Mapping The Moon: An Overview of Terra's Ecosystem

DEC 22, 2021 • 23 Min Read

Report Summary

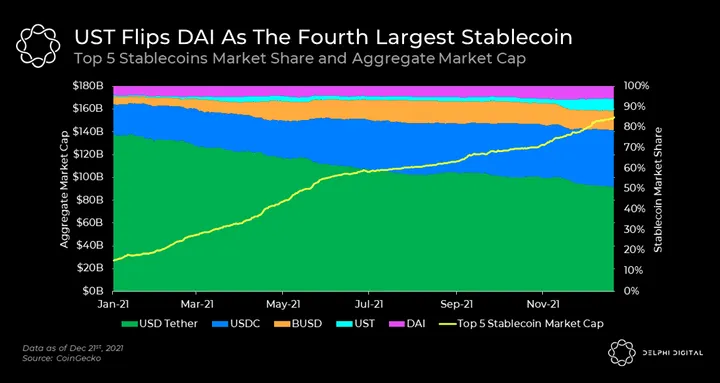

Terra’s native stablecoin, UST just flipped DAI as the fourth largest stablecoin with a $9.2B market cap. UST experienced extreme growth of ~50x in 2021 and is the only decentralized stablecoin among the top 5.

Every UST created burns $1 worth of LUNA, and every UST destroyed mints $1 worth of LUNA. This is, at its core, how UST maintains its peg. This mechanic has led to the net burning of ~33M LUNA in the past 30 days.

If UST can grow 150% in 2022 this will create over 13.8B UST, enough to burn roughly a third of LUNA’s circulating supply (>100% of the liquid supply) at $120 LUNA.

Terra’s TVL has grown to $16.6B, cementing it as the second largest L1 ecosystem behind Ethereum according to DeFi Llama.

Catalysts for LUNA include upcoming projects on Terra that will increase UST utility and demand. These projects range from DeFi to the Metaverse and gaming. There are dozens of high quality projects being developed on Terra right now.

Cross-chain initiatives to make UST more widely adopted and useful are currently in the works. This includes a seamless bridging experience, deep UST liquidity on key DeFi platforms for each chain, and having native dApps that leverage the power of UST.

The Decentralized Stablecoin Thesis

Before we get into the mix of all things Terra, there’s one very important thing we need to understand: why do decentralized stablecoins matter?

For the uninitiated, stablecoins are digital representations of various fiat currencies. The most popular and traded stablecoins are ones that are pegged to the United States Dollar (USD). Stablecoins enable users to transfer money in a cheap and quick manner; convert speculative crypto-assets into a stable alternative; and participate in the Decentralized Finance (DeFi) ecosystem. Thanks to the advent of public blockchains, stablecoins can do this without the frictions commonly associated with the traditional financial system.

Given the obvious use cases, stablecoin growth has been parabolic as they establish themselves as the backbone of the emerging DeFi ecosystem. These coins make up the majority of TVL deposited into top DeFi applications like Curve, Aave, and Compound. They’re also the main fiat trading pair on most exchanges, with over $150B in cumulative market cap and volumes of up to $300B per day.

Centralized stablecoins make up the majority of the market. USDT, USDC, and BUSD are a few examples of centralized stablecoins. They function as IOUs for USD in bank accounts or money market instruments attached to a legal entity, and they entail meaningful risk for users due to their custodial nature. Custodial risks that arise are centered around blacklisting coins on-chain and susceptibility to regulations.

To emphasize the custody risks let’s look at Tether (USDT). USDT is the largest stablecoin by market cap and volume, but it isn’t entirely backed by US dollars. A report released by Tether on June 30th 2021 shows that ~85% of assets are held in cash and cash equivalents (money market instruments). The other 15% are held in a variety of secured loans, corporate bonds, and other investments. While the assets Tether is investing in are relatively safe, USDT carries non-trivial redemption and regulatory risk.

The President’s Working Group on Financial Markets published guidance on stablecoins, recommending additional regulation for “user protection”. Following this report, the Chair of The US Senate Committee on Banking has requested additional information from prominent stablecoin providers such as Tether, Circle, Coinbase, and Binance U.S. At this point, it seems clear that some sort of additional regulation on stablecoins is imminent.

In light of this, centralized stablecoins like USDC and BUSD that fall under the purview of U.S. regulations could also prove to be a bane for DeFi users. When the assets that make up the lion’s share of DeFi liquidity are centralized, the censorship resistance of the entire ecosystem gets called into question.

Decentralized stablecoins are the need of the hour, and luckily there are already multiple efforts underway. Broadly, there are two types of decentralized stablecoin designs:

- Over-collateralized stablecoins: These stablecoins allow users to mint an asset pegged to a fiat currency (like USD) by borrowing against their crypto assets in an over-collateralized manner. Simply put, you have to put more money into the system than you take out. This design is the most common and has low financial risk, but a key constraint is capital intensity. One potential risk is re-centralization via collateral. DAI, the largest over-collateralized stablecoin, has 44% of its collateral in centralized stablecoins. If these coins were blacklisted and thus unmovable, MakerDAO (which issues DAI) would not be able to meet all of its redemptions.

- Algorithmic Stablecoins: These function in many different ways, but the gist of it is to use financial incentives to encourage the market to keep the stablecoin at its peg. These assets are easily scalable — in terms of supply — and more resistant to centralized forces. Although, they come with the trade-off of less financial security than over-collateralized counterparts (which we get into later in this report).

USD Terra, or UST, is an algorithmic stablecoin pegged to the dollar, and native to the Terra blockchain. UST’s mechanism arguably makes it the most censorship-resistant stablecoin, and the rest of this report examines UST’s traction and how it can transform DeFi.

Terra: Building Around a Decentralized Stablecoin

While Terra may be a Proof of Stake L1, the utility of its token, LUNA, extends beyond mere staking. When UST is created, LUNA is burned. This ensures that when value is created (UST is minted), an equal amount of value is also destroyed (LUNA is burned). This ties back to staking utility because as UST in circulation grows, more transaction fees are generated which then accrue back to LUNA stakers.

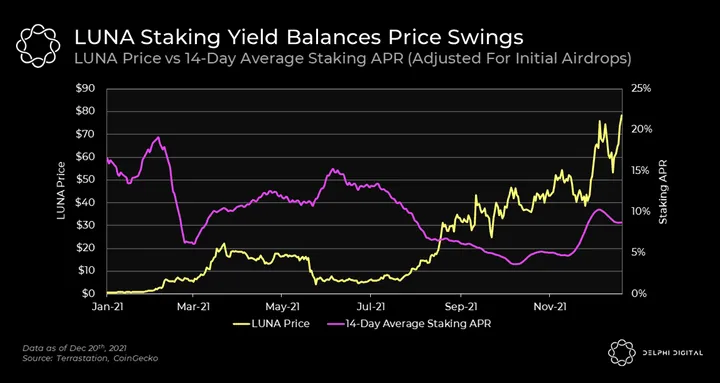

Where most staking rewards are paid out in the native token, and are thus reflexive, Terra staking rewards are paid out in UST. As a result, staking yields increase when the price of LUNA falls and decrease when the price of LUNA rises. These balancing forces allow LUNA burns to act as the collateralization mechanism for UST while simultaneously rewarding stakers for the risk they take. It’s worth noting that the mechanism is dual-sided: UST can also be burned for LUNA at any point.

You may be wondering how exactly UST holds its peg by having an equivalent burn-mint relationship with LUNA. Before we go any further, let’s briefly look at situations where UST is under and above $1 and how they’re rectified.

UST Expansion: If demand causes the market price of UST >$1, arbitrageurs can burn $1 of LUNA to mint 1 UST, which can then be sold at spot for a higher price than the peg, netting a riskless profit. Spot selling drives UST price back to its $1 peg, while minting expands UST supply. This process reduces the LUNA supply which is value-accretive to Luna holders.

UST Contraction: If demand causes the market price of UST <$1, arbitrageurs can buy UST at spot and redeem it at par value (i.e. $1) for newly minted Luna. Spot buying drives UST price back to its $1 peg, while redemptions contract the UST supply. This process increases the LUNA supply which is value-dilutive to LUNA holders.

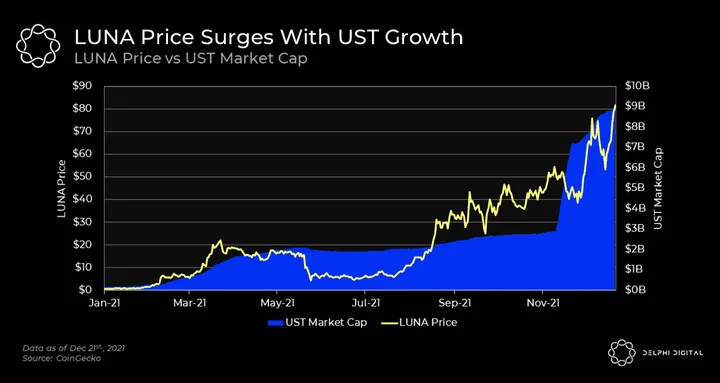

We’ve established that more UST volume and minting creates more value via fees for LUNA stakers. With UST’s tremendous growth in 2021, this has naturally resulted in more demand for LUNA.

Recently, roughly 80M LUNA (8% of total supply) that originally sat in the community fund was burned, causing a large spike in UST supply (as evident from the chart above). But where did this LUNA come from?

Before the recent Columbus-5 upgrade, when LUNA was burned for UST, it wasn’t all burned. A portion of LUNA used to mint UST was sent to a community fund to finance the development of the Terra ecosystem; a portion was rewarded to validators; and the remainder was burned. Since then, a change was made in Columbus-5 so every dollar worth of UST minted now equals one dollar worth of LUNA burned — permanently. From what we understand, potential uses of UST created from the burning of community-fund LUNA include facilitating UST arbitrage, covering adverse events, and community grants to aid UST’s multi-chain expansion [1].

After excess LUNA in the community fund was burned, we saw UST supply expand by roughly 2B tokens. This was mainly driven by recent cross-chain initiatives and upcoming project launches on Terra. Before this, however, the vast majority of UST and Terra’s growth came from payment applications like Chai and Memepay, as well as DeFi protocols like Mirror, Terraswap, and Anchor — which we’ll get into later in this report.

Projecting UST’s Growth

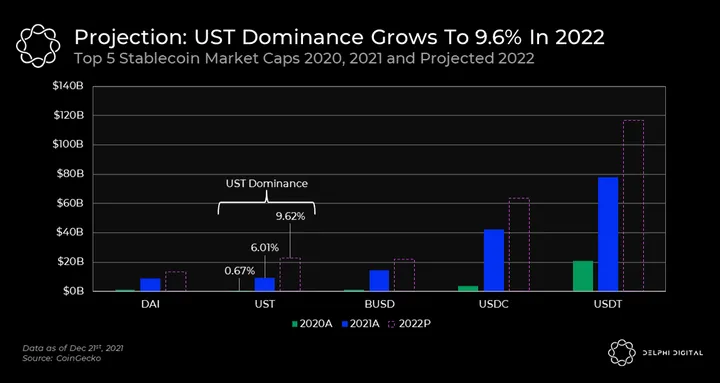

If we want to craft potential growth scenarios for UST, we can look at the top five stablecoins and how they’ve grown over the past two years. On aggregate, these stablecoins increased their market cap 5.6x from ~$27B at the end of 2020 to ~$153B today. Projecting out into 2022, if we believe there will be tightening regulation on stablecoins, we could see UST grow its market share further.

In the above chart, we estimate that USDT, USDC, BUSD, and DAI will grow their market caps by roughly 50% in 2022. This is conservative compared to their ~430% growth so far in 2021. UST market share grew from 0.67% to 6.01% in 2021, with its market cap growing an astounding ~4,900% over that time. At 150% estimated market cap growth for next year, this scenario would put UST supply at ~23B by EOY 2022. Meaning UST would need to increase by $13.8B over the next 12 months.

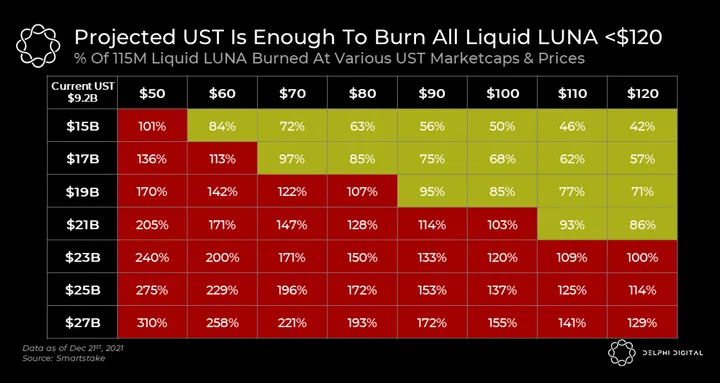

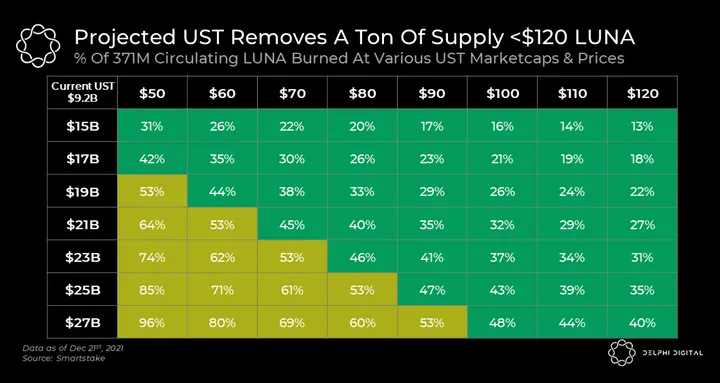

LUNA has a total supply of 833M — 371M of which are circulating and 115M of which are “liquid” (defined as circulating and not staked). The other ~462M Luna is held by Terraform Labs (TFL), the initial creators of Terra. This consists of a 150M stability reserve with the remaining coins held for discretionary use to pay staff and improve the resiliency of the Terra network.

After accounting for all coins, LUNA’s current “liquid supply” sits at ~$9.2B — significantly less than the projected $13.8B growth in UST’s market cap. Using a matrix of UST market cap and LUNA’s price, we can illustrate various supply expansion scenarios for UST.

The above sensitivity tables look at LUNA’s liquid supply and total circulating supply respectively. In reality, the burn would likely sit somewhere in between these two tables. This is because you have to consider a wide range of factors when calculating this, such as:

- The net amount of LUNA that will un-staked or be issued from the treasury.

- The amount of LUNA that is insensitive to price changes, held by those looking to keep their exposure and will not allow their coins to be used for burning.

- Effects of supply contraction and expansion. For example, between the expansionary period of Feb. to May. 2021, the network created ~$1.8B of UST at an average LUNA price of ~$13.5, equating to ~100M of LUNA burnt. And during the contractionary period in May. to Jun. 2021, ~$210M worth of UST was burned at an average of ~$6.5 per LUNA. This led to the re-minting of ~37M Luna. Effectively, a drawdown of just 10% in UST supply “undid” nearly 40% of the Luna burn. Note: this was before Columbus-5 so $1 worth of UST creation wasn’t directly $1 worth of LUNA burned.

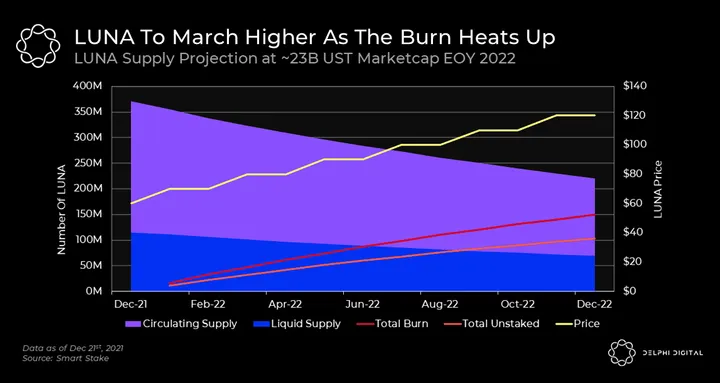

The creation of a decentralized asset reserve of over one billion dollars has been discussed, its sole function would be to help UST maintain its peg [2][3]. The creation of the reserve could help mitigate contractionary cycles by providing an underlying bid to UST. This should help make predictions easier, as it is impossible to foresee edge cases such as the scenario in May 2021. With all of these factors in mind, we estimate potential growth for LUNA and UST as we move through 2022.

This scenario assumes:

- UST will increase by an average of ~1.15B per month to hit the 23B target EOY 2022.

- LUNA’s price will step up in accordance to burning pressure with an increment of $10 every two months.

- The ratio between circulating supply and staked supply will remain constant at ~69%.

Per this model, ~150M LUNA would be burned over the course of 2022, which provides us with a middle ground between the two sensitivity analysis scenarios presented above. Yet, it is important to note that this is just one of many possible scenarios. It’s impossible to predict the real outcome. As we have seen above, increases in UST supply can provide LUNA with a serious bid in expansionary conditions, but this doesn’t come without a trade-off.

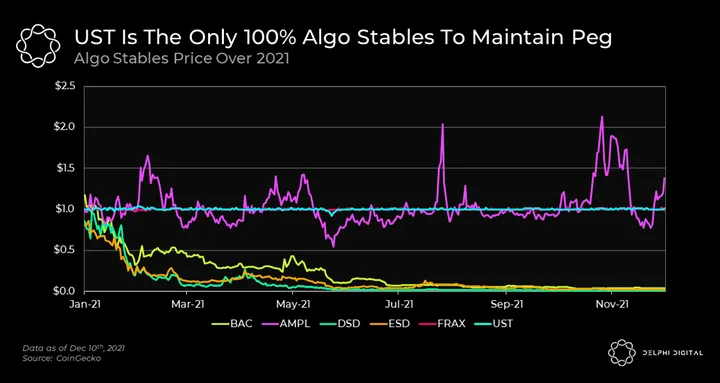

Risks To Algorithmic Stablecoins

Many projects in crypto have tried to build algorithmic stablecoins (often called algo-stablecoins), and almost all of them have failed to maintain their peg. Below are a few examples from 2021.

Note: FRAX is ~83% collateralized and 17% algorithmic.

Without delving into the specifics of how these algo-stablecoins function, the bottom line is that users held them purely speculatively. There was no long-term incentive for users to hold these algo-stablecoins — an incentive that would compensate them for the risk of low or zero collateralization. In times of volatility and uncertainty, this makes them vulnerable to a situation commonly known as “the death spiral”.

So how has UST broken this loop in times of stress and managed to keep its peg so well?

Firstly, a large portion of the UST user base is not holding it speculatively. Rather, they use UST for savings via Anchor, or asset exposure via Mirror; they use UST for everyday payments on Chai and Memepay. Terra’s decentralized finance ecosystem, dubbed “TeFi,” remains one of the only smart contract platforms whose TVL is mostly composed of decentralized assets.

Despite all this, UST is not fully insulated from crypto volatility. As we saw in May, liquidation events across crypto spilled over into Terra’s ecosystem. On May 23rd, UST lost its peg briefly, trading down to $0.92. This was caused by a market-wide drawdown, as well as extensive liquidations on Terra’s Anchor Protocol. Since then there have been improvements to the liquidation engine on Anchor, but there are other initiatives in the works. These include a reputation layer being built on top of Terra to reduce its reflexivity, which we dig into later, and the potential decentralized reserve that will assist LUNA in absorbing shocks to UST demand.

It is important to note that algorithmic stable coins are risky and it’s possible for the peg to the dollar to break. While UST has done a great job thus far of maintaining its peg, it’s not guaranteed to do this in the future.

Bootstrapping Utility for UST

As mentioned above, creating demand for UST fuels Terra’s growth; increasing UST’s utility and supply has a direct impact on LUNA’s price. With a higher market cap, LUNA is able to absorb UST supply shocks much better. But a rising LUNA price also has reflexive implications. Take the example of incentivized pairs on DEXes. When a new token/pool launches, new LPs push up metrics like TVL. And as there is now a yield on the base pool asset, the price of the base asset increases as speculators buy it to provide liquidity. This creates a positive feedback loop as new capital enters the ecosystem.

Terra supercharges this, as every marginal dollar entering is in the form of native tokens or UST. This causes either buying pressure for the native token or contributes to LUNA burns. An analogy for this would be if every time USDT, USDC, or BUSD was created on ETH, an equivalent amount of ETH was burned. While EIP-1559 introduced ETH burns at a transactional level, on a per dollar basis, it’s at a much smaller scale than Terra.

Reflexivity to the upside is always a sight to behold. However, it’s important that Terra balances these reflexive relationships because they can occur to the detriment of the network too.

When demand for UST shrinks, LUNA is minted (UST is burned) and UST is at risk of entering the death spiral. With respect to the reserve fund to defend UST’s peg, if done right, this can then help prevent contractionary cycles from getting out of control. More importantly, this reflexivity can also be dampened by on-boarding users of UST for non-speculative reasons — which is Terra’s main objective. If UST is usable across a myriad of applications — real world and on-chain — users will naturally hold it for its utility.

In the following section, we examine the current use cases for UST that help drive natural demand.

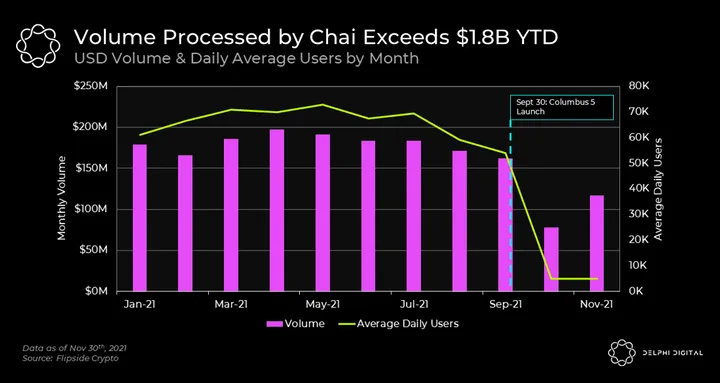

Payments on Terra

Note: The drop in USD volume and daily average users from October is due to changes in data indexing, and is currently being rectified. We suggest looking at the Jan. – Sept. data for a more accurate representation.

The first real world use case for Terra was Chai, a mobile payments app in South Korea. Chai uses Terra’s network and stablecoins to settle fiat payments with merchants at a fraction of the cost they would otherwise incur via traditional financial institutions. Since the inception of the partnership in 2019 until now, Chai’s user base has grown to approximately 40-50K daily active users. From the beginning of 2021 to the end of November, Chai has processed over $1.8B in payments, with over 70M individual transactions.

In 2019, Terra announced the launch of MemePay in Mongolia. MemePay is an e-wallet enabling instant stablecoin and P2P payments between friends. MemePay has attracted tens of thousands of users, partnering with the likes of taxi drivers and department stores to allow users to pay for goods & services using cryptocurrencies.

The success of Chai and MemePay are notable because Terra has managed to “close the loop” with the real world. Chai users don’t need to be crypto natives to benefit from efficiency gains since complexities are abstracted in the backend. Chai and Memepay users can confidently hold Terra stablecoins because they can spend their money on real goods and services.

Eventually, these applications will be able to interact with more of the “TeFi” ecosystem. And this is where it gets juicy.

The Rise of TeFi

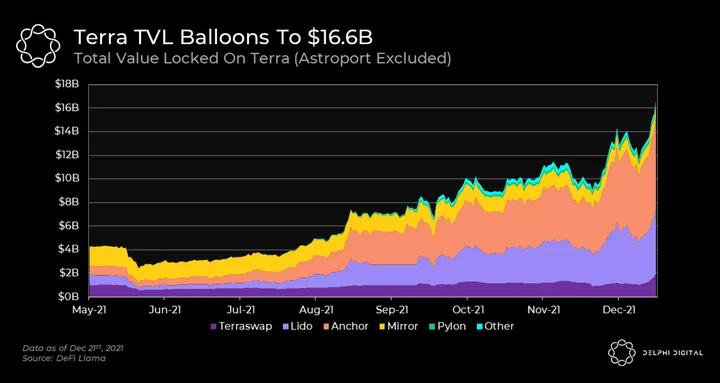

Beyond payments, Terra has grown by leaps and bounds over 2021. Overall TVL has grown to ~$16.6B, cementing Terra as the second-largest L1 ecosystem behind Ethereum according to DeFi Llama. Mirror, Terraswap and Anchor are the three stalwarts of the Terra ecosystem thus far, and currently make up the bulk of Terra’s TVL.

Note: DeFi Llama double counts some amount of TVL for base layer protocols. For instance, Lido and Anchor on Terra have partially overlapping TVL. We excluded Astroport from the above graphic for this reason, as it overlaps with Terraswap.

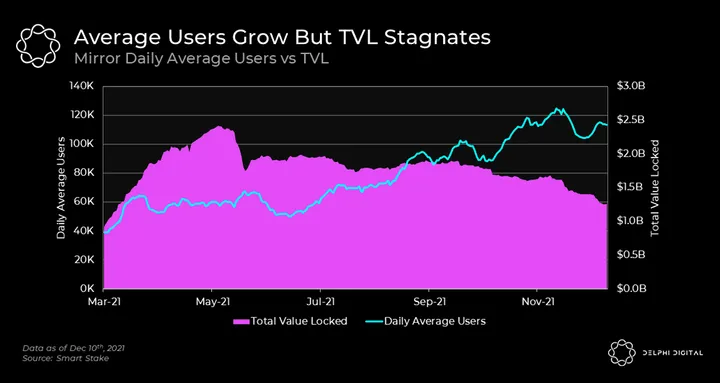

Mirror Finance is a synthetic asset product, offering on-chain exposure to any asset with a reliable oracle (price feed). These mirrored assets are called “mAssets”, the most notable of which are mApple, mAirBNB, and mAmazon. To mint these synthetics, a user has to “borrow” them in an over-collateralized manner (explained in the introductory section of this report). The base threshold to mint a position is 150% collateralization against UST, LUNA, or other mAssets. Mirror’s unique appeal to users is cheap and global access to equities at virtually any position size.

Since the most popular mAssets are a function of equities demand, this provides Terra with a less volatile, uncorrelated source of capital inflows and activity. In terms of protocol growth, Mirror’s TVL has been on the decline since mid-2021, but the number of daily users is on an upward trend. Which implies increased participation from users with small trade sizes and a decrease in whales.

Catalysts that may reignite TVL growth are the launch of new protocols that leverage Mirror’s infrastructure. Two such protocols are Nebula and Spar. Nebula offers clusters that will allow users to buy baskets of mAssets, and Spar is attempting to democratize crypto management.

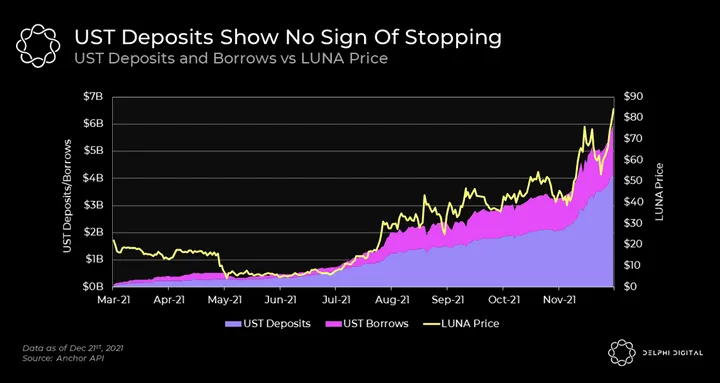

Anchor is a protocol on Terra that lets people borrow UST against staked L1 assets. For lenders, it’s a savings protocol to deposit UST and earn Anchor’s unique stable interest rate of 18-20% — called the “Anchor rate”. The high savings rate is generated through liquid staking yields and interest charged to borrowers. Similar to Mirror, there are a slew of protocols building on top of Anchor. Some examples include Pylon, Orion, Angel Protocol, and Suberra.

A point often overlooked is that Anchor is a counter-cyclical supply sink for UST. Anchor provides attractive and stable returns, helping source UST demand during market downturns as users risk-off into stablecoins. As seen in the graph above, when the price of LUNA dropped by over 80% in May, UST deposits continued to increase.

It should be noted that borrowers are currently incentivized by ANC emissions that will disappear in a few years. Furthermore, any decrease in borrowing directly puts pressure on Anchor’s yield reserve, which is used to pay UST depositors when the sum of staking yields and borrower interest falls below the Anchor rate.

The Anchor community has proposed several ways to avoid draining the yield reserve — which is what happened in July 2021 when borrowing demand dropped significantly. Firstly, an injection of $70M UST was provided to give Anchor runway to add more collateral, as it currently supports only LUNA and ETH. With more collateral options and staking yields, the reserve will be able to continuously grow. Second, there’s an ongoing discussion around deploying a portion of the yield reserve’s idle UST into upcoming money markets launching on Terra, making the yield reserve productive.

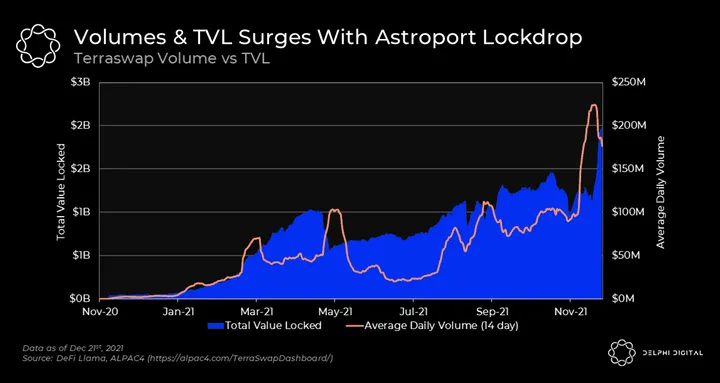

The last and oldest of the three is Terraswap — Terra’s leading AMM using a Uniswap v2 inspired model. Traders are charged a 0.30% fee paid entirely to LPs. Terraswap has been a core piece of infrastructure for Terra, averaging over $170M of daily volume in the past 30 days. That being said, Terraswap only supports standard XYK (50/50) pools and is outdated amidst the current AMM landscape.

A Unique Opportunity For NFTs and Gaming

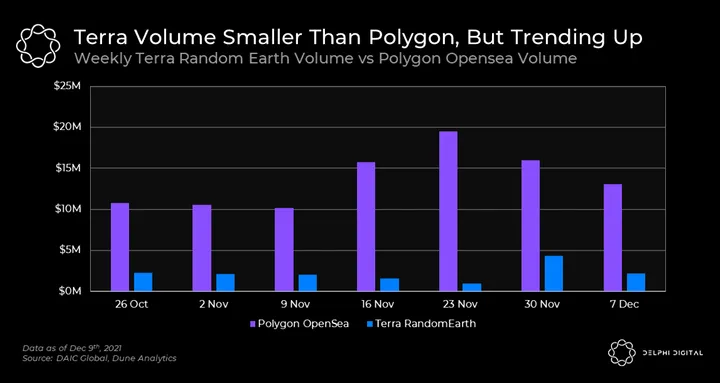

Terra’s NFT ecosystem has been evolving with the launch of its first NFT marketplace, Random Earth. At the time of writing, there are 51 active NFT collections listed, with an average of ~$300K in daily trading volume (16% of volume on Polygon’s Opensea) and ~2K daily users (25% of users on Polygon’s Opensea).

Another aspect of the ecosystem that’s being developed is Terra’s gaming sector. Do Kwon recently announced that top-tier Korean gaming companies were flocking to Terra. One such company is Gamevil Com2uS, a South Korean game developer. The company is building blockchain games and NFT marketplaces on Terra, which are set to launch next year.

Despite being less scalable than alternative solutions like Solana and Ethereum’s L2 rollups, Terra’s has certain characteristics that make it appealing to gaming companies:

- It has cultural and geographical proximity to South Korea, where there are many MMO RPG gaming companies. South Korea has the 5th largest gaming market in the world by revenue at $1.2B.

- Terra’s native stablecoins and fiat payment ramps enable globally settled payments, allowing for open-economy games with frictionless settlement.

Needless to say, the future of gaming on Terra looks bright.

Catalysts: New Primitives Coming to Terra

Terra has dozens of projects set to launch over the next year. Let’s take a look at the breadth of projects coming to Terra.

Astroport: Astroport can be thought of as a mix between Uniswap v2, Curve v1, and Balancer. It will provide standard XYK AMM pools, stableswap pools for pegged assets, and Liquidity Bootstrapping Pools (LBP) for token launches.

Mars: Mars provides lending and borrowing services offered like most DeFi money markets, but with some newly added features. The core innovations of Mars’ money markets are:

- Smart Contract Lending: Mars will extend credit lines to smart contracts, allowing for un-collateralized lending and leveraged yield farming.

- Dynamic Interest Rate Model: Unlike the usually kinked utilization curve, Mars uses a dynamic interest rate model that uses control theory and a PID (Proportion, Integral, Derivative) controller. The model targets an optimal utilization rate and interest rates shift every block to target this level. This allows borrowing and lending rates to be reactive to market conditions, thus improving capital efficiency.

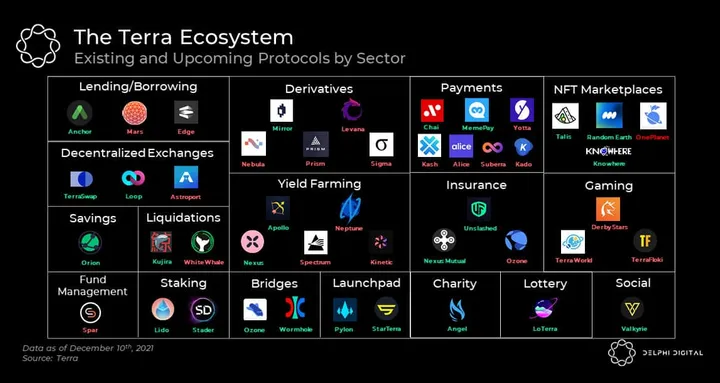

The Terra ecosystem is now at an inflection point with core money legos being built out. We’ve categorized some of the protocols that are active on Terra (text in green) as well as the more significant projects that will launch on Terra soon (text in red). What was a chain with 3 applications (Mirror, Anchor, Terraswap) at the beginning of 2021 has now evolved into a vibrant and multi-faceted ecosystem.

Beyond money legos, a reputation layer is key for building DeFi’s next primitives. The Lunatic Score, launched by Flipside Crypto, leverages on-chain data to give users a rating measuring their participation in the ecosystem. This is a slightly differentiated take on the popular “Degen Score” that exists on Ethereum, which solely focuses on speculation.

Building data sets like this is the first step in establishing an on-chain reputation layer. In the near term, this can be used to reward loyal users and reduce reflexivity. And in the long term, tackle more complex issues. A few examples of things that a native reputation layer enable includes (but is not limited to):

- Giving priority status to bid on Anchor liquidations to users with a historically low propensity to sell. This would reward users who are looking to buy cheap bLUNA to hold rather than opportunistic arbitrageurs. A feature like this would dampen the cascading effects of liquidations on Anchor.

- Future projects curating their airdrops based on users who have held their previous airdrops, staked them, and/or voted in governance.

The Future of Terra

A unique characteristic of LUNA is that its price performance isn’t solely predicated on the success of the Terra ecosystem. As long as UST is being widely adopted, whether on Terra or on other L1s, LUNA holders stand to benefit.

As described by Do Kwon, there are three components needed in order for UST to be adopted in other ecosystems: a seamless bridging experience, deep UST liquidity on key DeFi platforms, native dApps that leverage UST.

On the first point, the Terra community is dedicating a lot of resources to investing in and building a robust set of bridges, including Shuttle, Wormhole, IBC, and LayerZero. IBC, in particular, is a massive opportunity for Terra. The Cosmos ecosystem is nascent, but gaining significant traction on Hubs like Osmosis. Cosmos, however, lacks a native stablecoin — and UST could very well be that stablecoin.

In terms of deepening liquidity on other chains, there have been a number of UST liquidity mining incentives on Solana dApps like Saber and Mercurial. On Ethereum, MIM-UST and UST-3CRV pools are within the top four Curve pools by daily volume. Recently, three governance proposals (that can be found here) were proposed to enhance UST liquidity on Ethereum through novel mechanisms. Terra deploying its treasury in a strategic fashion can create deep UST liquidity across the top ecosystems, and is essential for its adoption as a top stablecoin.

And finally, products like Abracadabra have embraced Terra so UST can be posted as collateral to mint MIM on Ethereum. These efforts so far have attracted over $1B worth of UST. Projects such as Olympus DAO have a governance proposal to integrate with UST by adding it to its treasury via reserve bonds. And this is probably not the last we’ll hear of projects on other chains looking to tap into UST. Especially if the supply estimates from earlier in this report come to fruition.

We believe that LUNA’s value proposition will strengthen as more use cases for UST are built out on-chain and in the real world. USTs growth strategy is two-pronged: exporting itself as the most decentralized and useful stablecoin across all L1s, and building out a decentralized financial hub on its native Terra chain. UST and TeFi offer some of the most decentralized and scalable solutions available today. Only time will tell how much the market values this.

[1] Do Kwon’s Twitter Account @stablekown – https://twitter.com/stablekwon/status/1462063960845291530?s=20

[2] Do Kwon’s Twitter Account @stablekwon – https://twitter.com/stablekwon/status/1462063962506338318?s=20

[3] Burning Man On Mars Live Podcast – https://www.youtube.com/watch?v=WEWCigLmZfA

0 Comments