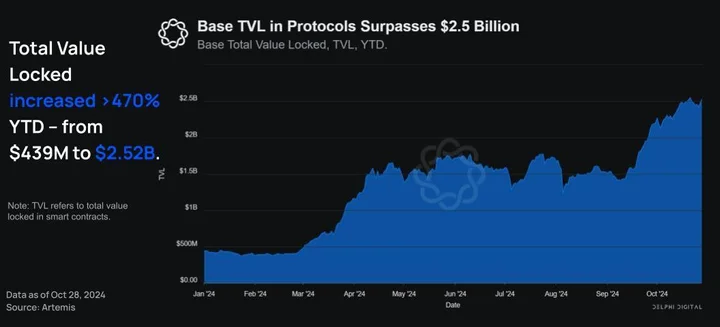

Year-to-date, Base TVL in protocols has risen from $439M in January to $2.52B at the end of October, a 470% rise. As of November 8, Base’s TVL has exceeded $2.77 billion, making it the leading L2 by Total Value Locked.

A ratio to monitor is TVL / Total Economic Value, as a healthy ecosystem will have both metrics growing at similar rates.

Diving deeper, by directly comparing each metric, a picture about the overall distribution of onchain activity can be painted. A similarity in values between TVL and Total Economic Value suggests that most capital is locked in protocols and smart contracts, indicating high DeFi activity. On the other hand, if Total Economic Value significantly exceeds TVL, it suggests that onchain activity extends beyond DeFi, highlighting a more diverse distribution — such is the case for Base.

Increasing Stablecoin Market Cap on Base

By all the aforementioned metrics and plenty more, Base is the fastest-growing L2.

Another interesting way to quantify a networkʼs ‘successʼ is to track the overall market cap of stablecoins on the network.

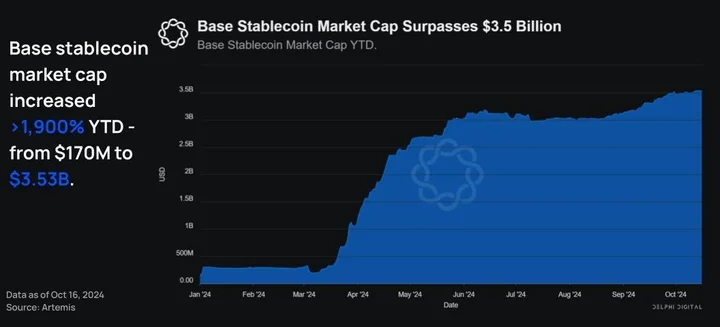

Year-to-date, the Base Stablecoin Market Cap is up over 1,900% from $170M in January to $3.53B at the end of October. This represents a substantial increase in both nominal value and percentage.

As of November 19, Base Stablecoin market cap stands at $3.3 billion (up over 1,800% from $170M in January), within an overall stablecoin market cap of $186 billion (up 38% from $134B in January).

Notably, the percentage increase surpasses that of economic value over the same period, indicating that the Base ecosystem is not only growing but starting to mature.

Base Onchain App Ecosystem

A variety of use cases beyond DeFi

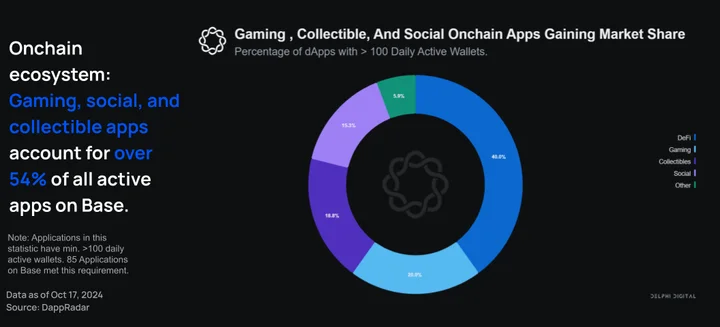

Alongside the rapid increase in users and transactions, the number of projects launched on Base has also been steadily increasing. A sign of a healthy network is a flourishing ecosystem, evidently achieved by Baseʼs commitment to providing an unmatched developer experience. As of October 17, 2024, there were 85 apps active on Base with >100 daily active wallets.

More than 60% of all onchain applications on Base are non-Defi related: 20% are gaming apps, while collectibles make up 18.8%, social apps 15.3%, and ‘otherʼ 5.9%.

As shown above, while DeFi apps are leading the charge as a single category, areas such as Gaming and Collectibles are also seeing significant usage accounting for over 54% of all active apps on Base.

This diversity of onchain applications shows that Base is more than just a DeFi hub. It’s a space where all types of onchain apps can flourish and a true economy can take shape. This is further supported by the growth of applications like FrenPet, which focuses on gameplay over monetary benefits.

Base application diversity is roughly similar to the cumulative application diversity across major networks supported by DappRadar.

This mix of utility provided by dApps shows that users are beginning to embrace all types of onchain applications. This is a healthy sign for the onchain ecosystem, with increased diversity beyond monetary-focused applications.

Supporting Ease of Use & Cost-Efficiency

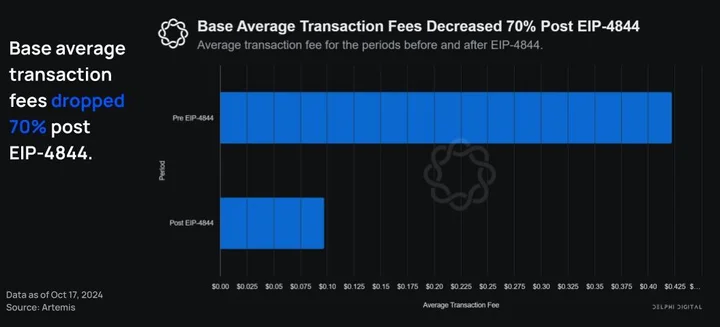

Splitting the year into two periods, post and pre EIP-4844, average transaction fees for users are down 70% from $.422 to $.097 post EIP-4844.

As mentioned earlier, transaction fees on base have dropped by 70% post-EIP 4844, which has driven a rapid increase in transaction volume. The continued increases in cost-efficiency will unlock a significant expansion in onchain use cases, and help bring new users onchain.

As transactions become cheaper it becomes more feasible for onchain apps to abstract gas fees away altogether. By apps covering minimal transaction fees via paymasters, users will not have to think about having ETH for gas.

However, Base is not the only L2 where users are seeing reduced fees. The development work Base contributes to outside of its own rollup (specifically EIP-4844) benefits all rollups.

The biggest kicker with cheap transactions is the ability for onchain apps to abstract gas fees away through paymasters. Through apps covering the transaction fee themselves (at a minimal cost per transaction), users do not need to think about having ETH for gas.

This simplifies the onboarding experience for new users. If full abstraction is indeed in the future – where onchain user experience closely mirrors that of web2 by streamlining it to the extent that users are unaware they are interacting with a blockchain – then applications will be able to absorb gas fee costs without meaningfully impacting their profitability.

As fees on Base continue to trend lower and approach the cheapest, economically feasible cost, the possibilities for onchain exploration are near endless.

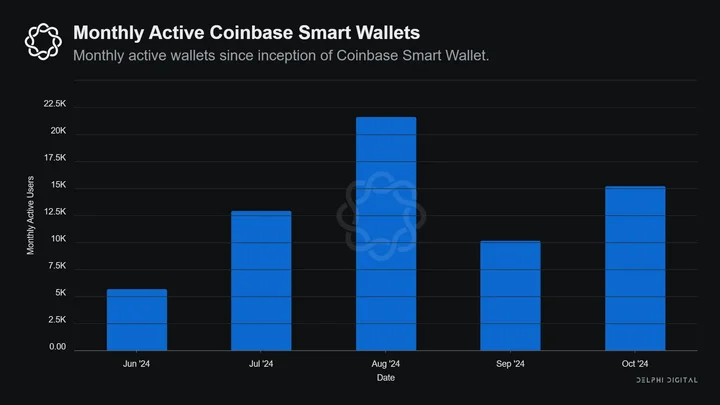

Increasing Adoption of Coinbase Smart Wallet since Inception (June 2024)

Launched in June 2024, the Coinbase smart wallet is a state-of-the-art wallet built to optimize UX and simplify onboarding. There are no extensions/installations needed, passkeys are utilized instead of complex seed phrases, and the wallet works across most major networks. Smart wallet shortens the user journey to get onchain to just a few seconds and just a few taps.

After hitting an all-time high in August of 21,660, Coinbase smart wallet monthly active wallets have surged 168% – from 5,700 to 15,280 since its release in June.

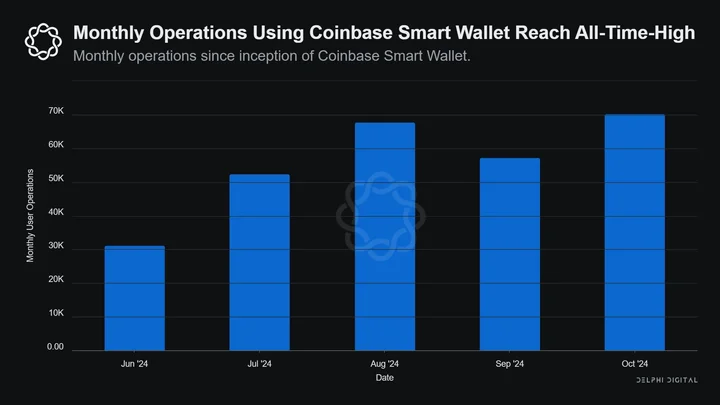

Additionally, monthly wallet operations using Coinbase smart wallet have soared from 31,200 to 70,320 – increasing by 125% and denoting a new all-time high in October 2024.

Note: Data refers to onchain interactions using a Coinbase smart wallet.

Incentives for Developers Building on Base

There are four main factors creating a developer-friendly environment on Base:

- Base is built as a standardized EVM, meaning developers write applications in Solidity– the most popular blockchain programming language.

- Base is part of the Superchain, a network of rollups using the OP Stack, allowing Base to share security and a communication layer with other rollups. As a result, Base is more attractive to developers due to the increased interoperability between Superchain rollups and the support it receives from other Superchain developers.

- The Coinbase Developer Platform and Onchainkit make development on Base even more straightforward, with ready-to-use components and tooling.

- Transactions are incredibly cheap relative to other rollups, and app fees are significantly cheaper than their Web2 competitors, fostering a massive user base.

Surging Onchain Economy Use Cases

Project Breakdown by Innovation and Utility

As Base continues to see an influx of activity year-to-date, there has been varying success within the different sectors.

The following will summarize a few prominent protocols within each sector and their performance this year.

Social – Farcaster Frames

Farcaster frames, launched in March, are a tool that allows interactive experiences to be embedded within casts on Farcaster.

Frames are simple to find, with Warpcast (the largest Farcaster client) having a subpage to view trending frames. They are similar to Blinks on Solana and Slinks on Starknet, which allow tweets to have embedded, interactable onchain content.

Frames unlock internal composability between the client, network, and users. Many are built on Base, allowing for several different onchain interactions, such as minting NFTs in-feed, making onchain payments, and playing games. These onchain tasks just require a click on the frame to complete the task.

They also create ease between consumers <> merchants, allowing for seamless transactions to take place within Farcaster clients. This increases purchases because it reduces hops to finalize the purchase.

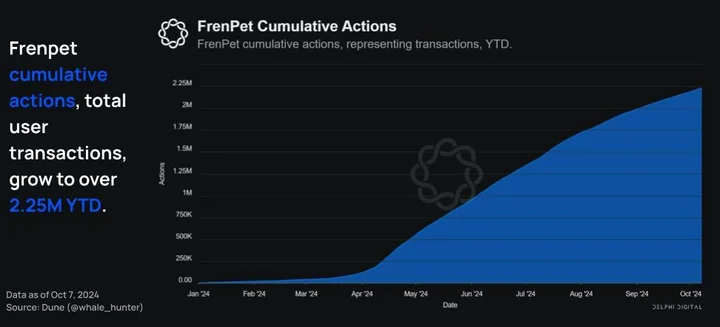

Gaming – Frenpet

Frenpet, an idle game on Base, is quietly seeing a lot of success over the past year. The app is built on a browser, and the creation process is fully abstracted through Privy and paymasters.

The game has been growing very consistently, with over 2.25M cumulative actions year-to-date.

The gaming scene on Base is only starting, and fun, small games like Frenpet have the chance to start picking up steam as Base continues to attract more users to its network.

NFTs/Digital Collectibles

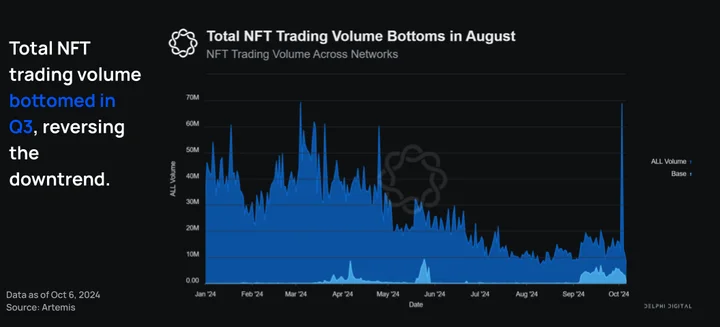

NFT trading volume across networks, including Base, has been trending lower for the better part of the year but bottomed in August (at least temporarily).

At the end of Q1 2024, we saw an upwards trajectory in volume. This excludes the outlier at the end of October that reverted back to the mean the following day.

Base NFT trading volume corresponds to different periods of spiked activity, lacking consistency across a quarterly basis. Most likely, this is due to specific NFT initiatives temporarily boosting NFT trading volume.

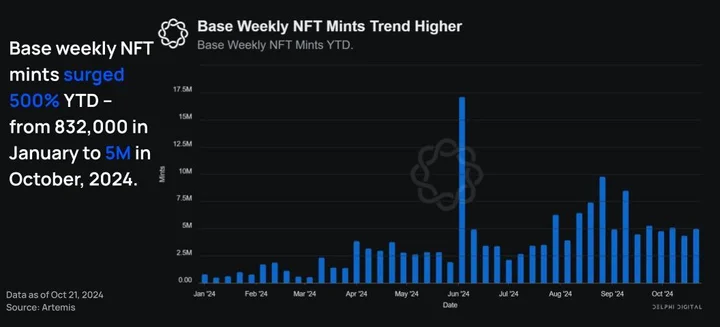

Interestingly, year-to-date, Base weekly NFT mints are up from 832k to 5M at the end of October after peaking at 17.12M in the first week of June. Showing an inverse trend of more NFT activity in this metric.

This is an increase of 500% year-to-date, indicating that Base is becoming a hub for non-monetary-focused NFTs.

Based on NFT activity for Base and other networks, NFT behavior appears to be shifting away from trading/speculation, and towards non-monetary use cases for NFTs. This is indicated by a 500% increase in weekly NFT minting on Base between January and October 2024, alongside a significant decline in NFT trading volume between March and October 2024.

A real value of NFTs beyond art (e.g., Bored Apes) is their ability to be tied to real world utility. Examples of this real-world utility are NFTs representing memberships within a coveted group or a real estate deed.

Mints are trending higher since Coinbase ran its Onchain Summer program, which incentivized participants to mint NFTs– often with a low cost or no cost required to mint (via gasless transactions). This suggests that Onchain Summer had a lasting impact on user engagement, as users remain active after the program’s conclusion.

DeFi on Base

Decentralized Finance (DeFi) provides financial products and services at an institutional scale, but without intermediaries that absorb value. With DeFi, the value can instead be redistributed to participants. As with most networks, DeFi is still prominent on Base, and takes advantage of sub-cent transaction fees. The following section covers four different embedded sectors: DEXs/derivatives, money markets, Telegram bots, and liquid staking/yield farming.

Trading Platforms

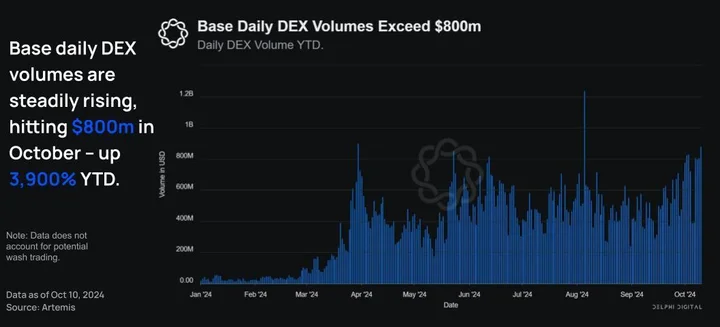

Base has become a prominent area for trading spot assets, with daily volume increasing at a consistent rate. Year-to-date, Base DEX volume is up 3,900% from $22M in January, to $880M at the end of October 2024.

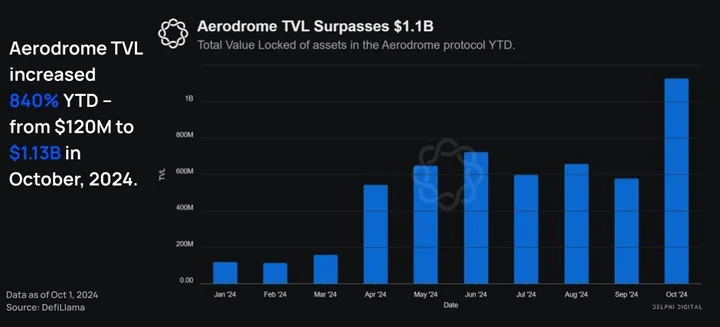

Aerodrome is the undisputed winner when combining both these metrics. Aerodrome has surpassed $1 billion in TVL, roughly 40% of Base’s total TVL, and facilitates the highest onchain trading volume pools in ETH, BTC, USDC, and EURC. The protocol is a fork of velodrome, a curve-inspired Automated Market Maker (AMM) whose goal is to serve as a liquidity hub on Optimism.

Aerodrome serves that same purpose on Base, and thus far has been wildly successful– accounting for the majority of DeFi trading volume (~50-60%) on Base.

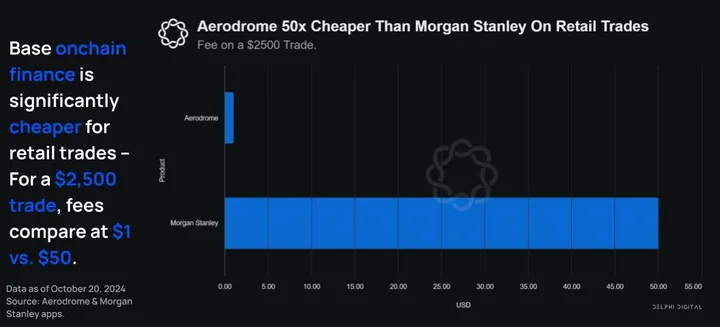

Aerodrome is particularly attractive for financial exchange. Users can swap USDC and EURC with a 0.05% fee, in 1-5 seconds, 24/7, and with virtually 0 slippage. In comparison, traditional finance transfers can take 1-5 business days, and can cost 0.3% (Wise, low end, 6x cost of Aerodrome) to 3% (Wells Fargo, 60x cost of Aerodrome). Additionally, international transactions on Aerodrome are available 24/7 and take just 1-5 seconds, vs. traditional finance transactions which take 1-5 business days.

Users like familiar structures where they can benefit from having a real stake in the protocol. This is why, in the early stages of most networks outside of Ethereum, Uniswap does not have the majority market share but rather the native AMM.

Users like familiar structures where they can benefit from having a real stake in the protocol. This is why, in the early stages of most networks outside of Ethereum, Uniswap does not have the majority market share but rather the native AMM.

Most alternate-network native AMMs traditionally have complex user incentives that revolve around staking a token for emissions or protocol fees. Once this happens, a flywheel kicks in, and the native AMM attracts all the liquidity. Uniswap is not usually able to come in and become the market leader immediately. This has played out across several rollups: Base (Aerodrome), Optimism (Velodrome), and zkSync (Maverick).

To keep in mind here: this flywheel tends to break as the rollup matures, and Uniswap liquidity on that network continues to grow, grabbing market share. Aerodrome’s incentive structure has positioned it as the clear leader on Base in terms of TVL and volume, however, as the rollup ecosystem matures, this may change.

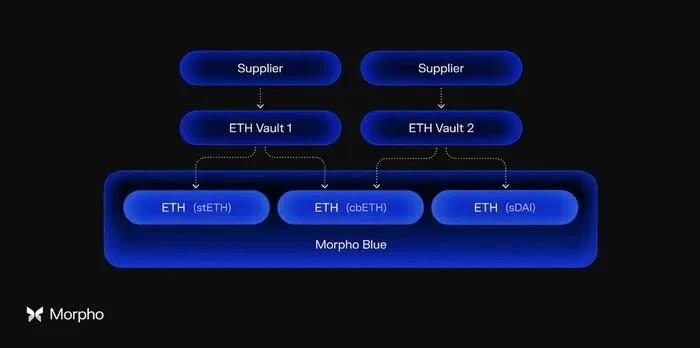

Money Markets

Three large money markets command the majority of market share on Base: Morpho Blue ($220M), Aave ($150M), and Moonwell ($146M). The figures represent the active deposits on the platforms.

Morpho Blue is a trustless platform containing immutable, isolated lending markets. MetaMorpho allows third parties to offer their own custom-built vaults on top of Morpho Blue. Morpho Blue automatically handles the structural force-keeping of market parameters to ensure the market stays solvent.

Isolated lending markets are really powerful because they silo the risk of each collateral asset. This means that Morpho Blue can technically onboard ‘riskierʼ collateral (e.g., less liquid and more volatile assets like uSUI) and increase its revenue without adding external risk for the ‘strongerʼ collateral (e.g., ETH) supplied in the market. The downside of this is that the borrowers do not benefit from the large deposits in other vaults.

On the other hand, Aave is a traditional DeFi lending market where all pools are tied together, allowing users to submit any choice of collateral and borrow any enabled asset. Aave is the ‘defactoʼ lending market across most networks due to its resilience and long-standing reputation.

Moonwell offers users a combination of the two. Moonwell is an Aave fork, where deposits can be accessed with collateral of any accepted asset. They also have core vaults, which are built on top of Morpho, for more isolated lending pools. The combined offering gives users the choice of which infrastructure they want to use, managed by the Moonwell DAO.

Having three competitive lending markets on Base is a healthy sign of decentralization and competition, fostering greater innovation and choice for users. While many networks with Aave as the dominant money market suffer from an SPF (single point of failure), Base does not because the capital is spread across multiple protocols.

This is optimal for long-term growth, although it requires more total liquidity to reduce the impact of fragmentation. More choice and competition is good for users, and the growth of Base DeFi has enabled each lending market to build up sufficient liquidity for almost any user’s needs. Continued growth in the ecosystem will benefit all lending markets and reduce the impact of liquidity fragmentation, benefiting users.

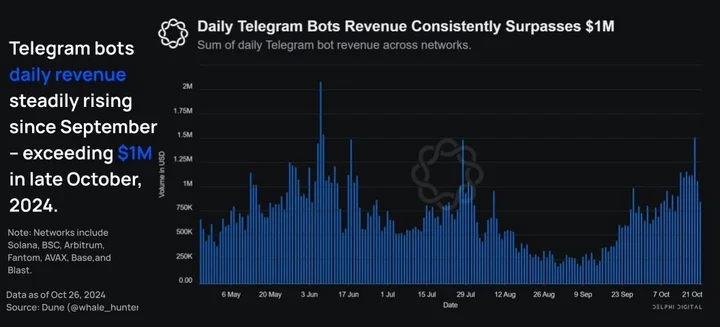

Telegram Bots

Telegram bots have gained strong momentum on most networks, driven by a sharp increase in onchain trading and the simplified UX, creating a significant shift in retail behavior observed this year.

The function of a Telegram bot is to snipe and efficiently trade onchain assets for a user, giving them an edge over users putting on trades manually utilizing self-custody wallets. Most bots charge a ~1% fee on trades.

There are significant UX benefits to using a telegram bot for onchain asset trading. Hence, Telegram bots have seen increasing adoption with daily revenues consistently exceeding $1M.

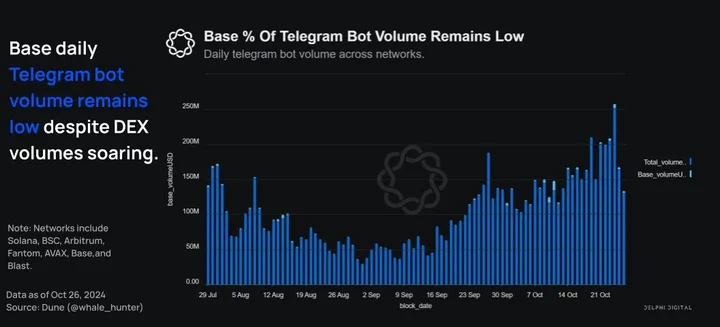

Contrary to other networks, Telegram bot volume has not been high on Base indicating a lack of adoption.

Low Telegram bot volumes coupled with rising DEX volumes on Base seems to suggest that Base has attracted a vast number of actual users, on top of activity migrating to Base from other networks.

Yield Farming

Decentralized yield farming in crypto is very popular. As almost all crypto is inherently financialized, tools to maximize yield that do not have centralization risks are very attractive to many users, driving adoption.

However, Base is not a chain built for yield farmers; it is built to be an onchain global economy. A low percentage of assets on Base are actively leveraged yield farming, as the majority of capital from institutions is risk-averse and would prefer to just hold the assets or, in some cases, borrow against them from permissioned actors.

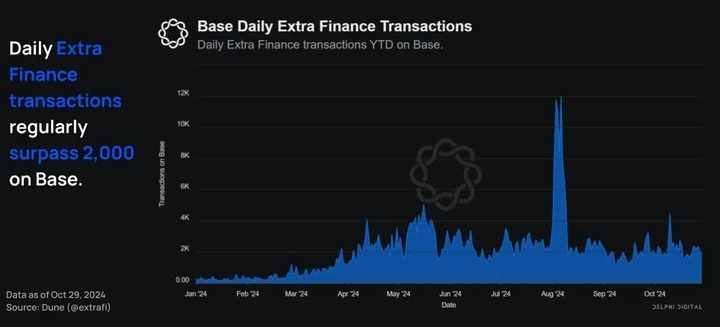

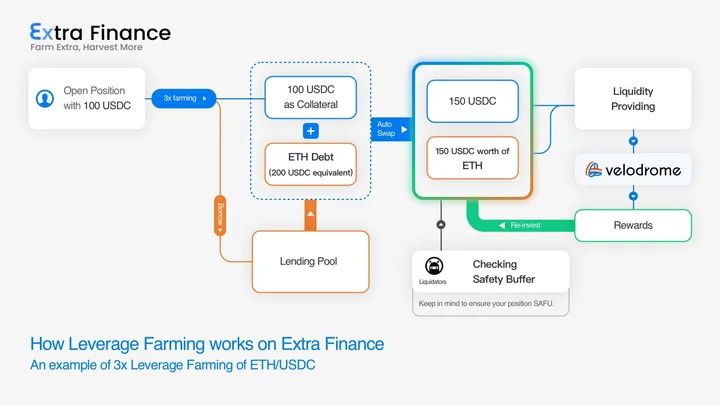

Base’s top yield farming platform by TVL is Extra Finance, which offers a suite of leveraged yield farming products.

They have amassed over $150M in TVL (meaningful, yet small percentage of the $8B in assets on Base) and their user transactions are approaching May 2024 highs– with daily transactions regularly surpassing 2,000.

The leverage farming design by Extra is a thin yet intelligent design that maximizes yield for all participants. The process works by the following structure:

Provide collateral -> Borrow different asset from lending pool -> Auto convert assets into equal proportions -> Provide liquidity -> Compound rewards

Users who do not wish to leverage farming can lend their assets into the pool to earn an interest rate, similar to any other lending market.

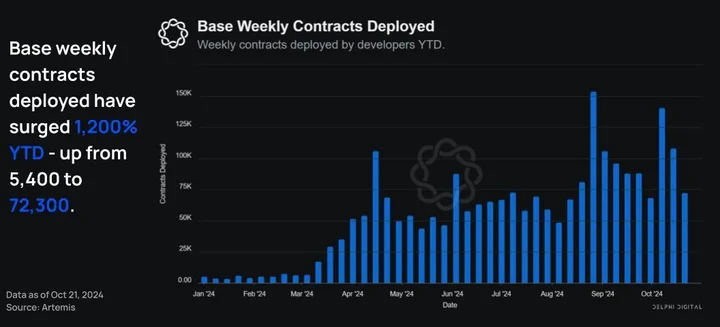

Base Weekly Contracts deployed Year-to-Date

Base can prioritize work on decentralizing the stack (e.g. fault proofs) and helping the broader Ethereum ecosystem because there is ample developer activity on Base.

We see this in practice today – weekly contracts are significantly higher than they were at the start of the year, up 1,200% from 5,400 at the start of January to 72,300 in October.

Note: Weekly contracts deployed refer to the number of unique onchain contracts deployed on Base for a weekly time period.

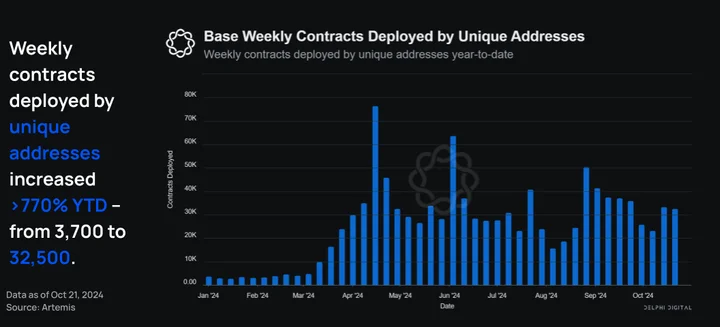

Base Weekly Contracts deployed by Unique Addresses Year-to-Date

Additionally, Base is seeing a rapid influx of contracts deployed by unique addresses. Since January, weekly contracts deployed by unique addresses have risen by 778% from 3,700 to 32,500.

Note: Weekly contracts deployed by unique addresses refer to the number of onchain contracts deployed on Base by developers who have not previously deployed a contract within the week.

Although this metric has slightly tapered off since April, the overall trend is still rising, a strong sign that the Base onchain application developer ecosystem is flourishing. Additionally, it shows that the teamʼs development work to establish Base as a developer-friendly chain is succeeding.

Onchain Job Market Insights

For the sections pertaining to non-public information, we interviewed recruiters at different headhunter companies.

Increase in Companies hiring engineers with smart contract expertise year-to-date

According to our sources, in the first two quarters of 2024, the number of companies hiring engineers to fulfill onchain development roles sharply increased. This increase slowed down post EthCC as the traditional ‘Summer slowdownʼ took place and prices recessed. However, even during this period there has been a noticeable uptick in hiring relative to other periods with recessed prices.

One interesting trend our sources noticed is that in bear markets, there is more of a focus on building infrastructure, leading to more developers working on infrastructure-related issues. Conversely, in bull markets, people are actively optimizing for mass adoption, which leads to more consumer applications being funded and, hence, more developers working on consumer applications.

Increase in Job Opportunities for Crypto-Savvy Applicants

As stated by our sources, there has been increasing demand for crypto-native applicants across the board. Crypto-native people understand the way blockchain projects can market to users because the applicants have been/are still users — a distinct advantage over non-crypto-savvy applicants. One source added that a crypto native employee familiar with the niche marketing structures appealing to the crypto community make or break a successful marketing strategy.

Interestingly, in Q1 and Q2 demand for crypto-native people to run socials exploded, aligning with protocols launching their product and token. However, our sources noted that companies within the crypto industry continue to place a strong emphasis on prestige. Even for crypto-native candidates, factors like attending an Ivy League school are often highly valued in the hiring process.

According to our sources, the demand for candidates who are both crypto-native and have a prestigious background has resulted in many roles within the industry being reserved for a limited pool of applicants.

Insights on Builders/ Protocols/ Founderʼs Perception on Talent Pool

Our sources indicated that, prior to the collapses of FTX, Luna, and Three Arrows Capital, the talent pool in the industry was broader and more diverse, with candidates from various fields beyond computer science. Making it apparent that the impact of these events on the crypto industry extends well beyond a drop in market valuation. General reputation issues persist, diminishing the number of applicants willing to work in an industry they perceive as volatile.

According to one source, this stigma against crypto is also evident in the decline in interest among students joining university blockchain clubs. Prior to the aforementioned collapses, there was significantly more demand for club memberships. Given the current competitive landscape for computer science and engineering internships, this waning interest in an industry with ample opportunities is particularly concerning.

That said, the crypto industry would benefit from a stronger appeal to younger builders to develop onchain– targeting interns and newly graduated students.

Insatiable Demand for Talent & Shortage in the Talent Pool

Despite market conditions, recruiters have seen a relentless, unwavering demand for engineering talent, driven by venture-backed projects competing fiercely for the limited pool of skilled engineers.

As a result, there is a pronounced shortage of crypto developers as demand continues to outpace available talent. Interestingly, three sources added that many traditional developers are hesitant to pursue roles in the crypto space, perceiving the industry as unstable.

This assertion is reinforced by three findings from a recent Coinbase survey conducted among onchain and mainstream developers, which underscores a lack of confidence in the ability to onboard new developers.

- Half (49%) of mainstream devs believe that “crypto and the blockchain are important areas of innovation for the future.

- 78% of onchain developers agree that “in the past it has been hard to onboard new users to start using cryptocurrency & blockchain applications.ˮ

- 73% of onchain developers say that a “lack of clarity on crypto regulations makes it more difficult to innovate in this space.ˮ

Coinbase is actively pursuing greater regulatory clarity around the world, on behalf of the industry. Progress in this area is likely to help unblock innovation by builders, and contribute on onchain economic development overall.

Conclusion

The onchain economy has indisputably exploded in 2024. Much of this growth is driven by activities outside of financial speculation and trading. Stablecoins have found product-market fit and are enabling a more global digital economy. L2s have brought down onchain costs and made building onchain easier, faster, and cheaper.

In just over a year, Base has solidified its position as a leading L2. By establishing a developer-friendly ecosystem with minimal transaction fees, Base has created an environment that not only attracts developers and users, but also sees robust retention.

DeFi continues to be a core onchain economic activity. DeFi provides financial products and services at institutional scale, but without intermediaries that absorb value. Instead, this value can be redistributed to participants.

At the same time, new use cases and applications are emerging as a significant piece of the onchain economy. Fostering diverse onchain app development and creating infrastructure to support sectors (like gaming and SocialFi) means that onchain experiences are branching out, and this is a major driver behind the growing global onchain economy.

Lower fees, more use cases, easier to use technology, and innovative products are all contributing to the thriving and growing onchain economy.

0 Comments