Managing Expectations Heading Into "The Merge"

APR 21, 2022 • 11 Min Read

Report Summary

The actual date of The Merge is still unknown but based on the rate of progress, and some expert opinions, we expect to see The Merge occur around late Q3 or early Q4 of this year. A go/no-go decision on performing The Merge or postponing it is set to take place on April 29th during the Ethereum All Core Developers call.

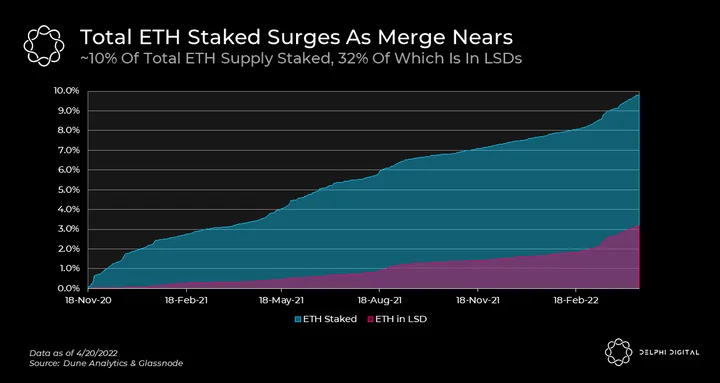

Currently, ~9.7% of the total ETH supply is being staked. All staked ETH will remain out of circulation until another upgrade finally happens after The Merge is complete. As a result, staking will continue to be a significant supply sink for ETH into the foreseeable future.

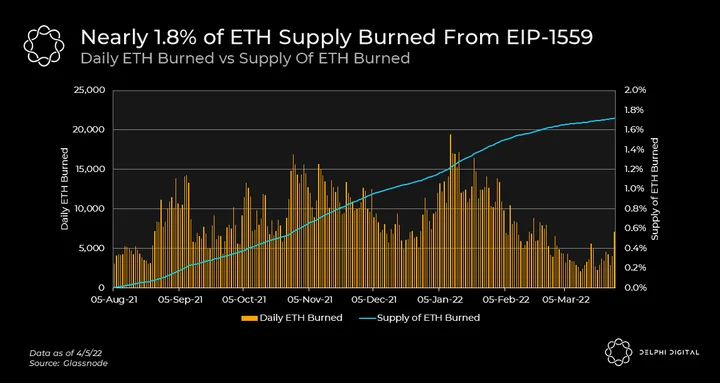

EIP-1559 was the first step to turn ETH into a deflationary asset and, since its introduction in August 2021, it has led to ~1.8% of the total ETH supply being burned. The Merge will take this a step further by slashing ETH issuance anywhere between 60-90%.

Depending on the amount of ETH staked, network fees, and MEV after The Merge, ETH staking yields could range between 8.7-10.3%.

Currently, the validator activation queue is just over 2 weeks long and is expected to increase as more ETH is staked. The validator queue could present an opportunity for liquid staking derivative projects like Lido if they are able to subsidize yields during the queue and continue onboarding users.

Introduction

While the nomenclature around the project has changed over the past few years, “The Merge” refers to the Ethereum mainnet transitioning from a Proof-of-Work (PoW) system to a Proof-of-Stake (PoS) system. This change will improve Ethereum’s energy efficiency, scalability, and decentralization. After The Merge, miners will no longer be needed to validate transactions, as that responsibility will shift to validators who have earned the right to participate by staking ETH.

In order for The Merge to be completed, the current PoW mainnet (i.e. ETH 1.0) will be combined with the Beacon Chain, introduced earlier under ETH 2.0, to create a new chain that utilizes PoS moving forward while maintaining the prior history of the Ethereum network.

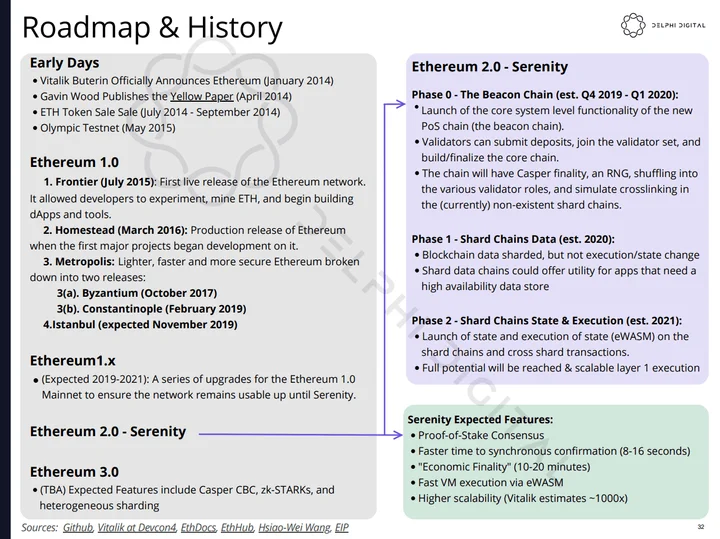

Ethereum’s History & Roadmap

The Merge has been anticipated for several years now after repeated delays to the initial roadmap. To give context for how expectations have evolved over time, we’ve provided a historical roadmap that was included in one of our first ever research reports back in March 2019. As shown in the purple section, the entire ETH 2.0 transition was initially expected to be complete at some point in 2021. However, the reality of the engineering required more time, as we’re still in ‘Phase 0’ essentially.

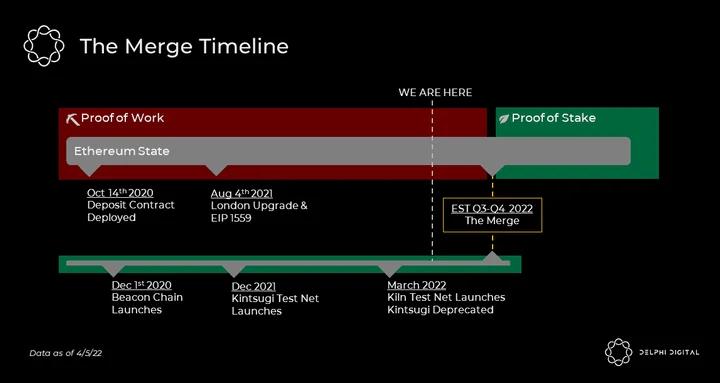

It’s important to note that even though Ethereum has suffered setbacks in this transition, it hasn’t been without good cause. There was crucial work being done to get in place the infrastructure required for Ethereum to successfully transition. At the time of writing this report, Ethereum is valued at over $380B and supports hundreds of other applications that require it to function. Not rushing such a monumental change is particularly important when you consider all of the value within the Ethereum ecosystem that would be negatively affected if something were to go wrong. In the graphic below, we’ve provided a more recent timeline of events, which we’ll contextualize in the following section.

Ethereum requires validators to propose blocks and validate transactions to operate securely under this new model. To enable this, a staking deposit contract was deployed on October 14th 2020, allowing would-be participants to send in a required 32 ETH so that they could be added to the validator list. If a validator experiences downtime and/or proposes malicious blocks, this stake can be slashed by the network. This forms the security foundation of Ethereum’s move to PoS.

At this point in time, there is no way for validators to remove their staked ETH. While validators can opt-out of their duties this only prevents them from being slashed and they won’t be able to retrieve their locked ETH until another update to the chain is made post-merge. Meaning that even months after “The Merge” takes place, validators’ funds could still be constrained, possibly resulting in the biggest supply sink ETH has ever experienced.

Following the deployment of the deposit contract, Ethereum launched its Beacon Chain on December 1st 2020. The Beacon Chain didn’t alter anything about the Ethereum chain used today, but instead was the introduction of PoS into the Ethereum ecosystem. The Beacon Chain’s objective is to coordinate the network and serve as the Ethereum consensus layer post-merge.

Later on August 5th 2021, Ethereum underwent the London upgrade which included EIP-1559, this introduced a mechanism to burn ETH with each transaction. An in-depth dive into this burn mechanism can be read about in further detail here, however, we’ll touch on the important parts of it later in this report. The introduction of this burn mechanism was the first step in turning ETH into a deflationary asset, with The Merge taking further steps to ensure that this is the case.

The actual date of The Merge is still unknown, but based on the rate of progress and some expert opinions we expect to see The Merge occur around late Q3 or early Q4 of this year (2022). A go/no-go decision on performing The Merge or postponing it is set to take place on April 29th during the Ethereum All Core Developers call. If it is cleared to proceed, the real Merge would be planned for the aforementioned period. A detailed checklist regarding the steps that still need to be performed in order to complete the merge can be found in the Ethereum GitHub here.

Transitioning From Miners To Validators

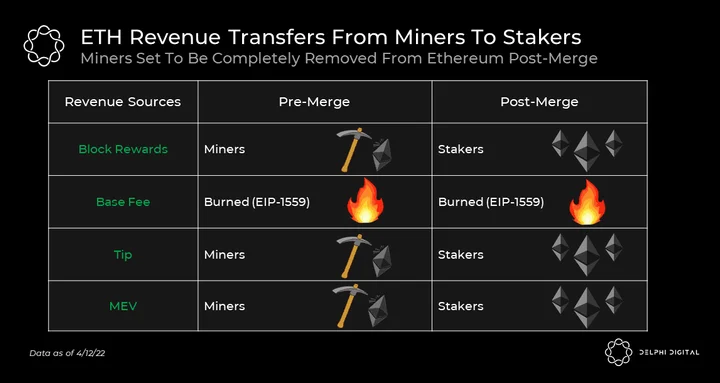

The change from PoW to PoS will drastically alter Ethereum’s economics. Miners will be completely cut out of revenue generated by the Ethereum network and that value will be returned primarily to ETH stakers/validators in a few different ways.

- Block Rewards: Block rewards are set to be slashed drastically following the merge anywhere between 60-90% depending on the amount of ETH staked, benefiting all ETH holders. The remaining block rewards are paid to ETH stakers/validators and are realized in the form of a staking rate.

- Transaction Fees & MEV: Since the implementation of EIP-1559 the base fee portion of transactions have been burned. Additional revenue generated through Tips and MEV are now paid to ETH stakers/validators and are realized in the form of a staking rate.

While miners are forced to sell a large part of the ETH collected via block rewards, Tips, and MEV to pay for costs, stakers/validators incur significantly fewer costs leading to less forced selling. Furthermore, since ETH validators/stakers already own a large amount of ETH it can be assumed they are bullish on Ethereum and would be more likely to hold these ETH rewards versus a miner.

All of these changes should significantly improve ETH’s value accrual (we will be diving into the numbers later in this post).

Staked ETH Continues To Grow

Since the deployment of the staking deposit contract in October 2020, there has been a consistent increase in total ETH supply being staked with a MoM increase of 12% from February to March of this year. Currently, about ~9.7% of the total ETH supply is being staked. With 32% of this in liquid staking derivatives (LSDs) and ~26% staked through exchanges.

For those interested in staking their ETH, there are a few different options to choose from depending on your available resources and skillset. One option is to become an ETH network validator. This is the most resource-intensive route but could provide the highest ROI since no other entity is taking a cut of the rewards you would earn as a validator. In order to become a validator, a 32 ETH stake is required in addition to resources that enable you to operate a validator node, such as a hard drive that can hold the ever-growing Ethereum state (~400GB for the main net execution chain data alone). A detailed set of the machine requirements to operate a validator node can be found here.

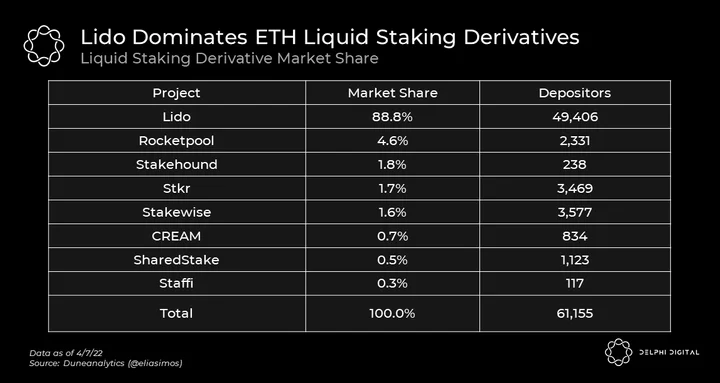

If you’re looking for an easier option to stake your ETH, you can also use a service such as Lido which takes care of the hassle for you. In addition, you gain the added benefit of liquidity via Lido’s staking derivative (stETH), however, there is a 10% fee charged on your staking yield in return. As shown in the table below, Lido currently holds over 88% of the market share for ETH liquid staking derivatives.

At the time of writing, Ethereum validators are receiving a 4.6% APR while those staking with Lido are seeing a 3.9% APR. This difference in yield is due to a 10% fee Lido charges on staking rewards alongside the validator queue (more on this later). Lido is still a solid staking option given its yield and liquidity versus other staking providers such as Coinbase which currently is only offering a 3.675% APR. While these are low single-digit yields, they’re still far higher than what can be achieved via alternative methods. For example, lending ETH on Aave only yields 0.33% APY. We will dive into a deeper breakdown of potential post-merge Ethereum staking yields later in this post.

Given the ease of use, integrations, liquidity, and yield offered on Lido’s stETH we expect it to continue attracting deposits and be a leading force behind Ethereum staking. If you wish to learn more about liquid staking derivatives and Lido please check out this previous report.

ETH Net Issuance and Staking Rate After The Merge

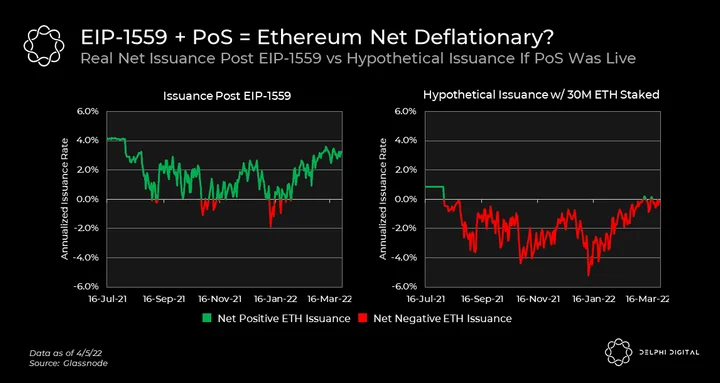

Since its introduction, EIP-1559 has led to ~$6.8B of ETH burned, just under 1.8% of the total supply. This was the first step in turning Ethereum into a deflationary asset. Net issuance of ETH has at times been negative (as shown by red-colored dips below). The Merge will take this a step further by drastically decreasing the amount of ETH being issued to validators post-merge, while still maintaining the same burn mechanism introduced by EIP-1559.

The above graphic presents us with two visualizations. The first chart shows us the real net issuance of Ethereum since EIP-1559 was enacted in August 2021, and the second chart shows us what net issuance would have looked like if Ethereum PoS were live over that same time frame. As we can see Ethereum’s issuance would have been significantly negative since EIP-1559 if PoS was up and running. Since issuance is based on the amount of ETH staked, in our example above we used 30M versus the current staked amount of 11.7M to be more conservative (a higher staked amount equals more issuance).

Beyond this not only would Ethereum have been net deflationary, but stakers would also have been earning a pretty sweet yield due to the Tips portion of transaction fees and MEV being returned to validators/stakers.

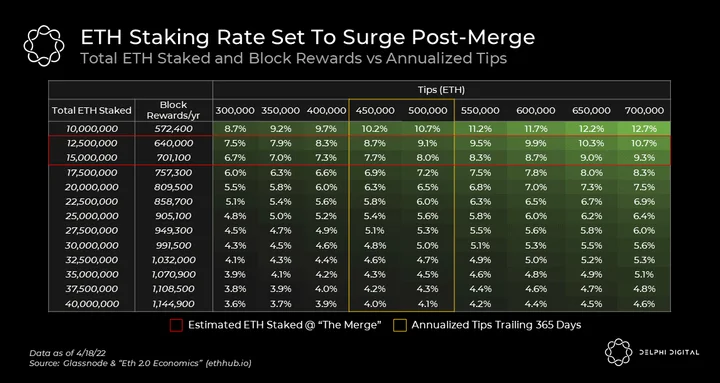

Although ETH staking deposits have been accelerating, if the merge occurs as planned in late Q3 or early Q4 we would likely see between 12.5M – 15M ETH staked with annual block rewards ranging from 640K-700K ETH. This represents a base APY of 4.6-5% from issuance alone. However, if we see transaction fees comparable to that of the last 365 days then the tips portion of fees could boost us up to a 7.7-9.1% APY (assuming tips = 15% of fees).

Furthermore, another potential source of yield is MEV (Maximal Extractable Value). This is additional revenue that can be extracted from deciding the transaction order within a block (ex Frontrunning). While diving deep into MEV is outside the scope of this paper we suggest you read our previous post here if you wish to learn more. Flashbots has built out a dashboard to help us track MEV but it certainly does not capture everything, a full description of what Flashbots accounts for can be found here. With that being said Flashbots has reported ~150K ETH generated by MEV in the past 365 days, using this as our lower bound we can expect MEV to add an additional 1-1.2% to yields at 12.5-15M ETH staked, bringing the grand total staking APY to a range of 8.7-10.3%. It will be very interesting to see if various validators/staking services can differentiate themselves by capturing more MEV and thus providing higher staking yields.

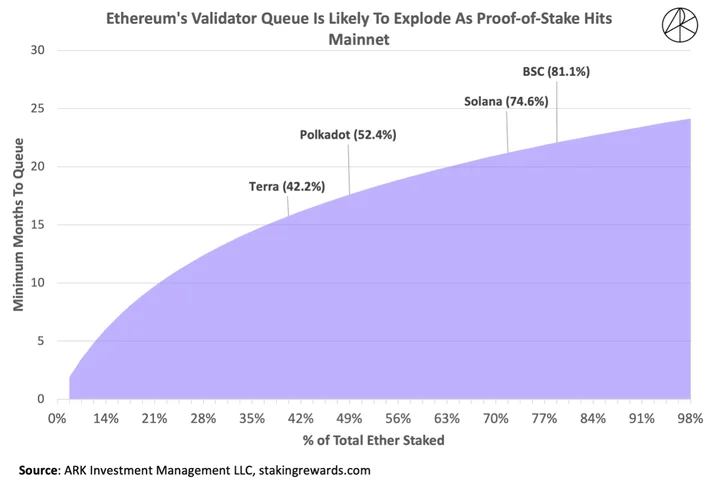

One last thing we’d like to note before wrapping this piece up is the validator queue. For every 32 ETH that is staked a new validator must be created and enters an activation queue before it can start earning yield. Currently, the validator activation queue is just over 2 weeks long. Right now the ETH staking APR is 4.6% but it could more than double following the transition to proof of stake meaning a surge in new stakers/validators and a significant increase in queue time.

The above chart was posted by Frank Downing (@downingARK) from Ark Investment Management and shows the potential length of the validator queue depending on the percentage of ETH staked. With the rise of liquid staking derivatives, we see a compelling argument for why the percentage of ETH staked could trend towards 80-100% over time. If users can benefit from both liquidity and yield then the opportunity cost of not staking is quite high. With a multi-month validator queue, we see a massive opportunity for liquid staking derivative providers like Lido to grab market share. Since ETH waiting in the queue will not be earning yield a project like Lido could continue to onboard users to stETH while subsidizing yield via their large treasury. This would only improve Lido’s already dominant position strengthening the network effects of stETH, allowing for more integrations into Ethereum DeFi.

Conclusion

With “The Merge” set to take place around late Q3 or early Q4 of this year, Ethereum is poised to benefit from some juicy staking yields and a significant reduction in issuance. While both of those could bode well for ETH’s price, we wouldn’t use that as the sole metric for success. Rather the focus should be on that which matters most – Ethereum safely transitioning into its hopefully more scalable and eco-friendly state.

0 Comments