Proof of Gamer: How KGeN is Reimagining User Acquisition

FEB 18, 2025 • 44 Min Read

Report Summary

Key Takeaways

- Gaming Market Challenges: Distribution is a major hurdle as content saturation and consumer preference for established franchises make it difficult for new titles to succeed.

- Old Games Dominate Playtime: In 2023, the top 10 games by monthly active users (MAU) were over seven years old, and 60% of playtime on new releases was spent on franchises with yearly installments. Despite a record 19,000 new game launches on Steam in 2024, only 15% of total playtime was spent on games released that year, highlighting discoverability challenges.

- Global South Growth: Emerging markets in regions like India, SEA, LATAM, Africa, and MENA present untapped opportunities due to rising smartphone penetration and increasing disposable incomes.

- Web3 Gaming Struggles: The Web3 gaming market remains niche, with only 6-7 million unique active wallets interacting with over 3,000 on-chain gaming protocols—of which only about 200 have more than 100 active accounts.

- KGeN’s Unique Approach: KGeN utilizes a blockchain-powered Proof of Gamer (PoG) engine to build player reputations, incentivize engagement, and provide targeted user acquisition for publishers. KGeN’s PoG engine categorizes users based on engagement, skill, social influence, and monetization potential, creating a valuable dataset for advertisers.

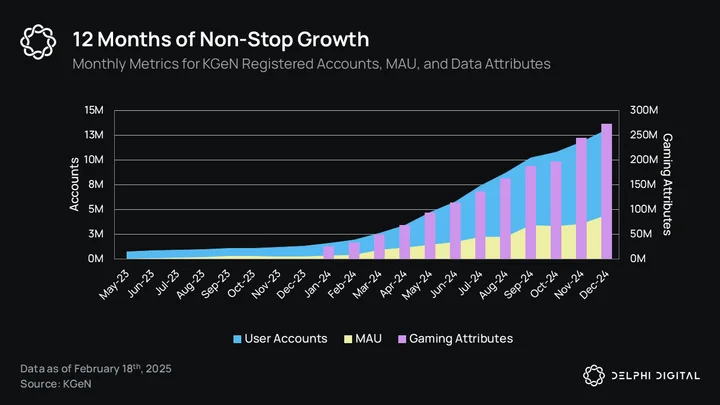

- KGeN’s Rapid Growth: Since January 2024, KGeN has grown its total number of registered accounts by over 700%, monthly active users (MAU) by 1333%, and total data attributes by 992%, making it the most active Web3 questing platform. KGeN has a network of over 2,525 clans, with 152 clans boasting over 100 members each. This grassroots approach has been instrumental in driving user acquisition, particularly in India.

- Approximately 1.7 million KYC’d (Know Your Customer) KGeN accounts have been acquired via clans, representing 39% of monthly active users. This emphasizes the platform’s focus on user verification and security.

- Future Success Factors: To maintain momentum, KGeN must optimize monetization, deepen data insights, and transition user motivations from financial rewards to intrinsic engagement within its ecosystem.

Introduction

The games industry, larger than film and music combined, currently faces a number of critical headwinds. Following a period of record growth during COVID-era lockdowns, 2023 and 2024 saw widespread layoffs and consolidation as development costs soared while investment waned.

Additionally, distribution is an increasingly prevalent challenge that is exacerbated by AI-driven content proliferation, platform saturation, and consumer preference for established franchises. Standing out and acquiring engaged users in an increasingly competitive market is more difficult than ever.

All that being said, several growth opportunities remain. Gen Z and Gen Alpha—digital-native generations that grew up in virtual worlds like Roblox and Minecraft–are expected to grow the industry further as they mature. These demographics

Moreover, the Global South–a collection of developing markets historically overlooked due to infrastructural and economic constraints–is now among the fastest-growing gaming markets. Over the next decade, these regions represent major untapped opportunities driven by smartphone penetration, improving internet infrastructure, and growing incomes.

This report’s first half explores the evolving challenges of game distribution while mapping high-growth opportunities in the Global South. The second half examines KGeN, a blockchain-powered gaming platform designed to reimagine incentive alignment between publishers and players. By assessing key incumbents, we evaluate the viability of Web3 questing platforms and the broader shifts in value distribution within gaming.

Challenges With Distribution

It is no secret that one of the largest challenges currently facing the games industry is distribution. A combination of changes in consumer habits, regulatory shifts, falling barriers to entry, and the subsequent saturation of gaming content has made it more competitive than ever to successfully scale a game to millions of users.

Gamers typically spend the majority of their time playing games/franchises they are familiar with, making it hard for new titles to break through. The top 10 games in 2023 by average monthly active users (MAU) were over seven years old, and 60% of playtime spent on new games was for franchises that have yearly releases. In 2024, despite seeing a record number of new releases launch on Steam (19,000 new launches), only 15% of gamers’ time was spent playing games released in that year.

The mobile landscape was historically one of more sophisticated distribution models. The rise of early mobile ad networks like Facebook and Google, combined with the proliferation of smartphones, helped scale many games to hundreds of millions of users and billions in annual revenues. However, in 2021, major changes were made to Apple and Google’s privacy policies, which directly impacted how publishers reached their target audience.

Although these changes did not bring an end to mobile advertising, they did drastically impact user acquisition (UA) strategies and mobile gaming business models. Many publishers have since found new ways to scale on mobile, but this is increasingly a game for the well-funded, with smaller teams struggling to compete.

Looking to the future, it seems increasingly unlikely that the state of play will improve. AI will indeed make managing UA campaigns easier and more efficient. However, this technology will equally reduce the barriers to entry and increase the amount of content available. UGC platforms, such as Roblox and Fortnite Creative, which have become common training grounds for indie developers, are already facing challenges with the curation and promotion of content on their platforms. AI is only going to accelerate these issues.

This brings us to the Web3 games market, where teams face a series of additional hurdles they must overcome. On top of the challenges outlined above, Web3 games must adhere to stricter platform policies on mobile, Steam (the largest distribution channel for PC games), and consoles. Web3 games are also outright forbidden in some key gaming markets, such as South Korea and China.

Note that the state of Web3 console distribution is deserving of a small caveat in that the recent release of Off The Grid has set a precedent for how Web3 games can launch on what was previously a “no-go zone” and we hope to see more games follow this path in the future.

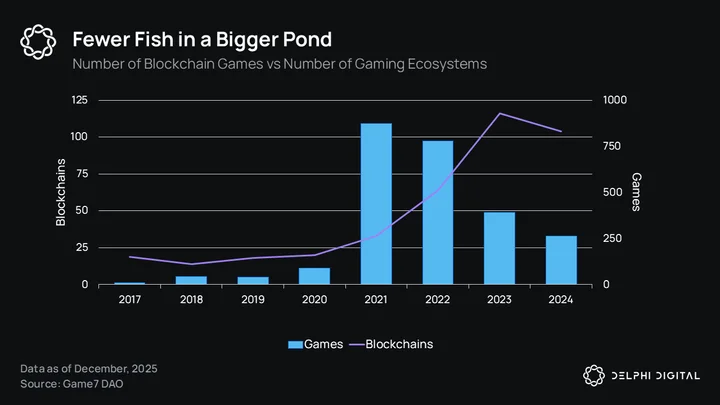

Additionally, the Web3 games market is still a niche sub-sector of the wider industry that has between an estimated 6M to 7M unique active wallet accounts interacting with over 3k on-chain gaming protocols. As always, it is important to note that these metrics do not account for bots, of which there are many in Web3, or the fact that only roughly 200 of these protocols have more than 100 active on-chain accounts.

The challenges faced by this relatively small market (remember there are over 3B gamers worldwide) are compounded by the fact that there has been an explosion of new Web3 gaming ecosystems launched over the past 24 months. Data from Game7 highlights that despite the number of new Web3 games declining by an average of 45% since 2021, the number of new networks has increased by an average of 187% over the same period. In 2024 alone, 104 new networks/ecosystems were announced next to just 263 new games.

The problem is that the majority of these new networks have failed at onboarding new gamers. The culmination of all of these issues has resulted in an ongoing theme we have detailed in multiple reports dubbed the fight for player liquidity. As all games continue to struggle in an increasingly competitive market landscape, Web3 projects are fighting over the same limited pool of wallets with few available options to help them break out of this bubble and scale.

The problem is that the majority of these new networks have failed at onboarding new gamers. The culmination of all of these issues has resulted in an ongoing theme we have detailed in multiple reports dubbed the fight for player liquidity. As all games continue to struggle in an increasingly competitive market landscape, Web3 projects are fighting over the same limited pool of wallets with few available options to help them break out of this bubble and scale.

In the face of all these adversities, a cohort of Web3 companies creating new blockchain-powered UA models has emerged. Novel incentive models and on-chain reputation systems both represent ways for companies to find competitive advantages via Web3 integrations.

Many of these Web3 companies have displayed significant product-market fit (PMF) in emerging markets. Looking past the increasingly saturated T1 markets which are dominated by Web2 incumbents, there are potentially huge opportunities for those that take advantage of blockchain’s globally accessible payment rails to fully unlock these new markets.

One of the more promising geographical regions that continues to grow at an above-average rate and has already displayed a high affinity for blockchain-integrated applications is the Global South.

The Global South

The Global South is a term used to describe countries that have a relatively low level of economic development and are generally located south of the more industrialized nations. Due to rapidly improving internet infrastructure, high levels of smartphone penetration, and growing disposable incomes, this broad region is often viewed as a largely untapped gaming market full of potential.

Gaming in the Global South is characterized by easily accessible large player bases playing predominantly on mobile devices with a relatively low appetite for spending. As such, these markets have historically been used by game publishers for soft-launch user acquisition testing and top-of-funnel vanity metrics.

However, the youth in these regions are the first generation to grow up with smartphones and have a high preference for consuming gaming content (categorized by games, video content, and esports). As this generation ages up and benefits from economic development and rising incomes, many believe that they will emerge as a new generation of paying gamers that propel the gaming industry to new heights.

Below we have highlighted some of the key characteristics of each of these markets to provide some perspective on the importance the Global South will play in the future of the games industry.

India

Despite its relatively slow start, India is sizing up to become the largest gaming market in the Global South. From a market of only 44.9M gamers in 2017, this figure is currently estimated to be roughly 466M and is expected to reach just over 640M by 2027. Market revenues were expected to grow by 13.6% in 2024 (reaching $943M), surpass $1B in 2025, and hit $1.4B by 2028, representing a 5-year CAGR of 11.1%. This growth is largely supported by growing habits around in-app purchases and a rising average revenue per paying user due to increasing disposable incomes across the country.

The market has a strong preference for mobile games in large part thanks to it being among the fastest-growing countries for 5G adoption and a widespread digital payments infrastructure called United Payments Interface (UPI), which saw transactions grow from 10.78B in 2019 to over 83.75B in 2023. Internet penetration has undergone similarly dramatic expansion, rising from 14% in 2015 to 52% currently, although this is far below some of the other promising gaming markets in the Global South, it does suggest significant growth potential.

These technological advances are complemented by strong macroeconomic fundamentals, including annual economic growth of 7-9% over the past three years and rising disposable income among its young, growing middle class.

Gaming preferences in India show distinct patterns that differ from other major markets. Mobile gaming commands a dominant 77.9% of total revenue, with PC and console gaming accounting for just 14.5% and 7.7% respectively. The current market composition reveals interesting revenue distribution patterns. Real Money Gaming (RMG) dominates the landscape with $2.0B in revenue, followed by casual and hypercasual gaming, which account for $700M, while other segments remain at $400M.

SEA

South East Asia (SEA), comprised of Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam, has one of the most mature gaming markets in the Global South. According to Niko Partners, the market generated $5.1B in gaming revenues, an 8.8% YoY increase, a figure that is expected to reach $7.1B by 2028, representing a 5-year CAGR of 6.7%. The region had 277M gamers in 2023 and is also expected to grow to 332M gamers by 2028, a 5-year CAGR of 3.7%.

In a report by Sensor Tower on the first half of 2024, Indonesia was recorded to be the country with the highest mobile game downloads (2.4B, 41% of the region’s total), and Thailand was the country with the highest IAP revenue ($400M next to Indonesia, the second largest, at $300M). However, despite the multitude of regional differences, common characteristics shared across all countries with the region include a love for community and competition. Word of mouth is the top source of information, and top-performing games typically have social features.

As with most countries in the Global South, smartphone penetration and the growth of broadband infrastructure are key factors in the strong market forecasts for the region. SEA, in particular, highlights this trend, with all major countries surpassing 80% smartphone penetration by 2022, with the average reaching 90.1% by 2026.

LATAM

LATAM is another notable mention with a large population and strong gaming culture, especially for esports. The region had an estimated 316M gamers in 2022 but this was highly concentrated in Brazil, which accounted for 101M gamers and $2.7B in game revenues that same year.

Unsurprisingly, the Brazilian market shows a high affinity towards mobile gaming, with 60% of players having interacted with the platform over a 6 month time frame. This segment is likely going to continue to grow over time, with smartphone penetration rates expected to reach 83% in 2025.

Monetization metrics highlight promising consumer behavior, with 43% of players spending money on games. The spending patterns reveal sophisticated consumer preferences, with primary motivations including unlocking exclusive content (39%), character customization (35%), and game progression (30%). This suggests a maturing market moving beyond basic monetization models.

Brazil is positioned to continue leading the region’s growth due to its positive education environment, with over 4000 gaming-related higher education courses available across 140 institutions. A recently passed legal framework is also expected to produce more game developers in addition to the current 1,042 studios (which generated an estimated US$251.6M in industry revenue in 2022), by officially recognizing it as a profession and providing various incentives, including tax benefits.

Africa

The African gaming market stands at a pivotal moment, with projected revenues expected to exceed $1B by 2024, up from $862.8M in 2022. The market’s foundation rests heavily on mobile gaming, which commands nearly 90% of the market share – a reflection of both infrastructure realities and consumer preferences. This mobile-first approach is partially validated by domestic research showing 92% of African gamers use phones for gaming, with significantly lower penetration rates for computers (51%) and gaming consoles (31%). However, considering the sample size of 2588, it would be difficult to definitively conclude how representative this data is for an entire content.

Infrastructure remains a critical bottleneck, with 42% of gamers citing data costs as a major barrier, followed by hardware expenses (31%) and connectivity issues (31%). Payment systems present both a challenge and an opportunity. While 63% of gamers have made game-related purchases, payment method preferences vary significantly by region. Kenya leads in mobile money adoption for gaming payments at 67%, while credit cards (45%) and mobile money (40%) compete as preferred payment methods across the continent.

MENA

The MENA gaming market stands as a testament to rapid digital transformation, emerging as the world’s fastest-growing games market with an impressive 4.7% revenue growth to reach $7.1B in 2023, significantly outpacing the global market’s 0.6% growth. This expansion is expected to continue, with projections suggesting a CAGR of 9.4% from 2024 to 2030.

The MENA-3 region is expected to reach $2.9 billion in gaming revenues by 2027, representing an 8.2% CAGR. Several key drivers support this growth, including a large youth population, strong improvement in digital inclusion rates in countries like Qatar and the UAE, and consistent adoption of new technologies.

The region’s gaming landscape is dominated by three powerhouse markets – Saudi Arabia, UAE, and Egypt – collectively known as MENA-3, which demonstrated exceptional performance with 7.8% year-over-year growth to $1.92B in 2023 and forecasts predicting this will reach $2.9B by 2028, representing an 8.3% five-year CAGR. Saudi Arabia leads the charge, accounting for 60.6% of total gaming revenue and 30.3% of total MENA gamers, showcasing the kingdom’s dominant position in the regional ecosystem.

Mobile gaming has emerged as the cornerstone of the MENA gaming market, with 87.2% of gamers preferring smartphones as their primary gaming device and dedicating an average of 8.7 hours per week to mobile gaming. This preference is reflected in the revenue distribution, with mobile gaming generating $998M in 2023, console gaming at $551.2M, and PC gaming at $375M.

What is KGeN

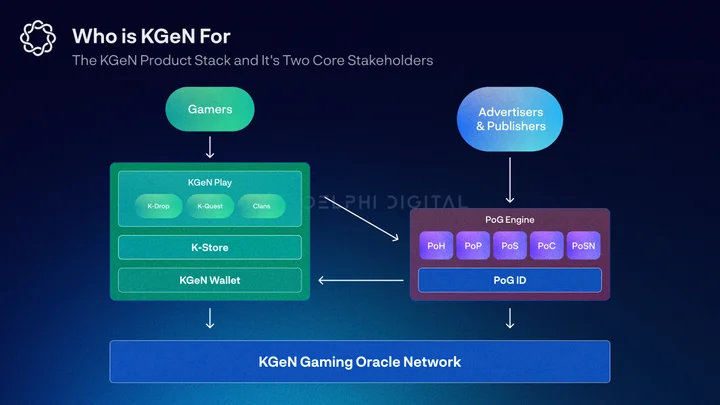

KGeN is a blockchain-powered gaming platform that leverages on-chain and off-chain data, an incentivized questing platform, and a decentralized reputation system to drive engagement across different games. Unlike other UA platforms, KGeN distributes publisher dollars back to its users, fueling its growth flywheel.

At the core of the platform lies a decentralized gamer data network that scales across millions of micro-gaming communities (KGeN clans). The network leverages a novel data model called the Proof of Gamer (PoG) engine that creates a cross-chain player reputation layer and provides publishers with highly engaged targetted user cohorts at a lower cost than many other incumbents.

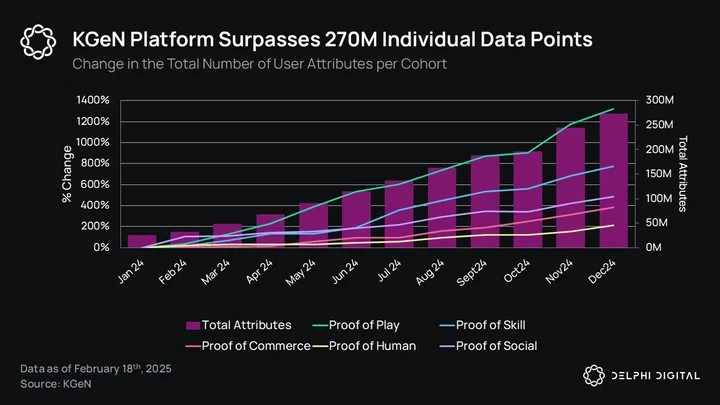

As more players are onboarded to the platform and the PoG dataset grows, more studio and publisher partnerships are established. This further fuels the ecosystem rewards, which in turn increases the value for engaged players. This growth flywheel has already demonstrated its effectiveness, growing the total number of registered accounts by over 700%, MAU by 1333%, and total data attributes by 992% since January 2024. This makes KGeN the most active Web3 questing and gamer reputation platform on the market.

As more players are onboarded to the platform and the PoG dataset grows, more studio and publisher partnerships are established. This further fuels the ecosystem rewards, which in turn increases the value for engaged players. This growth flywheel has already demonstrated its effectiveness, growing the total number of registered accounts by over 700%, MAU by 1333%, and total data attributes by 992% since January 2024. This makes KGeN the most active Web3 questing and gamer reputation platform on the market.

The KGeN ecosystem is now in the process of progressive decentralization across a network of distributed Oracles that secure the PoG engine and provide increased levels of transparency for all core stakeholders. This Oracle network, along with the KGeN Store, is powered by the KGEN token.

The KGeN ecosystem is now in the process of progressive decentralization across a network of distributed Oracles that secure the PoG engine and provide increased levels of transparency for all core stakeholders. This Oracle network, along with the KGeN Store, is powered by the KGEN token.

Grassroots Growth

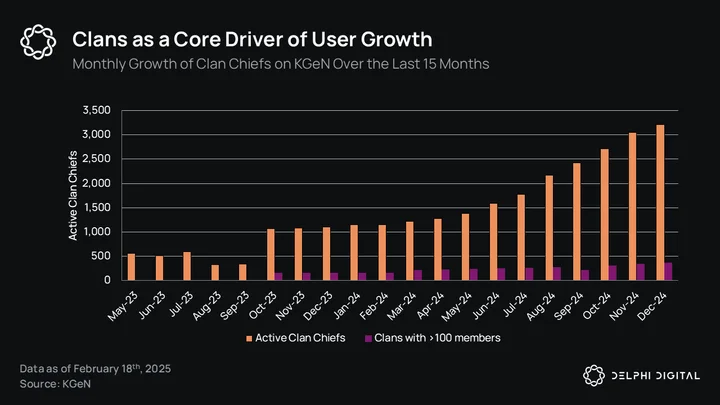

At the core of KGeN’s growth, and what will help them continue to scale across the Global South, is their grassroots network of clans and clan chiefs. Clans represent the thousands of micro-communities that have joined the KGeN ecosystem, such as colleagues, esports orgs, influencers, and gaming-focused social groups. As of December 2024, KGeN has a self-reported total of 2,525 clans, 152 of which had over 100 members.

Clans are one of the core ways KGeN drives referral-based user acquisition. At the time of clan creation, clan chiefs are rewarded points for inviting up to five clan members and having them complete at least one quest. These points feed into the KGeN leaderboard, one of KGeN’s primary reward systems (more on this later). This incentives-driven funnel has proved incredibly effective, with roughly 1.7M KYC’d KGeN accounts (39% of MAU and 13% of total registered accounts) being acquired via clans.

Clans are one of the core ways KGeN drives referral-based user acquisition. At the time of clan creation, clan chiefs are rewarded points for inviting up to five clan members and having them complete at least one quest. These points feed into the KGeN leaderboard, one of KGeN’s primary reward systems (more on this later). This incentives-driven funnel has proved incredibly effective, with roughly 1.7M KYC’d KGeN accounts (39% of MAU and 13% of total registered accounts) being acquired via clans.

Not only are clan chiefs incentivized to onboard new members, but they must also coordinate clan activities and maintain community engagement if they want to maximize their earning potential. This is because a percentage of total clan earnings flows back to clan chiefs, making this one of the platform’s key growth incentive mechanisms.

KGeN’s largest market by far is India due to the company’s origins and its strong presence across micro-gaming communities in the region. That said, over 30% of unique active wallets and transactions occur on Kaia, the LINE messaging app’s proprietary blockchain. LINE’s largest markets are Japan (86M users), Thailand (47M users), Taiwan (21M users), and Indonesia (13M users), which could suggest strong growth potential in Asia.

To replicate the success seen in India in other markets throughout the Global South, KGeN is encouraged to take a similar grassroots approach to growth. Partnering with local gaming micro-communities, such as schools, internet cafes, small esports orgs, and online communities, will allow them to slowly expand their reach while also creating opportunities to deepen social dynamics and further drive engagement and retention.

Another potential concern is the relative lack of social features available for clans on the KGeN PC portal and mobile app. As we will go into detail later in the report, adding social features is one way to increase engagement on the platform. More time on the platform equates to richer user data, more opportunities for users to interact with K-Quest and K-Drop features, and a larger surface area for monetization.

Incentivizing Engagement with KGeN Play

KGeN Play is the front end for the majority of gamer engagement on the platform and where all rewarded quests are posted. This typically marks the beginning of the user journey and will remain the main portal users interact with as they build their PoG reputation score.

KGeN Play is accessible via the PC portal or mobile app. Users will have the best experience via the PC portal, but the mobile app does provide a quick solution for those on the move and will prove a vital platform for scaling across the Global South.

Upon account creation, a blockchain wallet is automatically created on the backend, which stores all of the user’s assets as well as their non-tradable player reputation NFTs. Once the minimum withdrawal threshold is reached, users are prompted to verify a phone number via OTP and take full custody of their wallet – a crucial step that feeds directly into the PoG engine. The KGeN Wallet is limited in its features set but has a smooth onboarding flow with multichain support, and gasless transactions, and performs its main three functions (check balance, check transaction history, and withdraw) with low friction.

Before a user realizes they have a blockchain wallet, they will first need to start earning rewards. To do this, users engage with various campaigns posted on the KGeN Play portal. Quest campaigns are bucketed into K-Drops and K-Quests.

Before a user realizes they have a blockchain wallet, they will first need to start earning rewards. To do this, users engage with various campaigns posted on the KGeN Play portal. Quest campaigns are bucketed into K-Drops and K-Quests.

K-Drops and K-Quests are both time-gated limited-entry campaigns that reward participants with K-Points, leaderboard-based achievements, K-Cash, or tokens. The core difference between the two is that K-Drops offer automated real-time validations via end-point API integration and K-Quests go by a manual validation process.

It should be no surprise that questing platforms leveraging real-world financial incentives (especially those targeting users based in the Global South) experience above-average completion rates. What sets KGeN apart from the competition is how it combines KGeN Play with its PoG engine to deliver targeted campaigns that produce high conversion rates.

It should be no surprise that questing platforms leveraging real-world financial incentives (especially those targeting users based in the Global South) experience above-average completion rates. What sets KGeN apart from the competition is how it combines KGeN Play with its PoG engine to deliver targeted campaigns that produce high conversion rates.

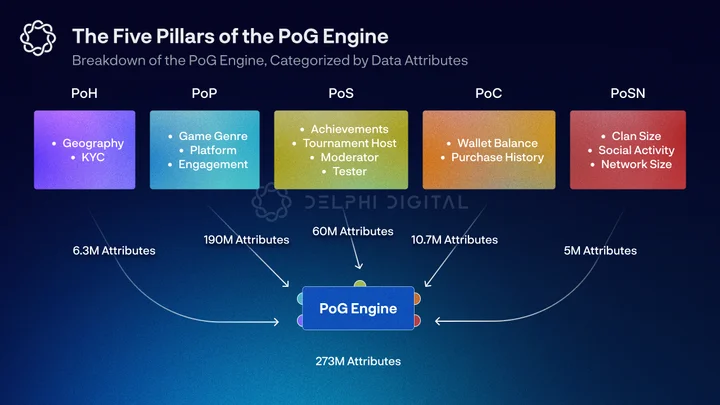

The PoG Engine

The PoG engine is a decentralized gamerscore hosted by a distributed network of nodes. The PoG consists of five core pillars, which are made up of five to ten attributes each. These data points track a gamer’s skill, “humanness,” level of engagement, wealth, and social network to build a multifaceted multichain reputation system.

This culminates in a PoG vanity score that benefits from blockchain technology’s inherent composability as players flaunt their gamer ID across different ecosystems. Meanwhile, publishers and advertisers can leverage the PoG engine to access competitively priced engaged player cohorts throughout the Global South.

The five core pillars are broken down into Proof of Human (PoH), Proof of Play (PoP), Proof of Skill (PoS), Proof of Commerce (PoC), and Proof of Social Network (PoSN).

- PoH is as it sounds – It tracks a variety of data points that reduce the likelihood of a user being a bot. This could include KYC status or the number of connected social apps and is one of the most valuable attributes in the eyes of publishers. In addition to tracking “humanness”, PoH further segments user cohorts by platform preferences and geography. This pillar not only helps with user targeting but also establishes greater trust in the quality of acquired users and the network as a whole.

- PoP ascertains a player’s engagement with the KGeN platform as well as the types of games they have played. It tracks metrics related to retention, play patterns, preferences, and user habits. This pillar improves targeting by further segmenting different user types and is another highly valued set of attributes for publishers.

- PoS celebrates a player’s abilities, competitiveness, engagement, and growth over time. It takes data from in-game achievements, tournaments, and platform campaigns to rank players. This pillar highlights the most engaged players and provides them with social capital.

- PoC identifies a user’s monetization potential. This could be from direct purchases, on-chain transactions, on-chain history, or net worth. Not only does this improve targeting and UA campaign efficiency but it also showcases the different ways users can add value. Aside from early-stage campaigns, such as playtests, PoC will ultimately be the most valuable dataset for publishers in a post-IDFA world.

- PoSN maps the size of users’ social profiles and establishes their social graph within the KGeN platform. This pillar filters out non-gaming data and tracks social accounts, clan activity, and network size to understand their social preferences, reach, and influence within the gaming community.

The PoG engine currently consists of over 270M data attributes, collected from over 13M total registered accounts, and 4.4M MAU. PoH, PoP, PoS, PoC, and PoSN cohorts have increased by roughly 214%, 1320%, 777%, 384%, and 487%, respectively, since January 2024. The growth in PoP and PoS-related data in particular stands out by illustrating how on-platform engagement has continued to increase over time.

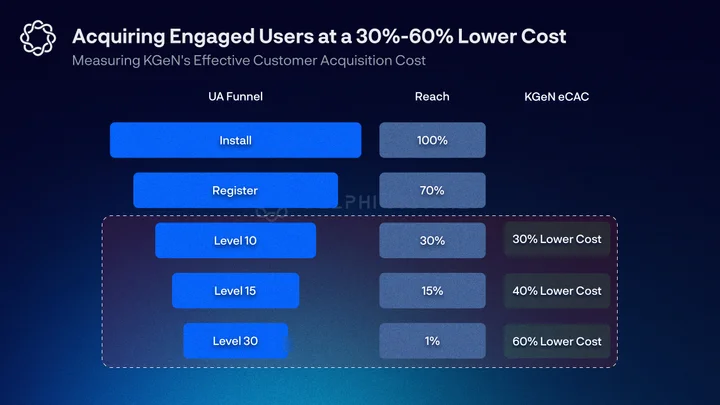

Leveraging the PoG engine, KGeN is spearheading an alternative framework for UA called “effective customer acquisition cost” (eCAC). Instead of charging for simple impressions or top-of-funnel installs, KGeN only charges clients for engaged users that reach the middle or bottom of the user funnel.

Leveraging the PoG engine, KGeN is spearheading an alternative framework for UA called “effective customer acquisition cost” (eCAC). Instead of charging for simple impressions or top-of-funnel installs, KGeN only charges clients for engaged users that reach the middle or bottom of the user funnel.

For example, in a campaign with Karate Combat, KGeN reports an almost 40% decrease in eCAC, while charging nothing for top-of-funnel installs, and a 5% bottom-of-funnel conversion rate. During a four-week quest campaign with Game7, KGeN states they helped onboard 50k PoH-verified users at a 55% lower eCAC compared to its competitors. User registration, wallet connects, and avatar creation events were all free of charge, meaning the client only paid for users who completed a minimum of four tasks and minted an SBT (at an estimated 20% conversion rate).

For example, in a campaign with Karate Combat, KGeN reports an almost 40% decrease in eCAC, while charging nothing for top-of-funnel installs, and a 5% bottom-of-funnel conversion rate. During a four-week quest campaign with Game7, KGeN states they helped onboard 50k PoH-verified users at a 55% lower eCAC compared to its competitors. User registration, wallet connects, and avatar creation events were all free of charge, meaning the client only paid for users who completed a minimum of four tasks and minted an SBT (at an estimated 20% conversion rate).

PoH and PoP cohorts are particularly valuable as these data points provide business clients with comparatively higher engagement ROI. This is especially true for Web3 projects that leverage financial incentives and regularly suffer from bad actors and bots. However, none of these data points are perfect and even KYCs can be manipulated.

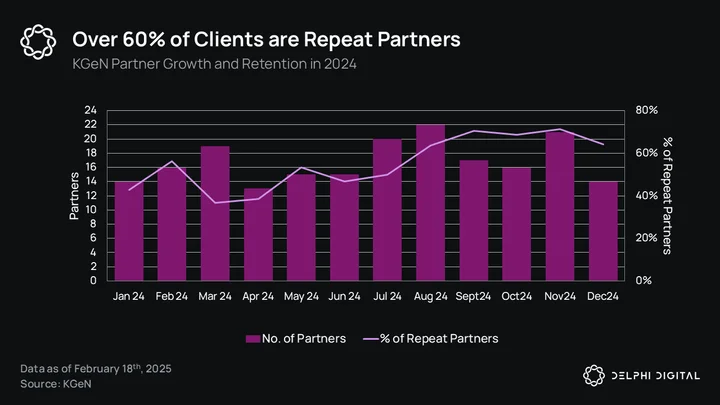

That said, KGeN’s ability to ascertain to a high level of certainty the quality of their users is a huge value add to their partners. As we will go on to explain in more detail later in the report, advertising fraud is responsible for approximately $84B in wasted digital advertising spend. This is also a large reason why since August 2024, over 60% of KGeN’s partners have been repeat clients.

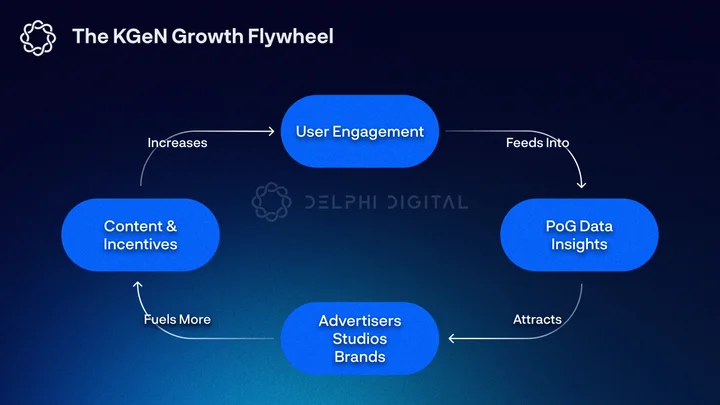

Over time, the growth flywheel that is crucial for KGeN’s future scalability should gain momentum. Provided there is demand for a positive PoG score, engagement across KGeN Play should increase (this can be further accelerated by PoG score-based financial incentives). This activity will feed the PoG engine, increasing the total number of attributes and enriching KGeN’s user database. Subsequently, more publishers will be attracted to the ecosystem, increasing the variety of offerings across KGeN Play and KGeN Store, which in turn attracts more users.

Over time, the growth flywheel that is crucial for KGeN’s future scalability should gain momentum. Provided there is demand for a positive PoG score, engagement across KGeN Play should increase (this can be further accelerated by PoG score-based financial incentives). This activity will feed the PoG engine, increasing the total number of attributes and enriching KGeN’s user database. Subsequently, more publishers will be attracted to the ecosystem, increasing the variety of offerings across KGeN Play and KGeN Store, which in turn attracts more users.

The PoG score is at the core of KGeN’s business model and how it can offer clients a competitively low-cost eCAC. A crucial question is what are the incentives that drive this user behavior?

The PoG score is at the core of KGeN’s business model and how it can offer clients a competitively low-cost eCAC. A crucial question is what are the incentives that drive this user behavior?

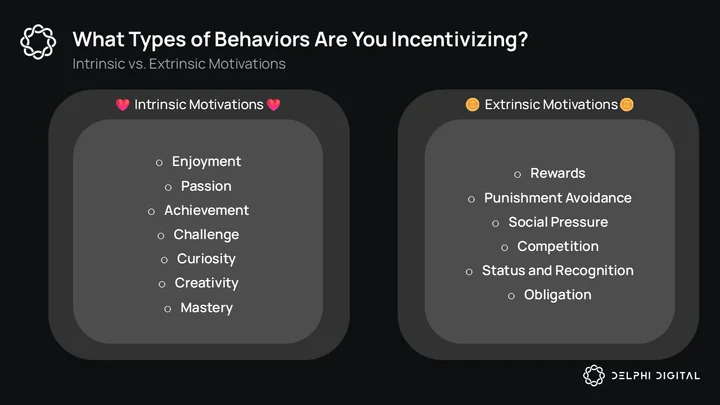

For as long as they are financial, the platform is undoubtedly going to show promising results. However, this creates extrinsic motivational forces that dictate how users engage with the platform and its partners.

Extrinsically motivated users are unlikely to keep playing a game they were first attracted to because of the rewards. Additionally, studies have shown that offering extrinsic rewards for something that was originally internally rewarding for the individual will reduce intrinsic motivation – also known as the overjustification effect.

Intrinsically motivated users search for value in the things they enjoy, such as social interactions, recognition and respect, progression, and fun. If, over time, strong network effects can change the core value proposition of the PoG score to something that is rooted in social capital and enjoyment then motivations will increasingly become intrinsic, which increases the potential value delivered to partnered publishers.

Intrinsically motivated users search for value in the things they enjoy, such as social interactions, recognition and respect, progression, and fun. If, over time, strong network effects can change the core value proposition of the PoG score to something that is rooted in social capital and enjoyment then motivations will increasingly become intrinsic, which increases the potential value delivered to partnered publishers.

KGeN Token Economy

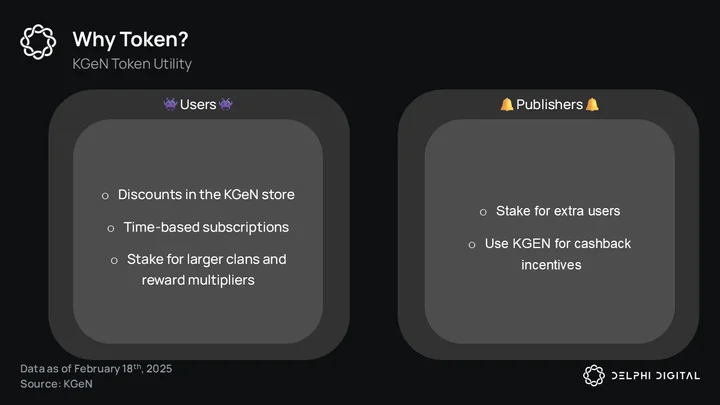

KGeN’s economy will feature two core assets, KCash, and the KGEN token. KCash has been live for some time now and is an off-chain asset used predominately as a rewards currency, but it can also be directly purchased with fiat. KCash’s main utility is within the KStore, where it can be used to purchase IAPs, gift cards, or enter VIP tournaments and quests.

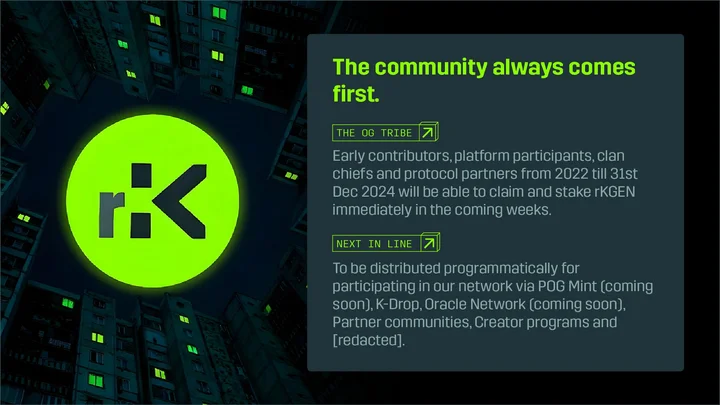

Fueling the flywheels of growth across the KGeN ecosystem is the KGEN token. A utility token with a healthy community allocation of 40% (8% of which is unlocked at TGE), and a four-year vest for the team and investors. A total of 12.6% of the token supply will be unlocked at TGE, however, this does not account for any circulating supply that is effectively locked with market makers or exchanges.

It was recently announced that in the lead-up to TGE, KGeN will leverage a K-Point -> rKGEN airdrop campaign. rKGEN allocations are derived from one’s total K-Points, time on the platform, and affiliations. rKGEN will be transferable into KGEN tokens at a 1:1 ratio once the token is live. However, select users will be able to start staking their rKGEN pre-TGE for additional token yield.

The K-Points -> rKGEN airdrop model prioritizes transparency and clear communication in an attempt to maximize community sentiment and token distribution in the lead-up to TGE. If executed successfully, this could help build momentum and secure additional CEX listings at launch but it comes with its own risks.

The K-Points -> rKGEN airdrop model prioritizes transparency and clear communication in an attempt to maximize community sentiment and token distribution in the lead-up to TGE. If executed successfully, this could help build momentum and secure additional CEX listings at launch but it comes with its own risks.

Ambiguous reward systems have been shown to increase engagement across a wide variety of different genres. A pure points airdrop campaign, while less transparent, provides teams with more flexibility when it comes to distributing a token airdrop. This same design concept raises the question of whether post-TGE, KGeN Play campaigns will leverage a K-Points -> KGEN reward system or simply direct token payouts.

At launch, we assume that the KGEN token will predominantly be used for incentives. However, over time as the platform matures, we expect more users to spend the token in the KGeN Store to access discounted rates compared to purchases made in fiat.

At launch, we assume that the KGEN token will predominantly be used for incentives. However, over time as the platform matures, we expect more users to spend the token in the KGeN Store to access discounted rates compared to purchases made in fiat.

Another potential token sink could be in the form of subscription fees. At some point, as users become increasingly sticky to the platform that hosts their reputation score, gaming achievements, and social touchpoints, KGeN may decide to gate the number of quests available to F2P users. This would effectively gate much of the earning potential on the platform and act as an additional bot protection.

That said, unless the non-financial rewards hold significant intrinsic value to users, many will not spend the token unless they can achieve a positive ROI. To prevent this from becoming an inflationary sink (one that emits more tokens than it removes), KGeN should offer third-party tokens, KCash, or NFTs instead. Ultimately, the most sustainable sinks are those that are driven by internal motivations such as entertainment and social capital.

In addition to direct token sinks, there will also be token staking. Aside from those seeking a straightforward staking yield, a feature that goes live with rKGEN pre-TGE, clan chiefs can stake tokens to increase their membership cap and gain access to additional platform tools. Publishers can also engage in a tired staking program to access more free top-of-funnel users in their UA campaigns – a feature we expect will see increasing amounts of interest provided the platform continues its current growth trajectory.

Typical token staking is an inflationary model that ultimately dilutes the token supply in exchange for delaying selling pressure. Despite the potential short-term benefits, it is great to see KGeN leverage non-inflationary staking incentives for clan chiefs and publishers.

Oracle Network

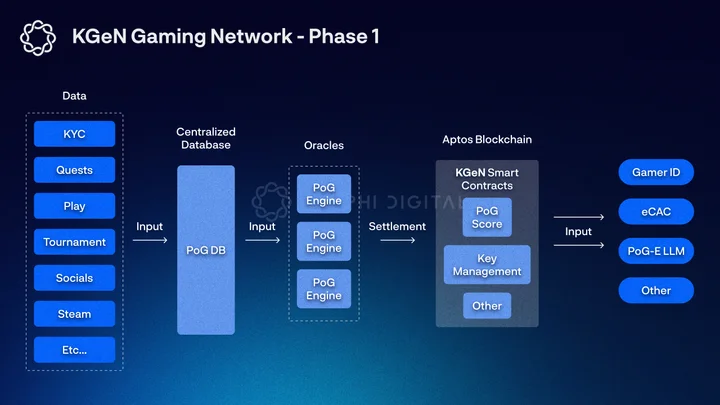

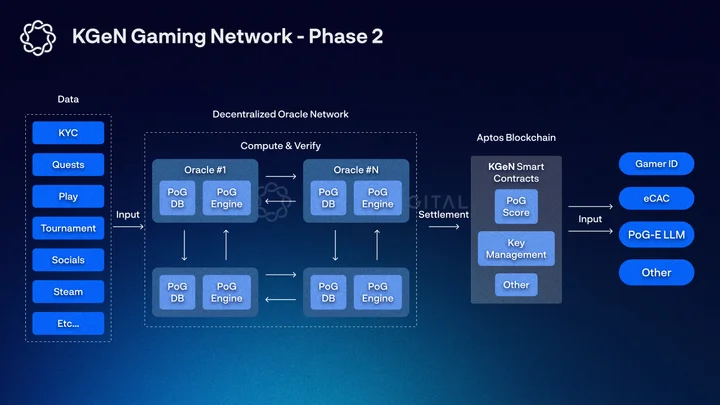

The KGeN Oracle network is a distributed web of permissioned nodes that will collectively form the backbone of the PoG engine. Each Oracle is tasked with storing PoG data, computing PoG scores (and collectively verifying their accuracy), and submitting these scores to the Aptos blockchain for settlement. In return for providing this service, Oracle operators are rewarded with a fixed KGEN token yield based on revenue forecasts, along with stablecoin yield relative to the amount invested in the Oracle.

The Oracle network is ultimately taking a process that would typically happen in a centralized manner and decentralizing various aspects of it. This will be a progressive process that is expected to take at least three years. During phase one, Oracles will primarily retrieve PoG data from centralized servers and engage in computation, validation, and settlement – decentralized storage of the PoG data will commence in phase two.

The Oracle network is ultimately taking a process that would typically happen in a centralized manner and decentralizing various aspects of it. This will be a progressive process that is expected to take at least three years. During phase one, Oracles will primarily retrieve PoG data from centralized servers and engage in computation, validation, and settlement – decentralized storage of the PoG data will commence in phase two.

Another core component of the Oracle network is Oracle Keys. Keys are NFTs that are required to participate in the network. The more an authorized Oracle operator spends on their Oracle license, the more Keys they are granted. KGeN has also stated there may be additional Keys sales available to the public at a later date.

Another core component of the Oracle network is Oracle Keys. Keys are NFTs that are required to participate in the network. The more an authorized Oracle operator spends on their Oracle license, the more Keys they are granted. KGeN has also stated there may be additional Keys sales available to the public at a later date.

Oracle Keys will remain account-locked until the network transitions to phase two, at which point they will be tradable and Key holders can delegate their Keys to Oracle operators. Key delegation is akin to a typical staking mechanism that temporarily locks Key NFTs in exchange for KGEN token yield derived from the Keys reward pool.

An Oracle’s weight within the Keys rewards pool is calculated based on three variables, the number of Keys staked to the Oracle, the protocol’s base rewards, and the Oracle’s performance. Performance is only relevant once KGeN transitions to phase two and specifics on how it is calculated are still TBC. Base rewards are emissions-based and an indicator of overall network health. Although specifics are yet to be confirmed, the goal is for base rewards across all Oracles to increase as the network value grows.

The Oracle network combines facets from both nodes and delegated proof-of-stake frameworks to decentralize the PoG engine. Under an entirely centralized framework, KGeN’s centralized data centers represent a single point of failure for data corruption or removal. Additionally, core stakeholders (namely gamers and publishers) hold a number of trust assumptions that these PoG scores have not been manipulated.

The benefits of decentralization in this case are fairly subjective to the user. In some circles, it might be hard to find a gamer who actively complains about the centralized nature of their Xbox Gamerscore or Steam account. Similarly, publishers are primarily concerned about scalable UA rather than decentralization.

However, this overlooks the potential network effects and aligned incentives a token model can help achieve. By providing stakeholders with an avenue to benefit from the upside of KGeN’s growth, you create brand advocates who will support the project. Under the assumption that KGeN’s growth flywheel translates into positive token price action, more stakeholders will be attracted to the ecosystem, which will further accelerate network effects.

Competitive Landscape

KGeN is not alone in its ambitions. As we have already discussed, distribution is viewed by many as one of the biggest challenges currently facing the games industry. Whether it is scaling UA campaigns profitably or improving core engagement metrics by boosting player liquidity, several incumbents are tackling these issues to varying levels of success.

We will now highlight a selection of companies operating in both Web2 and Web3 markets to compare and contrast business models, outline opportunities, and highlight some key considerations.

The King of Ad-Tech: Past and Present

In Web2 markets, two case studies stand out as having several synergies with KGeN’s current business model as well as highlighting some key opportunities for future growth. The first is Facebook due to its historic focus on deep user profiling and behavioral analysis. The second is Applovin, an ad-tech business with its foot on both sides of the mobile advertising market, gaining significant market share in the mobile UA landscape due to its sophisticated AI-powered toolset.

Facebook:

After some years of experimenting with alternative forms of advertising, Facebook found its footing at the tail end of the Facebook web gaming era and the emergence of the reign of mobile.

Companies like King (Candy Crush Saga), Playtika (Solotomania), and Zynga (Farmville), which had built successful games on Facebook’s web platform, began seeking ways to expand beyond organic traffic. These gaming companies started spending unprecedented amounts on Facebook ads, to the extent that for the first 6 months of 2011, Zynga accounted for 12% of the platform’s revenue.

Between 2013 and 2016 Facebook focused increasingly on mobile advertising and by 2014, it had taken just under 30% of mobile ad market share, up from 0% two years prior – becoming the defacto number 2 behind Google.

Facebook’s ad business found success by tracking user behavior, game engagement, and purchase patterns to optimize targeting and ad delivery. The platform’s value came from its ability to identify and target high-value users who were likely to engage and spend in games, and developers willing to pay premium rates for this targeting capability.

Facebook enhanced this through their SDK integration with games, allowing them to track post-install events and optimize for downstream metrics like return on ad spend (ROAS). This business model also benefited from Facebook’s social features, which provided additional organic user acquisition channels.

In some respects, KGeN follows a similar strategy to Facebook in that data on player habits and behaviors are core to its value proposition. However, it should be noted that Facebook focused on much more casual titles for its hundreds of millions of users. KGeN, on the other hand, is much more focused on mid-core + hard-core game genres, which is reflected in their entirely gaming-oriented user base.

In order to further assimilate itself as the decentralized Facebook ads network, KGeN could invest more into improving its platform/app social features (something they plan to roll out over time with new messaging and tournament features). This would not only increase the amount of data on the user journey, preferences, and behaviors outside of engaging with quests but also introduce additional distribution channels for publishers on the platform.

Applovin:

AppLovin is a sophisticated ad-tech platform that monetizes through optimized ad delivery and performance metrics while leveraging its Supply-Side Platform (SSP) data for pricing intelligence. The company operates on both sides of the mobile advertising market:

- Through its SSP, MAX (which is supplied with huge amounts of data thanks to acquisitions of MoPub, Machine Zone, and its in-house studio Lion Studios), Applovin helps game developers sell their ad spaces at optimal prices.

- Its Demand-Side Platform, AppDiscovery, helps publishers purchase this inventory based on their user acquisition targets and cost metrics.

The company’s data-driven competitive advantage strengthened after Apple’s App Tracking Transparency (ATT) privacy changes disrupted traditional user-level tracking. In a world where individual user tracking was no longer allowed, Applovin’s aggregated end-to-end data was a compliant way to provide publishers with a valuation metric for users at any given point in time in any category of games.

The crown jewel of the Applovin ecosystem is their machine learning engine called AXON, which analyzes user behavior data from mobile apps, along with platform bid data to predict which apps users will most likely download and engage with.

As a data platform, this two-sided structure gives AppLovin an edge because they are being fed information both by those who want to purchase ad space and those selling ad space in games. The company has visibility into market dynamics and pricing data, allowing it to provide unparalleled levels of data insights and campaign optimization.

There is no denying that Applovin’s ad-tech platform is more mature and more scalable than what KGeN currently has to offer. However, similar to Applovin, there is an opportunity for KGeN to work directly with its partners to either implement their own SDK into their games or have the games’ databases flow back into the PoG engine.

This would greatly enrich the PoG database while also allowing for better tracking of campaign success. This more robust dataset would also be highly beneficial for the recently announced POG-E LLM, an augmented LLM trained on KGeN’s proprietary data, which could be leveraged in a way similar to AXON to deliver more relevant quests to players who are more likely to convert into payers.

Mystplay:

Mystplay is a leader in the rapidly growing sector of Web2 rewarded UA platforms. At its core, Mystplay is a standalone discovery app where users can engage with the different games on the platform to earn points, these points can then be later redeemed for gift cards.

Rewarded UA platforms are a growing trend in the games industry and 68% of developers believe they have seen better ROAS from reward-based campaigns compared to other UA channels. These platforms claim higher-than-average retention and revenue from their acquired users, with Mistplay stating that rewarded users produce 20-50% higher 7-day retention or ROAS in certain case studies. Other notable rewarded UA platforms include Adjoe, Almedia (Freecash), Tapjoy, MyAppFree (MAF), and others.

What sets Mystplay apart is a combination of rich social features (chats, weekly contests, and leaderboards) and an AI-powered recommendations engine that matches players with games they are more likely to enjoy and spend longer in. Mystplay’s loyalty-driven UA approach and focus on quality over quantity has led to rapid growth over the past 24 months.

The company has ~16M registered users (as of 2022), over 2M MAU, and a growing collection of more than 400 game partners in 2023, and they are frequently ranked as a top 10 publishing platform in terms of performance and ROI (on Android). Annual revenues are estimated at around $55M, headcount has increased roughly 43% in the last year, and the platform achieved 445% growth over four years, earning a spot on Deloitte’s Tech Fast 50 in 2024.

On the surface, Mystplay has a very similar value proposition to KGeN. However, the focus on Western Tier 1 markets and the lack of globally accessible blockchain payment rails have forced the company to take a quality-over-quantity approach to rewarded UA. In this regard, the platform’s ability to leverage AI-driven targeting to increase conversion rates and boost retention is something that KGeN would benefit greatly from adopting.

Web3 Competitive Landscape:

When it comes to the Web3 market, competitors can be broadly categorized as either publisher ecosystems or questing platforms. Both are ultimately trying to accomplish the same goal: drive user growth across partnered projects.

Web3 Publisher Ecosystems:

Publisher ecosystems typically focus on providing partners with strategic support for optimizing Web3 UA, supplying token grants that can then be spent on UA, or leveraging ecosystem token emissions for UA incentives. A small selection of ecosystems leveraging one or more of these models include Ronin, Immutable, Xai, and Catizens, each with a fully diluted token valuation (FDV) of $1.65B, $2.34B, $288.2M, and $261.6M, respectively.

Several fundamental differences between publisher ecosystems and KGeN mean that they are not direct competitors. Publisher ecosystems tend to monetize via a fee structure that is foundationally driven by developer activity, whereas KGeN is focused on “owning” the user journey and can operate at a chain and game-agnostic level. One could argue that this platform-agnostic approach increases KGeN’s TAM by allowing them to avoid chasing zero-sum exclusivity agreements.

However, as mentioned in the above spotlight section on Applovin, in its current form, KGeN often misses out on a lot of valuable data points once users arrive at their destination (inside the game or application). Publisher ecosystems, like Ronin, have a lot more end-to-end visibility on user activity, especially on-chain data and wallet profiling. The leverage gained from providing funding and infrastructure support to applications further entrenches this competitive moat.

Questing Platforms:

Rewarded quests are frequently leveraged by Web3 projects across all sectors in order to grow mindshare and distribute assets to stakeholders. This is especially true for gaming projects that want to turbocharge growth with UA incentives, boost retention via rewarded engagement, and maximize protocol activity.

Rewarded quests are frequently leveraged by Web3 projects across all sectors in order to grow mindshare and distribute assets to stakeholders. This is especially true for gaming projects that want to turbocharge growth with UA incentives, boost retention via rewarded engagement, and maximize protocol activity.

The key advantage of questing platforms is that they aggregate quests from multiple projects, providing users with a one-stop shop for all questing activities and publishers with a wider potential reach.

In its current form, KGeN is a quest discovery platform that competes with other Web3 questing platforms for attention. Its strong grassroots presence in India and Brazil has provided KGeN with a first-mover advantage in these markets. However, that does not guarantee their continued success. The below analysis will double-click on what makes a successful blockchain-powered questing platform and highlight the strengths and weaknesses of KGeN’s approach.

Competitive Analysis

At their core, all questing platforms offer the same “quest-to-earn” service. Where they differ is in their scale and ability to provide value-driven results for publishers.

The demand for value-driven UA results has never been higher. Not only is distribution a growing challenge, but every year huge amounts of UA spend are wasted on low-quality engagement. It has been reported that bots in particular were the cause of an estimated $84B in wasted digital advertising spend in 2023.

Although fraud is less of an issue on self-reporting networks (SRNs) that own their ad inventory (like TikTok, Snapchat, and Instagram), wherever last-click models are used for the attribution of large-scale campaigns, there will be bad actors. Some incumbents, such as Applovin, are attempting to quell bot-related criticisms from gamers and publishers by partnering with third-party anti-fraud tech solutions. However, publishers and advertisers engaging in programmatic ads still require a level of trust in the ad platform.

For KGeN, results are driven by the PoG engine (and more specifically the PoH and PoP scores), which act as a critical competitive advantage for the company in a market with notably high levels of bot activity. By progressively decentralizing the PoG engine, KGeN is attempting to lessen any remaining trust assumptions. The demand for these verifiably engaged players is evident, as illustrated by the company’s growing revenue and high percentage of repeat clients.

All that said, eCAC alone is not as valuable as ROAS when measuring the relative success of a UA campaign. It is important that KGeN is able to monetize its users, accrue more data from across the user journey (especially for PoC attributes), and leverage this data to provide partners with effective targeting and optimizations that lead to profitability.

Looking past a platform’s ability to provide value-driven results, we can make a number of assumptions as to how Web3 platforms compete at scale with one another.

Provided switching costs are low and financial incentives are abundant, we can assume that the same users will attempt to engage with all platforms. When time becomes the leading constraint, users will allocate their energy to the campaigns that have the highest potential ROI.

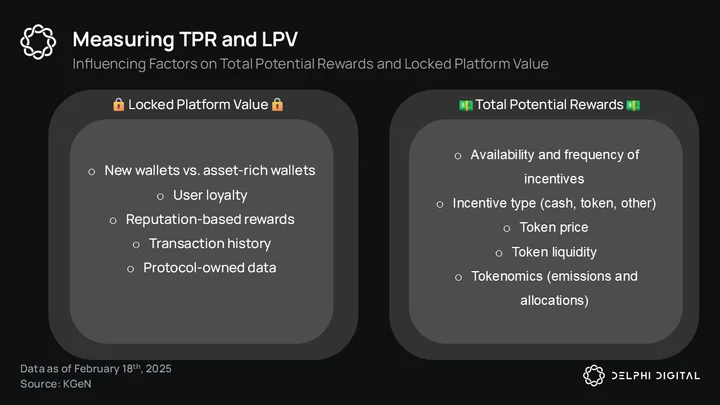

Under this assumption, and ignoring the constant narrative fluctuations throughout the Web3 attention economy, there are two primary metrics we can use to identify a Web3 questing platform’s ability to scale and retain its user base: total potential rewards (TPR) and locked platform value (LPV).

TPR is defined as the total amount of obtainable financial rewards a user can obtain over their lifetime usage of the platform. TPR is primarily dictated by considerations such as tokenomics (allocations and emissions etc.), the amount of available incentive mechanisms, the number of cash vs. token-based rewards, and the frequency of rewarded quests, etc., but it is also influenced by several extrinsic factors, such as token price and liquidity.

TPR is defined as the total amount of obtainable financial rewards a user can obtain over their lifetime usage of the platform. TPR is primarily dictated by considerations such as tokenomics (allocations and emissions etc.), the amount of available incentive mechanisms, the number of cash vs. token-based rewards, and the frequency of rewarded quests, etc., but it is also influenced by several extrinsic factors, such as token price and liquidity.

LPV relates to the extent to which the protocol “owns” its users and the perceived quality of said users. This can be impacted by the number of new wallets vs. asset-rich wallets associated with the protocol, user loyalty, use of reputation-based reward systems (this favors longer-term engaged users), on-chain vs. off-chain transaction history, and protocol-owned user data (this feeds into TPR as better user data translates into higher protocol ad-based revenue which fuels user rewards).

Regarding TPR, we can assume that over time, for as long as there is no monopoly pricing power, rewards for incentivized UA campaigns across different platforms will organically equalize over time.

For LPV, ultimately, from the advertiser’s perspective, the most value is found on the most scalable platforms (i.e. those with the greatest number of users), as well as platforms with the most amount of valuable data on those users (data depth that improves targeting and monetization).

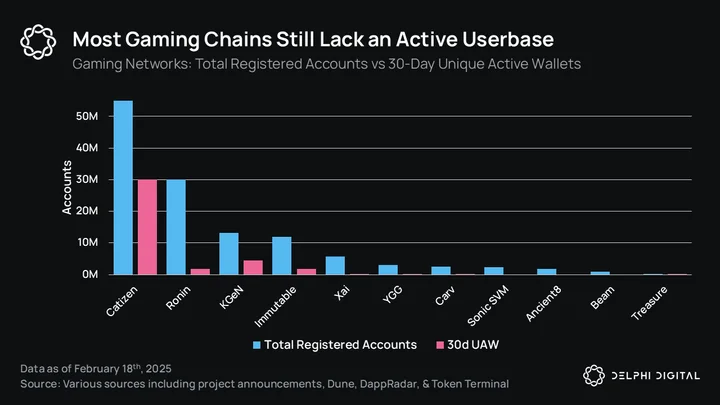

KGeN has the largest number of total registered accounts and the highest 30-day unique active wallets of any questing platform. Additionally, as we have previously stated, PoH and PoP attributes are valuable metrics that are missing in most other providers. Both of these points help KGeN stand out as a leading platform by LPV. This advantage will continue to grow provided PoC data improves.

Comps are a little less clear when it comes to TPR. One leading factor will be the number of rewarded quests at any given time and the frequency at which quests are added. A platform could leverage unsustainable token emissions to boost these metrics but for the sake of argument, we will assume rewards are in USD.

As previously stated, KGeN leads in terms of the total number of registered accounts, and MAU – both of which are key demand indicators for publishers. Additionally, due to the fact that, according to KGeN, the company has never sponsored any of the campaigns on KGeN Play, we can assume that there is equal, if not more demand from publishers for their services compared to Web3 competitors.

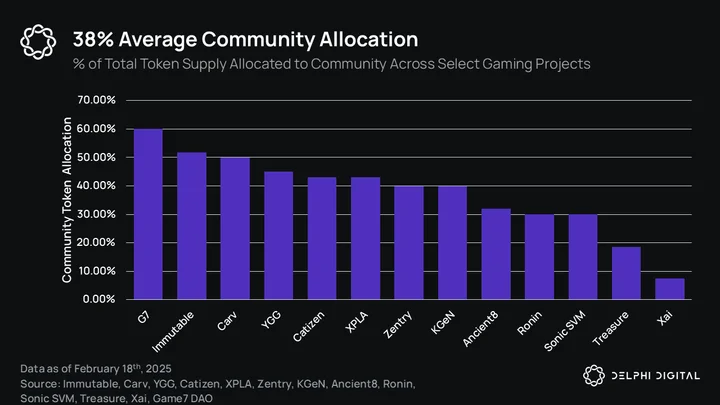

Several other considerations for TPR post-TGE will be the token price, token reward emissions, and total rewards allocation. Regarding the latter two, we can not speculate on exact reward issuance rates, but it should be noted that KGeN’s community rewards allocation falls within the upper range of reward allocations at 40%.

Regarding token price, assuming per quest rewards remain equal, the KGEN token would need to launch at no lower than a $140M market cap in order to compete with the likes of Zentry ($138M MCap) and YGG ($132M MCap). In terms of FDV, the most valuable questing platform is Carv at over $600M (although Carv appears to be transitioning away from questing into a multichain data infrastructure provider).

Regarding token price, assuming per quest rewards remain equal, the KGEN token would need to launch at no lower than a $140M market cap in order to compete with the likes of Zentry ($138M MCap) and YGG ($132M MCap). In terms of FDV, the most valuable questing platform is Carv at over $600M (although Carv appears to be transitioning away from questing into a multichain data infrastructure provider).

In order to become globally competitive in both Web3 and Web2 markets, KGeN will need to continue to scale throughout the Global South to offer partners with a total reach that is comparable to the likes of Applovin. Simultaneously, they will need to provide the same level of eCAC cost savings at this scale and prove (via PoC attributes) that these users have monetizable value.

Future Opportunities

KGeN’s core growth flywheel, albeit powerful, is driven by financial incentives at the user acquisition level. These incentives fundamentally change the motivations behind the platform’s engagement. It will be crucial that, as the network grows, KGeN can demonstrate its users are more than player liquidity.

Extrinsic motivations, such as rewards, can be fantastic growth catalysts. They can also help motivate people to acquire new skills or knowledge that may then translate into intrinsic motivations at a later date.

As such, it is recommended that, as they scale, KGeN leverages extrinsic rewards to primarily motivate users to perform tasks that they would otherwise be uninterested in performing (referrals, promotion, feedback, coaching, bug bounties, community management, etc.). It is also recommended the platform refrains from providing easily predictable ROI to users and avoids direct financial incentives in favor of in-game items or special benefits whenever possible.

Similarly, monetization will be crucial for the platform’s long-term success. By driving more commerce on-chain feeding into their PoC attributes, KGeN can create a unique dataset linking wallet activities to user behavior and demographics. This enables them to definitively demonstrate the correlation between on-chain wallet activity and user spending patterns, providing valuable insights that Web2 UA platforms aren’t equipped for currently.

Part of this will occur organically as the PoG engine grows and attracts more publishers who onboard a wider variety of SKUs to the KGeN Store. However, it can also be achieved through a combination of ambiguous rewards that encourage spending, and implementation of a payment gate for the majority of platform earnings, similar to the subscription model outlined earlier in the report. This may potentially hinder growth in the short term and lead most of the value-extractive users to churn, but the cohort that remains will be highly valuable.

A final note is regarding data. As it stands, the PoG engine provides clients with a reliable source of real users that add value as part of a game or application’s earliest golden cohort. This can be leveraged to execute a number of different types of campaigns, from esports activations to closed alpha tests and more.

However, when it comes time for these games to scale, the standard for all mobile measurement partners (MMPs) is to provide granular data points on things such as player LTV curves, attribution, and which ad networks to scale with. KGeN does not currently have a monopoly on its users but it does have the opportunity to aggregate data points across a relatively underserved market of Web3 games and gamers across the Global South.

Under the hood, all rewarded UA platforms are increasingly leveraging big data and AI to optimize campaigns and combat fraud. Recommendation engines (Mistplay), algorithmic user matching (Adjoe), and real-time optimizers (MAF) are hallmarks of this sector’s tech intensity. The sooner KGeN can create two-way user data funnels between advertisers and publishers and build out its attribution and AI tech stack, the sooner it will create a data moat that few can replicate.

Conclusion

KGeN stands out as the largest repository of gamer-specific user data in Web3 with over 270M data attributes across 13M registered accounts. The company has developed a compelling growth flywheel that provides publishers with competitively priced bottom-of-funnel eCAC while sharing more value with its users.

Additionally, KGeN’s early establishment in the Global South represents a significant first-mover advantage in markets poised for explosive growth. With an active user base of 4.4M MAU already established, they have built substantial infrastructure and community presence in regions where the gaming industry is actively growing amid stagnation in more mature markets. This positioning becomes increasingly valuable as major publishers look to expand into these emerging markets, finding in KGeN an already-established platform with deep local understanding and proven community-building capabilities.

The PoG engine is currently being leveraged to provide gamers with a composable on-chain gamer score and publishers with engaged cohorts of real users. By decentralizing this reputation system, KGeN is increasing trust factors and reducing the surface area for exploitation, subsequently increasing its robustness.

KGeN now needs to prove it can maintain its current growth forecast into and beyond its token launch, becoming the defacto UA partner throughout the Global South. Monetization is another key factor in KGeN’s future success. Improving its UA model to allow for ROAS calculations, while simultaneously building out its AI and data tooling will be important in ensuring the company remains relevant into the future.

0 Comments