Fraxlend Attracts $10M in Collateral as a Whale Deposits CRV

OCT 26, 2022 • 4 Min Read

🌅 Welcome!

A Southeast Asian crypto hub proposes clamping down on leverage and the CEO of a prominent crypto exchange is stepping down.

Today, we take a look at the reason behind the growth of Fraxlend and our Research team examines principal protected yield in DeFi.

This is the Delphi Daily. Let’s dive in.

🚨 In Case You Missed It

- Singapore proposes a slew of crypto regulations, including a ban on leverage for retail investors.

- Alexander Hoeptner, CEO of BitMEX, has left the firm. CFO Stephan Lutz has been appointed as interim CEO as the exchange plans to launch a token.

- Bybit invests $3.8M in T-Scientific, the third-largest shareholder of Bithumb, via convertible debt.

- Cash App users can now send and receive payments in BTC via the Lightning Network.

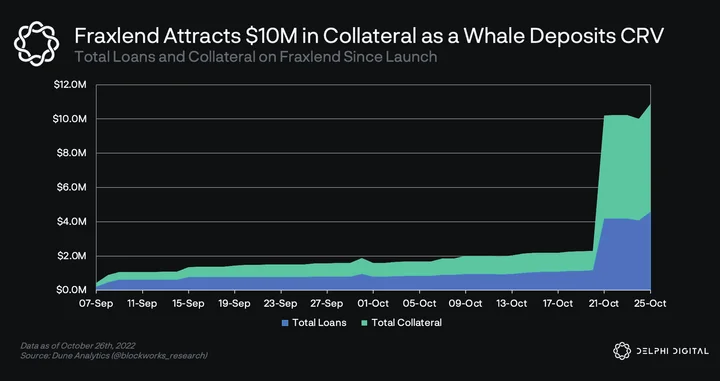

📊 Fraxlend Attracts $10M in Collateral as a Whale Deposits CRV

- Fraxlend is an over-collateralized lending and borrowing protocol that allows users to create isolated money markets between any two ERC-20 tokens. Currently, users can borrow FRAX against six collateral tokens.

- The protocol was launched on Sep. 6, 2022. Within seven weeks of launch, users have deposited more than $10M of collateral and borrowed more than $4.5M of assets.

- Most of this growth has materialized during the past seven days as total collateral deposited has grown by 382% and total assets borrowed has grown by 459%.

- The growth can be traced to three transactions by 0x7a…5428 in the CRV money market. The address collateralized 10M CRV tokens to borrow 3.5M FRAX tokens. The address is labeled “Curve.fi: Founder #1” by Nansen’s wallet profiler.

- As a result of the activity, the address forms 76% of the total loans issued by the protocol. Currently, the debt position stands at a healthy 40% loan-to-value ratio against a maximum allowed 75%.

- The CRV money market has reached a utilization rate of 90%. Currently, lenders are earning 9.8% APY while borrowers are paying 10.3% APY.

⚡The Emergence of Principal-Protected Yield in DeFi

- After two years of free money, DeFi yields have fallen to unimpressive levels. The days of depositing stables into a Yearn vault for 20% APY seem long gone.

- Crypto yields are now struggling to compete with government bonds. Users have been forced to venture further out on the risk curve to generate worthwhile returns.

- This usually entails prolonged exposure to cross-chain bridges and obscure yield farms – a recipe for disaster.

- Principal-protected vaults are an emerging niche of DeFi structured products that attempt to provide risk-averse investors with yield that compares to more aggressive strategies elsewhere.

- These vaults attempt to guarantee the user’s initial deposit by concentrating risk into house money earned by the principal via safer yield avenues.

- This is akin to a barbell strategy, where a strategy utilizes both sides of the risk/reward spectrum (low and high risk/reward) in order to boost returns.

- Theoretically, the potential for composability and the inability of this immature market to efficiently price risk should allow these products to flourish.

- But a key question remains: Are principal-protected products a value add, or another zero-sum gadget? Vovo, Brahma, and Ribbon are three projects paving the way in this space.

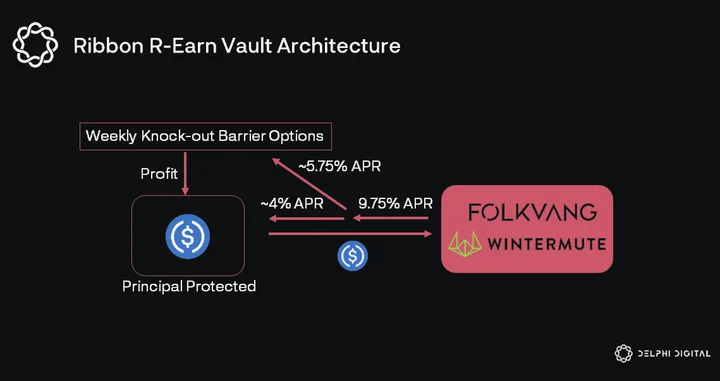

- Ribbon’s R-Earn vault takes an approach that is similar to Maple Finance. Vault funds are lent to market makers (Wintermute and Folkvang Trading) at 9.75% APR over 28-day epochs.

- The vault sets aside a portion of the weekly interest payments to guarantee a base yield of 4% APY. The remainder is used to purchase weekly ATM knock-out barrier options.

- Knock-out options expire worthless if the underlying asset exceeds or falls below a predetermined threshold.

- By purchasing both calls and puts, the vault creates a straddle-like “twin win” payoff structure that allows depositors to profit off of intra-week volatility up to 8%.

- For more on principal protected yield, Delphi members can read our Delphi Pro report here.

🐣 Notable Tweets

Types of DeFi Structured Products

Structured Products will bring mass adoption to DeFi.

They unlock high yield opportunities with relatively low risks📈

Discover:

• what are DeFi structured products

• 5 projects building DeFi structured productsA thread👇

Y2K Finance – Insurance for Stablecoins

Stablecoins are the source of chaotic creation in DeFi. Is there any way that can help us to control and prevent black swan events like UST depeg?

🧵 of:

Everything you need to know about @y2kfinance (including airdrops) – the best insurance protocol for stablecoins

0 Comments