🌅 Welcome!

SEC Chairman Gary Gensler continues to talk about crypto regulations and Genesis tells clients that the path forward may be longer than anticipated.

Today, we take a look at Frax Finance’s liquid staking solution while our Research team dives into the uncollateralized lending space in DeFi.

This is the Delphi Daily. Let’s dive in.

🚨 In Case You Missed It

- SEC Chairman Gary Gensler says the agency has all the authority that it needs to regulate crypto.

- Genesis informs clients that the path forward may be longer than anticipated.

- A New York judge approves subpoenas against 3AC founders, Su Zhu and Kyle Davies.

- Binance releases an audit report by Mazars that says customer BTC holdings are overcollateralized.

- The Bank of Spain announces plans to launch an experimental CBDC program.

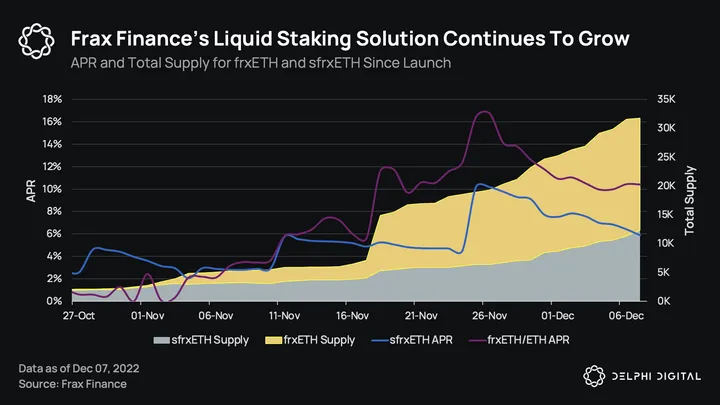

📊 Frax Finance’s Liquid Staking Solution Continues To Grow

More on Frax Finance – Frax Finance: Examining The Protocol’s Holy Trinity of De-Fi

- Over the previous 30 days, the total supply of frxETH has increased by 870% while the total supply of sfrxETH has increased by 285%. While frxETH is a stablecoin pegged to ETH, sfrxETH is a liquid staking token that accrues value from staking rewards.

- Users can deposit 1 ETH and mint 1 frxETH. Users can stake frxETH to get sfrxETH and earn staking rewards. Alternatively, users can also provide liquidity to frxETH pairs on Curve and earn trading fees and token rewards.

- The ETH deposited to mint frxETH is staked with validators with 90% of the rewards flowing back to sfrxETH holders. Rewards are deposited back in the vault, allowing sfrxETH holders to redeem more frxETH than originally staked.

- Currently, there are 31.7K frxETH tokens but there are only 12.3K sfrxETH tokens. This allows sfrxETH holders to earn enhanced staking rewards sourced from ETH deposited by other users who have minted frxETH as well.

- Currently, sfrxETH holders are earning an APR of 5.8% from all ETH staked with validators. For comparison, stETH issued by Lido is currently earning an APR of 4.7%.

- frxETH holders who provide liquidity on Curve are earning an APR of 10.4% from trading fees and token rewards (CRV, CVX, and FXS). The APR for sfrxETH and the frxETH pool is likely to converge over time as capital flows to the higher-yielding option.

⚡ The Year Ahead for DeFi

-

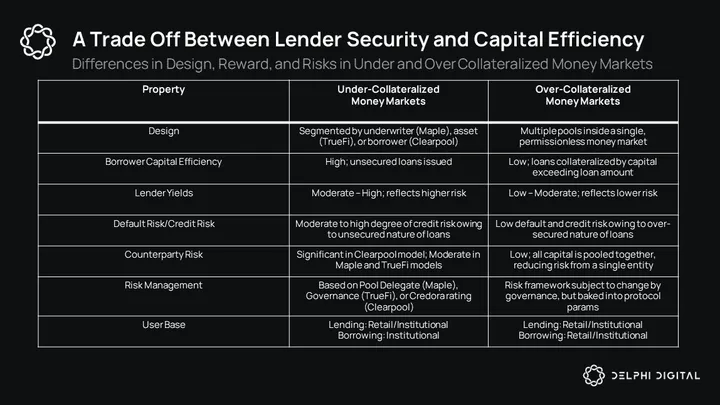

Undercollateralized money markets like Maple Finance, Clearpool, and TrueFi serve the speculation use case by funding market makers and hedge funds with accessible leverage.

-

Unlike banks, they use on-chain holdings as a means of gauging an entity’s balance sheet health and ability to repay. Their impact on providing the market with more liquidity is evident, but projects operating in this space haven’t really found the right model yet.

-

Effectively, lenders are giving out unsecured loans to market makers and hedge funds considered to be of “high stature.” It’s no riskless endeavor.

-

Not repaying their loans is akin to burning their entire reputation in crypto. Barring insolvency and a legitimate inability to repay funds, it’s unlikely for a fund to willingly burn their reputation for a few million dollars.

-

However, given the frequent occurrence of tail events in crypto, the actual risk for lenders is likely higher than the perceived risk. If we compare overcollateralized money markets like Aave to unsecured money markets like Maple Finance, there are certain types of risks that are heightened in the latter.

-

Default risk is the most obvious, given the unsecured nature of these loans. Counterparty and concentration risk are a close second. For example, Maple’s design is one in which a pool delegate decides who to loan lender capital to.

-

If too much is given out to one party, lenders in that pool are exposed to greater counterparty risk. This is all the more important in the case of Clearpool, where each pool is exposed to a single borrower and therefore has higher concentration risk.

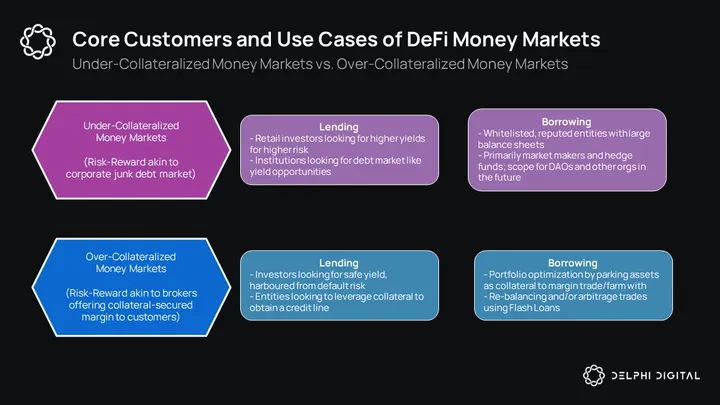

- Liquidity is the lifeblood of a well-functioning market. When used correctly, leverage is a powerful tool. Unsecured lending remains the easiest way to unlock capital efficiency for professional investors and traders in crypto.

-

The core customers of unsecured money markets are market makers. They need efficient access to spot leverage to fulfill their role. It’s unlikely that traditional banks are going to give Wintermute, Folkvang, or GSR a large loan to market make crypto assets.

-

But even if they did, it would be a time-consuming process marred by the bureaucracy that banks are infamous for. While the evaluation process differs for each protocol, on-chain undercollateralized loans are usually issued based on an on-chain balance sheet.

- For more on prominent themes in DeFi, Delphi members can read our Delphi Pro report here.

🐣 Notable Tweets

Contrarian Predictions

as the year comes to an end

give me your most contrarian thesis, idea, or prediction for 2023

– GCR (@GCRClassic) Dec 7, 2022

Delphi’s 2023 DeFi Year Ahead Report Launch

Our 2023 DeFi Year Ahead report has just been released to our PRO members. It covers:

- The State of DeFi

- Themes for the Future

- What Surprised Us

- Futuristic Ideas The Year Ahead for Defi, out now!

– Delphi Digital (@Delphi_Digital) Dec 7, 2022

0 Comments