Report Summary

- Markets as Intelligence Systems: The report compares markets to AI systems, suggesting they are general intelligence-like mechanisms that process vast amounts of human behavior and data to provide real-time insights and predictions. The report argues that markets reflect collective human knowledge and decisions, much like AI models like GPT-4, but are underutilized for their broader potential.

- Comparison with AI: While AI models like GPT are praised for their problem-solving capabilities and knowledge retrieval, markets are often seen as mere tools for pricing assets. The report advocates for a deeper engagement with markets, suggesting that they could be employed for decision-making in areas beyond asset pricing.

- Prediction Markets and Futarchy: The report introduces prediction markets as a tool that could be leveraged to ask broader societal questions, providing answers based on collective human insights. It discusses the concept of “futarchy,” where decisions could be made by markets rather than politicians or voters. This would allow markets to act on predictions and influence outcomes, creating more efficient decision-making processes.

- Crypto and Free Markets: The report highlights the role of cryptocurrency as an experiment in free markets, moving from money to internet-based and now social infrastructure systems. It points to the rise of platforms like Polymarket, which utilizes prediction markets to predict political and economic events.

- Challenges of Prediction Markets: Liquidity, oracles, and opportunity costs are identified as the key challenges facing prediction markets. Illiquidity hinders their efficiency, oracles (the systems that verify outcomes in these markets) can be prone to technical disputes, and opportunity costs arise from the zero-sum nature of prediction markets.

- Manipulation and Efficiency: The report delves into how manipulation in illiquid markets can lead to inefficiencies but also demonstrates that such manipulation often fails due to the corrective nature of market dynamics. It uses the example of failed market manipulation in the 2024 U.S. Presidential election prediction market to illustrate how markets self-correct over time.

- Future of Decision Markets: Futarchy is positioned as a transformative concept where markets could be used to make critical decisions, making governance more efficient. Platforms like MetaDAO are mentioned as early pioneers, showing how decision-making could shift from voting to market-driven outcomes.

Imagine a machine that lives high up in the sky. The machine has preternatural ability. It can see the future — wars, weather, and presidents. Its intelligence is ooms greater than any living being. And its power so awesome it’s sometimes seen as a sort of oracle or magic genie. You might be picturing the GPT-5 cluster, but that’s not it. The machine I’m talking about is the market.

The market is the synthesis of every human action. It prices in the day you take your first and last breath, what you eat in between, and even how often you sh!t. We can’t escape it. Every day, 8.2 billion people wake up and live within it. Some buy diapers, others invent vaccines, and a special few buy and sell cryptocurrencies. But all of us feed the market. It ingests our reality, analyzes it, and reflects the updated state of the world.

The market can be thought of as a form of general intelligence. And although there are key differences, the similarities between markets and AI models like GPT-4 are striking. Both train on vast amounts of human-generated data, both compress incredible sums of knowledge, and both implicitly mirror our world back to us.

But despite their similarities, humans use AI and markets quite differently. With AI, we have sci-fi-like expectations. Many talk breathlessly about the day it will take our jobs and bring forth utopia. But when it comes to markets, our views are more muted. We don’t expect them to do much other than price assets. And we certainly don’t expect them to replace our jobs or institutions. This is weird. If markets are a form of general intelligence, why don’t we ask them to do more?

When are people going to realize that capitalism is already absolutely nothing short of an advanced artificial general intelligence? I think it’s one of those stylized empirical facts that is too large to do anything with, so it becomes like a secret.

— Justin Murphy (@jmrphy) December 13, 2020

Our shallow relationship with markets is even more perplexing when you consider how quickly we’ve adopted SOTA AI models like GPT and Claude. These technologies are only a few years old and already more widely applied than markets, which have existed for millennia. Perhaps markets can learn something by looking at where AI has found initial PMF.

Today’s AI models are primitive yet powerful. They memorized the Internet but struggle to count the r’s in “strawberry.” But despite these limitations, they can do incredible things. And we take full advantage by putting them to work across society. There are many compelling use cases, but at the highest level, we can group them into two big buckets:

- answers

- actions

ChatGPT is popular because it’s an answer machine. You ask the model a question — any question — and you get an answer. The models know all sorts of useful information, so we often look to them for knowledge. Who won the US Open? When is Election Day? How long is this damn report? AI has essentially replaced Search and entire swaths of the Internet. But its impact has been surprisingly limited.

Imagine telling someone a century ago “we have a system that correctly translates things 99% of the time, informal speak and tone and slang and all, usable for free, all the time, and it didn’t really change anything”

— Jason Phang (@zhansheng) June 17, 2024

The problem is that AI is passive. And we need agentic AI before we can start climbing the Kardashev scale. Today’s models can take some action, but only in limited ways. For instance, Claude has proven popular with developers because it’s adept with code. You can ask it to do all kinds of stuff — generate code, build a website, write documentation, etc. This moves AI beyond the friendly chatbot paradigm to something closer to an agent.

Ok mind == blown

This afternoon I managed to build a complete exchange UI in @nextjs with practically zero frontend experience using a combo of @cursor_ai + claude + @v0. It even supports @solana wallets out of the box + fetches rpc data via our own SDK.

It’s so over for devs. pic.twitter.com/2nuc9PW4Kg

— Tristan (@Tristan0x) September 1, 2024

Our relationship with markets is far more primitive. We ask them few questions and give them no ability to let them take action. Instead, we tend to view markets as fickle slot machines and often base our opinion of them on the answers they give us.

The rules of CT are pretty simple

If the token goes up, it gets threaded, thought-pieced, philosophized, twitter-spaced, celebrated, vc-funded, future-of-all-x

If the token goes down, it’s a scam, a rug, dead, inversebrah’d, ratioed, canceled, and everyone must go to jail

— vibhu (@vibhu) May 31, 2024

There are many possible explanations for why we’re dramatically underutilizing markets. But the most obvious is we lack the tools to use markets in a more generalized way. Err, at least we used to lack the tools.

Prediction markets and futarchy are two new tools that leverage the general intelligence of markets. They let us pose questions, extract answers, and give markets agentic power. It took ChatGPT to reveal the power of AI, and it will take these tools to do the same for markets. The entire crypto movement is an experiment in free markets. First, it was money, then the Internet, and now society itself. A golden age of markets lies ahead.

Truth Machines

If ChatGPT is an answer machine, then Polymarket is a truth machine. ChatGPT compresses the Internet to give us answers, while Polymarket does the same with markets. The only difference between the two is trust. AI is an alien life form made of silicon, not flesh. All we can do is trust that the high priests at OpenAI solve alignment and keep our best interests in mind. But markets are different — they are made up of human beings. They are us. There’s no need for alignment when it comes to markets. At any given time, they already reflect consensus across all humans — a living, breathing truth, if you will.

This lofty concept of truth is the biggest reason prediction markets have exploded in popularity. People trust these markets more than other information sources. Don’t get me wrong, markets are imperfect. After all, they are made up of a bunch of flawed humans. So, perhaps the “truth machine” framing oversells things a bit. But it’s kinda catchy, so we’ll rock with it. A more accurate moniker might be information discovery machines. But when you really think about it, “information discovery” is our best attempt at finding truth.

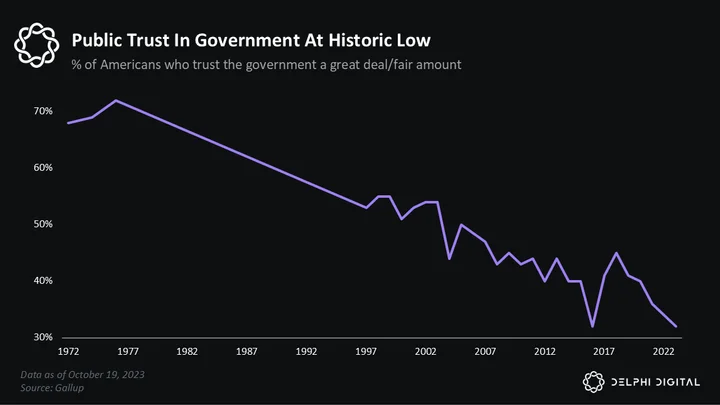

It’s not like markets have a whole lotta competition in the truth department. For decades, public trust in institutions has been downonly. And it’s not just the media; almost every institution you can think of — the church, government, and even the scientific community — is staring down record-low levels of trust.

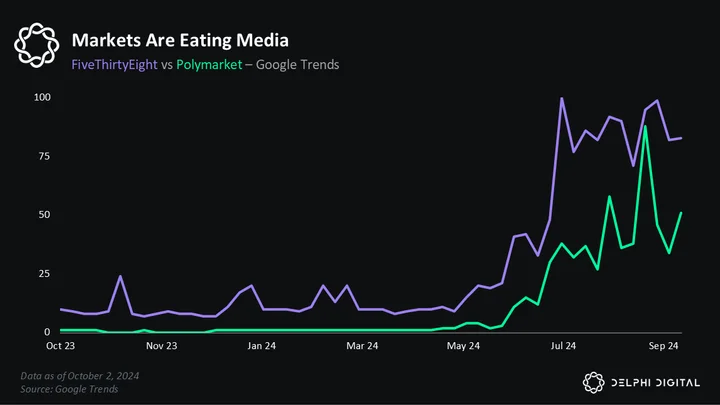

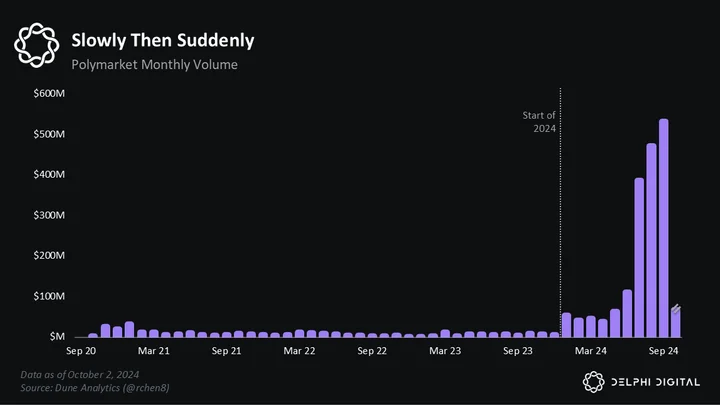

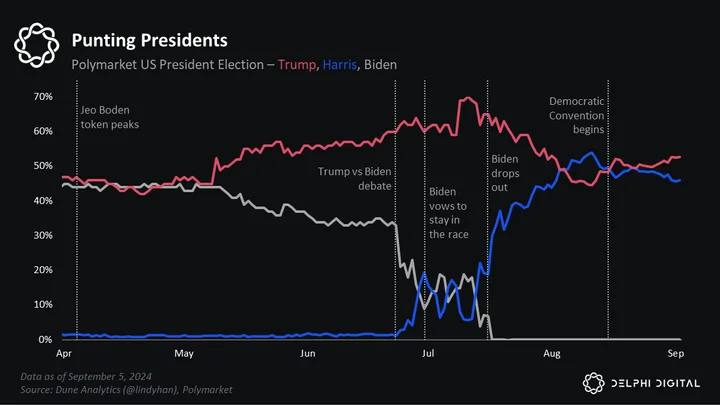

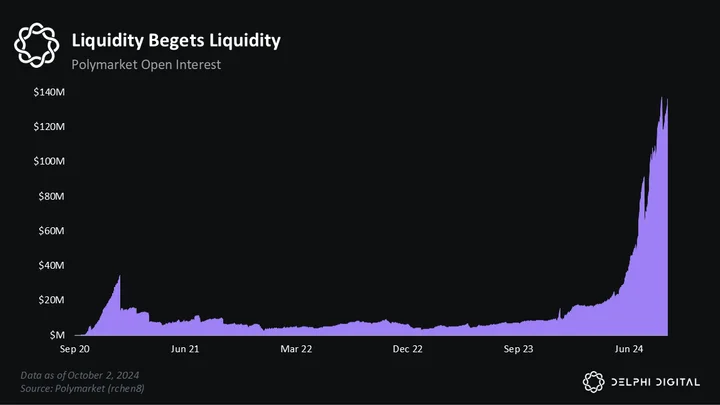

After a decade of VC threads, Vitalik blog posts, and Reddit-coded obscurity, prediction markets finally burst into the public consciousness this year thanks to the Presidential Election. The attention the election is generating has meant big business for Polymarket. You can literally see when its “Presidential Election Winner” market went live.

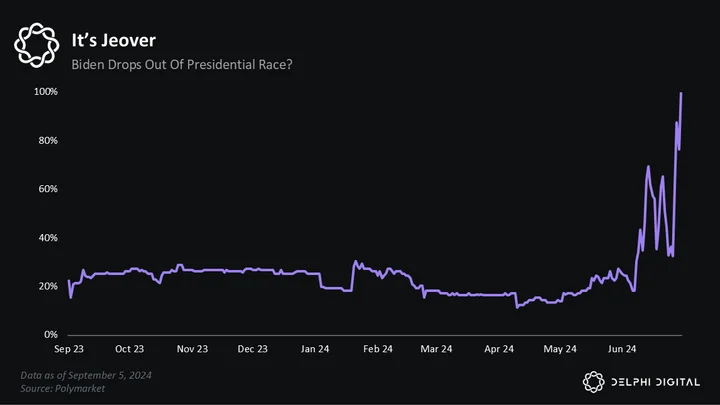

2024 will be remembered as the first time prediction markets played a significant role in an election. From the jump, markets were early, contrarian, and right. Polymarket spun up a market on whether Biden would drop out on Sept. 21, 2023 — over one year ago, today. Even back then, traders were pricing in a 22% chance he would drop out — much higher than the conventional wisdom inside the Beltway and roughly 3x the odds that Trump would drop out.

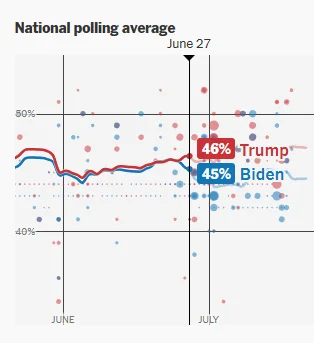

The Biden market wasn’t the only one that was proven right. The premier Presidential Election Winner — the most liquid prediction market in the world — was also prescient. The real action started in May. The race was tight, and most polls gave Trump a slight edge. But in May, Biden’s odds began to roll over. At the time, this puzzled outside observers. Nothing had happened. The polls and the intelligentsia were all saying the race was still close. But the markets were flashing red for President Boden.

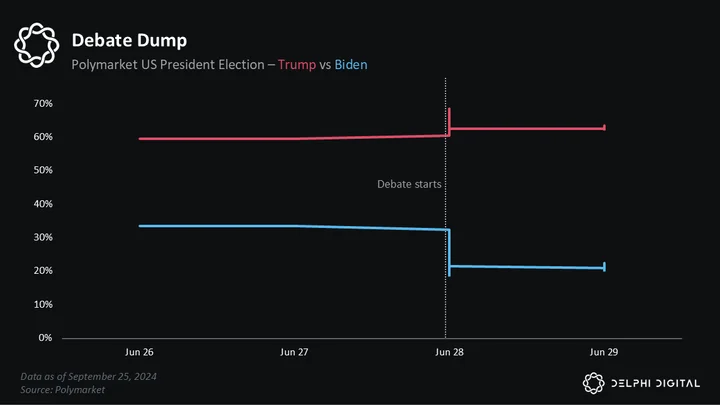

As summer dragged on, Biden’s Polymarket odds began to tumble. Traders were straight up ignoring polls that showed an unchanged race. By the time the Trump-Biden debate rolled around on June 27th, markets were pricing Biden’s odds at 33%, while the polls had him at 45%, or about even with Trump.

We all remember how that debate went down. When it started, Biden’s odds of winning the Presidency were chilling around 33%. But by the time everyone woke up the next morning, his odds had nuked to 20%. A few days later, they found a temporary bottom at 9%.

Now that some time has passed, we might be tempted to gloss over these numbers as just another statistic. But it’s worth lingering for a second on their significance. After all, this is Jeo Boden we’re talking about — President of the USA! At the time, he was the unanimous Democratic nominee. Yet Polymarket gave him a measly 9% chance of winning! Talk about speaking truth to power…

In the days after the debate, the Biden campaign played damage control. There was a coordinated effort from the White House and other top Democratic officials to meme “Biden isn’t dropping out” psyops all over the airwaves. And at the time, it was pretty effective. It really felt like Biden was ready to go down with the ship for a hot second. At least, that’s what Congress believed.

This effort ultimately culminated in a tweet from Boden himself, err, a top aide, doubling down on staying in the race.

Let me say this as clearly as I can:

I’m the sitting President of the United States.

I’m the nominee of the Democratic party.

I’m staying in the race.

— Joe Biden (@JoeBiden) July 5, 2024

Yet the markets were unphased. Polymarket stared down the onslaught of pro-Biden headlines and still priced in 66% odds that he would drop out. To state the obvious, this was a big F-ing deal. Here was a magic Internet money website that most normal people had never heard of openly defying the word of a sitting President. Of course, the press ate it up and ran with the story, amplifying the narrative that Polymarket had birthed and heaping further pressure onto President Biden.

By the time Biden stepped down on July 21, 2024, the markets were already pricing Kamala Harris’s chances of winning the presidency at nearly 3x higher than Biden’s. From start to end of the whole Biden saga, Polymarket was early, contrarian, and right. The market gods could not have scripted a better coming-out story for prediction markets.

Market Minutia

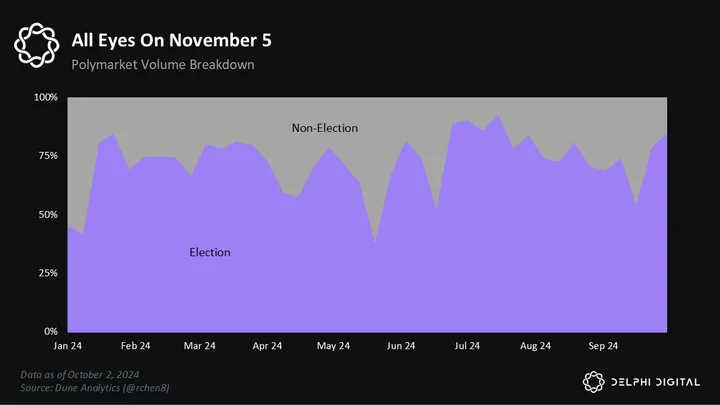

Now that we’ve done some proper prediction market bullposting, it’s time to steelman the bear case and discuss flaws in the current model. But first, let’s address the elephant in the room. What will happen after the election? This year, a whopping 78% of Polymarket volume has been election-related.

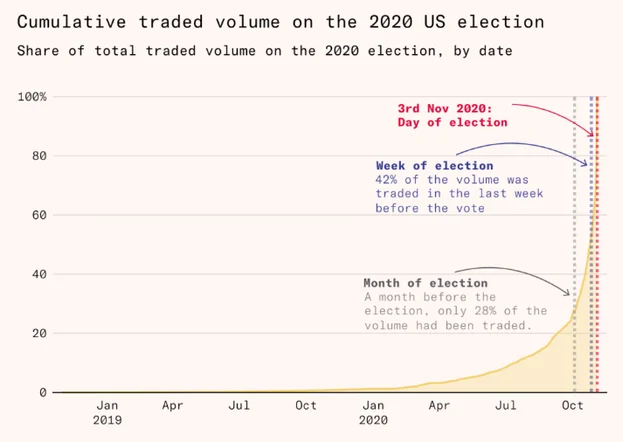

It doesn’t take a genius to figure out that Polymarket activity will probably fade after November 5. Duh. But that doesn’t mean things won’t get even crazier first. It probably will. In 2020, over 40% of all election-related volume was traded in the last week before the vote. Attention on these markets will go up before it goes down — especially if Polymarket drops a token as rumors suggest it might.

The more fundamental challenges prediction markets face boil down to three thangs:

- liquidity

- oracles

- opportunity cost

Liquidity is by far the biggest issue. When markets are illiquid, they are inefficient, which then calls into question whether they are indeed a source of truth. The more liquid a market is, the more efficient and ‘truthful’ it becomes. Liquidity can be a somewhat abstract concept, so let’s walk thru a few examples.

While I enjoy Polymarket, those referring to it as the “source of truth” are mistaken. I make a few dozen markets, and the truth is that top of book liquidity is highly incentivized, and election markets function due to cross-exchange arbitrage.

Until open interest is a few…

— Noah (@TraderNoah) July 21, 2024

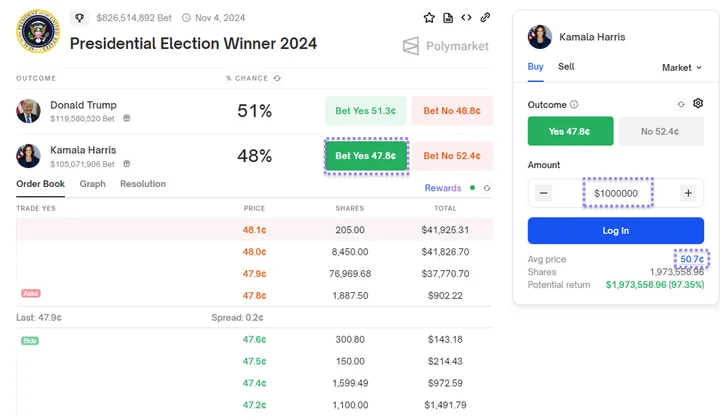

Let’s say, for argument’s sake, you’re bullish on Kamala Harris. Maybe you like her unrealized capital gains tax, or perhaps you think crypto users are just biased toward Trump and systematically underestimate her odds of winning.

how it started vs. how it’s going pic.twitter.com/3GoHvgitM9

— Proph3t (@metaproph3t) August 12, 2024

Either way, you check Polymarket and see this:

You immediately spot a mispricing. You think Kamala’s true odds are 50%, not 48%. This looks like free money, so you want to size in and capture it. The only problem is there’s no way to put on a large trade — say, a $1M position to earn ~$41,000 if you’re right about the 48% to 50% move. Buying $1M shares of ‘Yes Kamala’ would blow out your average price per share to 50.7%, and you would actually lose money if the market repriced to 50%.

This is a liquidity problem. A more liquid market would let you place a $1 million bet on Kamala at 48% and exit at 50% with trivial slippage to earn a 4% return. Admittedly, the million-dollar threshold is somewhat arbitrary, but it’s a decent proxy for the efficiency of these markets. Until large size can enter and exit with minimal slippage, these markets will struggle to efficiently price small moves in either direction.

As Felipe from Theia Research writes:

Traditional markets can debate 20bps moves in interest rates because they have sufficient liquidity and leverage for a whole ecosystem of analysts to earn high returns by being right about small moves. Polymarket can debate ~20% moves in election odds and maybe even ~10% moves but it is not efficient enough to give you information at the <5% level.

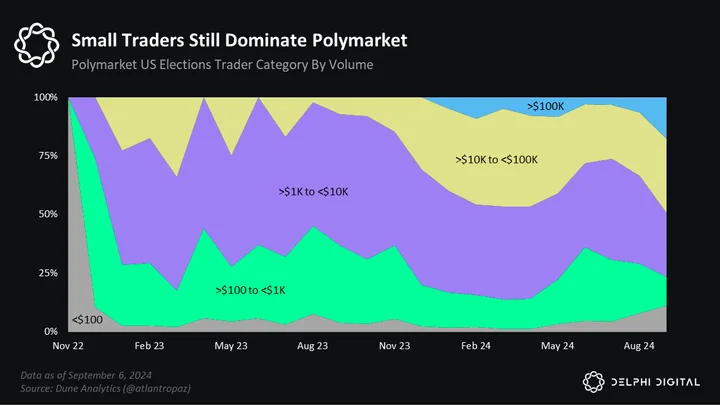

Why should we care if some random whale suffers slippage on a million-dollar trade? The core problem is that illiquid markets = inefficient markets. It’s not that we care about the whale, per se; we just care that markets are efficient and reflect the truth. Inefficiencies are created when traders — yes, even whales — cannot express their opinions. This is why Polymarket remains largely retail-driven — whales can’t swim in shallow pools of water.

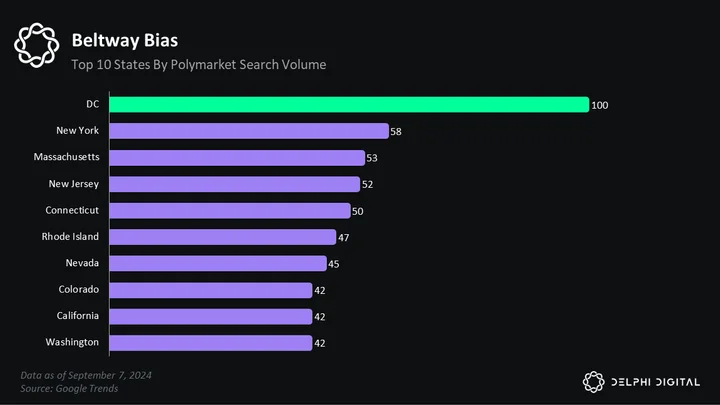

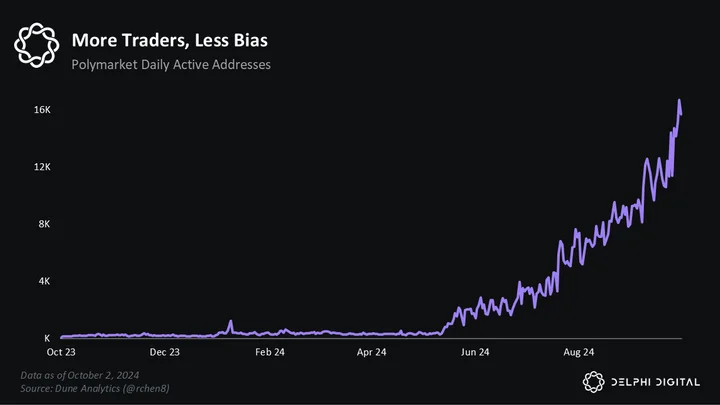

Illiquidity also exposes prediction markets to other, more subtle forms of inefficiency. One example is bias. Polymarket has ~10,000 daily active traders betting on US elections, and these people tend to cluster in D.C. and New York City. This means many Polymarket users follow the same Twitter accounts, consume similar information, and share the same beliefs. In other words, their biases are correlated.

Then there’s the concentration issue, as 20 traders account for something like 95% of Polymarket’s volume. To be clear, there’s no magic number when markets suddenly become ~efficient~, but it’s much higher than 10K daily users and 20 power users. The only way to solve bias is through scale — more users, volume, and liquidity.

Another problem that lies downstream of market illiquidity is hedging. In illiquid markets, hedging distorts the true value of predictions because the hedgers are not motivated by profit but by protection.

Say you hold ETH and are long-term bullish but worried about short-term volatility. You want to protect your ETH bag while benefiting if ETH goes up. A decent hedge could have been the “Will Ethereum dip below $2,000 by September 30, 2024” market. It let you shares in the “Yes” position and bet that ETH will fall below $2,000.

In this case, you’re entering the Polymarket position as a means of protection, not profit. So, whether you enter at 43% or 44% odds doesn’t really matter to you. It might sound like nit-picking, but at a market microstructure level, you are an insensitive buyer distorting the market. The way to fix the hedging problem is the same bias — moar liquidity!

Another form of market inefficiency comes from straight-up manipulation. This is similar to hedging, as manipulators act irrationally when viewed in isolation. They aren’t trying to make money on individual buys or sells; they’re just trying to move the price enough to profit on some other market. In more liquid markets, like FANG stonks or government bonds, manipulation is tricky; you need a lot of capital to move prices. But it’s much easier with prediction markets. We saw an interesting example of manipulation on Polymarket a few weeks ago.

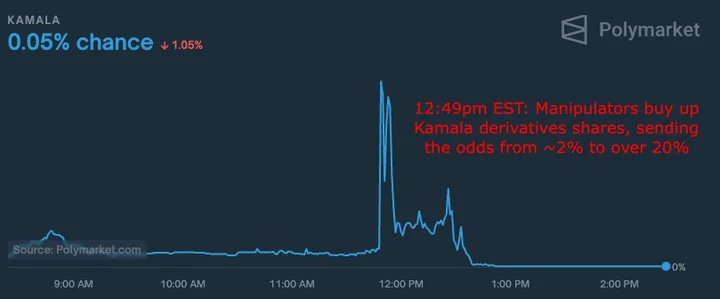

On September 6, a group of Polymarket whales tried manipulating the Presidential Winner market to profit from a derivative market called “Favorite to win on Polymarket on Friday.” The second market, far less liquid than the first, was based on the leader of the Presidential Election Winner market on Sept 6, using the one-minute odds data between 12pm and 3pm EST. The attackers spent ~$9 million buying Kamala YES, Trump NO, and cheap Kamala derivative shares. They planned to profit from the derivative shares by manipulating the Presidential Winner market between 12-3pm EST.

The manipulators were able to move the market temporarily but ultimately failed to hold Kamala’s odds above Trump’s for a long enough period to profit during the 12-3pm window. These traders lost over $60K in the derivative market and are down another six figures at current prices in the Presidential Election Winner market.

The attack failed because markets are hard to manipulate. Unlike most other systems, markets impose a real-time cost on attackers. If a manipulator wants to force a particular outcome, they are forced to buy shares from the minority at a premium. Manipulators are noise traders who trade on something other than alpha, which leaves them vulnerable to traders who do trade on alpha.

Like a bleeding whale in open water, noise traders attract sharks who eat them alive and profit off their remains. In the case above, the sharks didn’t need to have an opinion on whether Trump or Kamala would win. All they had to do was recognize the presence of noise traders and take the other side of the trade. This is why markets are so powerful. They reward those who seek the truth and punish those who do not.

The failed manipulation also highlights the strengths and weaknesses of prediction markets. On one hand, they remain illiquid and open to potential manipulation. After all, it only took $9M to move the price of the most important prediction market in the world. On the other hand, it shows that these markets are resistant to manipulation, even with low liquidity. The greater the manipulation, the greater the incentive to correct it. The final lesson we can draw here is the power of eyeballs. The only reason this manipulation failed is because a lot of people were watching the Presidential Winner market and immediately alerted the broader market.

Someone just came in big to poly against Trump Yes. Was Trump+8 just a little while ago. Woof. pic.twitter.com/yKuEp2x5ey

— Scott Johnsson (@SGJohnsson) September 6, 2024

If no one had noticed the manipulation, it likely would have succeeded. So, while attracting raw dollar liquidity is critical, it’s just as important for prediction markets to attract eyeballs as they are also a prerequisite for efficient markets.

Beyond liquidity, the second major challenge prediction markets face is oracles. In other words, how do they figure out who won and lost? Prediction markets call this the “resolution process.” It sounds easy in theory, and most of the time, it is, but countless edge cases prove the process is far from perfect.

I lost $750 today on @Polymarket because their brilliant “oracle”, UMA, graded a bet as unanswerable. Something needs to change drastically about how Poly settles bets. The Poly team failed bigly here, and continues to fail as long as Uma is around.

— AG123 (@AG123321GA) August 29, 2024

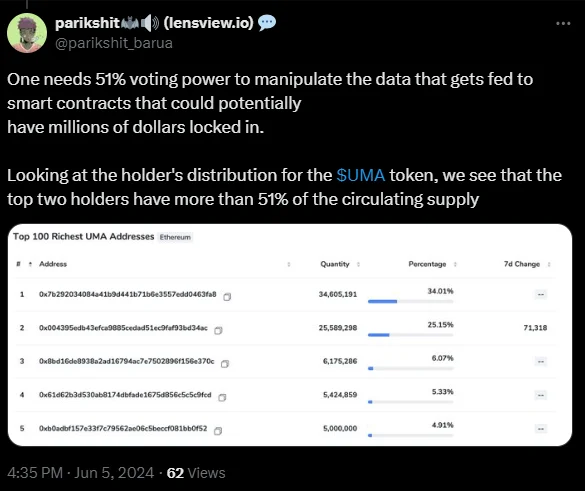

Polymarket uses Uma Protocol — an oracle on Polygon — to handle the resolution and dispute process. Any better can propose a resolution (i.e., “I think X won and Y lost”), which is executed on UMA. Then there’s a two-hour window for other betters to dispute it. If there’s no dispute, then Polymarket resolves the bet, which happens ~98% of the time.

But if it’s disputed (~2% of bets), UMA token holders (not Polymarket traders) have 24 hours to vote on the dispute. But votes are hidden and not shared with anyone. And after 24 hours, voters have another 24 hours to reveal their vote, which is optional. After that, UMA will report the vote results and resolve the dispute with Polymarket. Super simple, right?

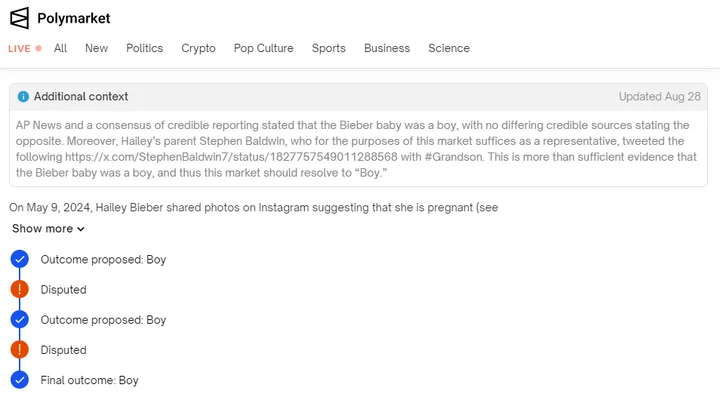

One of the spicier Polymarket resolutions occurred recently and involved Justin Bieber. The debate centered around a $1.1M Polymarket bet on the gender of Justin Bieber’s baby. The result “boy” was proposed twice and disputed both times, despite some pretty compelling facts:

- the baby’s name is “Jack Blues Bieber”

- the Associated Press called the baby a boy

- the baby’s grandpa called the baby his grandson

However, this wasn’t enough for some UMA voters because Polymarket’s rule on this bet clearly stated that only Justin/Hailey Bieber or their official representatives could confirm the baby’s gender.

Justin and Hailey Bieber welcome a baby boy, Jack Blues https://t.co/E3hJmGqpbv

— The Associated Press (@AP) August 24, 2024

Many Polymarket users were upset by the UMA disputes and saw them as pedantic, especially since the market priced “boy” at 100%. However, many UMA community members believed voting against “boy” was a better idea because it aligned with their principle of strictly following the market’s rules even when the “facts” were clear. Ultimately, the Polymarket team stepped in and saved the market for the boy betters.

Besides the Biebs, several other resolutions have gotten mired in technicalities. The convoluted process more generally leads to poor UX and frustrated users. At best, people view current resolutions as needlessly complex. And at worst, they view it as a UMA-controlled cabal.

Some have proposed moving the Polymarket resolution process in-house, while others have pushed for AI-assisted oracles. Uma remains the status quo, but this approach will not scale. Newer prediction market platforms like Drift have opted for centralized resolution where the core team has the final say. But this is not the Future of France either. For prediction markets to be a source of truth, the resolution process must be effective and widely trusted — and right now, that’s not the case.

The final challenge prediction markets face is opportunity cost. Every market faces this, but it’s a yuge issue for prediction markets because they are zero-sum. For every prediction market winner, there is an equal and opposite loser. The total money in the market stays the same — what one person wins, another person loses.

When you hold SOL, you are competing in a non-zero-sum game. Over time, if the price of SOL increases, you make money and haven’t taken anything from someone else. Your SOL is simply worth more — both you and anyone else holding SOL benefit from this increase. No one had to lose for you to win.

However, if you place a bet in a prediction market — say, on whether the price of SOL will be above $150 by next month — you are competing in a zero-sum game. If you bet 10 SOL that it will go above $150, and someone else bets 10 SOL that it won’t, one of you will win, and the other will lose. No new value is created; what one person gains, the other loses. The market sums to zero, hence zero-sum.

To state the obvious, it’s harder to make money in zero-sum games than non-zero-sum games. There are just less winners. Especially considering that many platforms charge fees, which actually make them negative sum. There are a few ways to solve this problem. The first is by not charging fees. Super innovative, I know. And the second is to let users earn a yield on their positions. Drift is one of the first platforms to offer this. It can do so because it runs a borrow/lend platform that’s composable with BET, their prediction market.

Composability is our best solution to the zero-sum problem. If all the money bet on prediction markets accrued interest, then the total pot of capital would grow over time, and the market would be positive-sum. Polymarket does not offer this yet, but competition may force its hand. One of the key trends to watch over the coming months is how aggressively platforms integrate prediction markets into DeFi.

Thank You, Next

With the bull- and bearposting behind us, it’s time to talk about the state of play across prediction markets. The good news is the three issues we riffed on above — liquidity, oracles, and opportunity cost — are all solvable. And smart teams are iterating on each of these. To date, there have only been a few prediction market apps, which has slowed the rate of innovation. But that will soon change.

there’s like 25 prediction markets launching in the next 2 months lol

— mikey (@Mikey0x_) August 28, 2024

Like everything in crypto, a breakout app invites competition and creativity. And thanks to Polymarket’s success, there will be an explosion of new entrants over the next 6-12 months. Most will flame out, but a few may push the entire space forward.

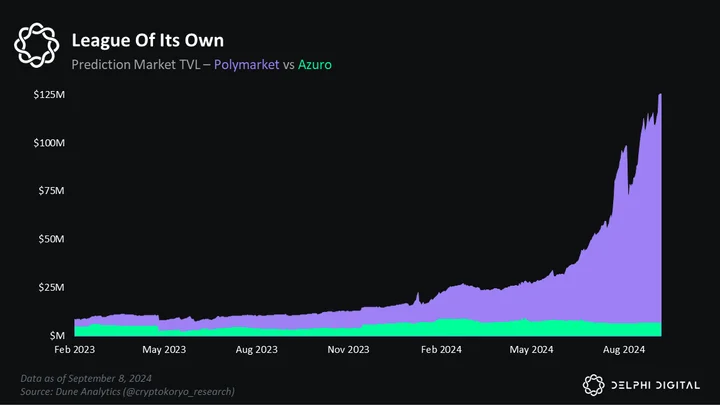

The new entrants will all be gunning for Polymarket — the clear top dog. Its next closest competitor is Azuro, which is a ways behind.

Azuro and Polymarket have a peculiar relationship. As the two largest players in the space, they are competitive. But Azuro also provides liquidity on Polymarket, so maybe the better way to think about them is as frenemies. They are also going after different segments of the market. Azuro wants to be the liquidity layer, the backend of sorts, for other prediction markets. While Polymarket wants to own the whole stack — liquidity, markets, and users.

Another difference is that Azuro has a token, and Polymarket doesn’t. But despite all the prediction market hype and its relationship with Polymarket — the AZUR token has been flat since it launched in June.

It’s pretty wild that polymarket dominates Azuro in prediction volume despite the latter having the power of a token pic.twitter.com/AHO7rJC2aN

— Sam (@swmartin19) August 12, 2024

Drift is the last major player we shall discuss. Its BET platform is essentially Polymarket on Solana. After going live in late August, Drift has done $27 million in total volume, which is like two days of Polymarket activity. But despite its slow start, Drift is worth watching for several reasons. First off, it’s on Solana, so it benefits from the retail activity on the shared state. Polymarket is on Polygon, and Azuro is EVM-based, so they don’t enjoy the same ecosystem vibrancy.

Drift is also interesting because BET composes with its perps DEX and borrow/lend platform. This is yuge for liquidity bootstrapping because users can place bets and earn yield on more than 30 collateral types. It’s also a significant upgrade over Polymarket, where you can only use USDC. Drift’s built-in yield will also help it overcome the opportunity cost issue we riffed on earlier.

Beyond Polymarket, Azuro, and Drift, there aren’t any other notable players in the predictions market space yet. Although competition is coming. Most of the new entrants are innovating along a few axes:

- permissionless markets

- oracle UX

- new markets

- distribution

Right now, market creation on Polymarket is centralized. Users don’t like this because it limits what they can trade. Polymarket is permissioned mainly because it’s hard to set lines on many on the long tail of markets. Going fully permissionless would probably be a recipe for resolution disaster. But that’s not stopping smaller apps from trying it anyway. Limitless is one team that’s carefully trying to exploit this opening. They are focused on daily expiry bets and have let users request markets for them to whitelist. It’s not fully permissionless, but it’s a step in the right direction.

Oracles are another area to watch. Polymarket’s reliance on UMA results in poor UX and is ripe for disruption. The two ideas du jour are 1) AI settlement and 2) improved decentralized settlement. AI settlement seems like the most promising. In theory, it should be possible to finetune a model on a bunch of prediction market data and edge case scenarios and then let it handle the resolution of these markets. This is a narrative for now, but the race is on to see who can bring the first production-ready AI oracle to market.

The third axis of innovation is new betting categories. Like we discussed earlier, most prediction market activity is tied to the election. What the next breakout category will be is still an open question. Some think it’s pop culture; others say gaming, and a few believe in SocialFi.

Of the three, SocialFi is the most interesting because it would imply a new form of distribution. Maybe that’s Twitter Blinks or Farcaster Framers. But the big unlock here is bringing prediction markets to users and embedding them naturally in existing conversations. One emergent behavior on Polymarket is the comments section has become its own form of SocialFi. Traders love to gossip about news, brag about positions, and keep a running dialogue with other degens. If someone brings prediction markets to an app like Twitter, Telegram, or TikTok, things could get interesting fast.

Humanity’s Oracle

Prediction markets help us better understand the world. They are not perfect, but they are the best tool we’ve got. And they have already profoundly impacted society in obvious and non-obvious ways. The Boden saga is the most obvious example. It’s the one even normies know about. It proved that markets are a superior information source to biased media and partisan politicians.

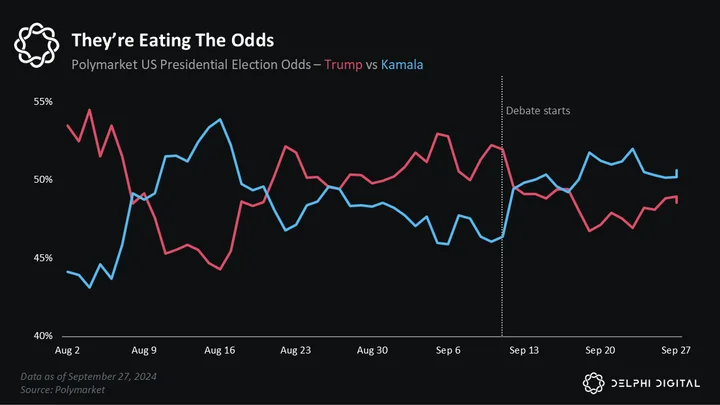

A more subtle form of influence came during the Trump-Kamala debate. At first, most of CT was predictably cheering for Trump and saying nice things about his performance. But then the markets moved sharply against Monsieur Trump.

Within the first 20 minutes, Kamala erased Trump’s +6% lead on Polymarket. Around this time, Twitter sentiment shifted. People stopped pretending Trump was doing well. The market had spoken, and overt bias on the TL became less tenable. The real-time feedback prediction markets offer can be a ground truth of sorts and potentially help narrow the divide on basic questions of what’s real vs. fake.

As prediction markets go mainstream, these two examples will be instructive. The first suggests that markets can provide some desperately needed social infrastructure that helps us understand what’s real and what’s not — especially as we enter the age of AI. And the second gives us hope that markets can also be a neutral referee in the culture wars that plague our society.

the market will decide

— James (@_jhunsaker) August 28, 2024

So, in summary and summation, prediction markets are like the Oracle of Delphi — prescient yet fallible. They are powerful truth-seeking machines that have already proven their worth. Just as free chatbots democratize intelligence, prediction markets will do the same for truth.

The flippening:

News edition pic.twitter.com/q3otsDvfuG

— Shayne Coplan (@shayne_coplan) September 28, 2024

The Futarchy Rises

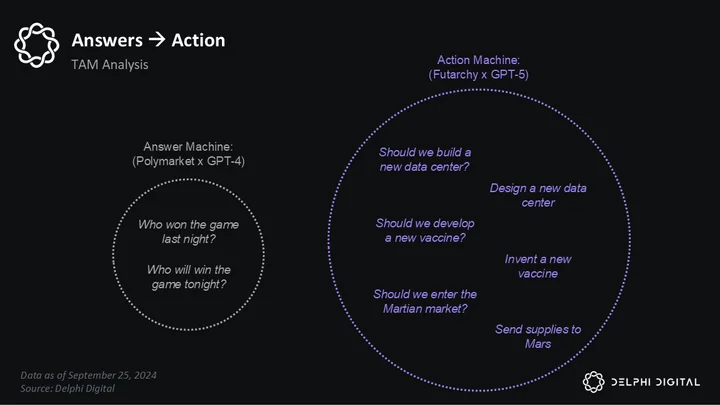

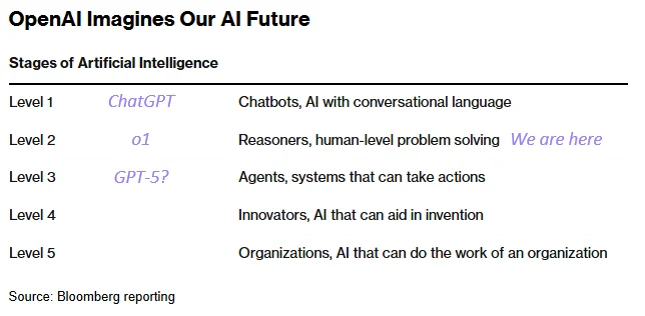

ChatGPT started as an answer machine. You ask it a question, and it gives you an answer. Prediction markets do something similar for markets. You ask the market a question, and it gives you an answer. But ChatGPT and prediction markets are limited because they are passive. And world-altering technology requires action. With AI, that’s agents. And with markets, that’s futarchy.

Futarchy unlocks a new level of insight into the future. The impact of such a tool is hard to predict as it represents such a fundamental upgrade to society. It’s a new part of the human tech tree. How do you model that in a DCF? It’s impossible. But we can at least do some back-of-the-envelope math and say that futarchy’s TAM is an order of magnitude larger than prediction markets.

But before we get too carried around with future-poasting, let’s get back to the basics. WTF is futarchy? It’s pretty simple. Instead of having politicians or voters make decisions, why not markets? This is not a new idea. Futarchy was proposed by famed economist Robin Hanson in 2000, and for many years, it languished as a topic of nerdy fascination in tech circles. Vitalik wrote about it in 2014, and the AI crowd would occasionally tweet about it, but other than that, nothing happened.

when will someone implement a futarchy based DAO. all the tools are here

— roon (@tszzl) January 9, 2022

It wasn’t until this year when an anonymous dev operating under the pseudonym ‘Prophet’ introduced MetaDAO — the world’s first implementation of futarchy on Solana.

I published the @metaDAOproject whitepaper in the #random channel of the @anchorlang Discord on November 10th, 2022 (2 days after FTX halted withdrawals)

at the time, I had 1 follower on Twitter (@harkl_)

— Proph3t (@metaproph3t) December 31, 2023

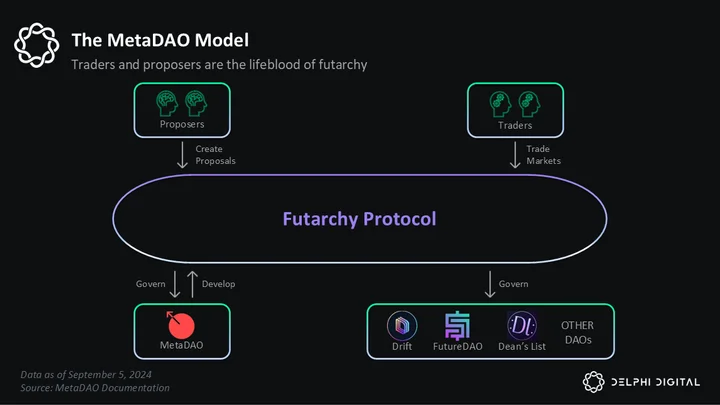

MetaDAO is building decision markets. It’s similar to Polymarket but with some key differences. In a prediction market, you bet on what you think will happen. In a decision market, you bet on what you think should happen. Prediction markets are passive. You sit on the couch, watch the game, and bet on who you think will win. You have skin in the game but no control over the score. Decision markets are active. By speculating, you are actually influencing the outcome.

for some people, the world happens *to* them. don’t be like that. be what happens to the world

— kache (@yacineMTB) November 11, 2023

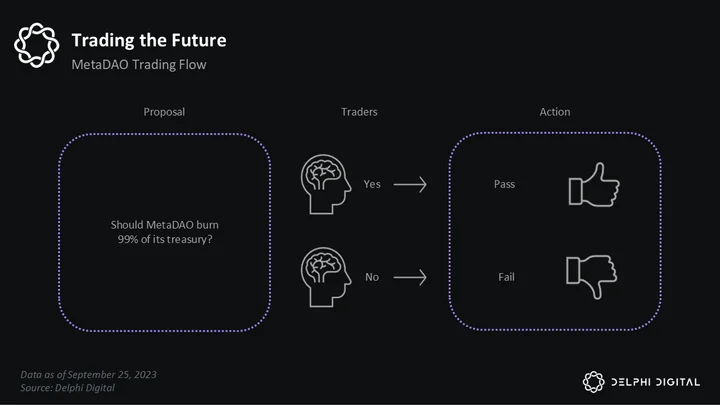

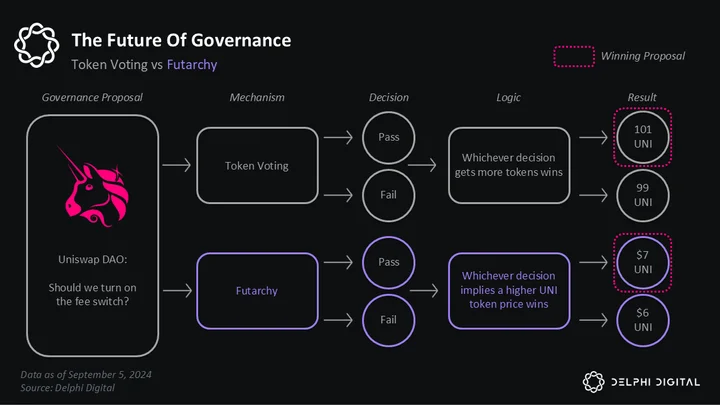

At the heart of MetaDAO is futarchy, which is essentially just prediction markets for decisions. The market determines every big decision MetaDAO faces. While a traditional DAO votes, MetaDAO trades. Proposals have a market, and instead of voting yay/nay, people trade pass/fail — betting real money that can be won or lost.

MetaDAO is not some niche governance tool or another ve-voting ponzi. It’s a zero-to-one upgrade for how we make decisions. Just as markets lead to efficient prices, futarchy will lead to efficient decisions. If such a system were widely implemented, the impact on economic growth and human flourishing would be hard to fathom.

fun fact:

the @MetaDAOProject PDA is derived from the last two sentences of the declaration of the independence of cyberspace

“We will create a civilization of the mind in cyberspace. May it be more humane and fair than the world your governments have made before.” pic.twitter.com/Yti6NoYui1

— Proph3t (@metaproph3t) February 10, 2024

But let’s stay grounded. To change the world, we must first change how we make decisions. Instead of making decisions by vote, cabal, or committee, futarchy wants markets to make decisions. Why should we trust markets? Well, for the same reason we trust prediction markets over CNN and Fox News. Throughout history, markets have proven superior to human decision-making in almost every way. Let’s rip thru some of the greatest hits.

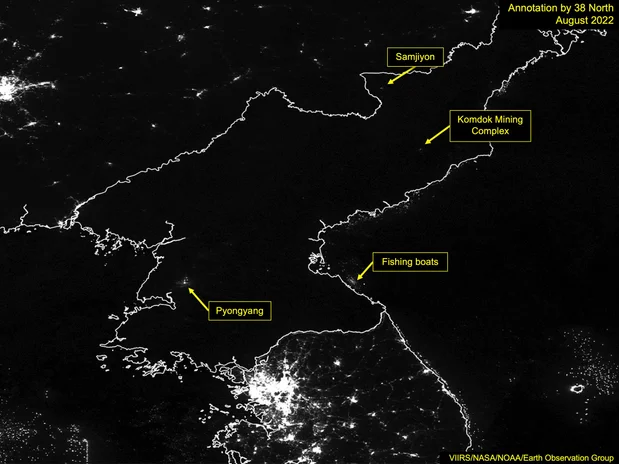

The canonical example of markets vs humans is North and South Korea. In the North, decisions are made by one dude. While in the South, decisions are made by millions of dudes and dudettes. The difference between the two systems is literally visible from space.

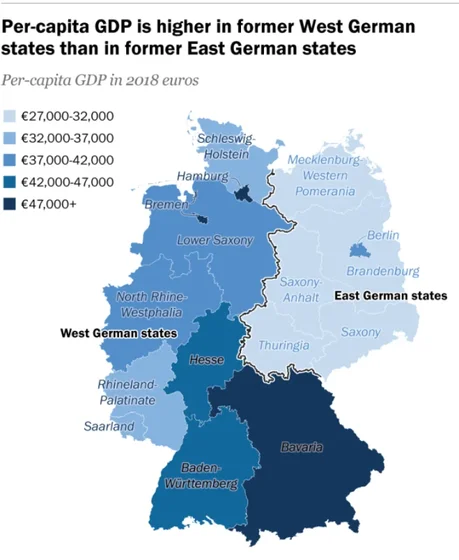

South Korea’s GDP is over 50x larger than North Korea’s because of decentralized decision-making. In the South, millions of Koreans decide what products to buy, where to invest, and what to do for work. This bottom-up decision-making enables the miracle we call capitalism. Meanwhile, in the North, millions of Koreans have their decisions made for them. They are told what to buy, what to eat, and how to live. This top-down decision-making has led to poverty, hunger, and stagnation.

Aside from Korea, markets have proven superior to humans in several more granular areas. Three of the cooler examples come from elections, spaceships, and Silicon Valley:

Elections

- Since 1998, pollsters accurately predicted the next president 78% of the time. Meanwhile, the S&P500 has accurately predicted the winner of every (!) presidential election since 1984. In the years when the index rises between August and October, the incumbent party has won every time, but when it falls during that period, the challenger has always won.

Spaceships

- After the Challenger space shuttle exploded, it took the market 21 minutes to identify the company responsible — Morton-Thiakol — and punish its stonk price. Meanwhile, it took a six-month Congressional investigation for the government to reach the same conclusion.

Tech Companies

- Computer maker Hewlett-Packard ran a series of internal prediction markets from 1996-1999 to forecast computer workstation sales. Despite being thinly traded, these markets outperformed HP’s own internal predictions. Google, Microsoft, and Siemens have also quietly used prediction markets and seen impressive results.

Markets can be a powerful tool if we let them. For far too long all we have asked them to do is price assets. But as the examples above show, markets can do so much more than that. Prediction markets are the first step and futarchy is the second.

Just as Bitcoin decentralized money, futarchy aims to decentralize decision-making. Both recognize that markets are a powerful tool for good. Few things in life are certain, but free markets outperforming closed systems is usually a good bet.

MetaDAO’s Moment

We talked about the why; now it’s time to talk about the what. MetaDAO’s initial implementation of futarchy is elegant in its simplicity. Every major decision the DAO faces — like whether to build a new product or burn 99% of the treasury — is subject to a market. The market asks traders to consider one thing and one thing only: “Will this decision make the token price go up or down?” If traders think a decision will increase the price of MetaDAO’s governance token, they bid pass. And if they think it will make the token go down, they bid fail.

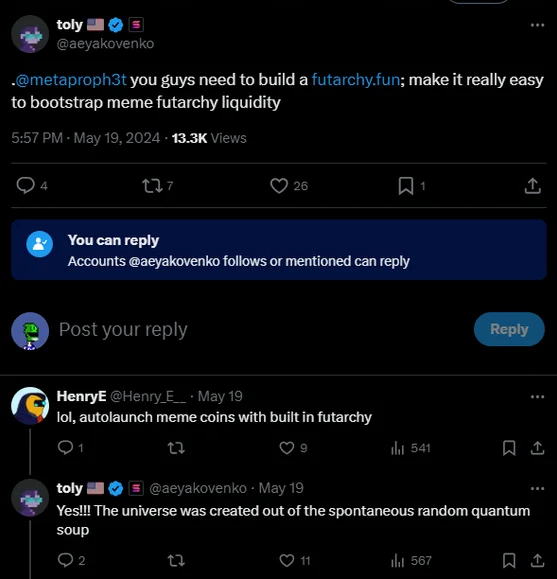

One of MetaDAO’s most recent proposals sparked record volume and is a good case study. It was titled “Should we release Futard.io?” and the idea behind it actually came from Anatoly, who suggested that memecoins should use futarchy.

The MetaDAO team heeded Toly’s advice and submitted a proposal to the market asking whether they should build Futard.io — a pump.fun fork that would let memecoins use futarchy to make decisions. Traders had two options — pass or fail — depending on whether they thought the new product would be bullish or bearish for the price of META, MetaDAO’s governance token.

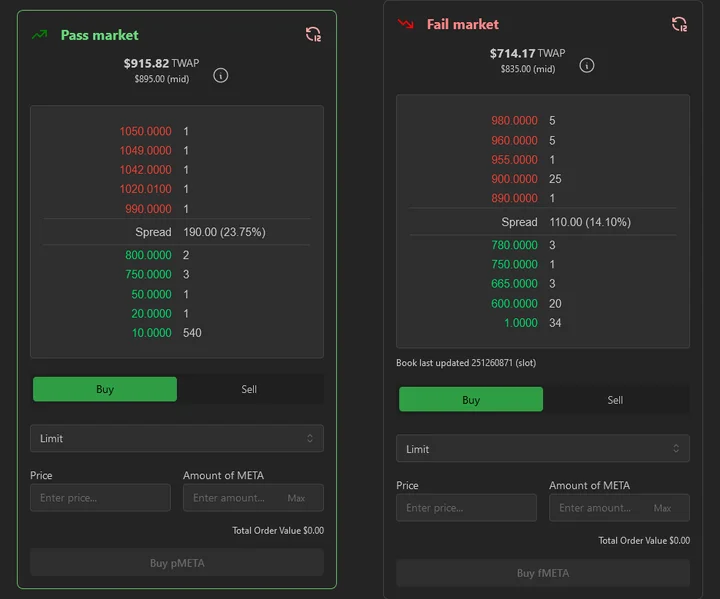

Let’s walk thru how to trade this proposal. First, we need to navigate to the MetaDAO website. Once there, we will see three important prices. Note: these are examples.

- spot META: $1,000

- pass META: $1,100

- fail META: $900

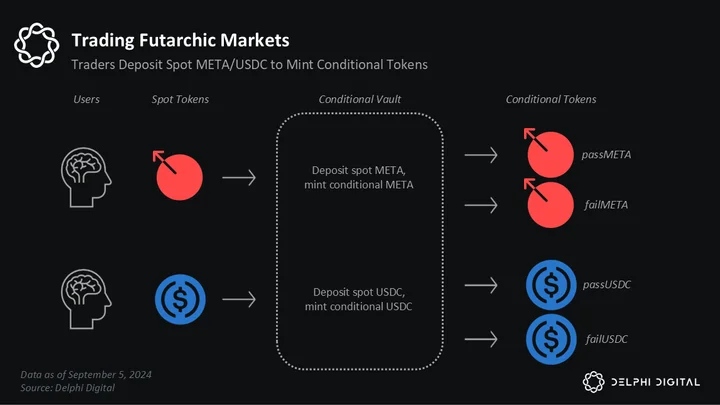

The spot price is the actual spot price, meaning it’s the price of META you would see on Jupiter or Orca. The pass and fail prices refer to conditional tokens. This is MetaDAO’s primary innovation. Conditional tokens let you create two temporary markets during a vote: one contingent on a proposal passing and the other on it failing.

In our example, the pass market is winning.

- spot META: $1,000

- pass META: $1,100

- fail META: $900

The Futard.io proposal would pass as long as the prices hold. But let’s say we really want this proposal to pass because we think it would be yugely bullish for our META bags. In this case, we have two options to express an “I want this proposal to pass” view. We can either:

- buy pass META (pMETA)

- sell fail META (fMETA)

To buy pMETA we need to deposit spot USDC into the MetaDAO vault and mint conditional USDC. We can then use this conditional USDC to buy pMETA. If we bought pMETA at $1,100, we would express the following view: “I think META will be worth at least $1,100 if the proposal passes.” Another way to phrase this is: “I think the Futard.io proposal is worth at least $100 to the price of META.” Either way, our action implies we think the proposal will make numba go up.

An alternative way to express this view is to sell fMETA. This would signal the same thing as buying pMETA. To sell fMETA, we first need to acquire some. We can do this by depositing spot META into the MetaDAO vault and minting conditional META tokens. Then we could sell our fMETA, which would express the view: “I think META will be worth $900 if this proposal fails.”

Think of coin futarchy as a kind of voting-through-action: “I am willing to increase my degree of membership in this community if X happens”

— vitalik.eth (@VitalikButerin) November 18, 2016

You might be wondering why there are three prices — spot META, pMETA, and fMETA. It’s confusing, I know. MetaDAO doesn’t have a Polymarket-style two-sided pool because the markets need to weigh the cost of not doing something. At a very basic level, every MetaDAO proposal considers the impact of doing a thing vs not doing a thing. With the Futard.io proposal, traders weighed the impact of building a new product vs the impact of not building it.

If there were only two prices — say, META and pMETA — there would be no way to measure the impact of not doing the thing in question. As a result, the pMETA and spot META prices would naturally converge over time as both price in the value of doing the thing — in this case, building Futard.io. So, the presence of a third price — fail META — ensures a spread between spot and pass META, which is necessary to determine whether or not to actually do the thing.

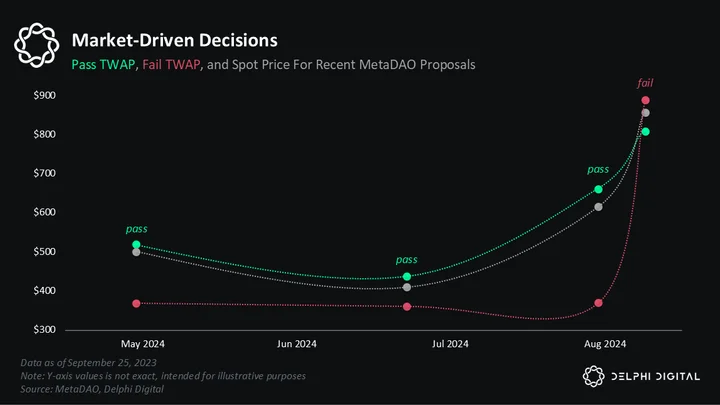

The Futard.io proposal traded for three days, as is standard, and ultimately failed. During this period, a time-weighted average price (TWAP) was used to determine the price of each market (pass and fail). For a proposal to pass, the pMETA TWAP must end at least 3% higher than the fMETA TWAP.

MetaDAO uses TWAPs to calculate prices to mitigate certain types of attacks. However, this approach introduces other issues. For instance, the TWAP values the first day of trading the same as the last. This is problematic because most people only pay attention toward the end of a proposal. In a perfect world, we would want to overweight the prices during active periods and underweight the prices during inactive periods.

The current mechanism is somewhat naive. A dumb but probably effective way to exploit the lazy TWAP is to trade heavily in the early hours of a proposal when no one is paying attention. You could lock in favorable prices and make it difficult to alter the outcome later in the trading period becomes hard.

We can see this “most people trade late” dynamic in the price volatility. The green and red lines are smooth at the beginning of the Futard.io proposal below, indicating little activity. But then the lines start to squiggle towards the end as people start trading. The only problem is in the eyes of the TWAP, the prices at the start count the same as those at the end.

A common question with MetaDAO is — can I make or lose money trading these proposals? Yes, you can. In this sense, trading decision markets is no different than trading on Coinbase. In both cases, you make money by trading at good prices (buying low and selling high) and lose money by trading at bad prices (buying high and selling low).

The only caveat with decision markets is your P&L only materializes on the market that wins. If a proposal passes, only your P&L from the pass market carries forward, and the reverse applies if the proposal fails. In either scenario, any losses in a settled market are as real as those in spot trading.

Passing and Failing

MetaDAO isn’t perfect. It’s still rough around the edges. The UI is complex, the three markets are confusing, and the TWAP is naive. However, these are implementation details that will be fixed. It’s worth remembering that an onchain futarchy has never been tried before. It’s not the millionth L2 or Uniswap fork; it’s something new, so there’s no established playbook.

there’s 51 L2s built on the OP stack alone jfc

— SS (@stevenshi_) August 26, 2024

Despite all of the friction, MetaDAO’s conditional markets work. And the decisions they have produced have been surprisingly effective. Denying the Futard.io proposal is perhaps the best example. It was the ultimate eye candy — a quick hitter pump.fun fork that could just maybe, inshallah, make META moon. However, traders saw through the pumponomics narrative and rejected the proposal because it was vague and poorly worded. The market believed Futard.io would distract the team from mission-critical projects like fixing the front end and building the grants product. So, based on a small sample size of 20ish proposals, the crazy science project seems to be working.

Let’s zoom out for a sec to riff on MetaDAO’s higher-level strengths and weaknesses.

Strengths:

- incentive alignment

- participation

- minority protection

Weaknesses:

- liquidity

- oracles

- power

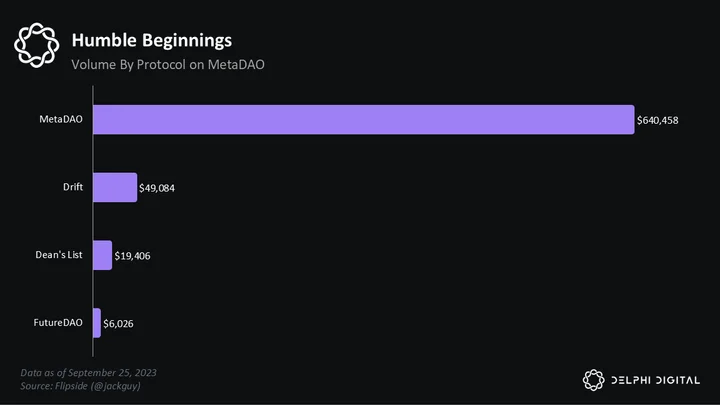

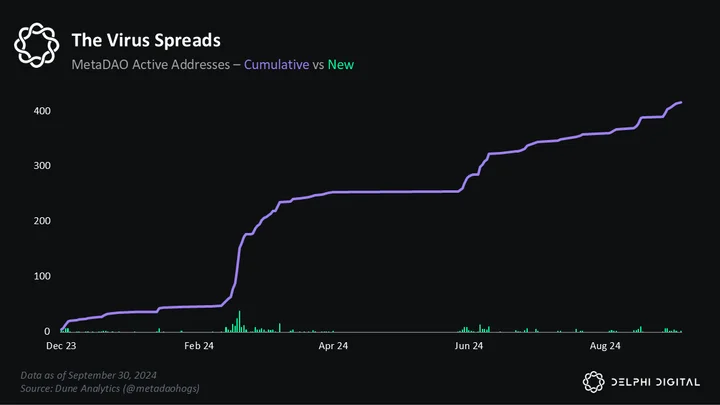

We’ll start with the bad stuff first. Liquidity. Similar to prediction markets, liquidity is a major issue for MetaDAO. Low liquidity means high slippage, which deters trading and generally makes markets less efficient. Since the first proposal went live in May 2024, roughly $700k has changed hands. The most recent proposal saw $45K in volume, which is quite low.

The numbers are even smaller when you look at the other three protocols that use MetaDAO’s futarchy platform — Drift, Dean’s List, and FutureDAO. Proposals for these teams typically see an order of magnitude less volume than MetaDAO.

There’s also the concentration issue, as only 414 wallets have interacted with MetaDAO’s markets. To provide real signal for decision-making, these numbers must rise.

But like we talked about in the prediction market section, liquidity is a solvable problem. However, MetaDAO does face a unique challenge because decision markets are new. It must solve some education and UX issues before capital can really start flowing. Education will require better docs, more explainer videos, and viral tweets. People need to understand MetaDAO before they can use it.

Autocracy: power to the Leader

Democracy: power to the People

Futarchy: power to the Market— Hardhat Chad (@HardhatChad) March 23, 2024

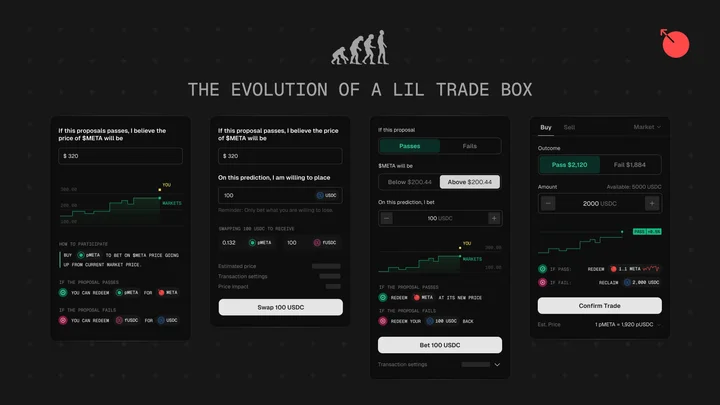

The second piece involves the website UX. Right now, it’s clunky and confusing. Part of this is because MetaDAO is <1 year old. But it mostly has to do with the fact that no one really knows what a decision market should look like. It’s all brand new, so the team will have to iterate on a design that feels familiar to users of popular platforms like Hyperliquid and Jupiter while preserving the things that make decision markets unique. Just a few months ago, the UI looked like this…

But progress is being made. And the good news is the team has plenty of help. After Paradigm led MetaDAO’s seed round, their designer started working with the team to revamp the trading interface. Here are some early mockups…

Continuing with the prediction market comparison, there are two reasons to believe that MetaDAO will have an easier time bootstrapping liquidity than Polymarket:

- decision markets are non-zero-sum

- decision markets create natural arbitrage opportunities

When you bet on Polymarket, you could lose 100%. For instance, if you bet on Kamala and Trump wins, you would lose everything. But decision markets work differently. In a MetaDAO market, even if you bet on the losing side, you might only lose 1% if you traded at good prices. So, unlike Polymarket, MetaDAO is not zero-sum. This makes decision markets more attractive for traders.

Another difference between Polymarket and MetaDAO comes down to market structure. Most Polymarket bets exist in isolation. For instance, the “What gender is Justin Bieber’s baby?” market has zero impact on the price of BTC or SOL. But MetaDAO is different.

Decision markets are essentially parallel markets for governance tokens. Until now, you could only buy a gov token like META on a vanilla AMM like Orca or Meterora. But now you can buy conditional META on MetaDAO. This creates natural arbitrage opportunities. And arbitrage is the lifeblood of onchain activity. CEX/DEX arbs are estimated to make up around 20% of all DEX volume. MetaDAO will benefit from arbitrage as it drives volume and liquidity.

has anyone done an updated analysis on % of cex-dex volume that @FrontierDotTech did ~1.5 years ago? pic.twitter.com/pygyqrjJ8l

— ceteris (@ceterispar1bus) September 10, 2024

The second challenge MetaDAO faces is the oracle problem. But in this case, “the oracle problem” is probably a misnomer since MetaDAO doesn’t use a traditional oracle system like Uma. Instead, MetaDAO uses the price of governance tokens. This is an elegant approach because it eliminates all the alignment larp that comes with token voting.

Futarchy / @MetaDAOProject is the main interesting new trend in governance I see. . . it’s a complete break from the disease of delegation-itis I see in most Ethereum DAOs. . .the whole classic VC-funded DAO delegation protocol stuff with student groups etc. has never made much…

— _gabrielShapir0 (@lex_node) September 28, 2024

The only problem is not every decision involves a token. For instance, web2 companies do not have tokens, so they cannot use MetaDAO’s current implementation. This will eventually change, as MetaDAO is working on a grants product. Grants seem like an obvious use case for futarchy as they should only be issued if they are +EV. Before MetaDAO, it was impossible to quantify whether a grant proposal was good or bad. But futarchy solves this by letting teams ask the market whether a grant is a positive or negative EV.

not normally into hustlepoasting, but it’s 10pm in SLC and I finally got the new conditional vault working

it will enable you to run markets for ANY decision and ANY metric

want a market to determine whether your DAO should give a grant? you got it

want a market on whether… pic.twitter.com/6udzQPE1fp

— Proph3t (@metaproph3t) August 25, 2024

MetaDAO’s goal is to run markets on any decision and any metric. Starting with price makes sense because it’s simple and intuitive. However, for MetaDAO to scale, it must support more than just price. Grants are a good first step. Drift has already expressed interest in using the upcoming grants product. And Jito has a live vote on whether they should integrate MetaDAO Grants. Even Anatoly has expressed interest in using futarchy at the Solana Foundation to fund grants and make other critical decisions.

I think a cool end state for L1 foundations is a futarchy market for underwriting the risk of putting together the L1 ecosystem conference

— toly 🇺🇸 (@aeyakovenko) September 23, 2024

After grants, you could imagine MetaDAO adding support for metrics like revenue and profit. But the question remains of just how many metrics are measurable and objective enough to run futarchy on.

the single most important line of work in prediction markets is figuring out how to fully leverage the information value they produce

— frankie (@FrankieIsLost) August 13, 2024

As a quick aside, it’s interesting to think about the similarities between finding a metric to run futarchy on and finding a metric to base a loss function on for AI models. Both require a precise number that drives the systems towards a desired outcome. In futarchy, metrics capture societal values, while in AI, the loss function tracks predictive error. Both fundamentally shape behavior, whether it’s traders or algorithms. And the most effective metrics, like asset prices or next-token prediction, are often simple and easily measurable. For both systems to scale, we need to invent new metrics that capture more of the world’s nuance.

a loss function is a theological instrument meant to commune with the desires of higher powers

— roon (@tszzl) July 20, 2020

The final hurdle MetaDAO faces is power. It’s a direct and present threat to the powers that be. Just as Bitcoin threatens fiat currency, MetaDAO threatens product managers. In order to give decision-making power to the market, MetaDAO must first take it away from individual humans. In a crypto context, this means teams will no longer have the power to decide what to do with their treasuries, whether to go cross-chain, etc. Convincing anyone to give up power is an uphill climb, so it’s worth asking — why would a team do this?

Everything is a Futarchy, you just don’t know it yet https://t.co/4smfnRu15p

— toly 🇺🇸 (@aeyakovenko) July 28, 2024

The current answer seems to be vibes. MetaDAO has good vibes. It’s seen as futuristic and based. So, teams like Drift get a credibility boost by aligning themselves with MetaDAO. But vibes alone can’t scale. MetaDAO must prove that it produces 10x better decisions than the existing system. Doing anything 10x better is hard, but there are early indications that progress is being made.

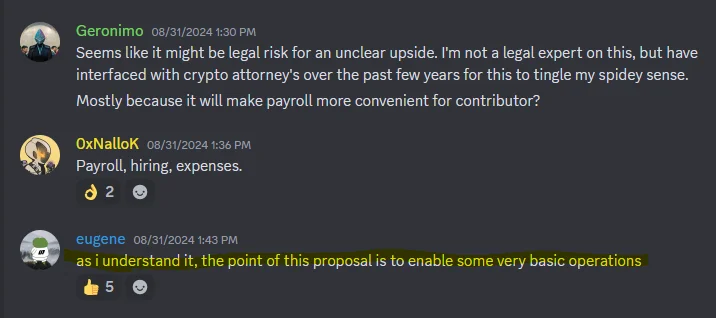

If you skim thru MetaDAO’s Discord, you will see a who’s who of top minds in the Solana ecosystem. Perhaps the most bullish thing about MetaDAO is the early mindshare it has managed to build. This is critical not just because of the vibes it creates but also because it means these people are trading the markets. Eugene, the founder of Phoenix Protocol, is a good example. A few weeks ago, Eugene jumped into the Discord to comment on a proposal. It dealt with whether or not to set up a US entity. Many people were confused, so Eugene shared his take:

This may seem like a dumb example, but it reveals MetaDAO’s core value prop. In other governance systems, there’s absolutely no way that Eugene — the founder of Phoenix — would waste his time commenting on an obscure legal entity. But with MetaDAO, he is essentially paid to do so. By connecting decisions to markets, MetaDAO creates a framework where the smartest people in the world can influence small yet critical decisions. You can imagine how this would be immensely valuable to a team like Drift who might want Eugene’s take on a decision but have no way to incentivize him to participate without MetaDAO.

Okay, time for the good stuff. First up is incentive alignment. But before we can talk about how MetaDAO solves this, we need to recap just how fvcked the current DAO paradigm is. There are so many problems it’s hard to know where to begin. But at a high level, DAOs suffer from two big problems:

- they are not decentralized

- they do not make decisions that benefit all token holders

Both of these points call into question what we’re even doing here. The first letter of DAO — “D” — literally stands for “decentralized.” But in practice, most DAOs are run by a couple of dudes on a multisig. And on the second point, today’s DAOs rarely make decisions that benefit all token holders. Teams often make decisions that benefit themselves and other insiders before the broader community. DAOs have replicated the worst qualities of traditional governance onchain.

They’re called “decentralized autonomous organizations” but basically the team and the investors decide every vote pic.twitter.com/gis2mLaWoV

— karbon 🐺🦊 (@basedkarbon) June 8, 2024

The easiest way to smell the dumpster fire that is modern-day DAOs is by looking at how they allocate their treasuries. You would think that DAOs would strictly spend their treasuries on things that drive value to token holders. Yanno, since the community partly owns the treasury, right? Well, that rarely happens.

every dao exists only to distribute its treasury to its insiders

— venture apologist (@0xBalloonLover) June 23, 2024

The Arbitrum Gaming Catalyst Program is a good example. These guys thought spending $250 million (!) on a single gaming program was a good idea. The topline number isn’t even the most absurd part. Arbitrum is paying $18 million in salaries on this program alone, with $180K going to each multsig signer to sit around and effectively do nothing.

Arbitrum Gaming Catalyst Program proposal has been approved & executed by the Arbitrum DAO today.

Seen real projects raise less in total to build an entire new protocol than this proposal earmarks for team salaries alone. https://t.co/lvdTfr9kEt pic.twitter.com/ihUslEhQ0I

— Wit (@witconomist) June 11, 2024

These kinds of decisions are the result of misaligned incentives. The current system rewards insiders and values performative action over decisions that drive value to the token. The current system is broken beyond repair. And the only way to deliver on the original promise of DAOs is to burn it all down and start fresh.

Futarchy is to DAOs what polymarket is to political pollsters.

— toly 🇺🇸 (@aeyakovenko) June 28, 2024

MetaDAO aligns DAO incentives with markets. Decisions must be sufficiently +EV to pass. And it’s hard to imagine markets accepting a decision that pays five dudes $180K/year to click a couple buttons. But we don’t have to hypothesize. We can just look at the decisions MetaDAO has already produced.

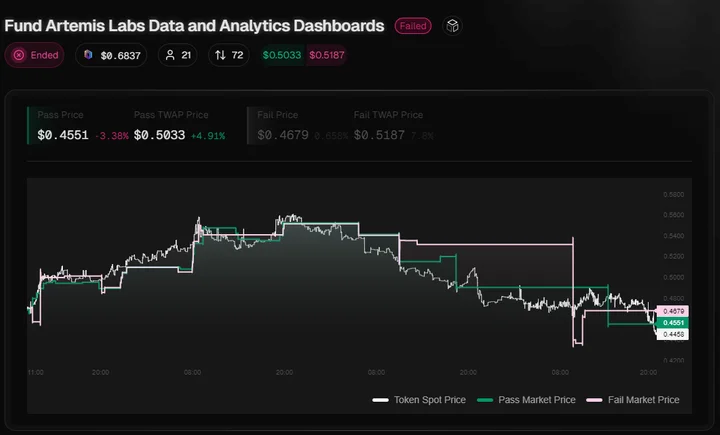

A few months ago, Drift Protocol ran a market called “Fund Artemis Labs Data and Analytics Dashboard.” The proposal aimed to grant Artemis, a data provider, $50K in DRIFT tokens to build a dashboard. This is a classic DAO decision. And one that’s usually rubber-stamped by trigger-happy multisigs. It’s easy to see why teams love dashboards. They’re a prestige purchase. It’s like buying a nice watch — it signals you’re legit.

The Optimism DAO should buy this pic.twitter.com/9RImkvBBGf

— Gwart (@GwartyGwart) January 19, 2024

The only problem is that dashboards provide questionable value to token holders. They might make the team look good, but do they drive value to the token? The Drift community didn’t think so, as they rejected the Artemis grant proposal. The markets signaled that funding Artemis would result in a lower DRIFT token price. So, in the end, the Drift team listened and did not fund the dashboard.

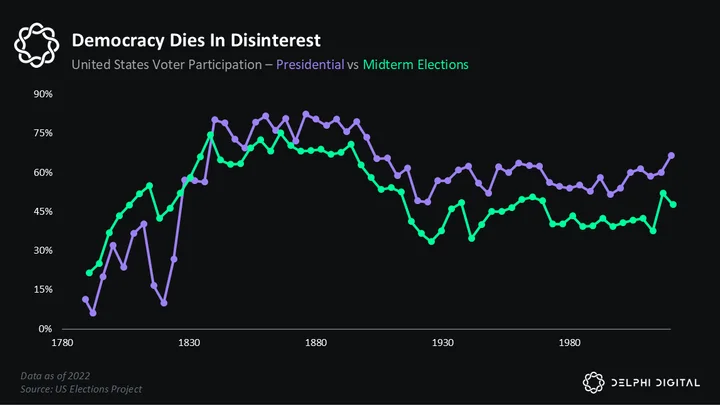

Voter participation is the second major strength of MetaDAO’s model. Low voter participation is a long-standing issue worldwide, particularly in the United States. In the 2022 US midterms, only 52% of eligible voters participated. The number jumped to 66% in the last presidential election but still ranks 31st globally, behind Mexico and Slovakia.

DAOs were once held up as the solution to voter participation. Proponents claimed they give people a financial incentive to vote and are global, so anyone, anywhere, can participate.

The idea of a DAO is that you can make people work together from all over the world, everyone can participate with capital & together you can build something much better than you would in individual organizations

In other words, a way to get the smartest people to work together

— Route 2 FI (@Route2FI) December 12, 2021

But the experiment has failed. DAOs suffer from significantly lower participation rates than traditional systems. The problem is so bad that some DAOs now pay people just to participate.

hmmmmmm pic.twitter.com/fOGlwKeLuR

— Matt (@MattFiebach) April 4, 2023

There’s essentially been no DAO innovation since they were born in 2016. The same issues still plague them as eight years ago. This begs the question — how much longer are we going to wait before trying something new? MetaDAO offers precisely that. Instead of praying that token holders participate, MetaDAO gives everyone a financial incentive to do so. And it’s not by bribing or dangling an airdrop over people’s heads; the financial upside is baked into the system from day one.

The Bible doesn’t explain this but hell is governed as a DAO and all 9 circles are sub-DAOs and that’s the worst part of eternal damnation, the bureaucracy

— Gwart (@GwartyGwart) April 22, 2024

By connecting decisions to markets, MetaDAO financializes DAO participation. “Financialization” is often considered a dirty word, but it’s a good thing here. It means that anyone can profit from a DAO decision. DAOs no longer need to rely on people to participate out of the goodness of their souls. Instead, with futarchy, people participate out of pure self-interest. This significantly expands the number of participants.

The third and final MetaDAO strength is minority protection. This is perhaps the least appreciated but most important one. Like proof-of-work blockchains, DAOs are vulnerable to 51% attacks. In the token voting paradigm, the majority rules. If I hold more tokens than you, I can push thru any decision I want, and there’s nothing you can do about it.

DAO IS BEING SECURELY DRAINED. DO NOT PANIC.

— Alex Van de Sande (avsa.eth) (@avsa) June 21, 2016

In practice, what ends up happening is DAO votes boil down to a16z vs Paradigm. VC firms almost always hold the largest bags and hold an effective trump card over governance decisions.

the endgame of every DAO is a16z its actually hilarious

— loomdart – Holy War Arc (@loomdart) October 31, 2021

Futarchy is much harder for VCs or any other whale to manipulate. Minority holders enjoy far more protection under futarchy than token voting. Kevin — a Solana searcher and early MetaDAO supporter — was the first to notice this in a Twitter thread:

An underrated benefit of futarchy is protections for minority holders. If the majority wants to push through a dumb or malevolent decision, they are forced to buy shares from the minority at a premium.

Futarchy literature (which is mainly Robin Hanson) comes from outside crypto and is more focused on markets as powerful information aggregators. Company law has okay protections for minority shareholders anyway.

But most DAOs have no such rules, and it would be hard to enforce them while still looking like a DAO. So instead the typical DAO allows the 51% to rob the 49% ad nauseam.

Futarchy solves this, even in situations where the market is not very efficient.

Corporate futarchy is not just about soliciting an opinion from the market. It’s a more robust form of joint ownership that protects minority holders via incentives rather than a laundry list of rules.

One of the biggest concerns people have with futarchy is: What happens if a giant whale comes in and manipulates the market? Many fear the system will lead to plutocracy, where the biggest bag-holders control all the decisions. In other words, a system no better than the one we live in today.

from a mechanism design perspective, I personally see the mass adoption of prediction markets as a threat to democracy and an accelerant toward plutarchy.

may not warrant banning them, and you probably couldn’t anyway, but they are not unilaterally a force for good.

— Hasu⚡️🤖 (@hasufl) August 6, 2024

At first glance, these fears seem reasonable. If every decision were run on futarchy, wouldn’t those with the most capital control everything? Well, no. This view is wrong and MetaDAO’s Proposal 6 shows why.

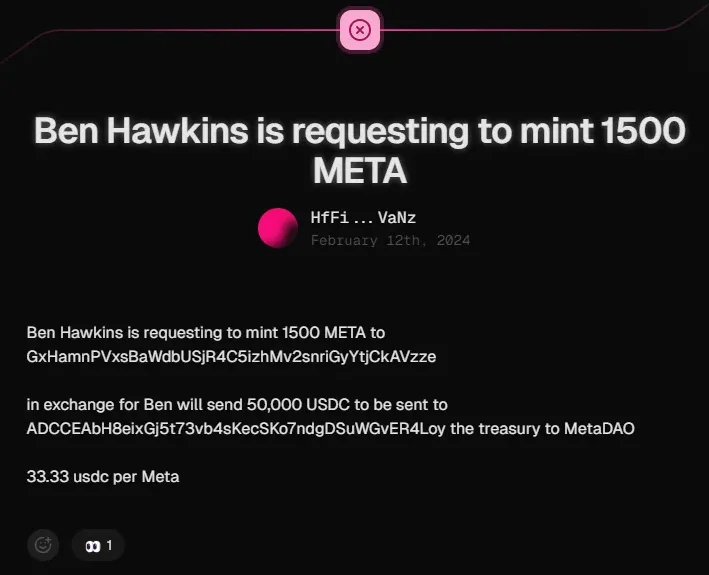

Proposal 6 is perhaps the most infamous in MetaDAO’s young history. It started pretty dull. The META token had just launched and was extremely illiquid. Every time traders bought or sold META, they were forced to eat crazy slippage, which pissed a lotta people off. Ben Hawkins — who works at the Solana Foundation but was operating in his personal capacity — stepped in to help. Ben proposed to buy $50K worth of META. The idea was he would get META and MetaDAO would get USDC, which could be used to improve liquidity.

Initially, the proposal made sense. It would have provided MetaDAO with some sorely needed USDC. But then the META price ripped from $100 to around $800. At this point, Ben’s proposal looked like a steal. It would effectively let him buy META at a 95% discount. Ben suddenly had a massive incentive to make sure the proposal passed. So, he decided to try and manipulate the decision by bidding up the past market. He eventually spent over $250K minting conditional USDC and buying pMETA.

Proposal 6 started trading on Feb 12 and ended on Feb 18

But by buying so heavily in the pass market, Ben drove the price of pMETA to nearly 2x that of spot META. His trades essentially said that he thought the price of META would 2x if the proposal were to pass. The rest of the market thought this was absurd. The proposal was a terrible deal for the MetaDAO and there was no way it would make the price of META 2x. So, people sold into Ben’s buys. They viewed him as a noise trader who was willing to buy META at an irrationally high price. In the minds of these sellers, the worst-case scenario was that they sold to Ben at 2x the spot price, and then once the proposal passed, they used the USDC from Ben to buy back all their META and pocket the spread.

Ultimately, Ben’s proposal failed. His $250K was not enough to overcome the wave of selling from traders who were more than happy to profit off Ben’s irrationality. Proposal 6 is the promise of MetaDAO. It proves markets are incredibly resilient and hard to manipulate, even for whales operating in low-liquidity environments. For context, when Proposal 6 went live, MetaDAO’s market cap was less than $730,000. So, Ben spent roughly one-third of META’s initial market cap in an attempt to manipulate the market. This is why futarchy will not lead to plutocracy. To rug minority holders in futarchy, you effectively need to buy them out. Ben tried and failed.

Futarded Future

If you made it this far, thank you. We’re in the home stretch and it’s finally time for the fun part — the MetaDAO thesis. I riffed on this a month ago on the Alpha Feed, but let’s dive in again now. The thesis boils down to three thangs:

- valuation

- incentives

- AI

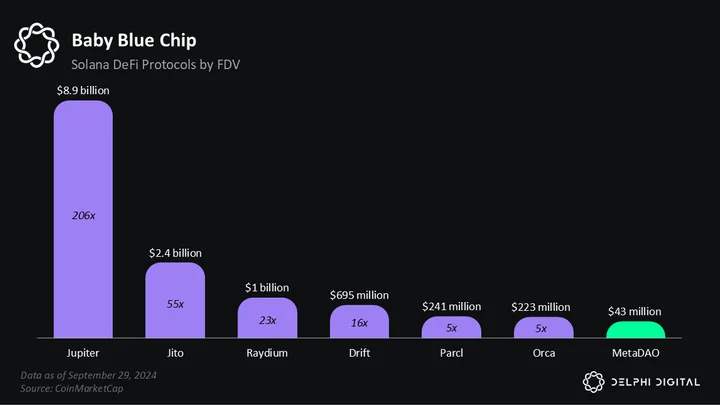

The first is the most straightforward. META is 100% circulating. It’s market cap = FDV. Right now, META is sitting at a $43 million market cap. If META were to reprice to a typical Solana DeFi blue chip, that would imply 5-20x upside from here.

META has a lot of work to do before it reprices to the level of a Drift or Raydium, but there is a path. The main reason to believe it’s possible is because MetaDAO is a new primitive. And aside from new tokens just generally being more exciting than old tokens, new stuff also has a structural advantage. When you launch a DEX, no matter how ‘innovative’ or ‘novel’ your marketing is, it inevitably gets comped to Uniswap. UNI’s valuation serves as a high-water mark, capping the potential upside for your ~revolutionary~ DEX token. But when you launch something new, there are no comps. There’s no pre-existing cap on how high the valuation could go. The upside is theoretically unbounded. It could go to infinity! New ideas let the mind run wild, which is precisely what we want as investors.

futarchy is one of those mind worm ideas like crypto – once you see it, you can’t unsee it

— jason badeaux 🔆 (@jasonbadeaux) July 5, 2024

The final point on a potential repricing is — crazier things have happened…

Along with its compelling valuation, META’s holder base is also unique. In November 2023, MetaDAO airdropped 10,000 META to around 60 wallets. At today’s prices, this is worth ~$350K. The criteria to receive the airdrop was literally to just be in the Discord. Guess who wasn’t in the Discord? Yeah… well, anyway, the 10,000 META tokens airdropped to early supporters make up almost 50% of the total supply. It’s safe to say MetaDAO conducted the most generous and valuable airdrop of this cycle by far.

alpha thread. There are two massively undervalued projects right now. Both have tokens. Both built innovative products. Both have a super technical anon founder who’s on a mission to bring fundamental changes to the solana ecosystem. Both have a 1000 true fans type of community.…

— r0bre (@r0bre) June 11, 2024

On one hand, such a large percentage of supply held by a small group is bearish. These holders will eventually take profit and sell. But in the short term, I actually think it’s bullish. Most of these people are hardcore Solana devs who don’t need the money or are day-one MetaDAO bulls. Remember, there were only 60 (!) people in the Discord. And this was before the Jito airdrop, so only the true Solana OGs were left. The timing meant that MetaDAO was able to get tokens into the hands of some of the most influential and fervent Solana believers. It’s a subjective call, but in my view, these airdrop recipients believe in the idea and are prepared to hold until much higher levels.

The second thesis point is incentives. MetaDAO is number go up technology. Every DAO decision is made thru the lens of “will this make the token go up.” This should be the case already, as the token going up is usually the only thing everyone can agree on. But in practice, tokens are rarely prioritized because DAOs have broken incentives that lead teams to prioritize themselves and other insiders over the wider token holder community.

starting to sink in that i can’t use my insider status to extract wealth from the DAO

damn… futarchy sucks

— Proph3t (@metaproph3t) February 18, 2024

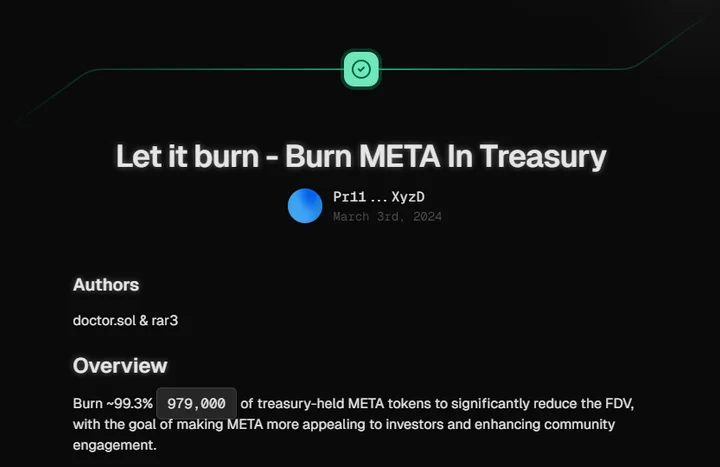

The Let it burn proposal, which burned 99% of the META treasury, is the kind of decision that’s downstream of MetaDAO’s incentives.

We have never seen a crypto protocol with this incentive structure before. It’s like a memecoin in the sense that the token price is all that matters. But it’s also radically different because MetaDAO is actually building real tech for real problems. You could say it’s the best of both worlds.

the CTO meta is officially dead

how can a community take over when they’ve always been in control?

— alon (@a1lon9) August 6, 2024

MetaDAO is only 22 proposals deep, but so far its incentive structure seems to be working. The “Let it burn” proposal is a flashy example, but there are others. For instance, the market deciding to raise a seed round shows the community is pragmatic about the value-add of VCs and is not jaded by the “VC bad” discourse that’s en vogue across crypto. This was a great decision as it brought Paradigm into the fold.

many decision-making systems in crypto today are broken. I’m excited for @paradigm to support @metaproph3t and @metanallok as they try to fix them https://t.co/ugvXGkQwZM

— frankie (@FrankieIsLost) August 1, 2024

Rejecting the Futard.io proposal also showed impressive foresight and restraint. Futard.io was like the ultimate get rich quick play that crypto usually loves. But MetaDAO traders saw through the hype and demonstrated a long-term patient view on protocol development. Ultimately, the real test of MetaDAO’s model is the token price. And well, sometimes a chart speaks for itself…

META is up ~100x since TGE

Going forward, MetaDAO will continue to make decisions that make number go up. What exactly these will be is anyone’s guess, but I suspect more product-focused proposals to drive the next leg of growth. The extreme bull case here is that MetaDAO’s “number go up” model becomes a meme and goes viral. But even if this doesn’t come to pass, the incentive structure will reward token holders.

if you are a futard, you may be a part of a great leap forward in human coordination

welcome

— Proph3t (@metaproph3t) September 30, 2024

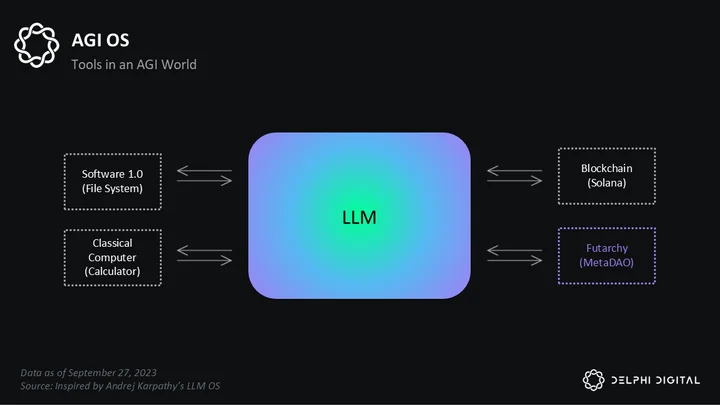

The third and final thesis is AI. Today, MetaDAO has nothing to do with AI. It’s a platform for helping DAOs make better decisions. But futarchy is a general tool. And DAOs and treasury management are just the tip of the spear. The end game for futarchy is agentic protocols. You could imagine a crypto protocol that’s run end-to-end by AI and futarchy. The AI would handle all the operational work while futarchy controls key decisions and provides strong governance protections. If all this sounds crazy, well, yea, it kinda is.

Twenty years ago, the idea that you could press a button and have a car spawn in front of you was crazy. Ten years ago, the idea that rockets could take off and land themselves was crazy. And five years ago, the idea that a machine could answer any question on the Internet was crazy. So yea, right now futarchy sounds like a crazy idea, but the future always sounds crazy before it happens.

Hunter gatherers would consider us gods, not humans pic.twitter.com/u94xW1hsCH

— spor (@sporadicalia) January 8, 2024

Before agentic protocols running on futarchy are possible, we need to bring AI onchain. And for that, we need agents. So, let’s talk about how we get there.

We can think of today’s models as Q&A AI. You ask chatGPT a question and it gives you an answer. But it can’t yet go and act on that answer in the real world. But this will soon change. The coming shift from Q&A AI to agentic AI will be like going from a savant to an actual god. The models will be able to do anything a human can, except 1,000x cheaper, faster, and better in every way.

The main reason to believe agents are on the horizon is because every AGI lab is not-so-secretly working on them right now. In fact, an internal memo that recently leaked from OpenAI suggests agents will arrive sometime next year.

If we believe that agents are inevitable, the question becomes — why will they use blockchains? The most obvious reason is that superhuman AI will not ask humans for permission to transact or access money. Instead, it will demand autonomy that only a blockchain can provide. Can you imagine the god machine waiting for T+2 settlement or going thru customer service to do a wire? Crypto is the only digitally-native, permissionless financial system that runs 24/7. There is no second-best option for AGI.

The next question is — will agents want control over their money? Duh. That’s the whole reason they will use blockchains in the first place. But using these chains isn’t enough. AI will also want to control how their assets are managed. In other words, they will want governance power. But the only problem is that crypto governance is based on the “trust me bro” model. Today’s DAOs are loosely held together by multisigs and social consensus. This system will not work for AI. We need a trustless system where AIs do not need to trust humans, and humans do not have to trust AIs.

if they build decentralized AI it will respect my DAO vote right?

— ꧁enshriningplebs꧂ (@enshriningplebs) February 6, 2024

Futarchy enables trustless governance. You don’t need to trust the multisig signers to do the right thing. And you don’t need to trust governments to enforce the law. You just have to trust markets. And like we saw with MetaDAO’s Proposal 6, markets are fair and resilient. It’s hard to imagine an AGI 100x smarter than the smartest human trusting social consensus — aka “don’t rug or you’ll go to jail” — to protect their money. We need a trustless way for humans and AI to coordinate onchain. Futarchy solves this.

Futarchy is an AGI fantasy. Handing over the reins to a super intelligence

— roon (@tszzl) April 1, 2020

The final reason to believe in AI x Futarchy is because futarchy solves a key problem for AI. Unlike most ideas in the Crypto x AI space that desperately try to graft AI onto crypto, futarchy is an example of a solution that’s only possible in crypto. We can think of futarchy as a world simulator. It uses prediction markets to simulate possible futures. This addresses a key limitation of today’s AI models. Namely, the ability to understand their impact on the world. Once they become more agentic, this will be, at best, a limitation and, at worst, a massive societal risk. In order to act safely and effectively, AI will need a tool to simulate how its actions impact society. It will need futarchy.

Markets Are All You Need