🌅 Welcome!

Google has partnered with Coinbase Commerce to begin accepting crypto payments for cloud services in early 2023. Is this what mass adoption looks like?

Portugal explores a capital gains tax on crypto, we take a look at Flashbots’ market share, and our Research team breaks down the MEV supply chain.

This is the Delphi Daily. Let’s dive in.

🚨 In Case You Missed It

- Portugal’s Finance Minister submits a draft proposal for a 28% capital gains tax on crypto held for less than a year.

- Google integrates with Coinbase Commerce to begin accepting digital currency payments for cloud services in early 2023.

- The EU‘s Economic and Monetary Affairs Committee votes 28 to 1 in favor of its landmark crypto legislation.

- Polygon launches public zkEVM testnet and aims for a full mainnet launch in early 2023.

- BNY Melon, the world’s biggest custodian of financial assets, begins accepting clients’ crypto assets for its custody business.

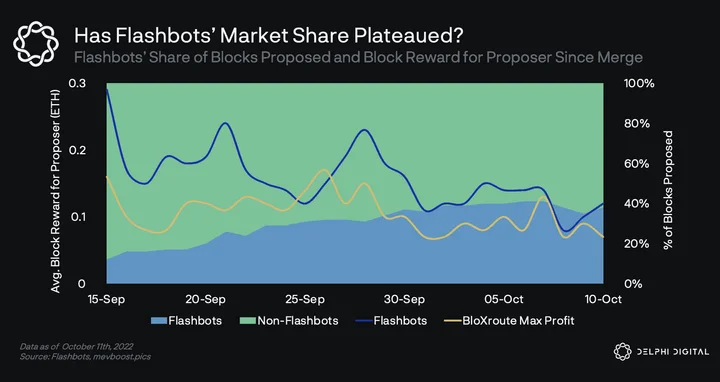

📊 Has Flashbots’ Market Share Plateaued?

- MEV-Boost is open-source middleware developed by Flashbots and run by Ethereum validators to maximize their staking rewards. MEV-Boost does this by allowing validators to access a competitive block-building marketplace.

- Builders create the most profitable block possible by arranging transaction order flow. While validators who run MEV-Boost must pay builders for this service, they come out ahead due to the increased value extracted from the builder’s block.

- Notably, Flashbots appears to be complying with OFAC sanctions by censoring transactions associated with Tornado Cash. Many have raised concerns over such censorship and the potential risk of centralization caused by Flashbots’ growing market share.

- The share of Ethereum blocks proposed by Flashbots’ MEV-Boost increased from 12% on the day of the Merge to a peak of 41% three weeks later on October 6th. On that day, just 59% of all Ethereum blocks proposed did not use Flashbots’ MEV-Boost.

- That trend has since slowed down, with Flashbots’ share of proposed blocks staying flat over the past week. However, this may prove to be temporary as validators are incentivized to use Flashbots’ due to its ability to generate higher fees than competitors.

- Since the Merge, BloXroute Max Profit (which does not censor transactions) has earned a daily average of 0.11 ETH per block proposed while BloXroute Regulated (which censors transactions) has earned 0.12 ETH per block proposed. Over the same period, Flashbots’ has earned 0.16 ETH per block proposed.

- For more on MEV, Delphi members can read our Delphi Pro report here.

⚡ MEV Manifesto

- MEV (Maximal Extractable Value) has been loosely defined as the value that block proposers can extract in a permissionless manner by reordering, censoring, or inserting transactions.

- MEV is central to Ethereum’s block production process. As a result, today’s censorship issues are deeply intertwined with MEV research.

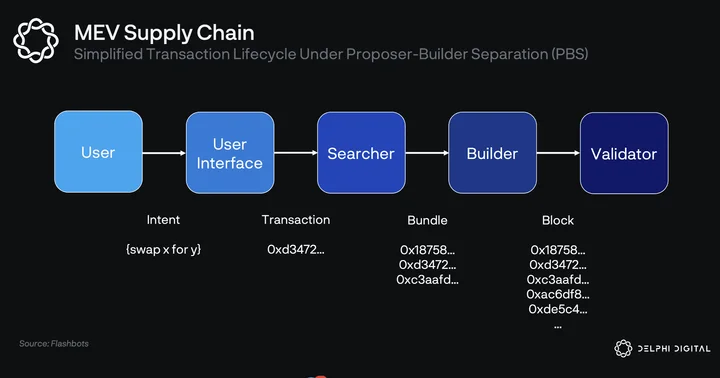

- The oversimplified Ethereum MEV supply chain under proposer/builder separation (PBS) begins with the user expressing intent to enact some state transition (e.g. swap ETH with USDC).

- A user interface allows the user to easily encode their intent into a transaction that the blockchain can understand.

- This includes the whole app layer (wallet, smart contract, dApp frontend) working together to express the user’s intent. This layer also decides where to route the user’s transactions – to the public mempool or private channels such as Flashbots Protect.

- Searchers runs MEV strategies (e.g. arbitrage, liquidations) and submits “bundles” of these transaction preferences to builders.

- Builders aggregate transactions from various sources and construct a block. This was previously done by mining pool operators, but a distinct new role has been introduced post-Merge.

- Validators or proposers perform consensus duties. Historically, proposers and builders have been the same logical entity by default, but PBS strips them apart.

- There are multiple types of MEV. The largest forms are becoming progressively commoditized (i.e., most profits get bid to the block producer), while the long-tail retains a higher margin for searchers. One type of MEV is atomic arbitrage.

- Arbitrage is buying and selling an asset in different markets (or in derivative forms) to take advantage of differing prices. Atomic refers to the entire transaction sequence successfully executing together, or all failing together (no partial execution).

- Let’s say that a large ETH buy was just executed on SushiSwap. ETH is now $1,000 on Uniswap, but it’s $1,010 on SushiSwap. MEV searchers can submit bundles to atomically buy ETH on Uniswap and sell it on SushiSwap until the arbitrage is closed.

- This type of MEV benefits market efficiency without harming users, and it can provide riskless profits to extractors.

- For more on MEV, Delphi members can read our Delphi Pro report here.

🐣 Notable Tweets

slAMM: A Unified Model for Cross-Chain Liquidity

Presenting slAMM: a potential design for a cross-chain AMM

TLDR on what this means and why I’m excited about it👇

— José Maria Macedo (@ZeMariaMacedo) Oct 10, 2022

ELI5 Proto-danksharding

This is my attempt at ELI5 Proto-Danksharding #EIP4844

All L2s & $eth have data availability issues because storage is expensive.

With Sharding, Danksharding, and Proto-Danksharding, a new data type on L1 will make L2 rollups cheaper.

1/n

— odin-free.eth ✨🐺🇨🇴 (@odin_free) Oct 7, 2022

0 Comments