Report Summary

Options volume has surpassed spot volume in traditional finance, but lags far behind in crypto. The small amount of volume captured by on-chain option protocols is dominated by centralized market makers.

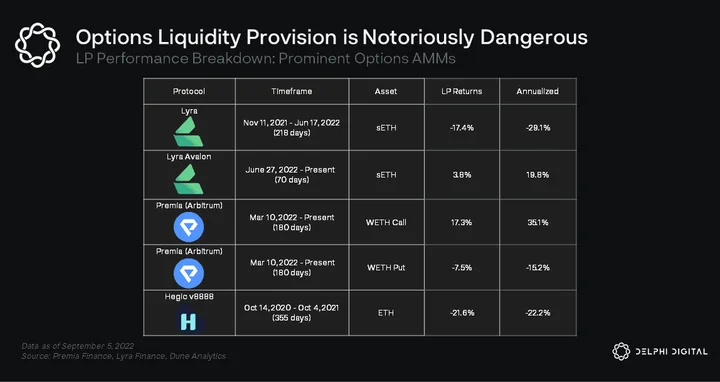

Options AMMs have thus far provided traders with an incomplete offering at non competitive prices, and have left LPs collectively rekt. Typically, this is offset through aggressive liquidity mining rewards and token economics fluff.

After a promising v1, Lyra’s Avalon update delivers a breakthrough in peer-to-pool options protocol design. Delta hedging allows for sustainable liquidity provision and offers a comprehensive trading experience.

The Synthetix ecosystem offers many benefits, but its drawbacks exacerbate existing capital efficiency hurdles. If Lyra succeeds in capturing buy-side demand, the capital inefficiency of sUSD could be a lingering headwind for Lyra’s growth.

The LYRA and OP incentive program has provided a huge boost to protocol growth so far. The LYRA token itself is in the midst of a transition phase while xLYRA token economics are pending audit.

Lyra is currently working on an ambitious v2, which will likely explore partially collateralized options beyond just shorting. This will help to lower fees and provide a possible sunsetting avenue for the trade rebate program.

Introduction

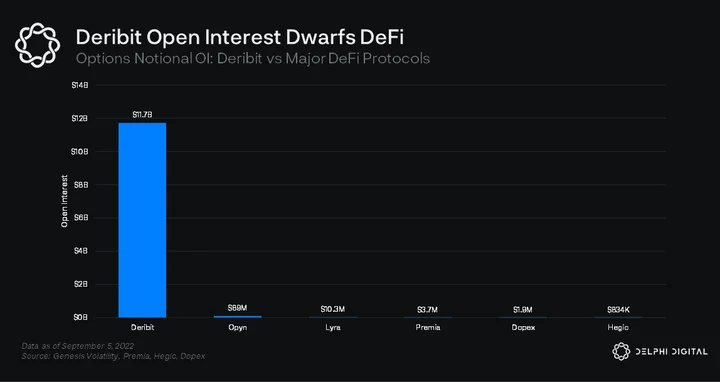

When it comes to crypto options, Deribit reigns supreme. As is the case with all centralized crypto platforms, DeFi teams are trying to build competitors that remove the market’s reliance on centralized infrastructure. However, despite an abundance of progress and product market fit in other DeFi subsectors, options growth has been largely underwhelming to date.

More recently, the options design space has picked up steam due to lower transaction costs and increased bandwidth on L2s.

Lyra is a DeFi options protocol on Optimism and is a cornerstone of the maturing Synthetix ecosystem. Lyra allows users to trade cash-settled European options fully on-chain via its AMM. Like other options protocols, Lyra has struggled in its battle with centralized options exchanges.

But we’re finally starting to see glimmers of hope within DeFi options. And with the recent launch of its Avalon update, Lyra is poised to battle CeFi giants for market share as it asserts itself as a worthy contender.

Before we can dig into exactly how Lyra’s mechanics work, we need a base understanding of what the competitive landscape is like.

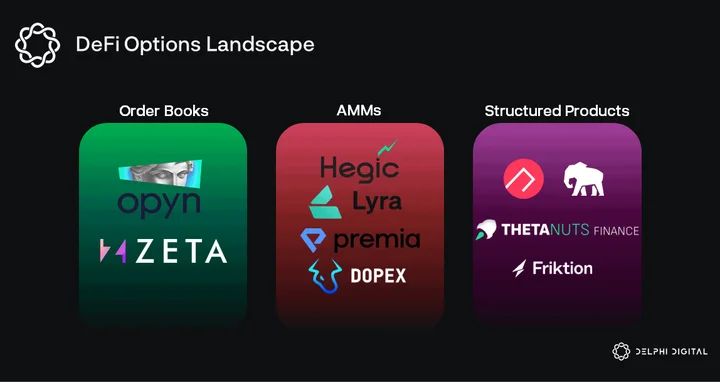

Competitive Landscape: Options AMMs

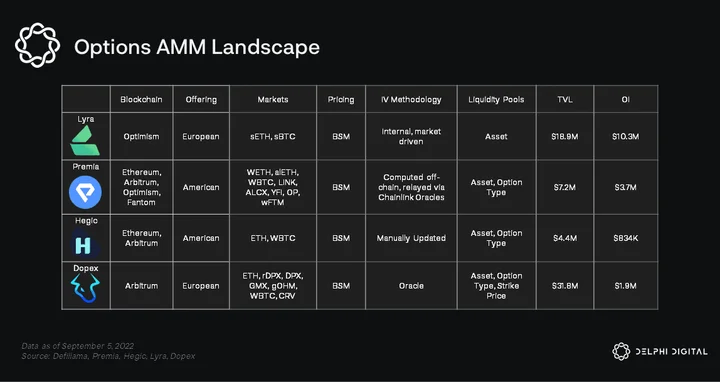

The main options AMMs include Lyra, Premia, Hegic, and Dopex. A full breakdown can be seen above, but each protocol has a select few defining characteristics.

- Hegic was the first options AMM, allowing traders to select any strike price. Hegic had many problems, from its manually updated implied volatility oracle to high prices and rekt LPs. Hegic Hardcore, its newest release, has pivoted to offering split liquidity pools for calls and puts, as well as providing easy access to one-click options strategies.

- Premia is a promising AMM offering American options with competitive prices. Premia computes implied volatility off-chain and relays it via Chainlink oracles. However, it suffers from capital inefficiency with its single-sided vaults for each asset, thus fragmenting liquidity. It has twice as many vaults per asset as Lyra but half the utility – traders can only buy, not sell, options.

- Dopex is a hybrid AMM and DOV. It uses a Black Scholes AMM to price options, but functions similarly to Ribbon, allowing users to deposit into vaults to underwrite options at their desired strike price. Dopex is the ‘other’ way to sell an option on-chain, but it is more clunky than Lyra. Dopex is doing interesting work with Atlantic options.

- Lyra offers a near-complete options trading experience without the off-chain concessions of its peers. Novel delta and vega hedging features protect LPs. Dynamic fees can sometimes heavily penalize users selling options back to the AMM, boosting the value proposition of Premia’s American options and sell-back feature.

The Synthetix Ecosystem

Synthetix is a derivatives platform that enables users to mint and trade synthetic assets, or synths. SNX stakers make up the collateral pool and are permitted to mint sUSD, which can be exchanged for other synths. These synths are pegged 1:1 to their corresponding crypto, fiat, stocks, or commodities via Chainlink oracles. Due to the nature of synthetic assets, Synthetix is able to onboard a wide array of assets without dealing with slippage, liquidity bootstrapping, and other overhead costs that plague development of nascent protocols.

The flexibility of sUSD and Synthetix provides an ideal foundation for bold projects to build on top of. If you’re interested in learning more about how Synthetix works and its burgeoning ecosystem, peep our recent deep dive.

Lyra utilizes sUSD and other synths as its sole form of collateral, and relies on projects within the Synthetix umbrella for its back-end operations. Synthetix’s composable architecture extends through Lyra, allowing protocols to seamlessly plug in to it. Brahma Finance and Polynomial Finance are two exciting projects building on top of Lyra.

- Polynomial Finance is a DeFi derivatives platform on Optimism. Its flagship product, Polynomial Earn, is a DOV product that is built on top of Lyra. The relationship is analogous to Ribbon and Opyn.

- Brahma Finance is a liquidity management protocol that features principal-protected yield strategies and an on-chain reputation system called Karma. The yield vaults harvest earnings from blue chip farms and use the proceeds to open up trades on Lyra and Perpetual Protocol.

How Lyra Works

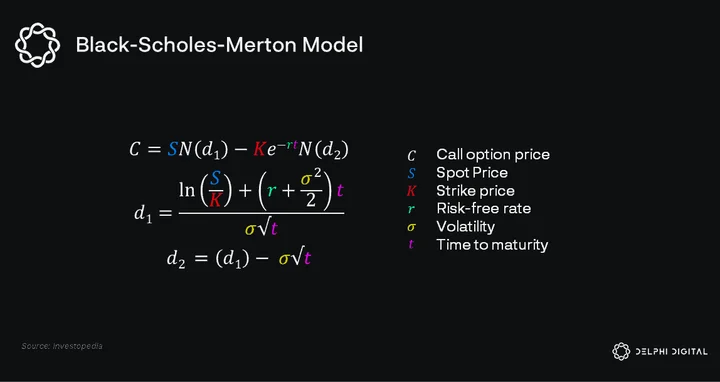

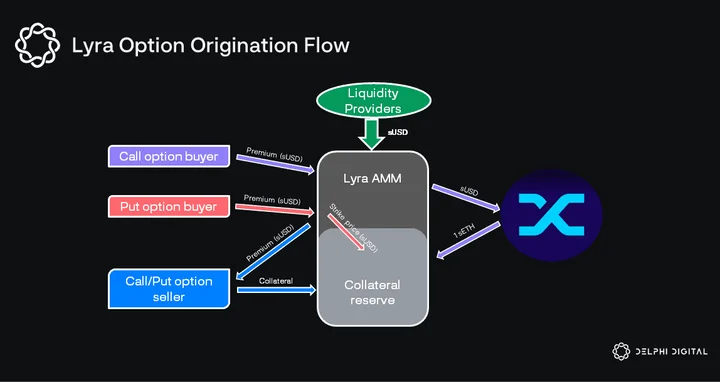

The Lyra AMM uses the Black Scholes model to price options. The AMM is uniquely capable of both buying and selling options – allowing traders to go long and short – with pooled liquidity from its asset-specific market maker vaults (MMVs).

While the math can appear overwhelming at first glance, the main idea here is that the Black Scholes price of an option is made up of four known/independent variables (spot price, strike price, risk free interest rate, and time/expiry) and one dependent variable (implied volatility).

Options mispricing can therefore be largely attributed to a mispricing of implied volatility. Lyra’s AMM produces a market-driven equilibrium price for implied volatility across all available strike prices. This output is known as the volatility surface and it is fed into the Black Scholes model to return option prices. Option contracts with low demand tend to signal an overpricing of implied volatility and vice versa.

Liquidity providers (LPs) deposit sUSD into Lyra’s MMVs, earning fees from traders and assuming the other side of all their trades. In order for the liquidity pool to guarantee settlement, calls are collateralized by the underlying asset and puts are collateralized by the amount of the strike price in the settlement currency (sUSD). When the AMM sells a sETH call, it purchases 1 sETH from Synthetix with LP funds. Users who wish to sell an option to the AMM must also collateralize the same way.

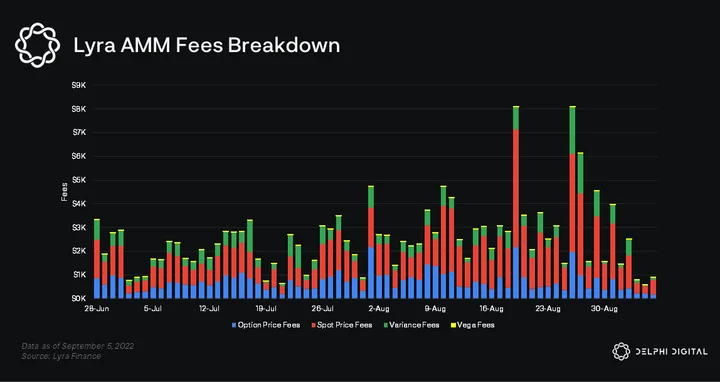

Lyra has four types of fees that are added to the option price:

- Option Base Fee: Flat fee applied to the option price.

- Spot Price Fee: Flat fee charged as a multiple of the spot price, used to cover hedging and exchange costs.

- Variance Fee: The variance fee is higher during volatile market conditions and is intended to mitigate impermanent loss for LPs. The variance fee scales with the traded contract’s vega, skew, and the difference between baseline volatility and its geometric time-weighted average volatility (GWAV). The variance fee is an important factor when it comes to liquidations and selling options back to the AMM before expiry.

- Vega Utilization Fee: Vega refers to the sensitivity of an option price to a change in implied volatility. The reading for vega is positive for option buyers and negative for option sellers. The Lyra AMM accumulates vega risk when it buys or sells a lopsided proportion of options. Lyra mitigates this risk by charging a dynamic vega utilization fee to compensate LPs when the vega risk of a pool increases.

Current Problems With Crypto Options

Before we get back to Lyra, let’s take a quick detour to understand critical problems with DeFi options. Bear with us; in the end, all of this ties together.

In traditional finance, option volume has surpassed spot volume in recent years. Between institutional players and the recent surge in retail interest, options have become a popular tool to hedge risk and speculate on price movements. The rise of Robinhood in recent years suggests there’s an enormous amount of latent demand for crypto options.

Could on-chain crypto options work if they could provide a Robinhood-like experience with efficient pricing? Where have DeFi options gone wrong so far?

DeFi options have delivered brutal returns for LPs, regardless of the implementation method. Poor returns can be attributed to three main causes:

- Option Mispricing: Market makers use sophisticated modeling and robust market data to rapidly update implied volatility. With options AMMs lacking the luxury of professional market makers, they often resort to unique methods of deriving IV, which can lead to stale or poorly estimated inputs.

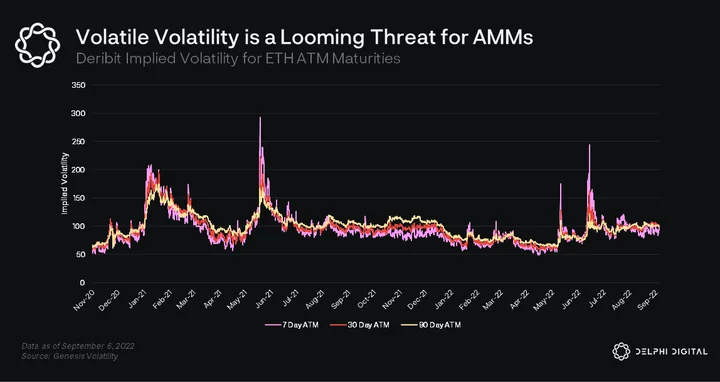

- Impermanent Loss: Professional market makers have the ability to quickly absorb information, react to it, and appropriately price it into options contracts in real-time. AMMs do not have this capability, and must let the price discovery mechanism run its course, leaving LPs on the hook during abnormal times. Impermanent loss for constant product AMMs essentially boils down to the opportunity cost of not being an omniscient trader. For options AMMs, impermanent loss is far more problematic, and results in LPs taking on liabilities without adequate compensation. In times of market volatility, the AMM could end up selling a basket of options with an implied volatility of 100% when realized volatility is 300%. These types of events have occurred sporadically over the past few years, and can cause substantial losses over a very short period of time.

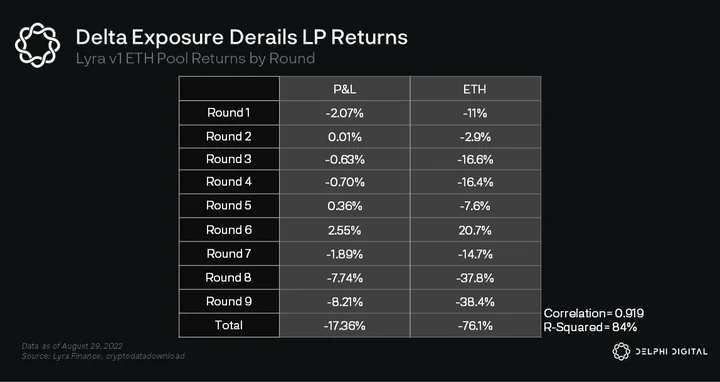

- Delta Reliance: Delta (Δ) refers to the sensitivity of an option price to a change in the price of the underlying. Because AMMs collateralize options with the underlying asset, they typically accumulate a high degree of exposure to the underlying. Large price swings in the underlying ultimately become the main driver of AMM returns. Consequently, this reliance on delta also poses a risk when the market moves against the AMM’s net positioning.

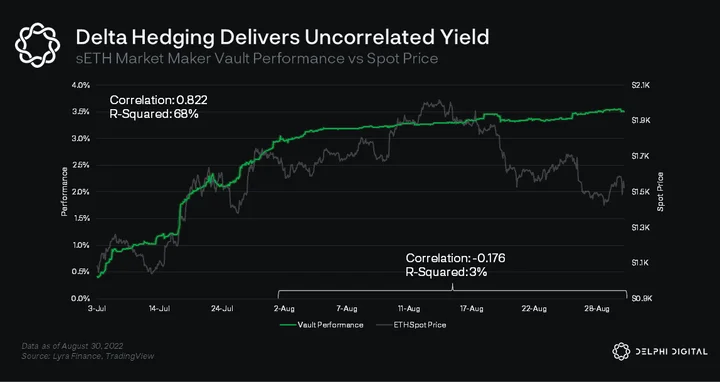

Despite the small sample size, the high R-Squared value supports the idea that AMM returns are mostly explained by fluctuations in spot price. Simulations suggest that if delta hedging had been enabled, Lyra’s sETH MMV return for v1 would have been between +0.5% and -0.82%.

In addition to poor returns, LPs have to deal with severe illiquidity. Options AMMs typically require users to lock liquidity for extended periods of time to match the maturity of the options contracts. This steep commitment combined with a poor track record is a deal breaker for most prospective LPs.

Crypto options have provided a poor experience for traders as well. Options AMMs have failed in a few key ways:

-

Incomplete Experience: Due to the maturity matching LP architecture, there is usually a very limited offering of strikes and expiries. In Lyra v1 and Dopex, for example, trading occurs in monthly or weekly rounds, with negligible liquidity in the middle to end of that period. A trader seeking an option for 35 days out on day one of a round would have to wait until the new round commences, buying that option at seven days out (a 28 day option). Traders are at the mercy of an arbitrary schedule, which is far from the ideal UX.

-

Bad Prices: Options AMMs typically have non-competitive pricing due to their inferior capabilities and need to protect LPs. Most AMMs are not capable of buying options, so traders are unable to short these overpriced options, which deters pricing from reaching equilibrium.

In a nutshell, options AMMs have thus far provided traders with limited options and a poor experience, and have left LPs collectively rekt. Typically, this is offset through aggressive liquidity mining rewards and token economics fluff. But, by now, we’re all well aware that this isn’t a sustainable solution.

Reflecting on Lyra v1 and Unpacking Avalon

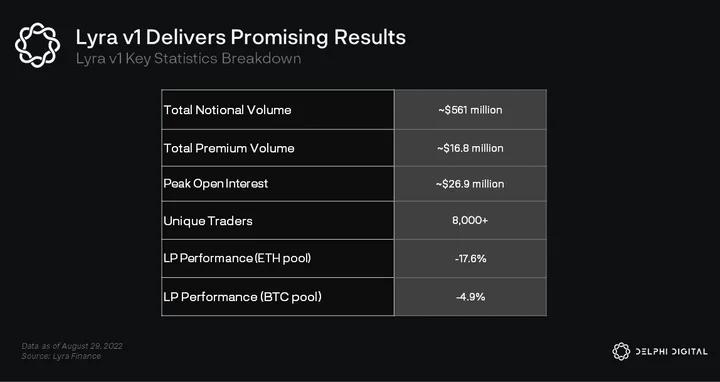

Lyra v1 launched in Nov. 2021 and enjoyed moderate success, with a cumulative total of ~$560M in notional volume and nearly $17M in premiums across ETH, BTC, LINK, and SOL. Lyra’s strong UI/UX helped it retain an impressive 70% of its users, with the average user completing nearly six trades. However, LPs on Lyra v1 did not fare so well. Lyra LPs suffered the same fate as those on other options AMMs, incurring losses of ~4.9% and 17.6% over seven months for BTC and ETH pools, respectively.

Lyra’s Avalon update was released on Jun. 27, delivering several improvements over v1.

Anytime Entry/Exit: In Lyra v1, options trading and liquidity provisioning occurred in four-week rounds. LP funds were locked for the duration of the round to ensure the risk associated with the pool’s outstanding liabilities was fairly distributed among depositors. Avalon allows users to deposit and withdraw at any time, subject to a seven day cooldown. At the end of the cooldown period, the fair value of an LP token is derived from the NAV of the pool, allowing the deposit or withdrawal to take place while still guaranteeing the fair distribution of pool assets and liabilities.

Rolling Expiries: Due to the pool structure of v1, traders were limited to a rigid selection of 7, 14, 21, and 28 day options, with negligible liquidity towards the end of the window. Avalon’s fluid liquidity provisioning enables Lyra to offer an expanded array of rolling expiries out to 3 months. Expiries are frequently added as near term options expire. Traders enjoy an abundance of strike and expiry options, with over 100 combinations.

This may not seem like a huge deal, but the prior architecture severely limited the viability and growth prospects of the protocol. Imagine a user wishes to speculate on the Ethereum merge by implementing a long calendar spread (buy a long-term expiry call, sell a nearer-term expiry call). Without rolling expiries, executing this is impossible. Users are, in effect, being told what they can buy rather than forming a thesis and being able to act on it.

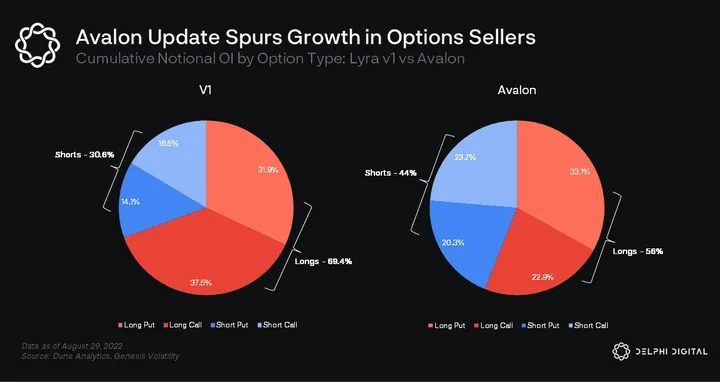

Partially Collateralized Short Positions: Avalon allows traders to partially collateralize short positions, allowing them to sell 4-5x as many options with a given amount of capital. This, of course, introduces the risk of liquidation. Partially collateralized shorting is a big deal for two reasons: it provides options traders with a more complete experience that rivals CeFi platforms and it allows the AMM to provide more efficient pricing.

In Lyra v1, options sellers made up only 30.6% of open interest. So far with Avalon, options sellers make up 44% of open interest. While changes in the mix of calls/puts can be largely attributed to market conditions, the balanced increase in call and put selling suggests Avalon is a key catalyst for short interest growth. A more balanced basket of options in the AMM leads to lower vega risk, resulting in lower vega utilization fees, and ultimately better prices for traders.

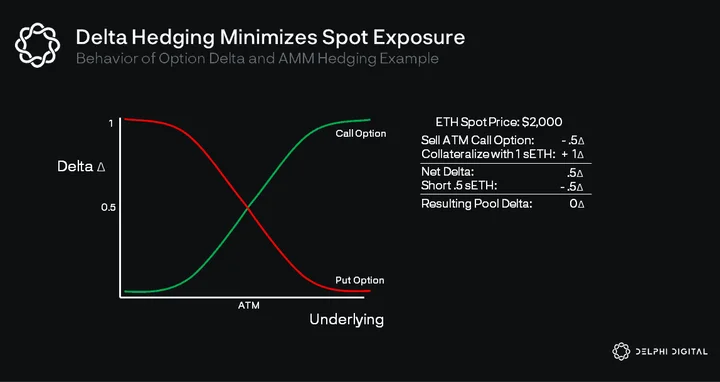

Delta Hedging: Perhaps the biggest improvement Avalon has to offer is delta hedging of the MMVs; providing uncorrelated yield and likely becoming the first long-term sustainable AMM in DeFi for options LPs. After successfully demoing delta hedging for the sLINK and sSOL MMVs at the end of v1, delta hedging is now live for sETH and future pools on Avalon.

Delta (Δ) refers to the change in the price of an option for a 1% change in the price of the underlying. While an ATM option has a delta of 0.5, a deep OTM option may have a delta of 0.1. A spot position – as well as perps and futures – have deltas of 1 (often called delta-1 products). As options move deeper ITM, they behave more like the underlying.

Every 6 hours, the Lyra pool hedger calculates total delta exposure and hedges via Synthetix.

As you can see above, the pool hedger dampens delta risk of the vault by over 90% on average. The vault can still gain and lose money due to sharp moves in the underlying while it carries larger than usual delta exposure.

Delta hedging is not an exact science and doesn’t eliminate all risk, but it allows the bulk of the AMMs P&L to come from its core business – market making for implied volatility and capturing spreads.

How Lyra Succeeds Where Competitors Have Failed

Other options AMMs protocols have tried to fix problems for LPs in roundabout ways, rather than treating the source of the issue. Hegic, Premia and Dopex split liquidity pools into call and put vaults, giving the user more control over the options they underwrite. This only serves to offload the burden onto end users and fragment liquidity.

DOVs sell deep OTM options, usually between 0.1-0.2 delta. Premia and Hegic are selling options that are often at the money or near the money, resulting in larger premiums earned at the expense of more frequent drawdowns.

Lyra’s delta-hedged market maker vaults flip the experience for LPs. From July onward, the ETH MMV has an R-Squared of 67%, a modest improvement over v1. But this is quite misleading, as ETH was coincidentally roaring at the same time that Avalon had just launched. The vault was at full capacity, leading to an explosive growth period.

When looking at the month of August (the start of liquidity mining and a more business-as-usual period for the vault), R-Squared is only 3% with a slightly negative correlation. Liquidity provisioning on Lyra has become an organic source of uncorrelated yield, rather than a treacherous game of hot potato.

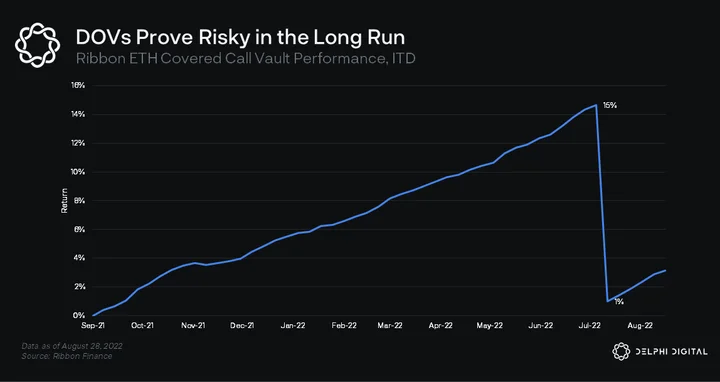

Lyra’s MMVs are likely to erode the value proposition of DOVs over time, forcing them to pivot to other use cases and cut fees. Lyra’s uncorrelated returns force covered call/protected put vault depositors to consider their position for what it truly is – a risk-on strategy that is dangerous if handled passively.

This phenomenon is showcased by the performance of the Ribbon ETH covered call vault. After consistently delivering 30-40 bps of weekly yield for nearly a year, vault depositors were caught out by ETH’s recent price surge, wiping out most of the vault’s earnings to date.

Option sellers are accepting unlimited downside in exchange for limited upside. As a result, LPs suffer from the same critical flaw of the Martingale betting system: small incremental wins are not sufficient to offset inevitable tail risk in the long run. DOVs allowed LPs to go from playing penny slots to playing Roulette. Avalon allows LPs to play Blackjack as the house.

For traders, Lyra’s Avalon update builds on the strengths of v1 and offers a more complete experience. Lyra v1 was already ahead of the competition with the ability to short an option on-chain – a surprisingly difficult endeavor. On a one-sided options AMM like Hegic or Premia, if a user believes an option to be overpriced, they cannot act – so they simply leave.

With a two-sided AMM like Lyra, a trader that believes the AMM is overpricing volatility can sell those options back to the AMM. While Lyra v1 was unique in offering short options, its capital inefficiency limited its effectiveness. The premium required to buy five options is miniscule compared to the collateral required to sell those same five options. In addition, locking up 1 ETH collateral for weeks in order to capture a small perceived mispricing in an option premium is futile. With partially collateralized shorting on Lyra, prospective traders have no excuse – they’re either a buyer or a seller.

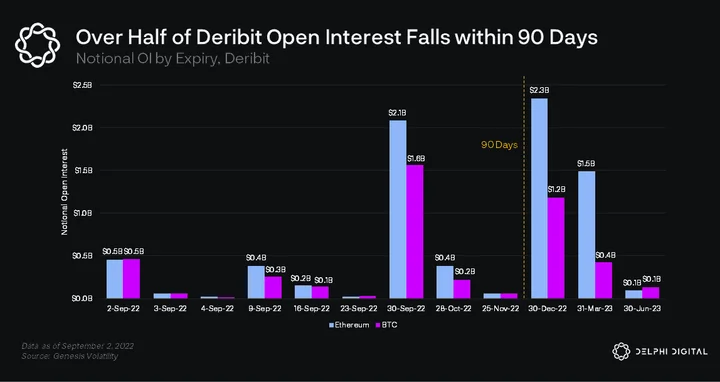

The robust selection of strikes and rolling expires dating out to three months is an unprecedented feat in crypto options. This offering is nearly on par with Robinhood, and meets the majority of the demand for crypto options. $6.4B of the combined $12.1B of Deribit open interest is in contracts expiring within 90 days. With the Avalon update, Lyra’s total serviceable market has reached 53% of Deribit’s massive business.

When Lyra proves it has the infrastructure and pricing locked in, the UI/UX will certainly not hinder customer acquisition. Lyra’s UI is remarkably similar to Robinhood; allowing users to see Greeks, the spread, implied volatility, payoff scenarios and more.

Remaining Obstacles for Lyra

Capital inefficiency remains a major problem in the options space due to the full collateralization of options. Traditional market makers can use a variety of hedging instruments to limit the capital burden of their liabilities. While order book protocols like Opyn and Zeta already employ partial collateralization and cross margining to boost capital efficiency, such mechanisms are more difficult to implement for an AMM. Therefore, notional open interest is capped by value locked in the protocol.

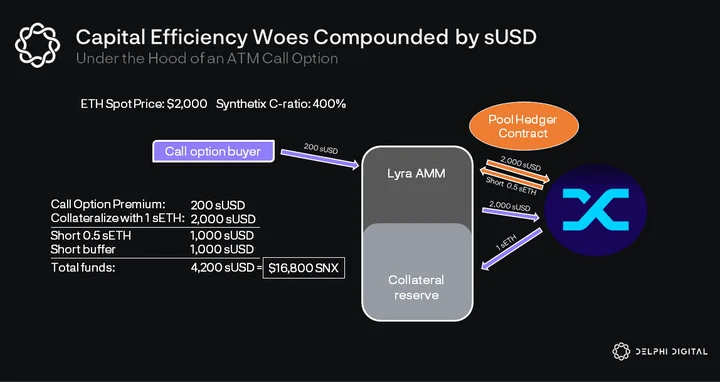

Despite all of the backend streamlining benefits, building on sUSD compounds this particular issue for Lyra.

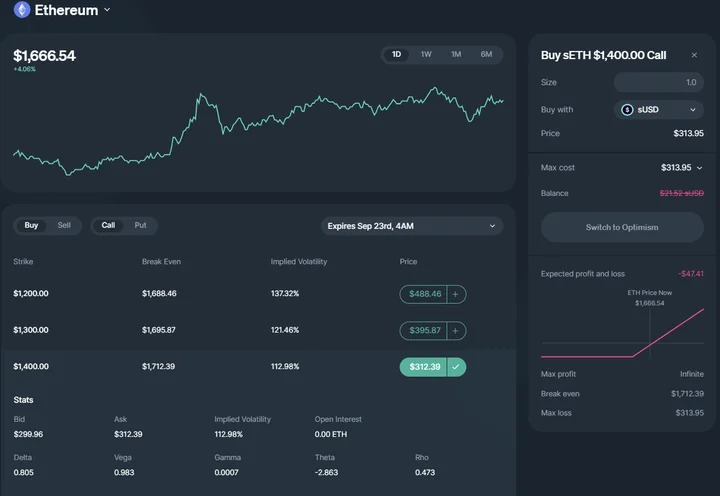

Let’s recall the option origination and delta hedging examples above and explore the capital required to underwrite one ATM call option. When considering the Synthetix C-Ratio of 400%, and assuming ETH price is $2K, the ATM call option in the graphic above requires the use of $16.8K of SNX.

Due to this structure, capital efficiency is inversely correlated with the price of the underlying. At ETH’s ATH of $4.8K, the same transaction would have required $39.2K of SNX. This suggests that Lyra is not only an asymmetric bet on SNX/USD, but a bet on SNX/liquidity-weighted synth index as well. This will continue to be an issue as Polynomial, Brahma, and other protocols building on top of Lyra try to foster organic growth, as they are currently limited to very low TVL caps.

If disillusioned DOV users who got caught out during the recent rally were lured to Lyra’s delta hedged MMVs, it would be difficult for sUSD to absorb that demand.

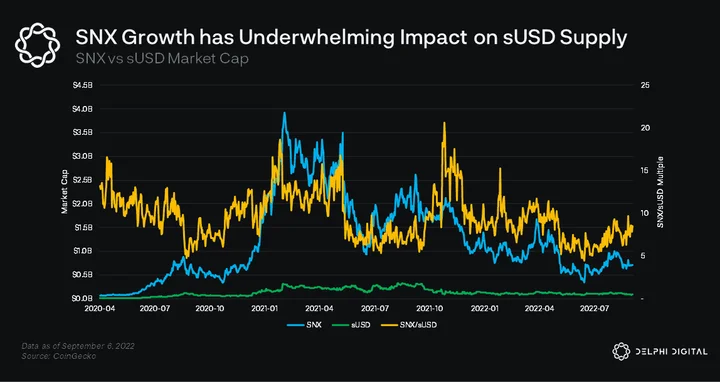

SNX growth has seldom correlated with sUSD supply growth. Even at SNX’s ATH market cap of ~$4B, sUSD has been unable to breach a circulating supply of 330M. To absorb the $100M of value locked in DOVs, or to make a dent in Deribit OI, we are looking at some pretty absurd valuations for SNX.

It is very likely Lyra sees growth plateau – due to these semi-exogenous reasons – while the DeFi options space solves collateralization issues and Synthetix increases sUSD liquidity. This heavy reliance on Synthetix could be long-term detrimental to Lyra if Synthetix fails to scale synth liquidity and Lyra doesn’t find a way to pivot.

Capital inefficiency tradeoffs are not new for DeFi protocols. MakerDAO found itself in a similar situation when DAI was backed mostly by ETH. DAI had demonstrated product market fit, but scalability was capped by ETH’s valuation, limiting its use case as the dominant DeFi stablecoin. Maker addressed this by onboarding more collateral types, including USDC, Uniswap LP tokens, and real world assets.

These measures have allowed DAI to successfully scale, but not without surrendering some of its brand and product market fit. DAI is no longer the universal non-ETH LP pair and DeFi darling it once was, often being called “wrapped USDC.” And with looming regulation over USDC, Lyra’s censorship resistance could be called into question – as DAI’s has – if they were to onboard it as collateral.

Liquidity will always be an issue for Lyra as long as it is built on Synthetix. Lyra just has to work harder for its liquidity than others.

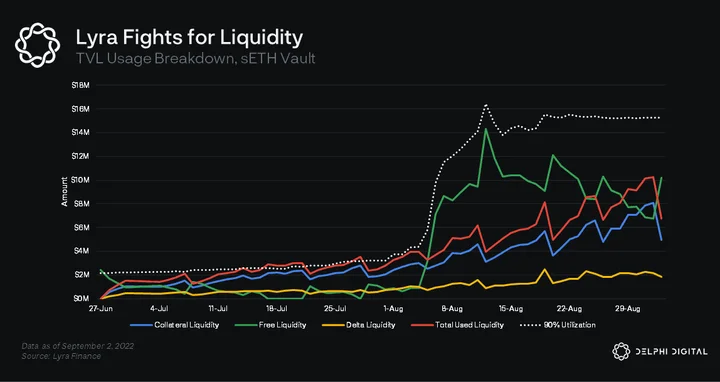

The utilization ratio represents a tightrope for balancing the interests of AMM stakeholders. With a consistently high utilization ratio, LPs enjoy impressive yield, but the vault is constantly in paycheck-to-paycheck mode, counting on weekly expiries to free up collateral.

The first month of Avalon was characterized by the constant threat of circuit breakers halting trading and locking liquidity due to the utilization ratio hovering around 85%-90%. This is similar to the Lyra v1 and Dopex situation described above. The liquidity mining program injected millions of TVL, but also diluted existing LPs. In August, the sETH MMV earned about 0.6%, with the utilization ratio often in the 35%-45% range, compared to July when the vault earned 3%.

Lyra can counter this by launching additional MMVs when vaults have excess liquidity, luring LPs to better returns. Ideally, this flywheel culminates with numerous MMVs having utilization ratios stabilized around 75%, balancing returns with reliability. The utilization ratio will be important to monitor going forward.

LYRA Token and Incentive Program

In order to bootstrap liquidity for the AMM, Lyra has just launched its incentive program. Since Avalon was released in late June, Lyra’s LPs have earned 3.8% yield and facilitated over $72M of notional volume. Lyra’s pointed incentive program targets both liquidity providers and traders, rewarding them with LYRA and OP tokens. Users can stake LYRA for stkLYRA to earn boosted rewards from LPing.

Since the program was launched, deposits to the MMV have skyrocketed, and pool utilization has dropped to around 35%. Lyra has been able to bootstrap enough liquidity to launch its second MMV – sBTC. The incentive rewards for the ETH vault currently sit at ~6% APY, which only serves to complement the impressive 20% annualized yield delivered by the vault organically. The token rewards don’t function as a crutch for a broken model, which bodes well for capital stickiness and the ability for Lyra to bootstrap MMVs for additional synths.

For Lyra to scale, growth in liquidity needs to be paired with growth in trading demand, or the returns for LPs will be too low. Fees make up around 7.5% of option prices on average, with spot and variance fees being the most painful. Trade fee rebates in LYRA and OP help to soften the blow and serve as a bridge to Lyra v2, which will allow for a reduction in fees.

Rewards from trade rebates must drive growth in options demand in order to keep the organic portion of total yield high. Despite delivering a functioning product and a clever incentive program, changing consumer behavior in such a drastic way is a tall order.

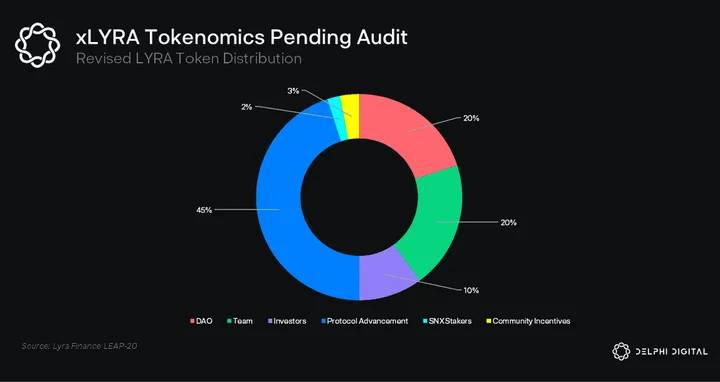

The LYRA token is currently in a transition phase while the new xLYRA token economics are pending audit. Lyra’s new token economics feature a standard veToken model, allowing users to vote lock tokens for up to one year in exchange for boosted rewards and voting power. The token distribution will be simplified as well, with four incentive buckets being combined into one all-encompassing allocation to be used for the advancement of the protocol:

- LP rewards – 15%

- Trading rewards – 15%

- Security module – 10%

- Token liquidity – 5%

This leaves a large portion of the supply with an ambiguous lack of direction.

Looking Ahead

Lyra v2 will likely explore partially collateralized options beyond just shorting, which will help to lower fees and provide a possible sunsetting avenue for trade rebates. The ambitious features of v2 will likely require the return of the security module. The security module insures traders and LPs in the event of a shortfall, and provides additional utility and revenue streams for LYRA token holders.

In the meantime, Avalon will soon use Synthetix perps for delta hedging, considerably lowering the capital burden of the pool hedger. Lyra is actively working with Synthetix to develop liquidity solutions for sUSD. Second order effects of potentially disruptive products such as Lyra’s MMVs and dHEDGE’s one-click debt mirror index are still unclear.

It’s quite possible that borrow rates for sUSD increase as opportunity cost rises and SNX stakers become reluctant to sell their sUSD. For the time being, the Synthetix ecosystem dynamic falls somewhere between synergistic and cannibalistic.

Lyra’s Avalon update is undeniably a huge step forward for on-chain options. Avalon is a remedy for the most severe pain points of DeFi options thus far. But the DeFi options space must overcome capital efficiency and liquidity issues in order to compete with centralized exchanges. It must also fight to reshape consumer behavior and establish on-chain protocols as a viable trading venue. Lyra’s concentrated bet on the Synthetix ecosystem could make these issues more difficult in the medium term, but it also offers a higher ceiling if liquidity issues are sorted.

0 Comments