MetaMask Revenues, DEX Fee Competition, and Aggregator Wars

NOV 18, 2021 • 3 Min Read

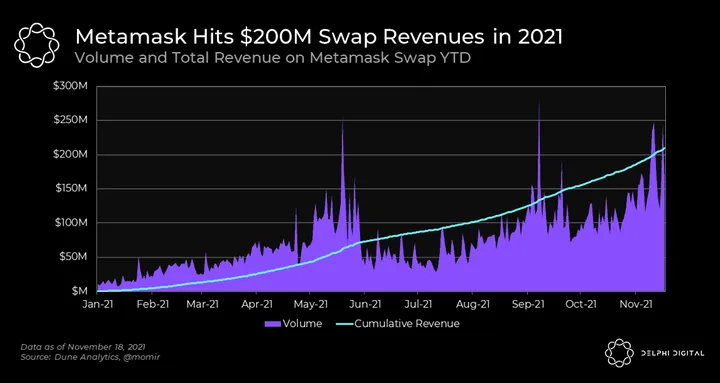

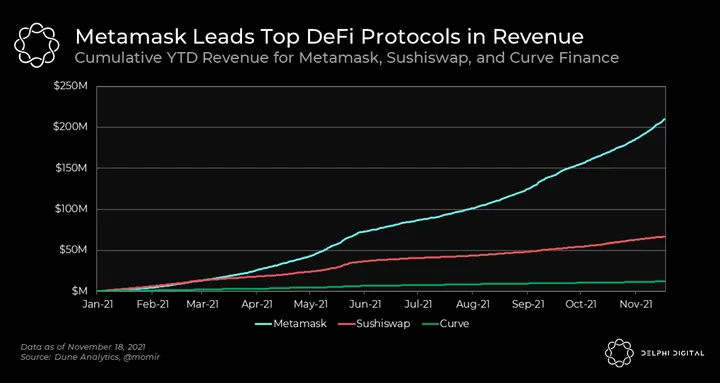

DeFi’s Secret Cash Flow Machine

- In Sept. 2020, Metamask announced its native swapping feature that gets quotes from multiple DEX aggregators to give users the best execution prices available on-chain. With this move, Metamask became an aggregator of aggregators — or a “meta” aggregator (pun intended).

- Metamask levies a 0.875% fee on each swap, which is exorbitant by DeFi standards. And this has resulted in over $200M in revenue over the last 11 months. The simple UX of swapping via the Metamask plug-in seems to trump the ludicrous fees the wallet charges for trades.

- If you don’t think $200M in revenue over 11 months is a remarkable feat — which you should — compare Metamask’s revenue to that of two of the top DEXes on Ethereum: Sushiswap and Curve. Sushiswap has made just under $70M YTD, while Curve sits around $12M.

- Now consider this: Metamask’s customer acquisition cost (CAC) is a big, fat zero. Metamask has no token incentives or emissions, so there’s virtually no cost to their revenue. Their profit margins are close to 100%. Imagine if they had a token.

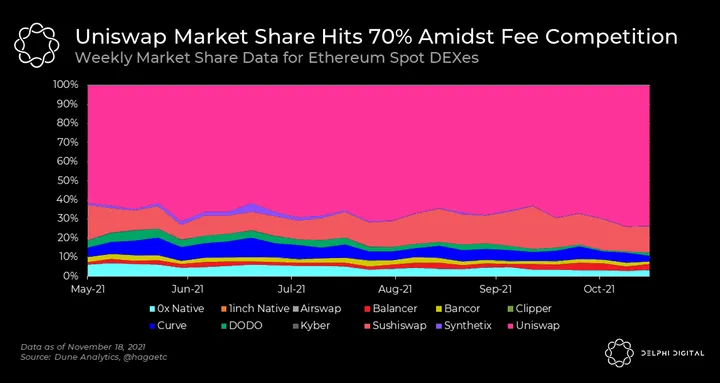

The (Fee) Race to the Bottom

- Uniswap’s market share among Ethereum spot DEXes hit a record high of 72%.

- The introduction of a new low-fee tier was a recent catalyst. On November 13, Uniswap launched its new 0.01% fee tier, making Uniswap’s stablecoin quotes among the most competitive in DeFi. As observers have pointed out, this likely marks the beginning of a fee-centric race to the bottom.

- On centralized exchanges, traders are always looking for ways to move into a lower fee bracket. Trading fees on Binance and FTX are far lower than on DEXes. As liquidity in the space grows and attracts serious players, DeFi’s evolution into a fee-competitive market is inevitable.

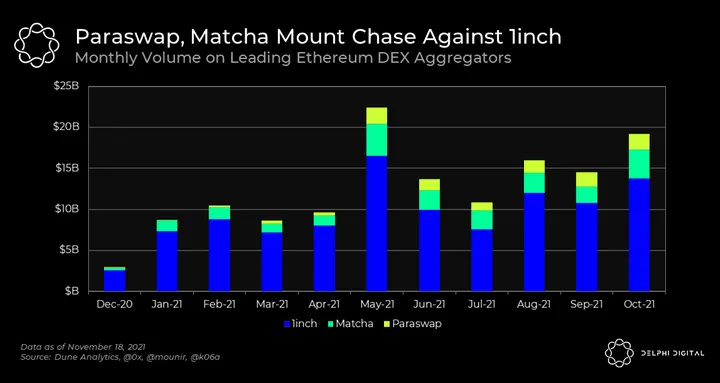

DEX Aggregator Wars

- 1inch is still the leading DEX aggregator by a large margin. However, competitors such as Matcha and Paraswap are starting to eat into its market share.

- 1inch had its second-best month ever in October, with $13.8B in volume. But Matcha and Paraswap — once-distant competitors — saw $3.5B and $2B in volume, respectively.

- Aggregators are a crucial piece in enhancing the UX of using DeFi-native liquidity. Watching how this shapes up is likely to be a key theme going forward.

- On the bright side, aggregator volume is back on the rise after a period of contraction in Q3. DEX volumes are on the same trajectory, and despite pathetic price action amongst DeFi majors, their fundamentals and usage are looking brighter than ever.

Notable Tweets

Terra’s grand entrance into crypto gaming

1/ Summoner’s War (50M+ downloads on Android alone) and other blockbuster IP by public gaming company Gameville is coming to @terra_money pic.twitter.com/lQbNmAn34x

— Do Kwon ? (@stablekwon) November 18, 2021

Some perspective on leverage for the friendly apes

mini-thread on managing leverage

I regularly run accounts at 3-8x leverage, not to over-size but to reduce the amount I have to keep on exchanges

but this means a bit of extra management. While trades might be sized properly, it’s important to consider liquidation risk

— David Holt (@IDrawCharts) November 18, 2021

A new bill to undo the mess in the Infrastructure bill

GM! Some good news: A comprehensive bipartisan bill has just been introduced in the House to fix EVERYTHING wrong with the infrastructure bill’s crypto tax provision–including the unconstitutional §6050I individual reporting mandate. https://t.co/rK3sbIKBu9

— Jerry Brito (@jerrybrito) November 18, 2021

0 Comments