Paradex: Reimagining On‑Chain Markets from First Principles

Imagine sitting at a poker table where your opponent gets a free last look at your cards before deciding to call or fold. You’d never agree to such a game, yet that’s effectively how many on-chain exchanges operate today. And oftentimes, these are the exchanges we all rave about, such as Hyperliquid. In the current decentralized perps markets, high-speed market makers enjoy a “free last look” at your trades, canceling their orders last-second if the trade would be unprofitable for them. It’s as if the house never loses – and you’re not the house. This structural imbalance is invisible to most users (the UI feels fast, after all), but it shows up in subtle ways: ever notice how you’re instantly down a percent or two after a perp trade on some DEXs? That’s your opponent peeking at your hand. Paradex’s core thesis is that they can build a better game, one where trading is fair by design, not by how fast you are. After all, isn’t the point of crypto to level the playfield to give the little guy a shot?

Two Roads for On-Chain Exchanges

We’re seeing two divergent philosophies in the race to build high-performance on-chain exchanges:

- Camp A: Recreate TradFi Microstructure on-chain (cancel priority). This camp, exemplified by projects like Hyperliquid (and some Solana-based DEXs), mimics centralized exchange mechanics as closely as possible. It means ultra-low latency networking, matching engines with strict price-time priority, and tricks like cancel-priority or speed bumps to protect market makers. Essentially, they bring the NASDAQ playbook on-chain, even if it requires custom sequencers or semi-centralized infrastructure to achieve speed. Hyperliquid, for instance, uses custom block building logic that prioritizes cancels over GTC and IOC orders. This gives makers confidence to quote tighter and gives takers the illusion of immediacy. It feels snappy: takers usually get filled if liquidity is shown, and makers feel safer quoting. But this is essentially a patch over a deeper issue. Cancel-priority is a double-edged sword: it cuts down on outright sniping of makers, yet it grants makers a perpetual option for a “free last look” to never trade at a loss (they can always cancel if the market moves against them). In other words, it’s like the house always getting to peek at your hand and fold when it’s not in their favor. Makers will indeed show tight prices on the screen, but as a taker you’ll rarely get those nice prices, the moment your trade would be a great deal for you, the maker cancels. What remains is slippage: the delta between the price you see and the price you get filled at, because makers were able to pull their quotes before you can get filled. This dynamic leads to a cat-and-mouse latency game: quote tight, get pinged by a fast taker, cancel, repost, repeat. It produces cancel spam, flickering quotes, and ultimately wider effective spreads for any participants who aren’t algos. It’s a high-speed game that works well for HFT firms but leaves normal users at a disadvantage. Camp A’s ethos is essentially “if it ain’t broke, don’t fix it”, copy traditional market structure to on-chain, even if that means running a semi-centralized fast path. This model also might not scale well as block-times reduce as your time to cancel advantage is eroded.

- Camp B: Rethink the exchange from first principles for the crypto context. This is Paradex’s camp. Instead of assuming the traditional model is optimal, Paradex is redesigning the playing field itself by embracing crypto’s unique strengths: on-chain validity proofs for trustless execution, protocol-level privacy, and new order types like RPI and supplementary execution protocols like RFQ to execute large and complex trades with atomic leg execution. This first principles approach changes the game to make it fairer for a broader range of participants. This camp acknowledges that blockchains are not NASDAQ and shouldn’t try to be; they have different constraints and superpowers. By using cryptography and thoughtful design, Paradex avoids the latency arms race altogether and eliminates the “free last look” option. The idea is to bake fairness into the protocol, rather than relying on centralized speed or bandaid rules. Paradex’s approach is admittedly more radical and involves more execution risk, but it aims to unlock a new wave of users, especially institutions, who have so far avoided DeFi due to issues like toxic flow and lack of privacy. Wall Street doesn’t just need fast execution, they need trustworthy execution and the ability to trade without broadcasting their hand to the entire world.

Both camps ultimately want to attract real trading volume on-chain. But I’m convinced Camp B’s approach is more likely to unlock the next wave of adopters, especially institutional players who have so far dabbled in CeFi but largely avoided DeFi. Why? Because Wall Street doesn’t just need fast execution; it needs trustworthy execution and privacy. A paradigm that offers deterministic trade finality, privacy for large orders, and protection against toxic flow is more appealing to an institution than one that says “we’re just like your current exchange, except running on a potentially unstable blockchain, favoring whoever has the fastest bot, and we won’t make you KYX/AML.” Paradex’s bet is that a slightly different design, one that breaks from TradFi orthodoxy in key areas, will ultimately win the confidence of traders who want to do size on-chain without fear. It’s a different road to the same goal: trustworthy finality for the pros, and a fairer playing field for the rest of us.

With that context, let’s dive into the core first principles that Paradex has built around, and how each principle translates into concrete features and advantages.

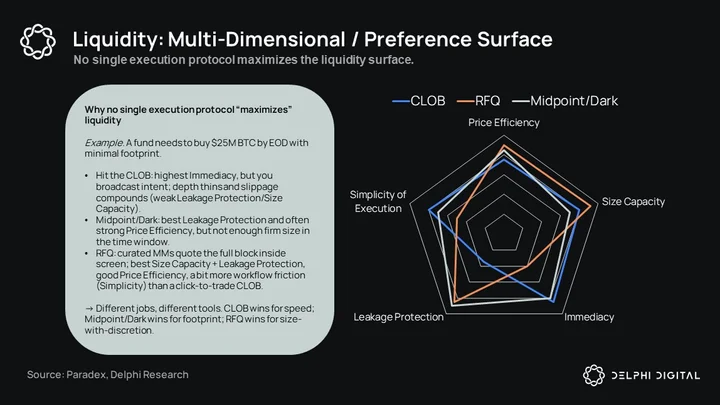

Principle #1: Liquidity is a System, Not a Number

Paradex’s signature design innovation is how it handles trade flow. It starts by asking a simple question: what if we made that “last free look” high-speed game mostly irrelevant? Instead of spending engineering effort on who wins the cancel-vs-taker race (a race that inherently rewards speed and hurts retail traders), Paradex tries to make the race itself matter less in the first place. It does this with two complementary mechanisms, Retail Price Improvement (RPI) and Request-for-Quote (RFQ), which fundamentally alter how liquidity is shared and consumed on the exchange.

This visual isn’t perfect, but it is how Paradex thinks about liquidity and its surface. Once I was able to picture liquidity as a surface, it became clear that liquidity was indeed not a number.

From Anand, CEO of Paradex/Paradigm, “We’ve always thought of liquidity as an n-dimensional vector in a tradeoff space. This completely changes how you think about building a marketplace. In this world, execution sits on a frontier where CLOBs, RFQs, and dark pools (execution protocols) each optimize for different axes – price, size, immediacy, info-leakage risk, execution complexity. You can slide along this frontier, but you can’t max every dimension at once (like the blockchain trilemma). That also means, there is no perfect venue or protocol…….just as there is no perfect blockchain. Only fit-for-purpose protocols and chains. Rational traders choose the microstructure that best matches their objective function and constraints for a given asset, instrument, or strategy.”

We’ve always thought of liquidity as an n-dimensional vector in a tradeoff space. This completely changes how you think about building a marketplace. In this world, execution sits on a frontier where CLOBs, RFQs, and dark pools (execution protocols) each optimize for different… https://t.co/9a6ssXKLLr

— fiddy.dime – priv/acc (@fiddybps1) September 4, 2025

This idea of sliding along this pareto frontier is what is important as you shift your preferences as a trader.

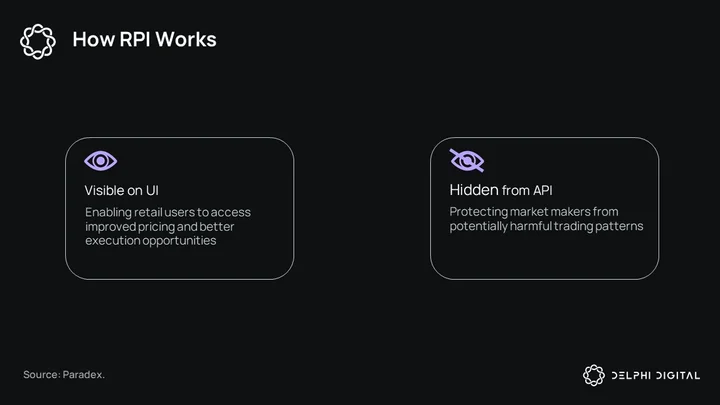

Retail Price Improvement

Retail Price Improvement (RPI) is a UI-only price-improvement lane that gives retail traders better prices while insulating market makers from toxic/latency-arb flow. Makers flag their quotes as RPI, making them visible in the app but not via API. These orders are post-only and can only match with non-algorithmic (UI) orders; they never execute against API flow. Practically, this creates two views: an RPI Book (visible only in the UI) and an API Book (visible in both UI and API). UI traders see both; API participants see only the API Book. Because RPI quotes are shielded, makers can post tighter spreads and larger size. Combined with the low friction of zero Taker fees, UI traders naturally interact with top-of-book RPI quotes via simple market orders, delivering better prices, deeper size, and zero fees.

This flow segmentation via RPI allows for a unique business model that is oftentimes overlooked, payment for order flow (PFOF), but is often seen and discussed as zero-fee trading.

What is PFOF?

Payment for Order Flow is a system where a trading platform (broker or exchange) routes customer orders to specific market makers in exchange for a fee. In simple terms, instead of charging you a commission, the platform gets paid by a third-party market maker for the right to fill your order. This behind-the-scenes payment is what allows some platforms to advertise “free” or zero-fee trading, because someone else is footing the bill for trade execution. (If you’ve ever wondered how brokerages make money on 0% commission trades, PFOF is usually the answer.)

The next logical question is: why is this so important?

PFOF enables trading platforms to charge zero taker fees to users while still giving the platform a revenue stream. It

Read the full report

This report is part of Delphi Pro.

- 800+ Pro reports across every major sector

- Talk directly with our analysts

- Private community of funds and builders

Already a Pro member? Log in

0 Comments