The Global Settlement Layer Thesis

Crypto’s greatest irony has been the fundamental misunderstanding that “mass adoption” would be achieved in the form of some breakout consumer application. Over the last decade we’ve seen that the major use cases have come from abstracting away the friction and complexities of money transfer (just take a look at the adoption of Tether). The age-old narrative of facilitating cross-border payments has been so dominant that XRP continues to remain one of the largest assets in crypto to this day.

And it seems after nearly an entire decade, the market is coming full circle back to this narrative. This is clearly evident with the proliferation of stablecoin-specific chains within just this year alone. Trillions of dollars move across borders every year, often through a patchwork of correspondent banks, intermediaries, and outdated networks like SWIFT. These systems impose high fees, multi-day settlement delays, limited transparency, and friction around compliance.

From a crypto-native perspective, this is paradoxical. If decentralized ledgers excel at anything, it should be moving value permissionlessly, instantly, and globally. And yet, despite more than a decade of innovation, the industry has not cracked this market. Stablecoins have grown into hundreds of billions in circulation, but they largely serve crypto-internal use cases like trading collateral and DeFi liquidity.

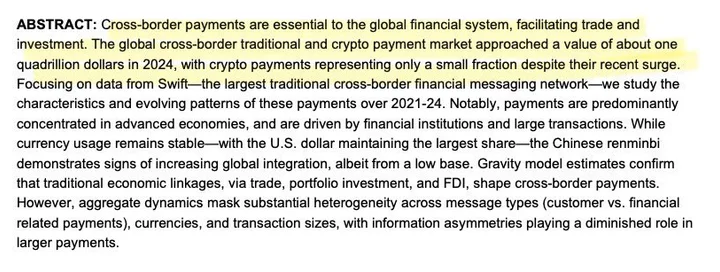

If a network can credibly become the settlement layer for banks and institutions across borders, it would be addressing the largest payment flow on earth. Global cross-border payments are measured in the hundreds of trillions annually. In 2024, this number reached approximately $1 quadrillion.

Source: Global Cross-Border Payments: A $1 Quadrillion Evolving Market?

In this report, we’ll take a comprehensive look at Keeta, a hyper scalable blockchain that focuses on bridging banks and financial institutions with crypto rails.

SWIFT Killer – Built for Financial Institutions

In the early days of crypto, Ripple was dubbed the “SWIFT killer” – a moniker for its ambitious goals of replacing SWIFT and becoming the digital rails for cross-border remittances. And although Ripple has made significant progress in partnering with banks and global financial institutions, Keeta has seemingly leapfrogged a decade’s worth of efforts on many technical fronts.

But much of this discrepancy in technical progress could be attributed to Ripple launching in 2012 (if we exclude lawsuits with the SEC). To Keeta CEO Ty Schenk’s point, they don’t have the same capabilities that Keeta currently has from a technical standpoint.

Keeta entered the space in a post-tokenization thesis world, where BlackRock, Citi, JPMorgan, and the BIS are actively experimenting with tokenized RWAs. The fact here is that Keeta was fortunate enough to have better timing, stronger technical primitives, and fewer regulatory baggage. It speaks directly to the current momentum in institutional crypto adoption.

But regardless of fortunate timing, Keeta has prioritized what really matters. From the beginning, Keeta has positioned itself as a compliant-by-design L1, purpose-built to service banks, fintechs, and sovereign issuers who can’t touch permissionless blockchains due to regulatory and risk constraints. The main focus here is institutional trust, compliance, and interoperable issuance, while maintaining an open permissionless system for the rest of the network. Keeta effectively serves both sides of the spectrum: regulatory complaint institutions and crypto-native users.

There are a number of unique components to Keeta that enable these advantages when it comes to institutional adoption:

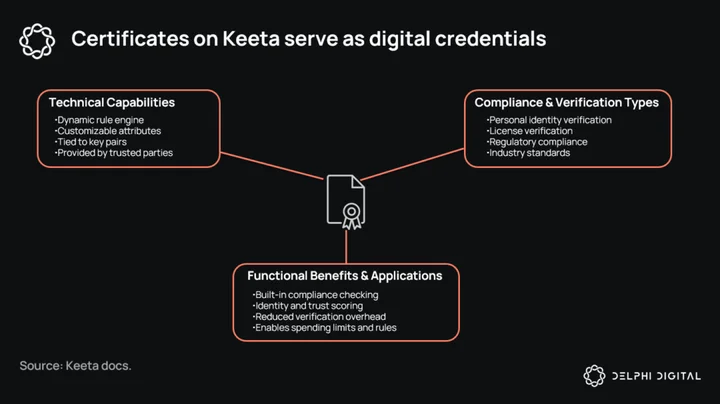

On-chain KYC / Identity Certificates

On-chain KYC sounds like a paradoxical concept. But the reality is that no financial institution is willing to interact with unverified wallets. Traditional financial institutions require strict identity verification, AML compliance, and counterparty transparency. Most L1s fall short here because pseudonymous addresses and privacy-first design run counter to these regulatory needs.

Keeta’s approach is quite unique. By enabling on-chain identity certificates, wallets are tied to verifiable identity attestations without doxxing the underlying identity data to the network. This is achieved via the X.509 standard used in many internet protocols, including TLS/SSL, which is the basis for HTTPS.

These certificates function as cryptographically signed credentials issued by trusted Certificate Authorities (CAs). They can represent a range of verified attributes: KYC status, business licenses, jurisdictional permissions, which are attached directly to a user’s account on Keeta. Once issued, they act as reusable proof of compliance across the network, eliminating the need for repeated verification with each counterparty. Encoded information in KYC certificates are ISO20022 compatible.

The issuance process is straightforward. A user generates a key pair and submits a certificate request to a CA, which performs the necessary off-chain checks. Upon verification, the CA issues a signed certificate tied to the user’s public key. This certificate is then attached to the user’s Keeta account, where it can be recognized and validated by any application or institution on the network. Because certificates are dynamic, they can be updated or revoked in real time, ensuring that the most current compliance status is always reflected on-chain.

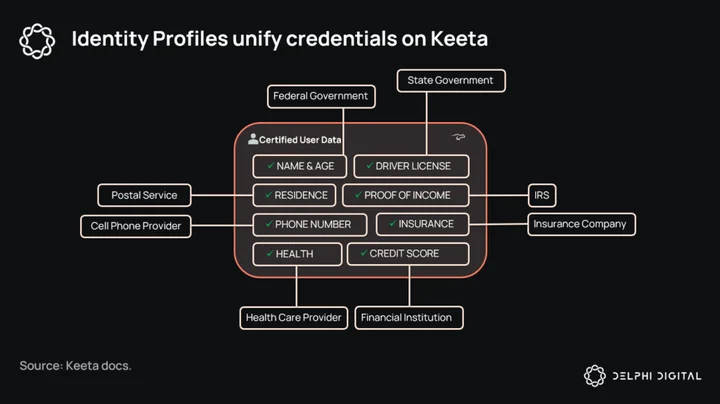

All attached certificates are aggregated into what Keeta calls an identity profile – a unified credential layer linked to the user’s public key. This profile can hold multiple credentials from different authorities, ranging from financial compliance records to sector-specific qualifications.

Most importantly, identity profiles support selective disclosure: users can prove specific attributes to counterparties without revealing unnecessary personal data. For example, a bank might confirm that a wallet is KYC-verified and within a certain jurisdiction without ever seeing the user’s name or address.

This system balances regulatory requirements with privacy preservation. Certificates and profiles enable institutions to enforce compliance rules at the protocol level, while still maintaining pseudonymity in the public ledger. Compliance is hard-coded into the base layer. This means that permissioned DeFi, tokenized securities, and jurisdiction-restricted asset issuance can be built without custom identity logic. For institutions, it’s a bridge into the on-chain economy without compromising on risk controls or regulatory obligations.

It’s worth noting that KYC as a feature is optional, but will be required when interacting with fin

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments