Opyn Squeeth Doubles, Concentrator IFO, Uniswap vs. Curve

JUL 20, 2022 • 7 Min Read

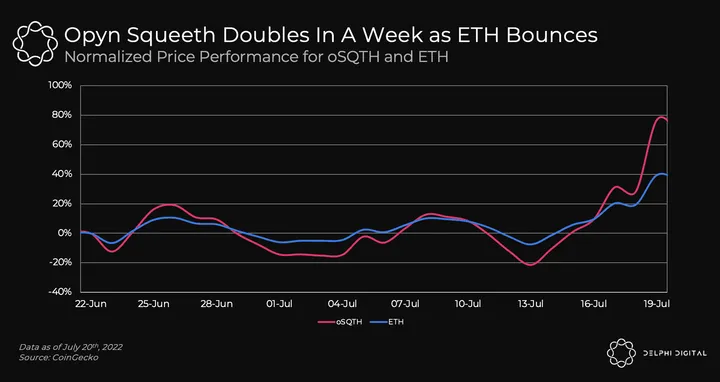

Chart of The Day: Opyn Squeeth Doubles In A Week as ETH Bounces

- Over the past week, ETH has gained 48% from $1,041 to $1,543 as the broader market experiences a relief rally. Over the same period, oSQTH has doubled in value and gained 117% from $62 to $135.

- Opyn Squeeth (oSQTH) is a new financial primitive that tracks the price of ETH squared. Squeeth works like a power perpetual, using an index price and funding rate to ensure that the contract trades at equilibrium price.

- Opyn Squeeth is an ERC-20 token, and users can simply buy oSQTH from the Uniswap v3 oSQTH / ETH pool. Users can also mint oSQTH by providing ETH as collateral to Opyn.

- Long Squeeth provides exposure to pure convexity, offering an asymmetric payoff with a higher upside and lower downside. As indicated in the chart above, oSQTH makes more when ETH goes up, while it loses less when ETH goes down.

- However, long Squeeth holders pay a high funding rate to maintain this asymmetric payoff. Therefore, holding Squeeth over extended periods during sideways and bear markets may cause a loss in exposure to ETH squared.

- For more on Opyn Squeeth, Delphi members can read a Delphi Pro report here.

Initial Farm Offerings, Optimism Pools and Retroactive Airdrops

[Excerpt from a Delphi Insights report]

- Concentrator by AladdinDAO extends the Curve/Convex ecosystem by helping Convex farmers earn up to 50% more with less hassle and less gas fees. Yields from multiple Convex pools are sold to buy cvxCRV, which is staked to earn maximum rewards while still maintaining exposure to the Curve/Convex ecosystem.

- Rather than buying more of the deposited token, Concentrator helps farmers accumulate yields from multiple Convex vaults into cvxCRV. The resulting rewards from staking cvxCRV are auto-compounded to grow those returns even more. When it’s time to withdraw, users can choose from cxvCRV, CRV, CVX or ETH.

- Yield calculations can be found here. To access Ethereum, you’ll need to configure your MetaMask to run Ethereum’s Mainnet.

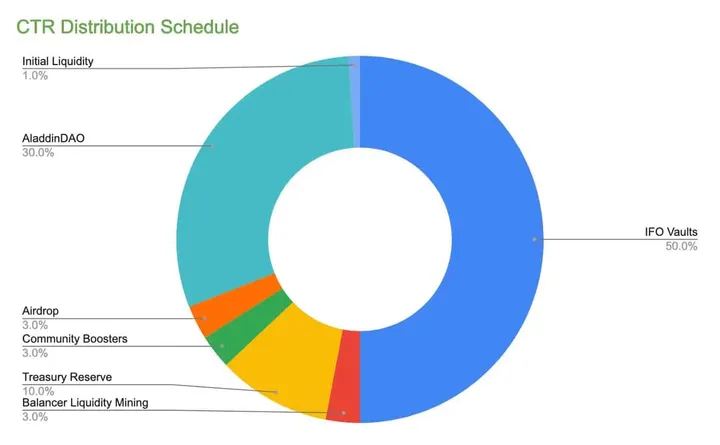

- Tokenomics:

- Total Supply: 5M CTR tokens

- 50% of the token supply (2.5M CTR) is reserved for IFO Vaults and distributed to IFO farmers.

- 3% of the token supply (150K CTR) is reserved for the Balancer Liquidity Mining program.

- Notable Unlocks:

- 30% of the token supply (1.5M CTR) is reserved for AladdinDAO, and does not have any lockups. However, Aladdin has vouched to instantly lock the entire allocation for the maximum duration (4 years) and continuously re-lock those tokens.

- 3% of the token supply (150K CTR) is reserved for an Airdrop that is yet to be distributed.

- 10% of the token supply (500K CTR) is reserved for the Treasury and does not have any lockups.

- veCTR: CTR tokenomics work the same way as Curve’s ve tokenomics. CTR holders will be able to lock their tokens for up to 4 years to get veCTR. The -ve power will be determined by the amount locked and the remaining lock time.

- Locking CTR to get veCTR will be available within a few weeks of the IFO period. Users will be able to lock their CTR and begin directing and/or receiving platform revenue.

- How does it work?: Farmers deposit their Curve LP tokens in Concentrator. These LP tokens are staked in Convex vaults. Yields from those vaults are harvested, swapped into CRV and then staked on behalf of the farmer in the Convex CRV vault where they auto-compound. Users may withdraw any or all of their deposits and yield at any time in cvxCRV, CRV, CVX or ETH.

- For more information, Delphi members can see read the full Delphi Insights report here.

Uniswap vs Curve: Which Is the Best DEX?

[Excerpt from a Delphi Pro report]

- Uniswap and Curve are two of the largest exchanges within all of crypto. While the two were not always competitors, Curve’s foray into unpegged assets and Uniswap’s move to drop fees for stablecoin trades have turned the two into rivals.

- With v3, Uniswap moved away from its popular constant product (XYK) liquidity curve to a more dynamic model where LPs decide what price range they want to provide liquidity in. The concept came to be known as “concentrated liquidity,” as it effectively allowed LPs to compress their liquidity curve inside a tighter band.

- As a rebuttal, Curve launched its v2 – a similar answer with a different approach. Curve v2 also relies on concentrated liquidity. Except, unlike Uniswap, LPs don’t choose their liquidity range – Curve’s market making algorithm does, enabling a passive LP experience.

- In this piece, we seek to examine Uniswap v3 and Curve v2 with the goal of answering a very important question: can Curve’s passive LP experience offer competitive price execution relative to Uniswap v3’s actively managed liquidity?

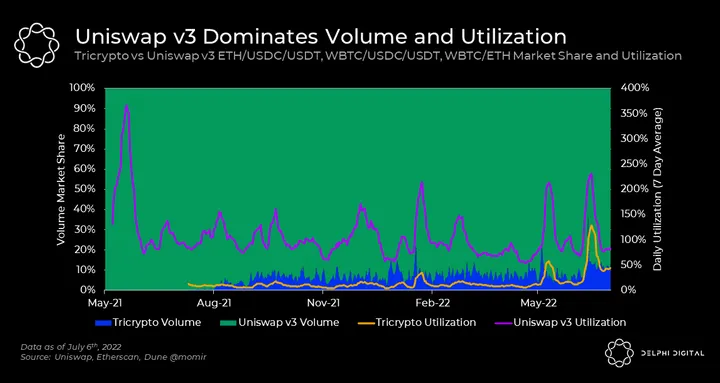

- At the moment, Uniswap holds just under 90% market share on ETH and WBTC volume. As a result, it’s been able to attract significantly more liquidity utilization (volume/TVL) than Curve’s Tricrypto (a Curve v2 pool made up of ETH, WBTC, USDT).

- Now that we understand the basics and have a sense of who’s leading this market, let’s take a look at how Curve v2 and Uniswap v3 work. Following this, we’ll get to the more interesting stuff. Namely, what the data tells us about Tricrypto’s chance of growing its market share.

- As mentioned earlier in this post, Uniswap v3 is the latest iteration of the product, launched on May 5, 2021. The third iteration of Uniswap introduced two improvements that changed the entire DEX landscape:

- Concentrated liquidity – A novel mechanism that allows LPs to manage positions by providing capital in specific price ranges. Contrast this to Uniswap v2, where LPs provided liquidity in a near infinite price range. The benefit of concentrated liquidity is that it allows LPs to express a specific view on the market. It further aids LPs by generating more fees with less capital whenever liquidity is in range (again, in comparison to v2). The downside is that this concentration of liquidity amplifies impermanent losses and requires LPs to actively manage their ranges.

- Customizable fee tiers – While Uniswap v2’s fees are fixed at 30 bps, Uniswap v3 allows for pools with different fee tiers. Lower fee tiers (1 bps and 5 bps) combined with liquidity concentration are good for things like stablecoins and have allowed Uniswap v3 to steal significant stablecoin volume share from Curve. Higher fee tiers (1%) are better for long-tail assets, helping compensate liquidity providers for volatility and thus the impermanent loss risk they take on.

- For more information, Delphi members can read the full Delphi Pro report here.

Notable Tweets

Comparing Decentralized Perpetual Exchanges

/1 The battle⚔️ of Perpetual DEXes has begun.

Decentralized perpetual exchanges are a trending topic right now. 🔥

So I decided to compare the most popular ones:

@dYdX

@GMX_IO

@GainsNetwork_io

Join me for a 🧵 to find out more about their Pros and Cons 👇

— The DeFi Investor (@TheDeFinvestor) July 19, 2022

Insurance For Pegged Assets with Y2K Finance

Is @y2kfinance the product we needed 3 months ago?

Here’s a thread to break down the in/outs of a project attempting to position itself as a critical mechanism in an ever-growing stablecoin market.

🧵👇…

— Minerva (@0xMinerva) July 19, 2022

250+ Projects Across Different NFT Verticals

1/ Put together a list of 250+ projects across different NFT verticals

It’s time to pay attention to the building blocks that will set the foundation for the next wave of users 👇

— Alex Gedevani 🇫🇷 (@alexgedevani) July 20, 2022

0 Comments