Pollen and Helium: The Race to Bootstrap a 5G Network

JUL 25, 2022 • 17 Min Read

Report Summary

Decentralized Wireless (or DeWi) seeks to build out physical wireless communication infrastructure (5G CBRS antennas) through incentivizing individuals to deploy hardware at homes or businesses and backhauled through an ISP.

Helium and Pollen are in a real estate competition across two vectors 1) the real estate within one’s home or business to deploy a 5G node and 2) to occupy the first eSIM slot on users’ devices. This report will focus on the former.

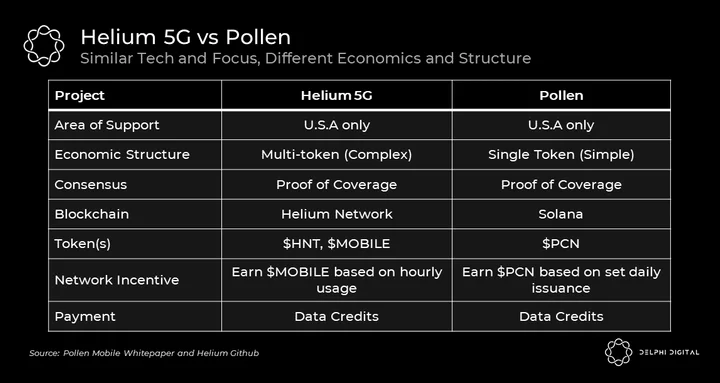

Pollen and Helium are in an incentive war to convince users to deploy their respective 5G Nodes. Helium has a more complex multi-token structure given its legacy incentives spent for IoT deployments (1M nodes, minimal usage) and Pollen has a simpler structure with rewards solely focused on 5G.

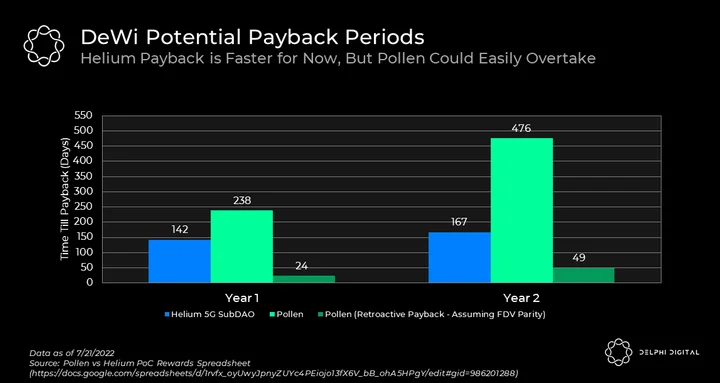

While variables will shift and no model is perfect, we expect Helium and Pollen to have payback periods of 142/238 days next year. Pollen’s higher PBP is driven from a FDV that is 1/10 of HNT’s, although if FDV parity is reached this will result in a retroactive payback period of 24 days. This in turn provides more profit for miners (all earnings after day 24 retroactively is profit) and more funding to build out the network which drives the flywheel of more coverage/capacity for users and dollars through the system.

The incentive war is of interest as whichever project can incentive more 5G nodes to blanket major cities to provide sufficient coverage and capacity will drive exogenous real dollar data usage through the network. Incentivizing nodes is the 1st inning and real data usage through the network is the endgame.

Disclaimer: 2/9/23 Update: This report is no longer accurate as the Pollen team has decided to memorialize the hard cap of PCN at $0.10. This impacts the build out, incentives and viability of the network.

Intro to Traditional Telecoms and Decentralized Wireless (DeWi)

The advent of cellular communication revolutionized how our world operates. In order to build out the vast infrastructure that enabled us to call our loved ones across the world and browse crypto-Twitter on the go required immense amounts of capital, as well as numerous decisions on where and how capacity should be built out.

Traditional telecom companies have spent hundreds of billions building out spectrum and tower infrastructure, as well as on ongoing maintenance and network upgrades. Lately, they have been investing into the next generation of wireless technology (“5G”), but they have not done a good job at providing 5G inside of people’s homes, in data-congested metropolitan areas, or in remote areas. These problems stem from the fact that the 5G spectrum has a difficult time penetrating into the home from a distant radio cell, because legacy wireless infrastructure is ill-equipped to handle the extra load, and because there is no incentive for them to build in areas with low population density.

Some other problems with the traditional model include a lack of privacy and consumers’ overpaying for their data. With regard to privacy, the data that travels through the carriers’ networks is owned by the carriers and theoretically can be viewed by them at any time, governed only by the Terms of Service. This should be unsettling for people who don’t want to share their daily or deepest thoughts and feelings with a corporation. With respect to the second matter, telecom companies have a high cost basis for the data they provide, sometimes as high as $2.50 per GB. As such, they’d rather convince people to subscribe to an unlimited plan so as to balance out usage across a pool of customers, some of whom use a lot and some a little. DeWi providers such as Pollen Mobile and Helium Wireless have a much lower cost basis, as low as $0.50 per GB, and thus customers could probably save money by switching to them. To learn more about the problems DeWi fixes, we recommend you read our previous DeWi report.

Out of all of these, the first issue is perhaps the most important, because industry reports reveal that consumers use cellular data the most when they are indoors. We feel that one of the explanations for this phenomenon is that the general public cannot, and for security reasons should not, log in to random internet hotspots. Therefore, it is reasonable to deduce that providing superior cellular service and faster bandwidth (i.e. 5G) indoors is imperative for the wireless industry. If only the incumbent companies had a means to do it better.

Decentralized Wireless addresses all these problems. 5G-focused DeWi is a telecom model that incentivizes individual network participants to build out a 5G wireless network that penetrates homes, works well in data-congested metropolitan areas, and even rewards people for building out capacity in rural areas, all the while encrypting the wireless data and protecting users messages, often at a cheaper rate per gigabyte of consumption (up to 5x cheaper).

This is quite a feat and quite an attractive business proposition, with 5G connections in the U.S. expected to grow to 17.6% of all mobile connections in 2023 (up from 0% in 2018) in the U.S. alone.

How it Works: Traditional Telecoms vs DeWi

The DeWi thesis is as follows: If one can properly encourage the general public to set up antennas in their residence or on their property then a fully functional wireless communication network can be deployed in any area regardless of population density and without a corporation needing to invest large sums of money into further physical infrastructure.

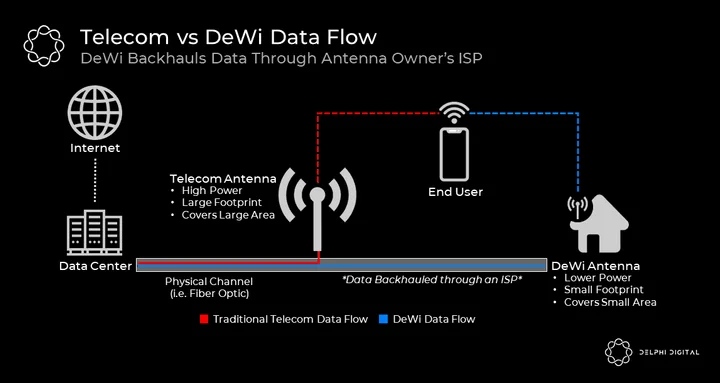

Traditional telecom companies outsource their infrastructure needs to tower companies (e.g. American Tower – $120B market cap, Crown Castle – $75B market cap) who manage big, high powered antennas that can cover a large area to provide 3G and 4G. These antennas communicate with an end user’s device. Once the antenna receives communication from an end user, it relays it to a data center (such as Equinix – $60B market cap and Digital Realty – $36B market cap) and then ultimately the internet via a physical channel such as a fiber optic cable. DeWi works similarly except the 5G antennas cover less range (meaning more antennas are required to cover the same area as a traditional telecom antenna) and the data the antenna receives is backhauled to the internet through the antenna owner’s Internet Service Provider (ISP) as opposed to traveling through a telecom company’s channels.

While data flows in these two models seem rather similar, DeWi initiatives make use of special parts of the spectrum, use unique protocols to secure their networks, and use third party technologies to transmit their data.

Since wireless communication is heavily regulated in most countries, it can be very costly to get the proper licensing. For this reason, DeWi projects have had to find cost effective portions of the spectrum to service their needs. In the USA, they use the publicly available Citizens Broadband Radio Service (CBRS), a 150 MHz section of the wireless spectrum. They use CBRS to perform wireless communication between end users (i.e. cell phones) and antennas. While CBRS is available for public use there are still some restrictions, and priority access is available for a fee. It is important to reiterate that the CBRS is specific to the USA and the DeWi projects we will look at later on in this article focus specifically on developing their infrastructure in this region.

While the aforementioned protocols and technologies aid in making DeWi a reality, it is important to note that there are still a number of hurdles that DeWi must overcome. One main concern would be an ISP turning off an antenna owner’s internet access. However, as traditional wireless companies and ISPs are in direct competition for users and data usage, one would expect that, in the long term, ISPs will allow such data backhauling in order to capture more value. For a more in depth discussion on the challenges that DeWi faces we recommend reading the section “Challenges On The Way To A Global Wireless Provider” in our Helium post linked here.

As a recap, wireline companies are in competition with wireless companies for data usage through their networks and by allowing DeWi companies to operate, it’s our opinion that the wireline companies can effectively compete with their wireless competitors by charging users an additional amount for DeWi backhaul, but a lesser amount than these users would pay to their wireless companies. Since wireline data rates are well below wireless, DeWi companies effectively arb this difference while driving usage for wireline companies.

With the overview out of the way we will now transition to talking about and comparing two interesting DeWi initiatives. The first is Helium, a project that pioneered decentralized wireless,initially starting with a focus on developing a decentralized Internet of Things (IoT) network but has recently expanded to offer 5G. The second is Pollen Mobile, a rising star in the 5G DeWi space whose go to market strategy will be discussed in the following section. Following that will be a breakdown of both projects’ approaches to the 5G DeWi space.

How It Works: Pollen

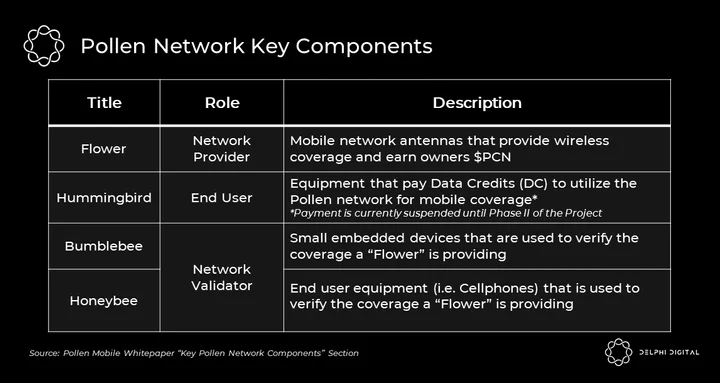

The above table defines terms used by Pollen mobile when discussing various components of their network infrastructure. Pollen mobile makes use of a token, PCN, to incentivize network participants to fill their respective roles, further grow the network, and manage the purchasing of Data Credits (DC) for use within the network. One DC is equivalent to a single Gigabyte (GB) of data and costs $0.50. The price of 1 PCN is set by the Pollen Operating Company (OpCo) and was initially set at a ratio of 1 PCN:$0.10.

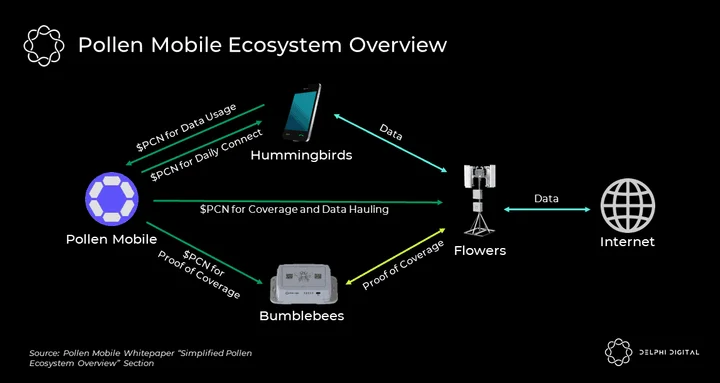

As outlined in the prior table there are three main actors in the network: flowers who provide network coverage, bumblebees who validate the network, and hummingbirds who are the end users of the network. During the build out of the network all participants, even the end users, are able to earn PCN on a regular basis. In order to incentivize network growth a set amount of PCN is released by Pollen Mobile on a daily basis to those who have participated in the network for that given day.

There are various flowers ranging from Dandelions to Buttercups and several in-between that vary in cost and strength to cater to various supply side participants. Since Pollen announced its cloud gateway, these flowers no longer utilize the external computer they historically made use of. Helium still does uses such a external computer. With this new architecture and fewer pieces of hardware in the system, deployments have gotten faster, easier, and cheaper for consumers.

300,000 PCN is awarded to network participants every day. The amount of PCN a participant receives is calculated based on the number of PCN Incentive Credits (PICs) a participant has earned in a given day, as well as the overall number of PICs earned by the total network. The daily amount of PCN an individual earns is calculated based on the following equation:

PICs are earned for things like a flower providing coverage or a bumblebee validating a flower. An in depth description of how various network participants earn PICs can be found here in the Pollen mobile whitepaper (note: the exact PIC amount earned for various activities is subject to change but the underlying mechanisms that earn PICs should remain static). It is important to note that the earning potential for certain activities is capped, and we strongly suggest that the reader check out the above linked report for specific earning details. One example of this type of behavior is that a hummingbird only earns PICs for its first daily connection and none thereafter. These restrictions ensure that participants don’t attempt to abuse the PCN incentive system for their own monetary gain, preventing harm to the growth of the network.

As a reminder, once a user has PCN he or she will be able to use it to purchase data credits at a cheaper rate than currently offered by major telecom companies.

DeWi Battle Royale: Helium vs Pollen

From a technological perspective there are quite a few similarities between the two DeWi projects. Both utilize the Proof of Coverage consensus mechanism to ensure that coverage is being provided and both utilize the antenna provider’s ISP to backhaul data to the internet. However, when one digs into the overall structure and economics of both projects, things start to differ.

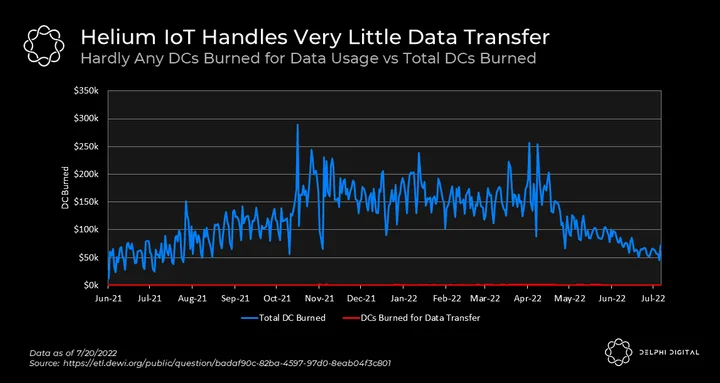

It is important to note that Helium initially began with a specific focus on IoT and has pivoted to include 5G in its product line, whereas Pollen currently focuses solely on 5G. Helium was able to build out a global IoT network with almost 1M nodes, but as seen from the chart above the data credits being burned for actual data usage is almost zero when compared to the amount of data credits being burned to maintain the network (i.e. add new gateways, assert device locations, pay fees, etc). While Helium proved that a crypto focused project could actually build out a physical, global network of hardware with the proper incentives, the fact that its IoT network isn’t being meaningfully used negatively impacts the strength of the IoT narrative and suggests that Helium should reduce or cease its core business activity..

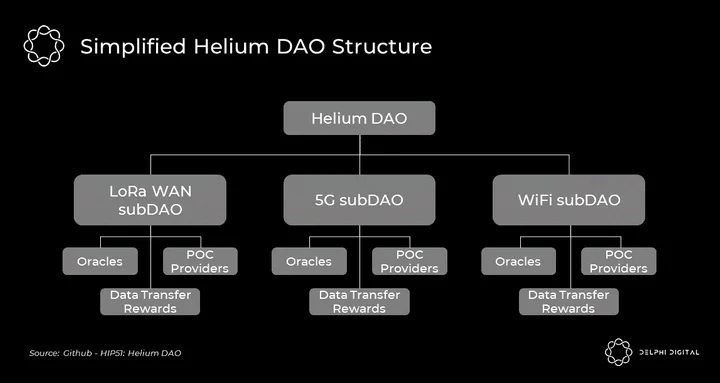

The Helium team recognized this and pivoted to penetrate the 5G market while maintaining the IoT arm. In order to accomplish this, Helium has proposed a DAO that would have subDAOs for each type of wireless communication it will offer in the future, as shown in the graphic below. Each subDAO is able to stake a claim to a certain amount of Helium’s token, HNT, dependent upon how much network usage that subDAO experiences.

The overall structure of the Helium DAO is logical, however due to the fact that a majority (55%) of the HNT tokens have already been emitted and were focused on their IoT initiative, only the remaining HNT will end up being split between each subDAO. HIP51 contains the full details as to exactly how HNT will be sent to the 5G MOBILE DAO and all of the factors that influence this process, such as the amount of veHNT staked, network usage, device counts, and activation fees.

One way that Helium is attempting to address this issue is by each subDAO having a token that can be staked in order to collect some percentage of HNT emissions. In the case of the 5G subDAO, that token would be MOBILE. Holders of MOBILE can do a few things with it, such as redeeming it for a portion of the HNT that accrued to the 5G subDAO, stake 50M of it in order to qualify to be a hotspot vendor, or stake 500M of it to be a service provider (500M MOBILE required). However, members of the IoT subDAO, the most developed arm of Helium, will also be able to stake their HNT to drive emissions to the IoT DAO, thus competing with the MOBILE subDAO for emissions that could be used to support Helium’s 5G initiative.

Unfortunately, there is no way for HNT holders to directly convert to MOBILE, further discouraging IoT participants to support the 5G initiative. HIP53 discusses the relationships between the tokens in more depth and we encourage you to read it.

While Helium’s structure and tokenomics are rather complex there is some value in this complexity as HNT and MOBILE owners are able to make use of the token through staking. All of Helium’s tokens are also governance tokens, providing some level of utility at the governance layer. This is unlike PCN, which is currently used solely for purchasing data credits. It should be noted that though Pollen’s whitepaper states that it intends to transition to a DAO in the future, there is not yet any indication that PCN would operate as a governance token similar to HNT and MOBILE.

Since both projects have their positives and negatives, the key factor to focus on is is incentivizing as many active participants in the network as possible. In order to bootstrap participation, users must receive payments and Pollen has a clear advantage as they have a larger token supply to give out. Furthermore, Pollen’s economic flow is simple and doesn’t come with the caveats that the more complex Helium multi-subDAO structure does. Delphi Digital’s Tommy Shaughnessy has a tweet thread discussing this, which can be found here.

Node Deployment Economics

Incentives to bootstrap 5G deployments are crucial to driving sufficient network coverage and capacity to eventually drive real paid usage through the network. Above we described Helium’s more complex model and Pollen’s simpler model, and below we will describe how this translates to node payback periods. Why node payback periods? Because if one network has the potential to pay its suppliers their capital expenditure back faster, that translates to more upside for node deployers and potentially a quicker buildout period as the faster payback implies more capital to buy and install more nodes.

55.6% of Helium’s rewards tokens (PoC and data transfer) are left for incentives. Of this amount we assume 26% of HNT issuance next year will go to the 5G DAO per community estimates. This amount will increase 10% per year thereafter. Of the 26% HNT sent to the 5G DAO, 5G node deployers have a claim over 60% of it, since 40% of MOBILE token is sent to other parties (mappers, providers, oracles, veHNT stakers, etc). Assuming 5,000 5G nodes this year and 10,000 next year, and a constant HNT price of $11, the payback period on a $2,500 HNT node is 142 days this year and 476 days next year.

Shifting to Pollen, the project has 92.3% of its reward bucket left for node incentives. Assuming 70% of rewards go to 5G antennas (flowers) and a constant PCN price of $0.25 with the same 5,000 and 10,000 nodes deployed as Helium, the payback time for Pollen is higher at 238 and 476 days for each year, respectively.

Pollen’s payback period is strongly influenced by a fully diluted value (FDV) that is nearly 1/10 that of HNTs. If we were to assume PCN’s FDV reached parity with HNT, which is not guaranteed, the retroactive payback period falls to 24 and 49 days respectively. On the other hand if Pollen’s FDV is unable to reach parity with Helium and instead stays as is, then the anticipated payback period would be the previously calculated 238 days for Pollen.

Why is this important? Rational actors seek upside and in our opinion they will participate in the network that allows them to earn more rewards. With a potentially lower payback period, Pollen’s network participants could see much higher profits (everything after day 24 and day 49 in this example is profit assuming the deployer held onto his or her tokens) that could be reinvested into nodes to drive a larger network build out. For those interested in toying with our model that we used to develop these estimates, it can be found here.

We have not forecasted beyond 3 years as data transmission dollars through the system will alter the payback periods.

Conclusion

While the concept of DeWi is still in its infancy the value that it could bring to network participants is immense. In this article, we covered the two frontrunners in the 5G DeWi space, Helium and Pollen. While both projects make use of similar technologies they differ in their overall structure and tokenomics. Helium started with IoT and has pivoted to include other facets of DeWi, such as 5G, leading to a complex multi-subDAO structure, whereas Pollen solely focuses on 5G, thus keeping their overall structure quite simple. Additionally, Helium’s 5G initiative competes with its already developed IoT arm for the remaining HNT emissions, whereas Pollen has no such issue. At the same time Helium’s complex structure gives its tokens more utility than Pollen’s in that they can both be staked and used to purchase data credits, whereas Pollen’s current architecture only allows for PCN to be used to purchase DCs.

Both projects need to incentivize network growth in order to succeed. Rational actors interested in participating in 5G DeWi will likely focus on time to payback as a main point to determine which project they’d invest in. Currently, Helium has the advantage in payback time, however if one anticipates that Pollen’s FDV will reach parity with that of Helium, Pollen will gain the upper hand. It is important to reiterate that this parity is in no terms guaranteed.

We will end how we began: incentivizing nodes is the 1st inning and real data usage through the network is the end game. Pollen has signed an MOU for their first data offload partner and Helium has seen interest by entities to offload onto its network. We are excited to see how these arrangements will evolve, and look forward to a world with ubiquitous 5G coverage.

More Resources

0 Comments