Liquidity Cascades & the Evolution of Financial Markets

SEP 23, 2022 • 24 Min Read

This paper is a logical continuation and practical application of many concepts that were discussed in the report “Reflexivity & the Fall of the Efficient Market Hypothesis.” These concepts include reflexivity, feedback loops (both positive and negative), incentives, and many more. Please give this paper a read if you have not already had the chance to do so! This topic was heavily inspired by a paper written several years ago by Corey Hoffstein of Newfound Research, titled, “Liquidity Cascades – The Coordinated Risk of Uncoordinated Market Participants.” Several core concepts are paraphrased in this report for simplicity.

Financial Markets Are Always Evolving

Markets have continually changed throughout history. From the famous accounts of Nathan Rothschild utilizing his vast wealth and communications channels to ascertain the result of the Battle of Waterloo before most, allowing him to make tremendous profits in Gilt markets, to the ticker tape readers of the early 1900s, and to the now infamous rise of high-frequency trading, one thing has remained consistent – the ever-evolving nature of financial markets and the strategies utilized within them. As markets and the dynamics at play continue to evolve and change with advances in technology, many of the most prominent frameworks for thinking about these markets over the previous decades are becoming redundant.

Perhaps one of the most important changes over the last two decades has been the frequency in which sudden drawdowns (also known as liquidity cascades) have impacted financial markets. Financial markets have always had risks of sudden sell-offs. Many have theorized that as markets get more mature and greater in size, they will tend to exhibit lower volatility profiles. This has not been the case, however.

We have seen an increase in the frequency of liquidity cascades occurring within financial markets – a direct contradiction to prevailing theory. Even more interesting is that even while experiencing more frequent liquidity cascades, equity markets have also benefited from one of the strongest bull markets in history. So how do we make sense of this?

Many people attribute this behavior to three main factors:

-

Increased use of accommodative monetary policy

-

The rise and prominence of passive investing and its implications

-

Fickle liquidity in the face of increasing margin requirements

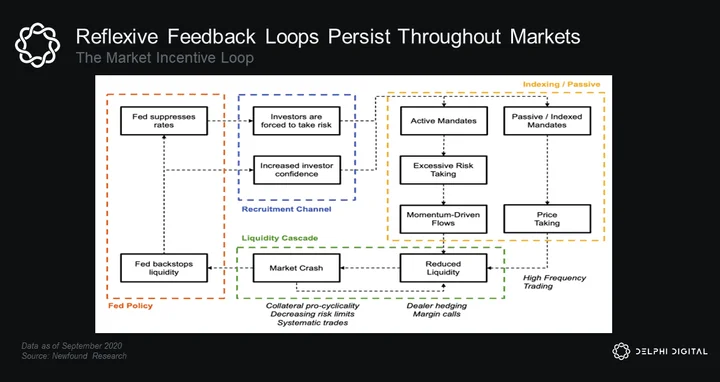

Interestingly, the common denominator behind all of these risk factors is liquidity. These three factors come together to form the “Market Incentive Loop.” The Market Incentive Loop is a real-world application of the reflexive feedback loops discussed in our Reflexivity Report.

Risk Factor 1: Accommodative Monetary Policy

The 2008 GFC gave birth to a new era of experimental monetary policy decisions in the form of QE and many of its successive programs. While these programs were initially aimed at stabilizing financial markets – both domestic and international – it was also the point of no return for many central banks. It was at this precise moment that central banks, led by the Federal Reserve, went from reactive referees to the most active, dominant market participants.

The actions taken by central banks to avoid a global financial meltdown had two major knock-on effects within financial markets. The first was a reduction in short-term interest rates. This provided investors with more incentives to take incremental risk. Complementary programs, such as QE, also provided investors with the second knock-on effect – renewed confidence, and thus the ability to take on additional risk.

Federal Reserve Governor Jeremy Stein discusses this exact dynamic in a speech from 2013, stating, “Thus, according to this theory, an easing of monetary policy affects long-term real rates not via the usual expectations channel, but rather via what might be termed a “recruitment” channel — by causing an outward shift in the demand curve of yield-oriented investors, thereby inducing these investors to take on more interest rate risk and to push down term premiums.”

This reflexive dynamic between Fed policy and investor behavior has second-order implications as well. By forcing investors to pursue higher-yielding foreign debt (driving prices up and yields down), the Fed can essentially export its policy abroad.

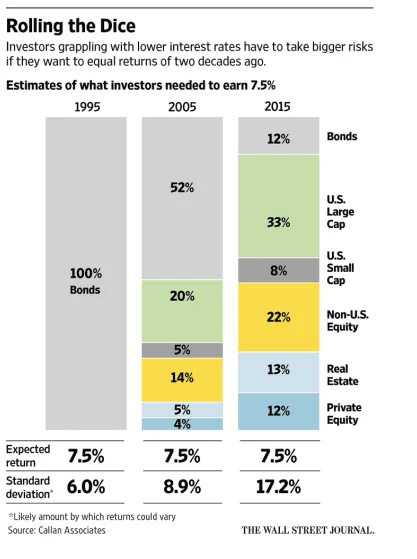

There are other ramifications as well when we take into account institutional investor mandates (pension funds, insurance companies, endowments, etc.). Many institutional investors have fixed liabilities and/or withdrawal obligations. Pension funds, for example, use asset-liability matching to try and mitigate the risk of a shortfall. As shorter-term yields fall in the domestic markets, these investors can no longer meet the minimum ROI needed and must either seek higher-yielding investment opportunities in foreign markets or reallocate capital to new asset classes.

The end result is the same; investors must take on additional risk. This can be visualized in the graphic above which illustrates the change in portfolio allocations required to target a 7.5% return from 1995 to 2015. Note the standard deviation/variance changes over time, as well.

“Ironically, increased demand for higher risk assets may reflexively reduce risk premia, forcing investors even further out on the risk curve.” – Corey Hoffstein, Newfound Research

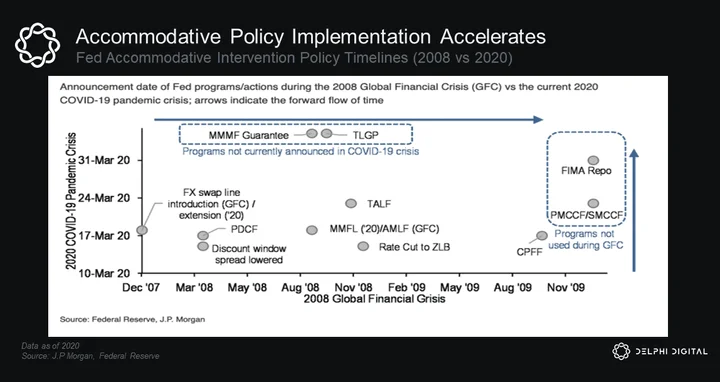

Another interesting dynamic that’s unfolded is the accelerated pace at which the Fed has intervened. In 2008, it took over a year for these decisions to be put in place. During the 2020 COVID-19 crisis, the Fed reacted in less than a month. While many modern economists may argue that these monetary decisions are necessary and are stabilizing forces for markets, others disagree. The opposing view argues the increasing nature of Fed policy intervention is outright distorting markets, and there appears to be some merit to this claim.

A study from 2020 observes that “not only do we find that each of the 10 strategies and the industry as a whole feature a number of structural change episodes in risk exposures, but we also find that most of the endogenously determined break dates match, or nearly match, the [unconventional monetary policy] announcement dates.” (Guidolin et al)

As more market participants take on additional incremental risk exposure guided by Fed policy decisions, market volatility can, and will, lead to reflexive responses in asset prices, resulting in a negative feedback loop in which volatility starts to increase as liquidity decreases. This is exacerbated as investors continue to attempt to de-risk, adding further sell pressure and stress during periods of already poor liquidity conditions. Eventually, this culminates in a sudden liquidity cascade – a vicious cycle.

Risk Factor 2: the Meteoric Rise of Passive Investing

Arguably one of the biggest innovations in financial markets over the last several decades has been the advent of passive investment strategies, pioneered and popularized by legendary investor John Bogle of Vanguard. Passive investing has made it easier for average investors to invest their capital and generate returns with seemingly lower risks.

It is estimated that passive investing has increased from 10% of total assets held in US equities in 1993 to over 45% of assets in 2016 – and this trend has only continued in favor of passive investing.

However, there are two major market impacts as a result of the increased use of passive investment strategies. The first is the impact on ‘cross-sectional asset pricing’, or asset prices as they relate to one another. The second is the impact on market microstructure.

Cross-Sectional Asset Pricing

The reflexive relationship between asset prices and fund flows is exacerbated by passive investing strategies. As passive, low-fee investing has become more popular, fund managers have increasingly used passive indices as benchmarks for their active performance. Studies have shown this increase in benchmarking has led (or forced) active managers to sell assets that underperform while purchasing assets that have outperformed, regardless of fundamentals or technicals. This leads to a reflexive relationship between asset prices, performance, and fund flows.

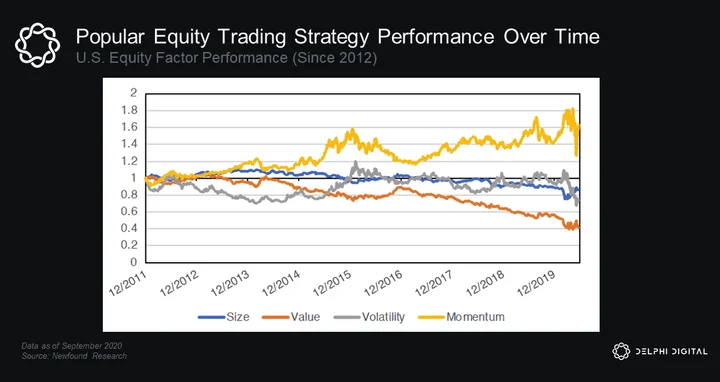

This type of investing behavior is also known as momentum investing. Perhaps predictably, there has been a rise in both the usage and performance of momentum-based strategies since 2012. Interestingly, these strategies have been some of the only profitable ones over the same time period.

Asset prices are also impacted when active managers switch their mandate from active to passive investing. In order to accomplish this transformation, a few things must happen. Active managers must first determine which assets they are over or under-allocated to relative to their benchmark (often times the S&P 500). Active managers must then sell the assets in which they are overweight and buy the ones in which they are underweight until they have the proper allocation relative to the index they’re tracking.

A fund manager’s portfolio is comprised of two parts: the passive benchmark tracking part and the active investing part. In order to outperform, a fund manager’s active bets must beat the management fee + passive benchmark. This forces active managers into allocation decisions they might not otherwise make, such as purchasing assets that have outperformed or taking on additional risk. This can lead to distortions in asset prices.

More concrete evidence of the rise and prominence of passive investing strategies has manifested in the form of marginal selling of smaller market cap stocks paired with marginal buying of larger cap stocks. This dynamic has been sustained and strengthened over time and has led to outperformance in larger cap stocks versus smaller cap peers, something that might seem counterintuitive at first.

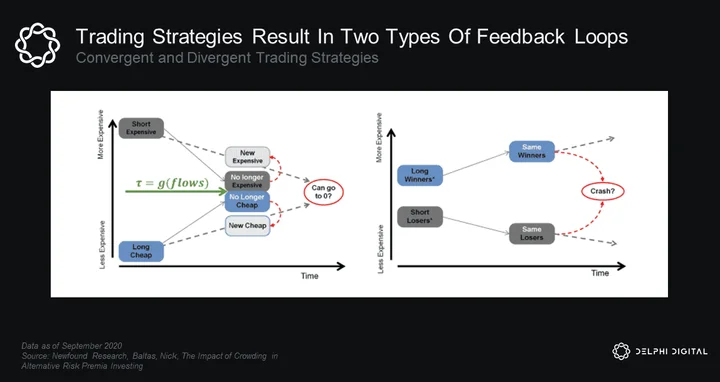

With regard to cross-sectional asset pricing, there are two types of market strategies that impact asset prices: convergent strategies and divergent strategies. Convergent strategies are those in which investors buy/sell at specific price levels (mean reversion, value investing). Divergent strategies are those in which investors benefit from price continuation (momentum). In a nutshell, convergent strategies follow the adage of “buy low, sell high” while divergent strategies fall more in line with “buy high, sell higher.”

When market participants crowd into convergent strategies, prices experience “stabilizing effects.” Winners are sold and losers are bought. When market participants crowd into divergent strategies, prices experience the opposite effect. Winners are added to and losers are sold. Passive strategies are, by definition, divergent strategies. Assets that outperform have a larger weight in the index, which then become the biggest beneficiaries of passive fund flows. As more strategies move from active/convergent investing strategies to passive/divergent investing strategies, there will likely be a destabilizing effect on cross-sectional asset prices.

For the uninitiated, most investable indices are market cap-weighted and rebalance periodically. This mechanism rewards assets whose market caps have grown and penalizes those whose market caps have contracted. Therefore, if a stock’s market cap increases, and that results in its inclusion in the S&P 500, that can cause an even larger increase in its market cap as index funds are forced to buy that security.

Impact on Market Microstructure

When we look at flows as they pertain to passive indexing strategies, fund flows that track a passive benchmark (basket of stocks) are not incentivized to execute at the BEST VALUE, but rather to execute in a way that minimizes the market impact (trading efficiency). This is an important, yet nuanced, distinction because as a larger percentage of fund flows are directed at passive basket trades, destabilizing price effects can become apparent within markets.

Baskets of stocks can experience a phenomenon known as “information leakages” between assets in the same basket. This dynamic leads to consistent price distortions for individual assets. Market makers have trouble discerning whether or not price fluctuations are caused by factors pertinent to their assets, or exogenous factors due to information leakages (information from one security in a basket impacting another security in the same basket). Interestingly, we have seen stocks that have the highest ETF ownership percentage experience higher volatility, higher trading costs, and increased return synchronicity. Some studies have even suggested that ETFs have introduced an entirely new source of noise to markets altogether.

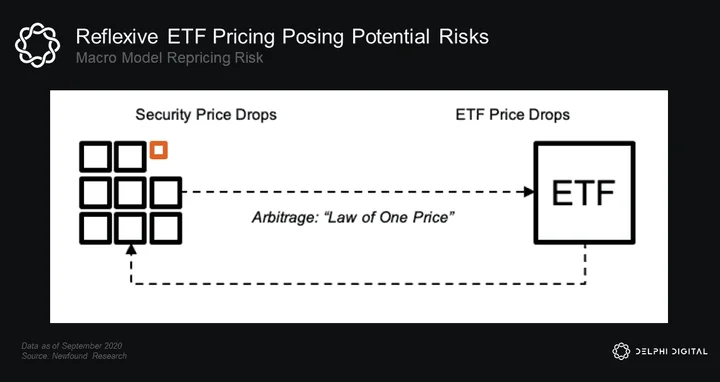

For example, if an asset in the S&P 500 loses value, the implication is that the index should also decrease in value. If the price function of securities in the S&P 500 are using the value of the index as a variable, a decrease in the value of the S&P 500 will lead to a decline in the value of other securities in the index. This again decreases the value of the S&P 500, leading to a negative reflexive feedback loop.

In healthy markets, we would expect to see other participants attempt to step in and reprice these assets. However, in distressed conditions, there may not be enough liquidity or willingness for participants to act.

In theory, active managers play a key role here. While market makers will sit at the top of the order book providing a constant market and palatable bid/ask spread, active managers provide what is known as order book depth/liquidity. These participants place orders at prices where they are willing buyers/sellers. As the role of active managers lessens, significant flow imbalances have the potential to send prices spiraling.

Risk Factor 3: Fickle Liquidity and Increasing Leverage

One of the most prominent factors impacting modern financial markets in the age of electronic trading has been the rise in high-frequency trading firms (HFT). Their impact on liquidity conditions during different market environments has been debated, with most arguments falling into one of two camps.

The first contends that HFT helps to reduce bid/ask spreads, thus improving liquidity and facilitating a more efficient form of price discovery, which is the main function of any market. The other side of the argument suggests HFT liquidity is unreliable at best, and only provides what is known as ‘at-will’ or ‘ghost’ liquidity, which only exacerbates price volatility.

There is no definitive conclusion as to whether or not HFT is a net positive or negative with regard to liquidity conditions in modern financial markets. However, there are many examples throughout its very short history in which small errors in HFT environments resulted in catastrophic losses and market impacts (e.g. Knight Capital Group, the Flash Crashes of May 2010, and August 2015).

A key factor for HFT trading strategies is the substantial leverage/margin that is employed within their systems. As we’ve previously discussed, margin requirements increase during periods of higher market volatility, which leads to a decline in available capital (net liquidity in the system). Therefore, firms that operate under strict margin parameters (e.g. HFT firms) are more severely impacted and are often forced to reduce their risk during times when liquidity providers are needed most. Unsurprisingly, studies have shown that stocks with a higher percentage of HFT participants (very liquid, index constituents) experience disproportionate impacts with respect to changes in margin requirements.

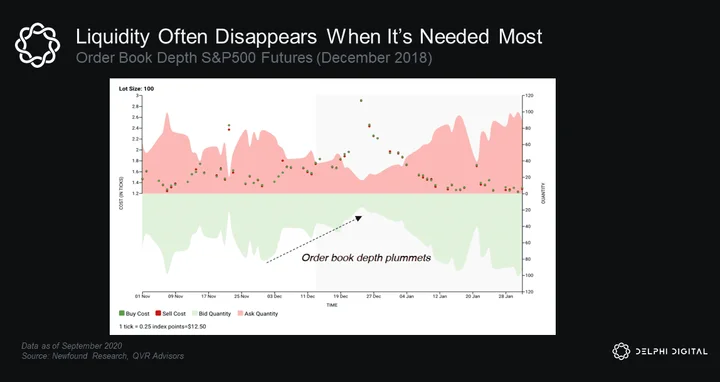

This leads us to a modern market phenomenon many have observed over the last 15 years – markets consistently experience a rapid deterioration in liquidity conditions during periods of market stress. Not only do we see order book depth evaporate, but bid/ask spreads also widen significantly, flying in the face of the supportive HFT argument made earlier.

Variable liquidity as a result of HFT is not an inherent problem with modern financial markets. The problem arises when variable liquidity turns into rapidly deteriorating liquidity during the precise time in which liquidity is needed most. Martin Wolf said it best in the Financial Times, “Beware the liquidity delusion. Market liquidity is like a fickle friend, and likely to disappear when one needs it most.”

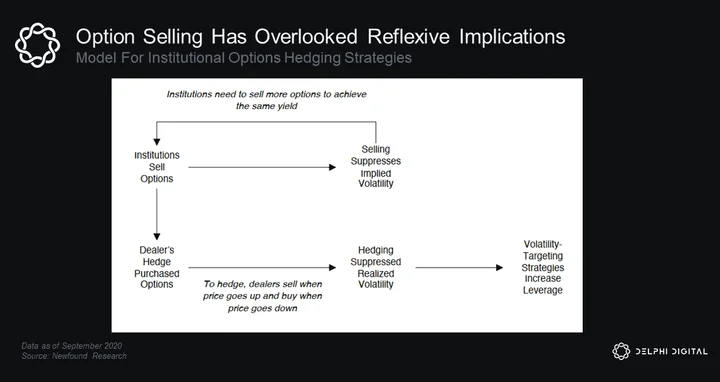

Options activity plays an important role in modern financial markets, as options account for a substantial amount of daily notional volume and value. Due to the size of these markets, we must take into account the impacts that these products have on the underlying assets they reference.

Consider the above diagram, which explores the dynamic between options selling and its impact on market participant decisions. Let’s use an example to illustrate.

A large insurance company decides to sell calls to increase yields, driving implied volatility lower. Future investors now need to sell more calls to achieve the same yield that the insurance company previously captured. This drives the implied volatility even lower as the amount of call selling increases. Options dealers must hedge their exposure, which suppresses realized volatility further. This is all well and good until it’s not. If, at any point, the market begins to sell off, massive position unwinds will begin to take place.

These complex structures are not exclusive to US institutions, either. Many banks in Asia and the EU have resorted to similar strategies to continue generating yields as global interest rates have fallen to near zero – or below zero – over the last 10 years. This type of environment has essentially pushed many of these institutions into ‘crowded trades’, which increase the risk of large potential unwinds. The intricacies of the institutional options hedging process are a bit beyond this report, but you can learn about these strategies in more depth here.

Liquidity Cascades: Putting it All Together

Liquidity cascades have become a more frequent market phenomenon over the last 15 years. This shift can largely be attributed to the major factors we’ve discussed: accommodative monetary policy, the prominent rise of passive investing, and insufficient liquidity in the face of increased leverage. As noted, the common denominator behind all of these risk factors is inherently related to liquidity. Corey Hoffstein’s description of market incentive loop flows is as follows.

Some adverse event triggers a disruption in markets. The Fed institutes an accommodative monetary policy to kickstart the economy and stabilize markets. This drives down yields and pushes investors further out on the risk curve, in part because they have fixed dollar liabilities they need to match. This causes investors, especially institutional investors, to seek out alternative sources of yield. Selling calls is one alternative that’s grown in popularity, and with it the need for increased hedging by options dealers.

Meanwhile, the Fed’s backstop creates renewed confidence among investors, so they start pouring money into the market. The growing role of passive investment strategies (which are largely divergent trading strategies) creates distortions in the market as price momentum benefits outperformers via new fund flows.

The increase in flows to passive strategies makes basket trading more prominent, which leads to “information leakage” across assets and more permanent price distortions. Coincidentally, many basket traders are often high-frequency trading firms, and the liquidity they provide is often fickle.

Eventually, the market hits a period of extreme stress. When that happens, all of these investors begin rushing for the exits at the same time, attempting to offload the riskier securities and trades that now comprise a material portion of their portfolios. Market makers and HFTs also reduce their risk, which is exacerbated by the amount of leverage they employ. So at the very moment when liquidity is needed most, it’s suddenly nowhere to be found.

This increases the potential for sudden liquidity cascades considerably.

Whether or not fickle liquidity is a byproduct of the strategies employed or margin constraints applied to these participants (or a combination of the two), the end result is the same. There is a severe dislocation in liquidity needed versus net available liquidity in times of stress, often resulting in sudden liquidity cascades and price distortions. The Fed then responds to these periods of market stress, providing relief through accommodative policies that inject liquidity into the financial system, thus restarting the market incentive loop once again. Time is a flat circle.

How Does This Apply to Crypto Markets?

It is worth applying everything we’ve learned about traditional markets, their evolution, and the latent risk factors of liquidity cascades to crypto markets. What are the similarities? What are the differences? Where do crypto markets go from here and how can market participants be prepared?

Perhaps the most applicable risk factor we’ve discussed as it pertains to crypto markets is the increased use of accommodative monetary policy and its macroeconomic implications. Crypto markets have been tied at the hip to global macro conditions and monetary policy over the last 12-18 months. Therefore, it’s not too surprising that many of the same knock-on effects that impact traditional markets are also influencing crypto asset prices. We’ve seen parabolic price increases during periods of accommodative financial conditions, and sharp and sudden drawdowns during tightening regimes. As crypto markets continue to mature and attract institutional capital, this relationship is likely to remain relatively strong.

A less obvious, but still critical risk factor is the dynamic between fickle liquidity and increased leverage. Crypto investors, much like traditional market investors, are often constrained by leverage parameters that can be subject to change. Crypto markets are also playgrounds for many high-frequency trading firms in much the same way traditional markets are, which means many of the same concerns present in traditional markets as it pertains to ‘at-will’ or ‘ghost’ liquidity are ever-present within crypto markets as well.

This risk is perhaps even greater in crypto markets as leverage (which typically exceeds traditional standards) has become the norm. We have seen liquidity cascades within crypto markets simply due to excess leverage built up in the system – a result of overcrowded trades during strong momentum trends.

Once a sell-off begins, leveraged crypto participants rush for the exits the same way we see in traditional asset classes.

The result is always the same. Liquidity cascades.

As the crypto market matures, one would expect it to develop many of the same characteristics traditional markets exhibit with respect to liquidity. What remains to be seen is how leverage within the crypto industry evolves over time. Will leverage be reined in, or will crypto remain a speculative sandbox for those with higher risk appetites? Options are still a relatively small part of crypto markets, but will certainly grow in the coming years. How will this impact market structure? What will be the impact if the same structural hedging practices develop?

The risk factor that shares the least in common with crypto markets is that of passive investment strategies. As of now, passive investment in crypto is minuscule compared to conventional markets. This will likely change as more products become available (e.g. spot ETFs) and institutional interest ramps up.

That being said, many of the market impacts of passive investing strategies are not as apparent in crypto markets. This can create an edge for crypto market participants which has been slowly taken away from traditional markets over the last 10-20 years. It is worth noting that although crypto markets are still dominated by active market participation, there are still similarities.

With respect to cross-sectional asset pricing, we see a similar pricing dynamic unfold. Most specifically, we see this dynamic during bull markets as different narratives emerge and gain traction. It does beg the question: does this lead to a similar type of momentum investing style as exhibited by passive divergent trading strategies?

For example, if we think back to our traditional market analysis, we remember that momentum strategies have been the best performers over the last 10 years (the strongest bull run in history), and some of the only profitable ones at that. We have identified similar momentum-based pricing dynamics at play between crypto bull market cycles and traditional market cycles.

If we can define momentum as something crypto native, such as narrative, we can apply a similar investing framework to crypto markets. Those who have been around for some time have likely already realized how powerful narratives are, and the momentum that they bring to price action. This is just one way of framing the conversation. There are many more ways to take advantage of the market incentive loop as it applies to crypto markets.

Caught in the Loop

After digesting the market dynamics that have evolved and are at play over the last two decades, the first question becomes immediately clear, “Are we caught in a loop? Are we stuck with this new phenomenon of increasingly frequent liquidity cascades, or are there other paths forward?” Unfortunately, the answer to this question isn’t nearly as clear.

Regulatory change is likely the most obvious factor that could bring a change in these liquidity dynamics. For example, regulatory changes that impact market maker behavior can result in a restructuring of liquidity profiles within markets. If we think about the core function of a market maker, which is to provide competitive, 2-way liquidity in a market while also attempting to detect toxic flows before other market makers in an effort to pull liquidity before market stress becomes apparent, we can see why regulatory change may have an impact. Without an incentive to provide liquidity during these times, market makers will simply attempt to avoid them altogether.

Regulations as they pertain to HFT are also a likely avenue in which a change can be brought to current liquidity dynamics. As we have discussed, HFT firms are often very capital-constrained. During periods of crises, capital becomes further constrained, exacerbating the issues. Giving large liquidity providers access to liquidity vehicles (in much the same way depository institutions have access to liquidity via the Fed discount window) can provide relief in times of stress.

We have also learned how large institutional hedging via options markets can have adverse effects on liquidity and increase the potential for liquidation cascades. Should there be a change in the dominant hedging strategies utilized by these large market participants, liquidity pressures will likely experience some form of alleviation.

Finally, the risk that passive indexing and investing pose to liquidity conditions in times of crisis has been discussed at length. As this form of investing continues to grow and take market share (already accounting for over 50% of investing AUM in the US), we would expect to see the destabilizing effects continue to materialize. How markets evolve and adapt to these changes still remains unclear. Will regulators have to step in here as well? Only time can answer this question.

If we zoom out even further, many have posed the question, “Can the Fed ever actually remove itself from financial markets after entrenching itself so deeply?” My gut instinct is that the Fed is indeed caught in a loop and cannot remove itself unless a systemic change occurs within the global financial system.

An often under-appreciated problem created by central bank policy has been the increased risk-taking behavior of market participants, as previously discussed. This has had hidden second-order effects. Most prominently, financial markets have become a proxy savings vehicle in the absence of attractive yields. This essentially ends the debate around whether or not financial markets can impact the economy; the reality is financial markets and the real economy have become increasingly interdependent.

As we know, the Fed has become the largest, most active market participant in recent years, essentially underwriting not just economic stability, but market stability. This makes it nearly impossible for the Fed to truly remove itself from financial markets under its current structure.

So, where does this lead? The most obvious example of a central bank taking an ever-increasing role in its domestic financial markets has been pioneered by nations like Japan. This route poses its own set of problems, as we have seen with the Japanese central bank’s YCC (yield curve control) experiment, and does nothing to address how we have arrived at the current situation.

This also poses an important question for crypto markets as a whole. As we have stated many times in the past, BTC is the most levered bet on global monetary debasement. In the unlikely scenario that the Fed can remove itself from financial markets to a significant degree, will BTC remain an attractive asset? The question shifts to the intrinsic value provided by BTC in the form of decentralization, self-custody, and cross-border transfer of capital, as well as the other useful innovations pioneered by the broader crypto ecosystem.

If you are a fan of financial markets, it is likely that there has not been a more interesting time to be paying attention in the last 50 years. The last 20 years have brought tremendous change and advances. There is no telling what the next 20 will bring.

0 Comments