TLDR: Mirror Finance is a new synthetic asset protocol built on top of the Terra blockchain, with both sharing the same founder, Do Kwon. While Mirror ($MIR) is attracting much of the attention right now, we’ve pursued a different strategy by investing in Terra ($LUNA). We believe Mirror, while potentially valuable in its own right, is a bootstrapping strategy for Terra, and the LUNA token stands to benefit the most from its growth.

Terra is an application-specific chain built using Cosmos SDK and relies on Tendermint for PoS consensus, similar to THORChain. This enables Terra to be optimized for its specific use case, facilitating cheap transactions with high-throughput, while also having good functionality in terms of interoperability.

What makes Terra unique is that it has multiple fiat-pegged, algorithmic stablecoins incorporated natively into the network’s economic design. $LUNA, Terra’s native token, is used to both stake the network and collateralize the algorithmic stablecoins. The latter point being similar to how FXS collateralizes the price of FRAX. Let’s explain the elastic supply and price stability mechanics using UST (TerraUSD) as an example:

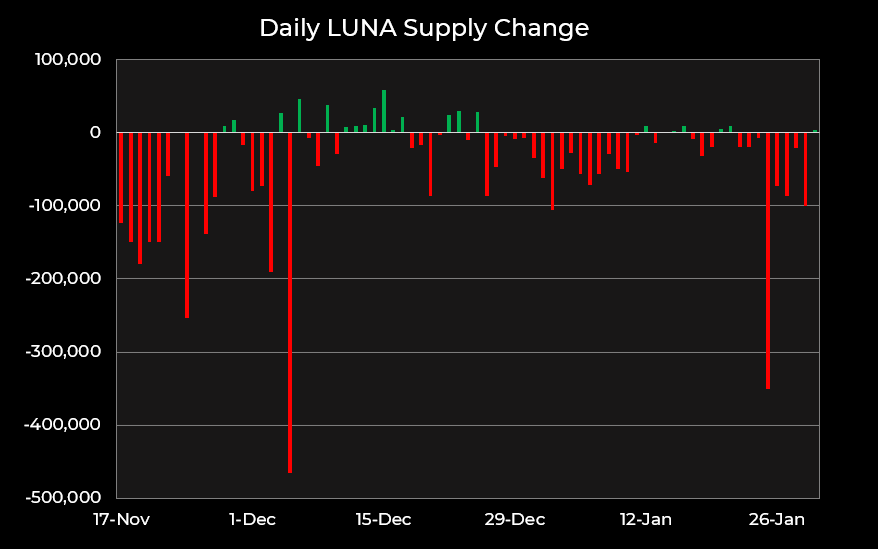

Expansion: If demand causes the market price of UST >$1, arbitrageurs can burn $1 of LUNA to mint 1 UST, which can then be sold spot at the higher price for a riskless profit. Spot selling drives UST price back to its $1 peg, while minting expands UST supply. This process reduces the LUNA supply which is value-accretive to the network’s stakers.

Contraction: If demand causes the market price of UST <$1, arbitrageurs can buy UST spot and redeem it at par value (i.e. $1) for newly minted LUNA. Spot buying drives UST price back to its $1 peg, while redemptions contract the UST supply. This process increases the LUNA supply which is value-dilutive to the network’s stakers.

The explanation above is overly simplified to make it easier to understand. In actuality, because Terra has multiple fiat-pegged stablecoins, this process actually works using a basket of their currencies, which they refer to as TerraSDR or “SDT”. This is modeled after the IMF’s SDR and is valued a similar way. The exact workings of the SDR are beyond the scope of this report, for the sake of timeliness, but here are the main takeaways. At launch, there were 1 billion SDT and 1 billion LUNA issued, both of which currently compete for seinorage rewards from stablecoin supply growth. When an expansion happens and SDT is available, the team uses the seinorage rewards from burning SDT, converts it into fiat, and keeps it in reserve to help defend the peg if necessary, in addition to using it for fiat transaction settlement. Each year in May, 100m SDT vest. Importantly, the entire amount of vested SDT was just used up a few days ago, due to the growth experienced from Mirror’s launch. The current total supply of SDT is sitting at ~800m, but that entire amount is locked / unvested, which means LUNA will be the primary beneficiary of stablecoin growth on Terra, at least until May.

Base layer protocols typically use inflation to incentivize people to run their networks in the early days. The plan being that their reliance on inflation can gradually decrease over time as adoption and utility reach a point where transaction fees can generate most, if not all, of the mining/staking rewards. Terra takes a different, somewhat ingenious approach, to the design and bootstrapping of its network. The proliferation of stablecoins on Ethereum has proven to be a massive boon for the networks utility, with stablecoins now acting as the preferred medium of exchange on the network, alongside ETH. However, Ethereum lacks a native stablecoin of its own, instead relying on what the market builds on top of it. In contrast to this, Terra utilizes the inflation of its staking token (LUNA) to collateralize a set of algorithmic stablecoins, which in turn increase the utility of Terra’s network. This could be a much more effective strategy for utilizing inflation rewards and bootstrapping utility.

Terra’s ability to accrue value from its suite of algorithmic stablecoins could be significantly higher than similar stablecoin projects deployed entirely on Ethereum because it doesn’t solely rely on seigniorage rewards. When an individual transacts with stablecoins on Ethereum, it’s the miners of that network which earn the transaction fees rather than the stablecoin protocol itself. With Terra, the network’s stakers receive the full benefit of fees derived from the stablecoin velocity they help facilitate and support. At scale this could prove to be a sizable value stream. In addition, Ethereum’s base layer lacks the transactional throughput for such algorithmic stablecoins to truly scale adoption in the first place, perhaps making their efforts at maintaining stability futile. For perspective, Terra can achieve ~2,500 TPS relative to Ethereum’s ~14 TPS currently.

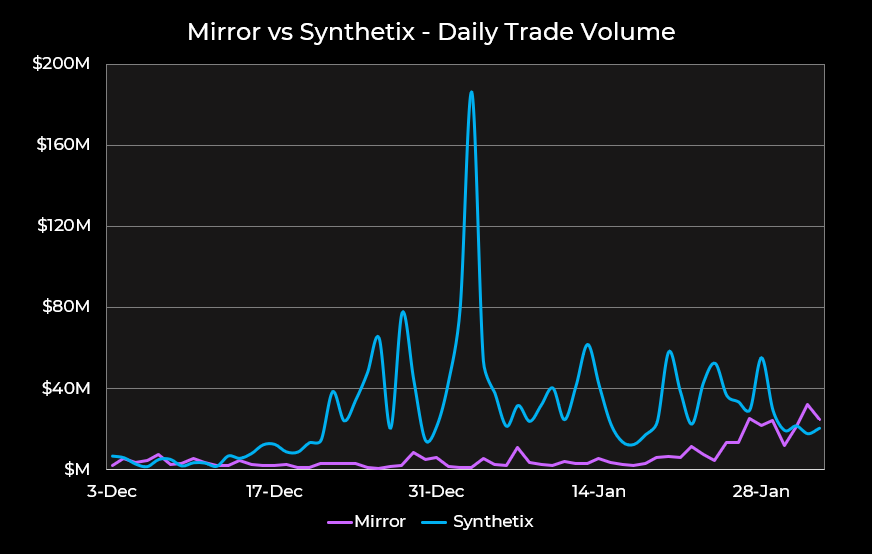

Terra’s value accrual isn’t solely limited to stablecoin growth and velocity, it also benefits from new applications being deployed on top of it. Let’s talk about Mirror, which just passed Synthetix in daily trade volume for the first time.

Mirror Finance is similar to Synthetix in that they both facilitate the creation and trading of synthetic assets (“mAssets” in Mirror’s nomenclature). However, there are a few key differences between Mirror’s mechanics and how Synthetix has historically worked up until this point. We should note that Synthetix is currently undergoing modifications that will make it more similar to Mirror in certain regards.

Minting a synthetic asset (“mAsset”) using Mirror entails opening a collateralized debt position (“CDP”), similar to Maker. To mint a mAsset, an individual can either lock up Terra stablecoins or other mAssets as collateral. There is a minimum collateralization ratio of 150% and falling below this threshold will trigger a liquidation to keep Mirror solvent. If a trader mints and sells a mAsset they are effectively taking a short position on that asset. This is because they will need to purchase that asset back later on the open market to close out their position and retrieve the collateral they’ve posted. If the asset falls in price over that time, they’re in profit (and vice versa). An individual could also mint a mAsset and hold the exposure but, in the absence of any temporary yield farming incentives, this would be pointless and cost the minter a 1.5% fee when they eventually close their position.

The 1.5% protocol fee taken when people close their CDPs is the main value driver for the MIR token at this stage, in addition to its governance power over new asset listings. These protocol fees are collected, converted into UST and used to purchase MIR, which is then distributed to MIR stakers.

Scaling the mAsset supply could face headwinds, because growth is dependent on individuals wanting to go short those assets. If we look at the supply of inverse synths on Synthetix, relative to long synths, this fear is seemingly justified. However, if there is strong demand for mAssets within the crypto markets, to a point where they trade at a premium relative to the underlying asset’s actual market price, sophisticated investors may be tempted to step in, mint and trade them back to parity. Let’s use a real example to explain what we mean. At the time of writing, the oracle price for mTSLA is $838.2 UST, while the TerraSwap market price is $907.68. An individual could mint mTSLA at $838.2 UST and sell it on the open market at $907.68. This act would scale the mAsset supply while the sell pressure would help drive mTSLA back to parity with the oracle price. This strategy has its risks though, as the mTSLA market price could continue to rise regardless, putting the short seller underwater, even if they should be in profit based on the oracle price. We’re currently having conversations with the Terra development team on ways to improve this process.

For those familiar with Synthetix, the process outlined above has some notable differences from it. To start, there aren’t distinct long and short (i.e. inverse) synths. If a person wants to go long, they simply buy the mAsset on the open market. If a person wants to go short, they mint and sell. You also don’t need to use $MIR to mint mAssets like you do with $SNX for their synths. By letting people collateralize their synthetic positions with Terra stablecoins, the risk profile of minting is much safer, requiring a lower collateralization ratio. The liquidation threshold for Mirror’s collateralization ratio is 150% while Synthetix’s is 200%. That may not seem like a massive difference at a glance but consider this. For Synthetix, if a minter/staker falls below the target collateralization ratio of 500%, they are unable to claim their rewards. Since most Synthetix minters are there for the rewards in the first place, this results in Synthetix having a current active collateralization ratio of 627% vs Mirror’s 199%. As the data shows, Mirror has much better capital efficiency which is made possible by the price stable collateral it accepts.

Another key difference to consider is that Synthetix co-mingles all of the minters’ debt into a single pool, whereas Mirror silos debt through its CDP-based system. Why does this matter? Earlier we mentioned that if you mint a mAsset just to hold it, you’re going to end up being flat on the position, net the 1.5% protocol fee to close out. With Synthetix, however, you can mint synth exposure, hold it and still find yourself underwater based that asset’s performance relative to the overall system debt pool. As we explained in our Synthetix report from August 2019, when you stake your SNX you’re effectively taking the other side on the protocol’s net directional exposure. For example, let’s say you mint sUSD and sit in it during a bull market. As asset prices rise higher, the price of their respective synths follows suit. If the value of all the other long synths increased by 3x, then the system’s debt pool would ~3x with it. This means that the person who minted and sat in stable exposure, in addition to those who held inverse synths, are the people paying out to the bulls. It’s a zero sum game, always has been.

Now, there are a few design changes that fix this which the Synthetix developers are already working on. The ideal exposure for Synthetix as a platform is to be market neutral across their book. This means that longs and shorts would balance each other out so that SNX stakers aren’t at risk when there is an imbalance. To the best of my knowledge, Synthetix has never been market neutral since launch, with overall exposure typically skewing net long by a wide margin. The reason why is because there was never a mechanic at play which attached a cost to the minters/traders who make it imbalanced, such as a funding rate. SIP-80 changes this by finally incorporating one. If a funding rate forces market neutral exposure where longs pay shorts and vice versa, then the risk profile for staking SNX falls dramatically, as should any collateral ratios associated with it. This would drastically improve the platform’s capital efficiency. We should also note that in Synthetix’s 2021 roadmap, Kain signaled the development team’s intent to move towards siloed debt pools and open interest caps, which could further help.

How the synthetic assets are traded and who accrues value from the volume are also important, but nuanced, aspects to understanding both Mirror and Synthetix relative to each other. Trading Mirror’s mAssets takes place on a Uniswap-inspired AMM deployed on the Terra blockchain called Terraswap. Trading fees on Terraswap are 0.30%, again similar to Uniswap, which are paid to liquidity providers. The lack of a trading fee captured by Mirror means it does not directly accrue value from derivatives trade volume the same way that Synthetix can, depending on where the synth is traded. There is another type of fee taken, however, which is why it’s always important to read the fine print. Because Terraswap is deployed on Terra, trading on it is subject to the network’s “tax” when one of its algorithmic stablecoins is involved. Currently, this tax is equivalent to 0.607%, but is capped at 1 SDT*, and accrues to LUNA stakers. At scale, capturing this type of fee on mAsset trades could drive a significant amount of value to LUNA stakers and the Terra network. One caveat of using a Uniswap-inspired AMM for trading mAssets is that price slippage becomes a concern depending on the trade’s size relative to the size of the liquidity pool. A strength of Synthetix is that trading synths on their exchange never resulted in slippage, even on large orders. The reason being is that there isn’t any “trading” happening in the sense that most people typically think of it. Rather, trading on Synthetix exchange was always just the protocol internally adjusting the derivatives exposure you’d be subject to moving forward.

Currently, traders can experience significant slippage due to a supply shortage of UST on exchanges, such as Curve’s UST MetaPool. Jump Trading recently put forward a proposal to improve on-chain liquidity, which will be implemented on February 8th.

Time to pull this all together and synthesize our thesis for Terra moving forward. An aspect of Synthetix that we, and apparently the market, always appreciated was the positive reflexivity of its design mechanics. Again, going back to our old Synthetix report, we explained it as follows – “Synthetix’s design can facilitate a positive feedback loop. Higher trade volumes lead to more trading fees, which should fundamentally lead to a higher SNX price, which then allows for more Synths to be minted, which can then lead to higher trade volumes. This dynamic could play an important role in helping to bootstrap the network”. Now, in Mirror’s case, there are no trading fees being captured by it and the value of the MIR token does not directly impact the amount of mAssets that can be minted. LUNA does, I’ll explain. The total value of mAssets can only grow if the collateral they use grows in value too. mAssets, either directly or indirectly, rely on the supply of Terra’s algorithmic stablecoins to use as collateral. As demand for Mirror drives demand for Terra’s stablecoins, supply expansions for them will be triggered which results in a contracting LUNA supply. This is value-accretive to LUNA stakers. In addition, as trading volume for mAssets increases on Terraswap, so will the tax revenue derived from the fee levied on those transactions. This is value-accretive for LUNA stakers. Furthermore, as the now increased stablecoin supplies are used for cheap and fast payments, made possible through the scalability of Terra’s Cosmos/Tendermint-based chain, more gas fees will be generated. Again, this is value-accretive for LUNA stakers. In summation, LUNA stands to benefit from fees derived from stablecoin payments, derivatives trading, a multi-fiat forex market emerging amongst its various algorithmic stablecoins, as well from the seigniorage rewards reflected in a contracting LUNA supply as the network’s stablecoins continue to grow. Terra’s founder, Do Kwon, didn’t launch Mirror just to compete with Synthetix. He launched it to help bootstrap Terra.

Other Points:

Mirror’s token distribution and launch strategy is currently offering attractive yields on unique exposure, across both the Terra and Ethereum blockchains. Individuals can provide liquidity on mAssets & UST in TerraSwap or Uniswap, and stake their LP share tokens. On Terra, these APYs average ~300% while on Ethereum APYs are ~500%. The ability to have exposure to Netflix stock and stablecoins, while earning triple digit yields could certainly be appealing to a wideset of people in crypto already, but also to people not yet familiar with crypto. This could be particularly true given the attractiveness of permissionless trading in the wake of the GameStop/Reddit fiasco. There’s also the opportunity to earn MIR rewards from staking LUNA to run the Terra network. More details on the distribution can be found here.

Anchor is another promising project, built on Terra, which is set to launch soon. On the supply side, the protocol is going to accept staked PoS tokens from many different protocols as collateral (Ethereum, Terra, Solana, etc…); thus, the interest rate depositors will be accruing is a combination of all the staking rewards from these networks (which can potentially be more stable than the current leverage-driven rates observed throughout DeFi). On the demand side, the protocol is going to encourage (and facilitate) different applications (think fintech) to connect to their API, with the intent to reach a larger mainstream market. On the backend, Anchor will be using Terra stablecoins, further incentivizing demand for their native assets.

Chai was the first app to be built on top of Terra. It’s a payments app built by the Terra team mainly catering to the Korean market (up until now). It’s currently facilitating ~$1.5B in annualized transaction volume and has activated ~2.5M users in Korea. The more Chai grows, the more demand there is for Terra stablecoins and the more value accrues to LUNA.

In January of this year, Terra raised $25m from prominent investors such as Galaxy Digital, Pantera and Coinbase Ventures. In December of 2020, SoftBank and Hanwha, along with others, invested $60m in a Series B financing round into CHAI, the payments app built on top of Terra.

By the end of last year, Terra added support for CosmWasm – a generalized and battle tested smart contracts engine. The addition of CosmWasm now allows anyone to build native and trustless apps on top of Terra. These new capabilities are what allowed Terra to build Mirror and Anchor, but most importantly they will allow anyone to build on top of Terra.

Terra will be transitioning into a DAO this year with the objective to further decentralize the project. This will create a better environment for new projects to spin up around the Terra ecosystem as decisions will no longer be centralized around Terraform Labs and will also bring more transparency to the funds currently being held by the project.

Mirror already has a sizable treasury at its disposal, as it was funded with 36.6M MIR (~$168M USD) as part of the initial MIR airdrop. We expect some of this treasury to be used to fund development on top of Mirror going forward. Notably, Do Kwon (founder of Terra) has hinted at proposing a user farming framework to incentivize developers who bring new users to the platform using these funds.

Terra currently has a bridge to Ethereum active called Shuttle, which Mirror is utilizing to move its mAssets back and forth between chains. While detailed information is scarce on it, when we asked Terra’s team they confirmed Shuttle was a fully centralized solution that would only be used over the near-term. On the topic of interoperability, Terra, as a Cosmos/Tendermint chain, will also leverage IBC for cross-chain communications. Given how new IBC is, it will probably take a few months of battle testing it before it sees significant usage by Terra.

0 Comments