Plasma: Stablecoin Infrastructure & The Trillion Dollar Opportunity

JUN 05, 2025 • 28 Min Read

Report Summary

Summary:

The report analyzes Plasma, a new blockchain ecosystem designed as a stablecoin-native chain—tailored specifically for high-volume, low-complexity USD₮ (Tether) transfers and payments. It argues that general-purpose blockchains (like Ethereum and Tron) are not optimized for stablecoin transfers at scale, and Plasma aims to become the global settlement and issuance layer for digital dollars.

Key Takeaways:

1. Why Plasma?

-

Stablecoins (especially USD₮) are the primary onchain asset by volume but are not well-served by general-purpose L1s.

-

Ethereum is too expensive for repetitive USD₮ transfers; Tron is efficient but has centralization concerns.

-

Plasma is purpose-built for predictable, low-cost, high-speed stablecoin activity.

2. The Case for a Stablecoin-Specific Chain

-

Plasma consolidates USD₮ liquidity and avoids fragmented cross-chain bridging risk.

-

Like Visa owning the payment rails, Plasma lets Tether vertically integrate issuance, settlement, and compliance.

-

This removes the overhead of deploying USD₮ across multiple execution environments.

3. Architecture & Features

-

PlasmaBFT Consensus: Optimized two-phase BFT consensus for high throughput and low-latency.

-

Bitcoin-Anchored Security: Periodic checkpoints to Bitcoin for finality and censorship resistance.

-

EVM Compatibility (via Reth): Full Ethereum compatibility for apps and yield protocols.

-

Zero-Fee USD₮ Transfers: Planned design to make basic USD₮ transfers free while monetizing DeFi-like services.

-

Shielded Transactions: Research-stage feature for privacy-preserving stablecoin payments.

4. Revenue Model & DeFi Flywheel

-

Plasma doesn’t charge for basic USD₮ transfers—its revenue comes from DeFi and business settlement services (FX, merchant payouts, yield, etc.).

-

Already secured partnerships:

-

Yellow Card (African stablecoin rails)

-

BiLira (TRYB bridge to Plasma)

-

Uranium Digital (physical uranium trading)

-

Axis (yield strategies)

-

Curve Finance & Ethena for deep stablecoin markets.

-

-

Positioning itself as the DeFi hub for all stablecoin-related economic activity.

5. Competitive Dynamics

-

Plasma threatens Tron directly: if Plasma captures even 30% of global USD₮ activity, Tron’s fees, blockspace demand, and TRX token utility could collapse.

-

Ethereum will see less direct impact—since DeFi (not transfers) is its main usage.

-

Other L1s (like Solana) could lose USD₮ flows if Plasma centralizes remittance and cross-border payment volumes.

6. The $1 Trillion TAM Opportunity

-

In 2024, stablecoins saw ~$5T in transaction volume, nearly 1/3 of Visa and Mastercard’s.

-

Plasma aims to unlock the full trillion-dollar+ stablecoin market, especially in emerging markets and remittances—where stablecoins are real financial lifelines.

Conclusion:

Plasma is not just another L1—it’s a purpose-built, vertically integrated stablecoin chain that positions USD₮ as the monetary base layer of the crypto economy. Its success would:

✅ Remove friction for stablecoin transfers.

✅ Boost Tether’s ecosystem dominance.

✅ Erode market share from Tron and other chains reliant on USD₮.

✅ Become the de facto global stablecoin settlement layer.If Plasma succeeds, it could redefine how remittances, payments, and DeFi are done onchain—especially in unbanked economies and emerging markets.

-

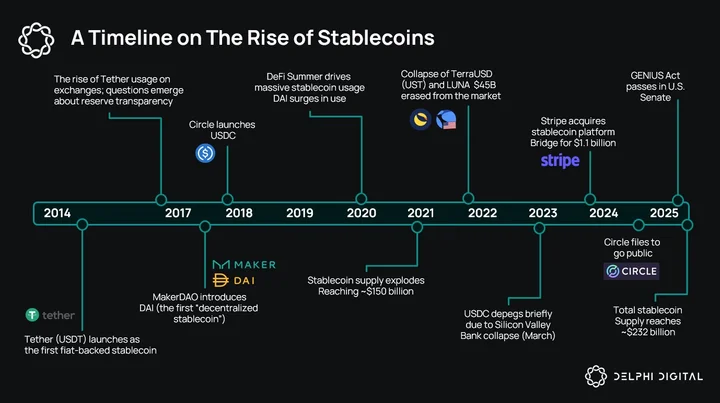

A Timeline on The Rise of Stablecoins

The early days of crypto were riddled with the inefficiencies and extreme volatility of not having proper stable assets onchain. During the early ICO era, nearly all trading pairs were denominated against either BTC or ETH. This meant one of two options for traders: trade into BTC and hope it doesn’t dump, or constantly off and on-ramp profits into a bank account.

Arguably, stablecoins found PMF as a response to the inherent volatility of crypto. Their promise was simple yet powerful: combine the advantages of crypto (programmability and speed) with the price stability of fiat currencies.

The first breakthrough in stablecoins came in 2014, with the launch of Tether (USD₮) originally on the Omni Layer. It wasn’t until post-2017 when Tether actually became the first widely adopted stablecoin pegged to the U.S. dollar, setting the standard for fiat-collateralized stablecoins. As crypto adoption increased, stablecoins became essential infrastructure for trading, arbitrage, and on/off ramps. Exchanges began listing USDT pairs for nearly all major crypto assets, and alternative stablecoins began emerging (Circle’s USDC, TrueUSD, etc.)

By 2020, stablecoins became a common onchain asset. Their utility would eventually extend into DeFi in the coming years as the primary unit of account, used for lending, borrowing, and yield farming. Soon, algorithmic & CDP-backed stablecoins (UST, DAI) would emerge, trying to achieve price stability without fiat backing, introducing new risk dynamics. These new risk dynamics would also lead to some of the largest blow-ups in the space (UST/LUNA).

Over the next two years the total stablecoin market would explode from ~$5 billion in 2020 to over ~$150 billion by the end of 2022, primarily dominated by USDT and USDC.

As of June 4, 2025, the total market cap of stablecoins has reached an ATH of $233.5 billion, with Tether maintaining a dominant market share of ~66%, equating to approximately $154.5 billion.

Despite the history of fud and allegations questioning the solvency of Tethers reserves (which were completely fair concerns early on given the opaque nature), it has continued to not only maintain its dominance but also grow year after year. It has consistently held the top position by market cap and transaction volume while becoming one of the most profitable companies to date.

Tether – An Anchor for the Stablecoin Economy

Tether’s rise to dominance has mirrored the rise of stablecoins themselves. It not only represents the largest stablecoin by market cap but is the de facto unit of account across much of crypto today. And much of its success has hinged on the adoption and need for a stable and accessible asset in the emerging global economy as well as countries plagued by hyperinflation. But this burst in demand in emerging markets has deepened Tethers liquidity as well, a win-win situation for both crypto natives and everyday stablecoin users.

Even as other stablecoins like USDC and DAI have grown, none have matched the scale, reach, or liquidity profile of Tether. It has presence across nearly every major chain, and its usage extends beyond crypto-native contexts into real-world payments and OTC settlements. Tether has even financed a $45M crude oil transaction between a publicly traded oil company and a commodity trader back in October, 2024 – suggesting that they have their sights on expanding beyond crypto and p2p payments.

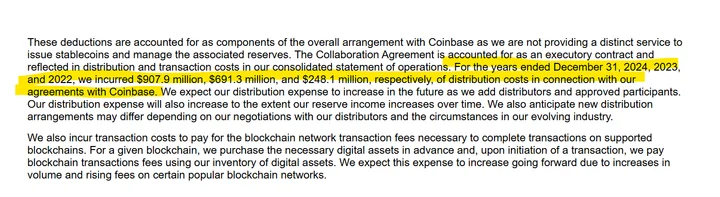

When it comes to its closest competitor, Circle’s USDC; Tether’s business model has proven to be far more profitable. Especially considering Circle is paying a majority of its revenue directly to Coinbase as a distribution partner. And to my point earlier, Tether’s GTM strategy has captured the stablecoin market where it matters the most: in the emerging and unbanked economies. If anything, Circle faces even more challenges if we assume banks will slowly begin to launch their own stablecoins. That competition will be primarily isolated to the US and western economies.

Link to the full S-1 form: https://www.sec.gov/Archives/edgar/data/1876042/000119312525070481/d737521ds1.htm

However, Tether is not without its own structural value leakage and expansion constraints. As Tether’s issuance spreads across chains, the infrastructure supporting USDT is largely outside of Tether’s control (settlement, execution, bridging, etc.). This means that the economic value generated by USDT usage is disproportionately captured by the base layers it relies on, especially Ethereum and Tron.

Take Ethereum, for instance. As one of the earliest chains to support native USDT, Ethereum benefits from billions in daily stablecoin volume. Every transaction involving USDT on Ethereum incurs gas fees paid in ETH, subsequently accruing to validators.

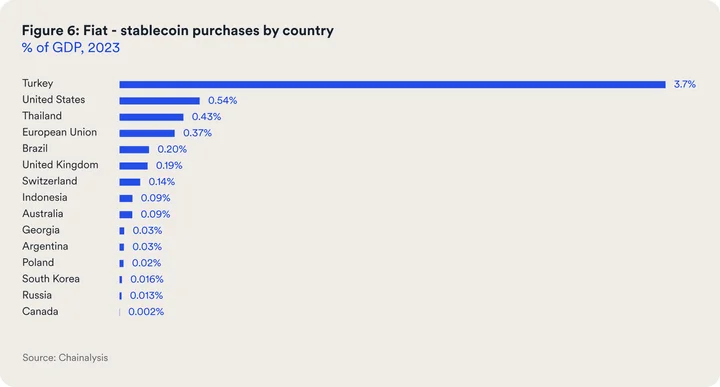

Tron exhibits a similar pattern, though with different mechanics. Tron has become the dominant chain for low-cost, high-throughput USDT transfers – especially in regions with high remittance activity. However, I do have to note that even transaction fees on Tron have shown a consistent trend upwards – indicative of the exponential growth and demand of a stable fiat-pegged asset like Tether. This is especially the case in countries with hyperinflated native currencies such as Turkey and Argentina.

Source: Chainalysis https://www.bvnk.com/report/decade-of-digital-dollars

But again, the transaction fees generated from this activity accrue to the Tron network itself. In this case, Tether acts as the commodity, not the rail – enabling usage but not extracting value from it.

Now, from strictly a revenue standpoint, Tether isn’t really suffering from the disproportionate flow of value on the settlement and execution front. Its current business model more than well makes up for it. As an issuer of dollar-pegged stablecoin, its business model is remarkably simple, yet extremely profitable. It makes the vast majority of its revenue from interest earned on the reserves backing USD₮.

- Users mint USD₮ (depositing USD or equivalent fiat)

- Tether holds these funds in various reserve assets (primarily U.S. Treasury bills)

- These assets yield interest. Because Tether does not pay yield to USDT holders, the interest income becomes pure profit

With over $155 billion in USD₮ circulation, even modest yields (eg. 5% on Treasuries) equate to billions in annual interest revenue. In Q1 2025 alone, Tether reportedly earned ~$1 billion in net profit, mostly from interest income on Treasury holdings. This effectively has made Tether one of the most profitable companies in crypto, despite offering no consumer-facing services and charging no direct usage fees. In fact, Tether is the highest revenue/employee company in the world, with roughly $83M per employee in 2024.

But while Tether’s revenue model remains resilient, the infrastructure that supports its usage is under mounting pressure. Ethereum and Tron may have facilitated USD₮ to ubiquity, but their foundational design choices were never optimized for the scale and velocity that stablecoins have since demanded. It once again becomes an issue of scaling. And this raises the question: what would it look like to design an entire blockchain ecosystem with Tether at its core?

Plasma begins to answer that question. But before diving into its architecture and role, it’s worth zooming out to understand the broader infrastructure landscape that stablecoins operate within.

Current Stablecoin Infrastructure

The idea of a Tether-specific chain might seem paradoxical. Ethereum and Tron essentially created the conditions for Tether to thrive. Demand for a stable dollar-pegged asset was the value prop that brought Tether to where it is today, and to abstract away from that demand layer seems counterintuitive to its continued growth. Stablecoins are demanded where the most onchain user activity resides. And although this is true, Tron’s dominance as the “Tether chain” is telling of the growing demand of stablecoins outside of crypto.

It reveals that the chains that serve Tether best are ones optimized for throughput, latency, and deterministic cost structures. In other words, they behave less like experimental compute layers and more like financial settlement layers.

The simple fact is: general-purpose blockchains are not optimized for stablecoins – especially if we assume their continued growth and trajectory of adoption.

Scaling is the single most important case for a stablecoin-specific chain. Ethereum is simply too expensive and inefficient to accommodate for the adoption of global remittance or cross-border payment networks. Tron, on the other hand, was the alternative solution to this. The main problem with Tron has always been centralization concerns, but even now Tron is seeing fees get quite high in the $1-3 range. These chains were never architected for high-frequency, low-margin transactional throughput.

Even post-EIP-4844, Ethereum’s blobspace doesn’t materially help stablecoins. They don’t benefit from data availability scaling; they need execution-layer scaling and predictable low-fee finality.

Tron’s architecture mitigates some of this, with its delegated PoS and low fees. But even then, it comes with its own trade-offs of validator centralization and non-deterministic fee spikes (hence the recent increase in base fees).

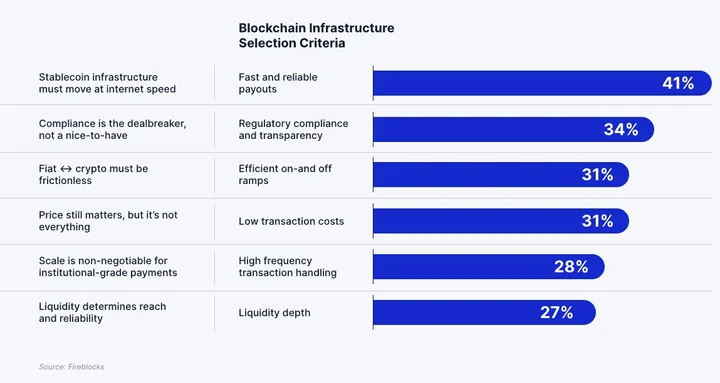

A recent report by Fireblocks on the state of stablecoins in 2025 highlights where the criteria focus is on enterprise-grade stablecoin infrastructure. Speed and reliability, low transaction costs, and high frequency txn handling are common themes.

Another point worth noting is that stablecoin transfers have distinct network patterns. Unlike DeFi operations, simple stablecoin transfers are almost universally single-purpose, linear and frequent, and initiated by external accounts, not smart contracts. Stablecoin transfers do not require complex inter-contract logic or recursive calls. They’re stateless in the sense that the transfer is self-contained and doesn’t require persistent on-chain program state beyond a balance update.

An example of this may be a remittance corridor involving a user in Argentina receiving USDT multiple times a month. Each time is a vanilla transfer, yet each must be bundled, validated, executed, and written to disk in the same pipeline as a Uniswap v3 rebalancing or another complex DeFi execution if we’re referring to execution on Ethereum.

The execution bottleneck is therefore not complexity, but volume. This creates unnecessary network load, with high-frequency transactional patterns shoehorned into compute-constrained environments.

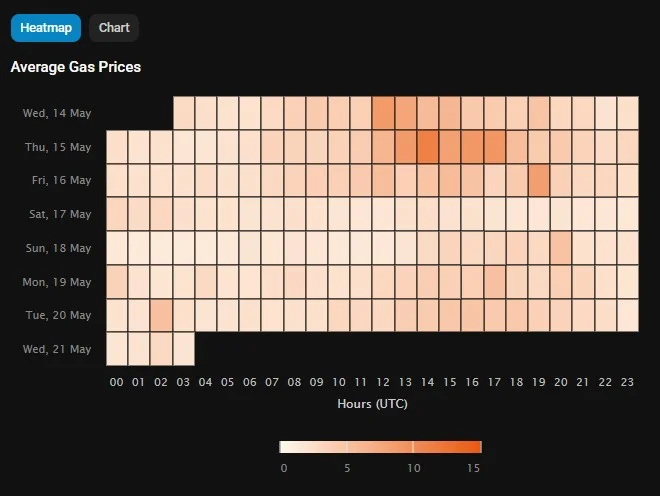

https://etherscan.io/gastracker#gasguzzler

Tether is currently ranked as the number one gas guzzler on Ethereum – and that’s simply from the sheer volume of transactions.

Stablecoin transfers are also reflective of fiat cycles since that’s where the vast majority of adoption is from: payroll, remittances, consumer payments, OTC deals, etc. This leads to periodic bursts of high activity that don’t correlate with gas fee dynamics in many cases. The average user isn’t going to pull up etherscan to check the heat map on average gas prices before sending a cross-border payment – they expect a consistent flat fee across the board.

https://etherscan.io/gastracker

For stablecoins to move from crypto-native utility to global financial infrastructure, the chains that host them need to be:

- Execution-optimized for simple, high-frequency txns

- Fee-stable, with costs tied to predictable system usage, not speculative blockspace bidding

- Latent-efficient, offering low finality times for payment UX parity with systems like Visa

- Scalable, without compromising on validator decentralization or state pruning

Is A Stablecoin-Specific Chain Necessary?

There seems to be a stark divide in how Plasma (or at least the idea of stablecoin-specific chains) has been received on CT recently – either you get it or you don’t. And I see the criticism well warranted; are we actually creating a novel use case, or are we just repackaging an L1 under the current trending narrative of stablecoins?

Sure, we can make the case that Ethereum is not performant or cheap enough, and that Tron carries centralization concerns, etc.; but what about the existing crop of high-TPS chains? What about something like Solana?

Wouldn’t a high-TPS chain like Solana be sufficient to handle stablecoins? If so, why do we need a stablecoin-specific chain like Plasma?

On the surface, this seems like a fair critique. Solana seems to check all the boxes that we mentioned above for the ideal chain to host stablecoin settlement on: optimized execution, latent-efficient, and scalable without compromising on decentralization. But the case for Plasma isn’t just about whether a general-purpose chain can support stablecoins – it’s about how optimized can an ecosystem be solely around stablecoin usage. Although Plasma is technically considered “general-purpose” due to it being permissionless, stablecoins are the focal point here.

Plasma treats stablecoins as the native behavior, not an afterthought. This allows for minimalist VM logic and fee market flattening, all of which we will cover within Plasma’s architecture.

Aside from pure TPS metrics, stablecoin usage is more so about liquidity coordination and settlement cohesion. Stablecoins don’t exist in isolation – they are liquidity bridges between exchanges, apps, and users. When Tether is spread across 12+ chains, its liquidity is fragmented, its bridges become attack surfaces, and capital becomes inefficient.

Plasma consolidates this into a single locus of stablecoin liquidity, reducing slippage, arbitrage gaps, and inter-chain bridging risk. It’s best described as a coordination shell rather than a simple transaction layer. Even Solana, despite its performance, contributes to this fragmentation. A transaction on Solana is fast – but global stablecoin movement is still bottlenecked by the fact that Solana is just one of many Tether-hosting chains. Plasma re-anchors that fragmentation by making Tether-native applications converge on a single vertical chain.

Now, I will also note that Tether has also focused on expanding the stack horizontally with LayerZero OFT – a standard that allows fungible tokens to be transferred across multiple chains without the need for asset wrapping. This multichain version is referred to as USD₮0.

Plasma also represents a strategic consolidation of Tether’s role as both issuer and infrastructure layer. Solana supports USD₮, but Tether doesn’t control Solana. On Plasma, Tether isn’t just an issuer – it becomes the monetary and infrastructural substrate. This matters because it lets Tether:

- Build vertical integration between issuance, transfer, and redemption

- Set protocol-level guarantees around things like redemption windows, transaction visibility, or compliance

- Offer native stablecoin tooling and SDKs, without the overhead of supporting 15 different execution environments

Think of it like Visa launching a global card network that also controls the payment rails, identity layer, and merchant backend. Plasma is Tether’s opportunity to consolidate its economic stack into a programmable chain.

In reality, Plasma’s architecture and GTM strategy is more akin to that of Ripple & XRP. As much of a meme it is, there is a huge market for global payments and remittance services. Plasma’s approach is just different. It focuses on an already existing demand from corridors outside the US where a majority of the unbanked populations reside. And Tether is the best vehicle to onboard this already existing userbase.

Plasma – Purpose-Built Stablecoin Architecture

Plasma is a chain architected specifically to meet the demands of high-frequency, low-complexity stablecoin transfers, specifically tailored for USD₮. It addresses many of the inherent constraints we’ve discussed with today’s general-purpose L1s when it comes to handling these types of transactions. The goal of Plasma is to become the global settlement and issuance layer for digital dollars.

There are a few components in Plasma’s architecture that make this possible:

PlasmaBFT Consensus

PlasmaBFT is a streamlined implementation of the HotStuff protocol optimized for low-latency, high-throughput execution. Unlike traditional HotStuff, which involves a three-phase commit process (prepare, pre-commit, and commit), PlasmaBFT condenses this into a two-phase commit. This significantly reduces consensus overhead while still preserving liveness guarantees under partial synchrony. This is important in the context of high-volume stablecoin transfers, where the bottleneck is not computational complexity but instead raw volume.

The following paper discusses how two phases are enough for BFT in case you want to go down that rabbit hole: https://decentralizedthoughts.github.io/2023-04-01-hotstuff-2/

PlasmaBFT relies on Quorum Certificates (QCs) to move securely through consensus phases. Validators vote on proposed blocks, and once a quorum is reached, these votes are aggregated into a QC. This structure allows for rapid and provable finality without the need for lengthy confirmation windows. Additionally, in scenarios where a leader fails or becomes unresponsive, PlasmaBFT supports a fast recovery path via Aggregated QCs (AggQCs).

In this scenario, validators forward their most recent votes to the new leader, who aggregates them to determine the highest safe block to build upon. This ensures progress without risk of equivocation or rollback.

PlasmaBFT makes use of pipelining, enabling concurrent consensus rounds – a quite common implementation among many of the newer gen high-throughput L1s. While one block is being finalized, another can already be proposed and processed in parallel.

Bitcoin-Anchored Security

One of the main features of Plasma is that it leverages Bitcoin as a root of trust, anchoring its security to the most battle-tested and censorship-resistant blockchain available. It does this through periodic state commitments (these could be referred to as sort of a checkpoint) where a snapshot of its chain’s state is taken (specifically, a Merkle root of recent finalized blocks) and published onto Bitcoin. Once committed to Bitcoin, this snapshot is immutable – to rewrite it would require a reorg of Bitcoin itself, which is economically and practically infeasible.

This anchoring provides objective finality: if a Plasma block root is published on Bitcoin, it becomes part of Bitcoin’s global state. Assuming Bitcoin’s level of censorship-resistance, anchoring Plasma’s state to Bitcoin significantly reduces the chance of collusion or censorship on the Plasma chain itself – effectively giving it the same level of security. Any inconsistencies or attempts to alter Plasma’s history can be detected by comparing against these Bitcoin-anchored checkpoints.

Users or applications can use Bitcoin as an external source for verifying whether a given Plasma transaction or state transition is valid, without relying solely on Plasma’s validator set.

Full EVM Compatibility & Reth Execution Layer

Of course, none of this is significant without liquidity – and the vast majority of stablecoin liquidity is on Ethereum, with ~56.5% of total outstanding stablecoin supply. As far as USD₮, both Ethereum and Tron hold roughly the same amount (~$71.2B – $77.8B respectively), Tron recently flipping Ethereum within the last month.

It only makes sense to integrate chain compatibility where the most stablecoin liquidity resides, hence Plasma’s implementation of full EVM compatibility. Plasma nodes can interpret and execute Ethereum bytecode exactly as Ethereum does. This means developers can take a contract written for Ethereum (for example, a USD₮-compatible ERC-20 contract) and deploy it directly on Plasma with no changes.

Remember, Plasma isn’t only for facilitating stablecoin transfers, but also allows a wide range of stablecoin-focused products and applications to be built and integrated on. Although Plasma retains full EVM fidelity, its architecture encourages simplified and repetitive contract patterns (stablecoin focused).

Plasma’s EVM compatibility is anchored by Reth – an execution client written in Rust and designed ground up for modularity and performance. Reth’s modular state provider design enables Plasma to build execution environments that can decouple storage from computation. This means Plasma can experiment with alternative DA or compression layers without needing to rewrite its execution logic – a perfect way to optimize for things like zero-fee USD₮ transfers or tightly-coupled gas abstraction layers.

Zero-Fee USDT Transfers

Before we jump into this section, I do want to caveat this by mentioning that “zero-fee USD₮ transfers and shielded transactions are currently considered to be in the “active research” phases. We will cover the basis of these architectures, but it’s worth considering that these concepts are still hypothetical.

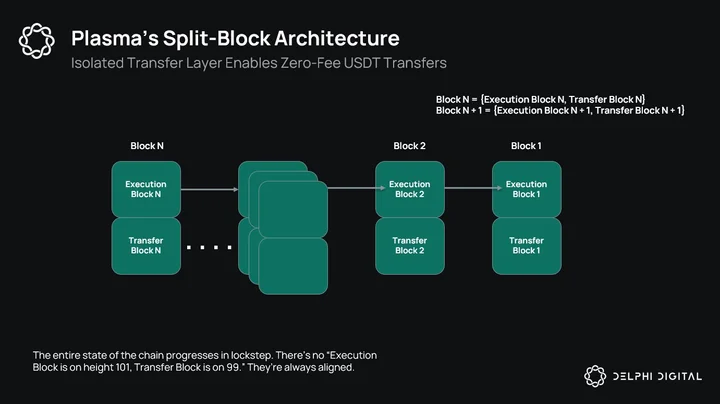

One of Plasma’s key shilling points lies in zero-fee USD₮ transfers. It achieves this through an architectural design that isolates these transactions from fee-paying activities. The mechanism enabling this is what Plasma refers to as a split block architecture.

A split-block architecture involves a two-layer block structure within a single blockchain height. This includes:

- Primary Layer (Execution Block): This block contains general-purpose, fee-paying txns – typically smart contract calls, DeFi operations, etc.

- Secondary Layer (Transfer Block): This block exclusively contains USDT-to-USDT transfers that do not pay gas.

Each block in Plasma is logically divided into these two sub-blocks. They are both committed to at the same height and validated atomically by consensus, but their execution environments are isolated. Rate limiting, minimum balance requirements, and aggressive transaction replacement policies are additionally used to mitigate spam.

*This feature is still under active research with the plan to be rolled out in phases and may be subject to change. This is not active on day one.*

Dissecting Plasma’s Zero-Fee Paradox

Plasma’s revenue model is a bit nuanced, particularly because USD₮ transfers are planned to be zero-fee, which at first glance might imply reduced economic activity for validators or the protocol. However, when we take a look at the architecture and monetization pathways, we can see that zero-fee transfers are not the intended source of revenue, hence why they are exempt from fees.

Plasma essentially has two types of executions: one containing general-purpose, fee-paying txns, the other, exclusively containing USD₮ transfers. The nuance is here: zero-fee USD₮ transfers are not to be confused with all transactions using USD₮ on the chain. The zero-fee element is strictly a feature of sending and receiving USD₮ from one wallet to another, similar to a Venmo payment. All other operations, be it DeFi related, contract calls, swaps, etc. are all still subject to regular transaction fees.

So how does Plasma achieve zero-fee transfers? Does this mean they are subsidizing or eating the fees on the backend?

Once again, this ties back to Plasma’s split-block architecture. All general-purpose txns go through the full EVM execution path and incur normal gas fees. Since USD₮ transfers do not interact with the EVM, it drastically reduces this computational overhead. And by bypassing EVM execution entirely, they don’t require traditional gas metering or execution costs.

Of course, this is only if it does get implemented.

For perspective, on Ethereum, a simple Transfer()call is deceptively expensive:

- 21,000 gas for base transaction cost

- ~25,000–40,000 gas for ERC-20-specific storage updates (depending on slot state)

All of this for what is essentially a simple balance update.

Now, on day one, these specific fees will indeed get subsidized by Plasma. As volumes trend higher, the need to implement these sort of solutions will be considered.

Privacy & Shielded Transactions

Stablecoin usage is heavily skewed toward individual accounts and custodial wallets, not smart contract interfaces – which inevitably brings up the concerns around privacy and compliance.

- Transaction clustering is predictable

- Flows are directional and cash-like

- Anonymization is weak where everything is public and indexed

This is a paradoxical topic in the context of blockchains since everything is transparent on a public ledger. However, in the traditional financial system, users require certain levels of confidentiality – from corporate payrolls to investment loans to personal credit scores. These are all information that would require some sort of anonymity within the context of onchain integration in order to be adopted at scale by users.

Plasma acknowledges this gap by planning to introduce a nascent mechanism it refers to as shielded transactions. While the documentation is sparse on implementation specifics, the idea of implementing these sort of features signals a design direction that aligns more closely with privacy-preserving financial systems.

In a hypothetical implementation, Plasma could follow similar principles to those used in Zcash or Aztec – systems that leverage zero-knowledge proofs to validate transactions without revealing amounts, senders, or recipients. In fact, onchain financial products are one of the few killer use cases for ZKPs.

More realistically, given Plasma’s EVM compatibility and performance optimizations, it might adopt a selective disclosure model, where only certain aspects of a transaction are encrypted or concealed, while others remain public for validation purposes.

Another plausible approach is integrating confidential transfer modules that utilize zk-SNARKs or zk-STARKs, but scoped specifically to token transfers. This would allow, for example, USD₮ transactions to remain private within a shielded pool, while still interoperating with the broader Plasma economy. These designs could be optionally enabled via transaction flags, or integrated into the split-block architecture, isolating shielded flows similarly to how zero-fee transfers are processed in the Transfer Block.

These are just some hypothetical approaches.

As of now, this area is still under research. The Plasma team will be sharing more information regarding this soon.

Implications for Tron & Stable Payments on Other Chains

Tron is currently the undisputed leader in Tether usage, so any credible attempt by Plasma to consolidate that liquidity poses real implications for Tron.

At first glance, Plasma looks like a simple vampire attack on Tron. And yes, I would agree that Plasma’s value proposition is an indirect vampire attack. However, Tron was never intended to be a stablecoin-specific chain. Its default position as the “Tether chain” was consequent of its low transaction fees from the demand outside of crypto. And that advantage is slowly decaying as its fees steadily increase.

how are people affording to transact on tron when gas fees are ~$6 (most of their user base is in emerging markets)

“tron is cheap” just doesn’t hold anymore pic.twitter.com/Q70y1pZZMJ

— Bridget (@bridge__harris) March 25, 2025

Tron’s transaction economy is overwhelmingly driven by USD₮. Currently, more than half of Tether’s $155B supply resides on Tron, and an even higher share of daily transactional volume is USD₮-based. Tether is the activity on Tron. This alone is enough to destroy Tron’s value prop. But Plasma isn’t fully to blame here – it’s consequent of Tron’s economic value being propped up by a single stablecoin. How come we aren’t saying this is a vampire attack on Solana, or Arbitrum? It’s because their activity isn’t solely concentrated in Tether transfers.

If Plasma manages to capture even 30% of the global USD₮ velocity, Tron’s blockspace demand will collapse, validator fees dry up, and its native token TRX loses its monetary role in transaction processing. The problem for Tron is that it doesn’t have a secondary market to fall back on. This isn’t much of a concern for Ethereum. Yes, if Plasma succeeds, Tether TVL will also leave the ETH L1 – but this would be marginal since the majority of activity on ETH mainnet is DeFi related. I would assume your average user isn’t choosing Ethereum to send and receive USD₮. And this follows to my second point on how it will affect stable payments and flows on other chains.

In many cases, and depending on the level of success of Plasma, we’ll likely see outflows of USD₮ from the long-tail of chains. This doesn’t necessarily imply that stablecoin usage or USD₮ will become obsolete on these chains. If there is any sort of meaningful volume or activity on a chain, the need for stables in that ecosystem will always exist. Plasma’s role isn’t to abstract away USD₮ entirely – it’s to have a native hub specific in facilitating cross-border remittance, payments, and merchant settlement.

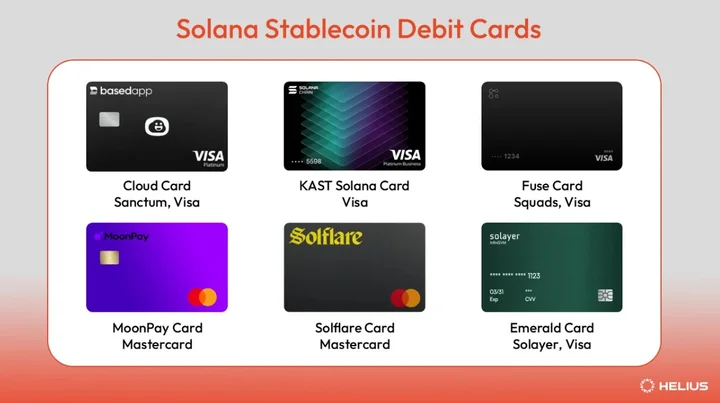

But the topic of stable payments is a bit more ambiguous. Their success within a particular chain is partially dependent on the applications that enable practical use cases. Solana is great example of this. Recently, there has been a new wave of off-ramp products on Solana in the form of debit cards, both physical and virtual. As a crypto-native, this allows me to use my stables as payments for everyday financial activities off-chain.

https://www.helius.dev/blog/solanas-stablecoin-landscape

It’s also worth noting that crypto-natives will likely keep most of their stables on the chain that they are most interacting with on a regular basis.

Plasma Ecosystem

So how does Plasma aim to generate any revenue assuming USD₮ transfers are free? The trillion-dollar question.

We need to first understand that Plasma isn’t trying to monetize the base transfer of value (USD₮), but rather the ecosystem and services built around that value transfer. Its model is based on monetizing financial flows, not raw transactions. Yes, essentially, it’s another L1. A chain built around stablecoin velocity – and where there’s velocity, there’s margin, even if it’s not user-facing.

Plasma’s GTM strategy is quite impressive. USD₮ transfers acts as a public utility: free, frictionless, and built to encourage maximum volume and user adoption. The real revenue opportunities exist in the contract lane, where all meaningful financial operations that emerge because of stablecoin flows are processed. For example, FX conversions, yield routing, DeFi operations, or business settlement logic are all transactions that would incur normal fees. So, while the act of sending USD₮ is free, the services that wrap around that transfer are monetized at the protocol level.

Let’s take a look at some of the already existing protocols and partnerships with Plasma.

Yellow Card – Africa’s leading stablecoin payments and on-ramp platform, has partnered with Plasma to route USDT transfers and remittances across several countries within Africa. Currently one of the largest unbanked populations among emerging markets.

BiLira – A Turkish Lira–backed stablecoin, integrates with Plasma to offer efficient cross-border stablecoin access between Turkey and USDT rails. This strengthens Plasma’s role in the MENA and Eurasia corridors.

In this scenario it looks like BiLira serves as a fiat-denominated access rail – a regulated and compliant layer to bridge Turkish Lira (TL) to TRYB (onchain).

Commodity settlement is another area that Tether is exploring.

Uranium Digital is developing the first 24/7, institutional-grade spot uranium trading platform, offering physical settlement. By tokenizing uranium, Uranium Digital and Plasma are bringing a traditionally opaque and illiquid market onchain.

Of course, a stablecoin-specific chain isn’t complete without its yield protocols.

Axis is a native yield hub for hard assets on Plasma. They introduce xyUSD, a yield-bearing synthetic asset backed by regulated hedge fund strategies, connecting DeFi users with institutional-grade returns.

Curve Finance is a foundational protocol in the stablecoin economy, and it wouldn’t make sense to be excluded from the stablecoin-specific chain. It’s optimized for low-slippage swaps between assets of similar value, making it the ideal DEX for stablecoin markets.

Ethena, known for its synthetic dollar, gives the network access to yield-bearing and synthetic assets built atop stablecoin infra on Plasma. This expands the design space for financial apps that need dollar-denominated logic and provides diversity in Plasma’s stablecoin ecosystem.

Plasma as the DeFi Hub

Earlier we touched on the potential implications Plasma has on Tron. But if Plasma really succeeds in capturing the lion’s share of stablecoin volume, Ethereum could experience second-order effects. This would be due to the flywheel Plasma has created combining their architecture with their GTM strategy.

Let me break this idea down:

- Plasma captures the USD₮ market from Tron with zero-fee transfers > Tron becomes obsolete

- The deep stablecoin liquidity on Plasma attracts existing DeFi protocols to the chain

- Users prefer Plasma over Ethereum due to its speed and low cost > activity on Ethereum drops

Now, the reason why Plasma has a competing chance is because it inherits its security from Bitcoin, has the dominant market share of USD₮ and stablecoin liquidity, all while being EVM compatible with the speed and scale that Ethereum lacks. The argument that Ethereum is more secure and has the most liquidity and TVL no longer holds true in this scenario. Plasma in a sense, becomes the leading chain by capturing crypto’s one standout use case: stablecoins.

But as with any narrative in the space, there is no shortage of competition. Stable recently announced the launch of their product, hinting that we’re likely to see a proliferation in this stablecoin-focused trend.

i’ve heard there are about 5

— tunez (evm/acc) 🤖 (@cryptunez) June 5, 2025

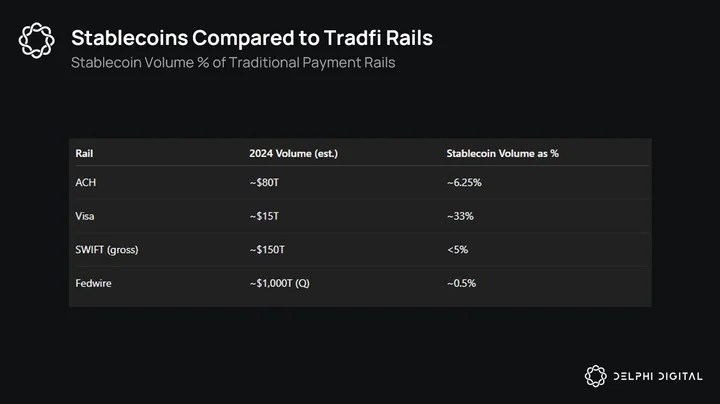

Stablecoin TAM – A Trillion-Dollar Opportunity

Plasma isn’t just a response to technical limits. It’s the thesis that stablecoins have grown large enough to justify infrastructure designed for them alone – the same way AWS built dedicated services for specific compute needs. Last year, stablecoins facilitated over ~$5 trillion in adjusted transaction volume, over 1/3 the volume of traditional payment giants like Visa and Mastercard.

In the U.S. alone, systems like Fedwire and ACH process well over $1 quadrillion in annual volume – orders of magnitude greater than GDP. Globally, the numbers are even higher. And within this context, stablecoins are just beginning to penetrate a market that spans consumer payments, interbank settlement, FX, cross-border remittances, merchant services, capital markets, and more.

For millions around the world, Tether has become the most practical form of digital dollar exposure. And this is the point I want to really harp on – there is a perspective disconnect in just how impactful stablecoins are for those in emerging markets versus the west that has easy access to banking. The echo chamber of CT incredibly underestimates the actual TAM of stablecoins. A global, 24/7, instant settlement digital dollar is the killer use case of crypto.

Crypto in itself is a hyper financialized sector. To this day, the major use cases are still trading assets and transferring value. For crypto-natives, stablecoins represent a fiat-pegged asset to denominate in. For the broader population in emerging markets, it represents a hedge against hyperinflation, a source of savings and payment rails for the unbanked.

It’s worth considering that for the latter group, stablecoins are viewed as a SoV. Unlike us degens, they aren’t looking to capture a 30% yield on their stables – they’re much more willing to forgo that for credibility, deeper liquidity, and global acceptance.

And I think this points to a future where stablecoins won’t be defined strictly by APYs or protocol incentives, but by infrastructure that can scale to meet real-world usage. If Tether continues to lead that thesis, Plasma may prove to be one of the most direct, high-leverage exposures to the next wave of stablecoin adoption; especially in the parts of the world where crypto isn’t just a trade, but a necessity.

Trillions.

0 Comments